GLP-1 Market Overview 2026 | Size, Share & Industry Trend 2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

GLP-1 Market Summary

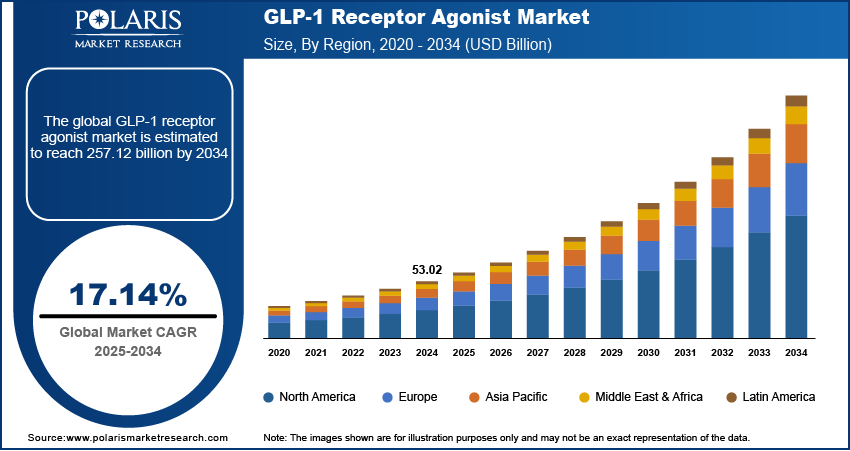

The global GLP-1 market size was valued at USD 52.82 billion in 2025, growing at a CAGR of 10.9% during 2026–2034. The growth is driven by expanding therapeutic applications beyond diabetes, such as obesity and cardiovascular diseases.

Market Statistics

Key Takeaways

- By type of GLP-1 agonist drugs, the long-acting GLP-1 agonist segment dominated in 2025. It is driven by its superior dosing convenience and sustained therapeutic efficacy.

- By route of administration, the oral GLP-1 market is expected to witness a faster growth during 2026–2034. The growth is attributed to the increasing demand for noninvasive and patient-friendly treatment options.

- Based on target indication, the obesity segment held the largest GLP-1 drugs market share in 2025. Rising clinical acceptance and expanding regulatory approvals for obesity indications fueled the segment dominance.

- By type of molecule, the biologics segment is expected to report substantial growth during the forecast period. The growth is propelled by its strong clinical performance and extended half-life properties.

- North America dominated the global revenue share in 2025. High disease prevalence and advanced healthcare infrastructure boost the leading position.

- The Asia Pacific GLP-1 industry is projected to record the highest growth rate during the forecast period. Rapid rise in lifestyle-related diseases and improving healthcare access contribute to the growth.

Industry Dynamics

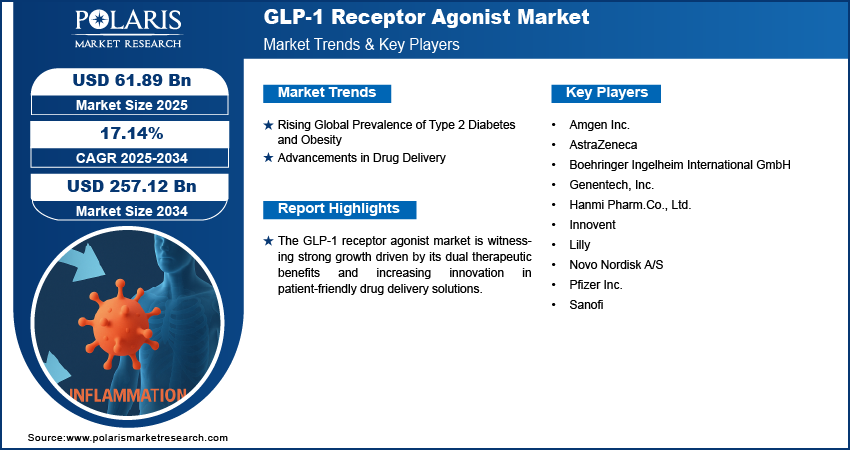

- The increasing prevalence of type-2 diabetes across the world and rising focus on innovative diabetes drug developments propel the market growth.

- Rising incidence of obesity and related conditions is driving the GLP-1 industry growth.

- Surging focus on developing personalized therapies is expected to offer lucrative opportunities in the market during the forecast period.

- Rising research and developments, and collaborations to extent the applications of GLP-1 are expected to emerge as GLP-1 market trends.

- High cost of GLP-1 drugs and affordability challenges hinder the market expansion.

To Understand More About this Research: Download Sample Report

Why GLP-1 Matters?

GLP-1 (glucagon-like peptide-1) is a hormone-based therapeutic class used to improve insulin secretion and regulate blood sugar levels. It also slows gastric emptying and reduces appetite. Thus, GLP-1 is effective for managing type 2 diabetes and obesity. The GLP-1 market growth is driven by advancements in drug formulations, particularly the development of oral and long-acting therapies. In June 2024, UBC launched under-the-tongue insulin drops with rapid absorption for diabetes treatment. These innovations are improving patient compliance and expanding treatment accessibility, especially for individuals who prefer autoinjectors options. Long-acting formulations reduce dosing frequency. It allows for better observation and convenience. Collectively, these advancements are reshaping treatment protocols and boosting the role of GLP-1 therapies in chronic disease management.

Health organizations such as the American Diabetes Association (ADA) and the European Association for the Study of Diabetes (EASD) provide clinical guidelines and recommendations. Their support promotes the use of GLP-1 analogues for specific patient populations. Furthermore, ongoing research and development activities would bring next-generation GLP-1 therapies, oral formulations, and dual incretin therapies. In addition to glycemic control, the market is increasingly being shaped by demand for obesity management and cardiometabolic risk reduction. Also, the industry is influenced by more convenient treatment pathways, including oral GLP-1 therapies and digitally enabled prescription access. ADA’s 2026 Standards are expanding the relevance of GLP-1-based therapies in diabetes, obesity, and related metabolic care. They are strengthening long-term commercial demand.

Market Drivers: Why the GLP-1 Market is Expanding Now?

Rising Prevalence of Type 2 Diabetes Globally

Consumption of highly processed food containing refined sugars and unhealthy fats is causing more people to develop type 2 diabetes. The excessive intake of sugary beverages, fast food, and snacks is directly connected to weight gain and impaired glucose metabolism. It is significantly boosting the risk of diabetes development. According to a report from the WHO, in 2022, ~830 million people worldwide had diabetes, and over 95% of diabetes cases are type 2. The International Diabetes Federation projected that the number of diabetes cases is expected to reach 643 million by 2030 and 783 million by 2045. The rising prevalence of type 2 diabetes worldwide is driving the GLP-1 development. These therapies have a central role in improving glycemic control and reducing cardiovascular risk. GLP-1 receptor agonists offer dual benefits by improving insulin secretion and suppressing glucagon release in a glucose-dependent manner. This functioning aligns well with current clinical management needs. Their ability to address early-stage and progressive disease stages reinforces their importance in diabetes care. Thus, the expanding type 2 diabetes market is driving the demand for GLP-1 drugs.

Increasing Rates of Obesity and Related Metabolic Disorders

Various countries are reporting the growth for the obesity treatment market. GLP-1 receptor agonists have shown effectiveness in promoting weight loss and improving metabolic parameters. Obesity is a major risk factor for type 2 diabetes, cardiovascular diseases, and other comorbidities, creating a pressing need for therapeutic solutions that manage multiple conditions simultaneously. According to a May 2025 WHO report, 2.5 billion adults worldwide were overweight in 2022, including 890 million having obesity. GLP-1 therapies help regulate appetite and food intake and also support sustainable weight management. The utility of GLP-1 receptor agonists continues to expand as healthcare providers and patients seek holistic treatments for complex metabolic syndromes, strengthening their position in modern therapeutic regimens. Therefore, the increasing rates of obesity and related metabolic disorders are fueling the GLP-1 receptor agonist market growth.

Market Opportunities

The rise in partnerships, product launches, and an increasing focus on personalized medicine will created lucrative opportunities. Leading pharmaceutical companies collaborate to improve R&D efficiency, speed up regulatory approvals, and bring new therapies to market more quickly. In May 2025, CheqUp, based in the UK, and WeightWatchers teamed up to offer clinical GLP-1 medication support along with behavioral lifestyle programs. This partnership will provide integrated weight management solutions. The goal is to improve patient outcomes through a mix of medical and behavioral methods. Together, they aim to introduce new products tailored to individual patient needs, showing the industry's focus on targeted treatment approaches. Combining genetic insights and digital tools into care delivery is further improving therapeutic results. This supports the value of GLP-1 receptor agonists in personalized healthcare strategies.

GLP-1 Analogues Market Trends

Rising Geriatric Population

Older adult are highly prone to type 2 diabetes and related health conditions due to age-related factors. According to the UN, the global population of individuals aged 65 years and above is expected to increase from 761 million in 2021 to 1.6 billion by 2050. The demographic of people aged 80 years and above is growing at a faster rate. Geriatric population increasingly require therapies that offer glycemic control, weight reduction benefits, and broader cardiometabolic support. ADA guidance also notes benefits of GLP-1 RAs in diabetes patients who also have cardiovascular disease, chronic kidney disease, or obesity-linked complications. Therefore, rising geriatric population is expected to drive the GLP-1 receptor agonist market during the forecast period.

Segmental Insights

By Type of GLP-1 Agonist Drugs Analysis

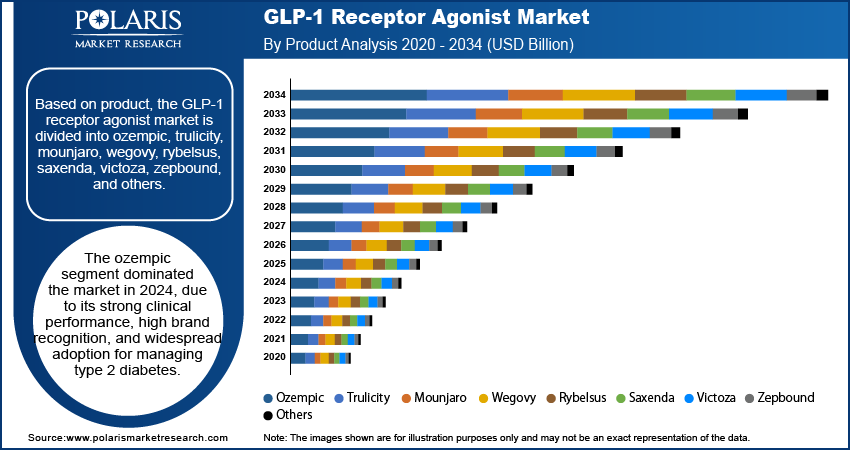

The segmentation, based on type of GLP-1 agonist drugs, includes long-acting GLP-1 agonist and short-acting GLP-1 agonist. The long-acting GLP-1 agonist segment dominated the market in 2025 owing to its superior dosing convenience, improved patient observation, and sustained therapeutic efficacy. These formlulations require less frequent administration, often once weekly. It reduces the treatment burden and improves long-term compliance. This type of GLP-1 agonists provides extended glycemic control and cardiovascular benefits. Thus, they are becoming a preferred choice among healthcare providers. Their clinical advantage in managing type 2 diabetes and obesity has positioned them strongly in treatment guidelines. These factors are contributing to their dominant share in the global sector.

By Route of Administration Analysis

Based on route of administration, the segmentation includes oral and parenteral. The oral segment is expected to witness a faster growth during the forecast period. Rising demand for noninvasive and patient-friendly treatment options boosts the growth. Oral GLP-1 therapies eliminate the need for injections. Improved drug delivery technologies allow the development of effective oral formulations with comparable efficacy to injectable counterparts. This growing shift toward oral therapies is expected to expand market reach and improve access, especially in primary care settings. The preference for oral GLP-1 drugs will be high in populations with injection-related hesitations.

By Target Indication Analysis

The segmentation, based on target indication, includes Alzheimer’s disease, non-alcoholic steatohepatitis, obesity, sleep apnea, and type 2 diabetes. The obesity segment held the largest market share in 2025. GLP-1 receptor agonists have shown great success in supporting weight loss and controlling appetite. Obesity is a major risk factor for many chronic conditions like type 2 diabetes and cardiovascular diseases. GLP-1 obesity drugs provide a twofold benefit. They address both metabolic issues and excess body weight. Thus, they are ideal for long-term weight management. Growing clinical acceptance of GLP-1 drugs boosts the segment growth. Also, expanding regulatory approvals for obesity indications have reinforced this segment’s dominance.

By Type of Molecule Analysis

By type of molecule, the segmentation includes biologics and small molecules. The biologics segment is likely to grow significantly during the forecast period. The growth is attributed to its strong clinical performance, precise targeting, and long half-life properties. Biologic GLP-1 receptor agonists are produced using recombinant technology. They have proven highly effective for managing blood sugar levels and helping with weight loss. These agents act more specifically, which lowers side effects and improves patient outcomes. With ongoing advancements in biologic drug development and more investment in biopharmaceutical pipelines, this sector is expected to grow in the future.

Regional Analysis

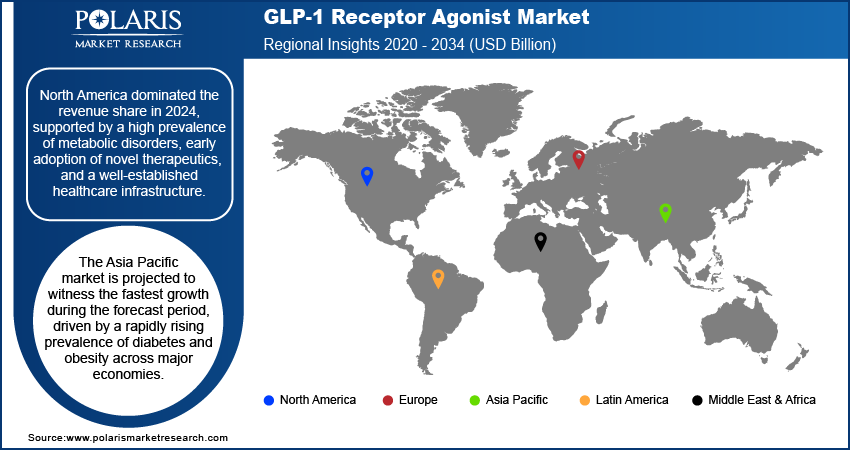

The report provides market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America dominated the global revenue share in 2025. High disease prevalence and advanced healthcare infrastructure propel the North America GLP-1 market growth. According to May 2024 CDC data, diabetes affects 11.6% of the U.S. population (38.4 million), with 38% of adults (97.6 million) having prediabetes. Strong presence of major pharmaceutical companies and early adoption of novel therapies and favorable reimbursement policies boost the regional market growth. Also, widespread awareness among both clinicians and patients drives the expansion. Also, early adoption of novel therapies contributed to the dominance.

The U.S. GLP-1 market held the largest share in North America. It is due to its strong healthcare infrastructure and high awareness among healthcare providers and patients. The market benefits from the early adoption of new therapies and broad insurance coverage. Established clinical guidelines positively influence the market. These factors support GLP-1 use in diabetes and obesity treatment. Growing focus on personalized medicine and preventive care dries widespread acceptance of GLP-1 receptor agonists in various care settings.

The Asia Pacific GLP-1 market is projected to witness the fastest growth during the forecast period, owing to the rapid rise in lifestyle-related diseases and improving healthcare access. According to the November 2024 report, ICMR's 2023 study stated that India has 101 million diabetes cases. Increasing awareness of diabetes and obesity treatments propels demand for effective treatments, such as GLP-1 receptor agonists. Also, expanding urban populations and healthcare reforms drives the regional market growth, Growing pharmaceutical investments and efforts to integrate advanced therapeutics into public health programs bolster the market expansion. Improved affordability and local production initiatives accelerate GLP-1 drugs adoption in the region.

The China GLP-1 market is experiencing growth supported by a rising prevalence of metabolic disorders and increasing investments in healthcare modernization. Government initiatives to improve chronic disease management and expand access to innovative treatments are accelerating demand for effective therapies such as GLP-1 receptor agonists.

The Europe GLP-1 market is projected to record substantial growth during the forecast period. Strong regulatory framework and structured disease management programs boost the growth. Also, rising incidence of metabolic disorders also drive the regional market expansion. Healthcare systems in the region are increasingly prioritizing preventive and personalized care. It boosts the demand for GLP-1 receptor agonists. Public health initiatives, favorable reimbursement schemes, and widespread clinical research support market potential. Countries backed by high healthcare expenditure, increasing awareness of obesity, and sustained efforts in clinical adoption of advanced therapies contribute to the expansion.

The UK GLP-1 market has emerged as a major sector due to its well-structured public healthcare system, strong clinical focus on chronic disease control, and evidence-based prescribing. The integration of GLP-1 therapies into national treatment guidelines for type 2 diabetes and obesity supports their broad adoption.

Key Players & Competitive Analysis Report

The GLP-1 sector is witnesses competition due to revenue growth opportunities in both developed and emerging markets. A few key players are AstraZeneca, Boehringer Ingelheim, D&D Pharmatech, Eli Lilly, Hanmi Pharmaceutical, Novo Nordisk, Pfizer, Roche, Sanofi, and Tonghua Dongbao Pharmaceutical.

Major players like Novo Nordisk, Eli Lilly, and AstraZeneca are making strategic investments. This helps them expand their product lines, especially in obesity and type 2 diabetes. Innovations, such as oral formulations and dual-target agonists, are reshaping competitive positioning. Patent expiries are creating opportunities for generics. Economic and geopolitical changes, including pricing pressures and regulatory policies, are affecting vendor strategies and driving partnerships. Sustainable value chains and pricing insights are becoming key factors as payers focus on cost-effectiveness.

GLP-1 Market Key Players

- AstraZeneca

- Boehringer Ingelheim

- D&D Pharmatech

- Eli Lilly

- Hanmi Pharmaceutical

- Novo Nordisk

- Pfizer

- Roche

- Sanofi

- Tonghua Dongbao Pharmaceutical

GLP-1 Pipeline Phases

The GLP-1 agonists industry is evolving with key players advancing candidates through clinical stages for obesity, diabetes, and cardiometabolic indications. The following table summarizes pipeline timelines and phases for the specified companies as of March 2026.

| Company | Key GLP-1 Drug(s) | Current Phase | Indiacation |

| AstraZeneca | Elecoglipron (oral GLP-1RA) | Phase 2 |

|

| Boehringer Ingelheim | Survodutide (GLP-1/glucagon) | Phase 3 |

|

| D&D Pharmatech | DD01 (GLP-1/glucagon dual) | Phase 2 |

|

| Pegsebrenatide | Phase 2 Completed |

| |

| Eli Lilly | Orforglipron | Phase 3 |

|

| Hanmi Pharmaceutical | Efpeglenatide | Phase 3 |

|

| Novo Nordisk | CagriSema | Phase 3 |

|

| Pfizer | PF-3944; MET-097i | Phase 2b |

|

| Roche | CT-388 (GLP-1/GIP dual) | Phase 2 complete |

|

| Tonghua Dongbao | THDBH120 (GLP-1/GIP dual) | Phase 1b complete |

|

Industry Developments

February 2025: Biocon launched its GLP-1 peptide liraglutide in the UK under two brand names: Liraglutide Biocon (for diabetes, similar to Victoza) and Biolide (for chronic weight management, similar to Saxenda).

May 2025: Illumina and Ovation.io developed a clinical multiomic dataset from 25,000 GLP-1 therapy patients to support drug discovery. The dataset will be available to pharmaceutical researchers for advancing therapeutic development.

GLP-1 Market Segmentation

By Type of Molecule Outlook (Revenue, USD Billion, 2021–2034)

- Biologics

- Small Molecules

By Active Compound Used Outlook (Revenue, USD Billion, 2021–2034)

- Dulaglutide

- Liraglutide

- Orforglipron

- Retatrutide

- Semaglutide

- Survodutide

- Tirzepatide

- Other Active Compounds

By Type of GLP-1 Agonist Drugs Outlook (Revenue, USD Billion, 2021–2034)

- Long-acting GLP-1 Agonist

- Short-acting GLP-1 Agonist

By Route of Administration Outlook (Revenue, USD Billion, 2021–2034)

- Oral

- Parenteral

By Target Indication Outlook (Revenue, USD Billion, 2021–2034)

- Alzheimer’s Disease

- Non-Alcoholic Steatohepatitis

- Obesity

- Sleep Apnea

- Type 2 Diabetes

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

GLP-1 Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 52.82 billion |

| Market Size in 2026 | USD 58.48 billion |

| Revenue Forecast in 2034 | USD 133.92 billion |

| CAGR | 10.9% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The GLP-1 market was valued at USD 52.82 billion in 2025 and is projected to reach USD 133.92 billion by 2034. IT is expected to register a CAGR of 10.9% during 2026–2034.

Originally approved for diabetes, GLP-1 drugs are positively used in the management of weight loss, cardiovascular risk, fatty liver disease, and neurodegenerative conditions.

Key players driving the GLP-1 market include Novo Nordisk, Eli Lilly, Pfizer, AstraZeneca, Roche, Sanofi, Boehringer Ingelheim, and Tonghua Dongbao Pharmaceutical.

Surging prevalence of type 2 diabetes and growing GLP-1 drug applications are fueling the market growth.

A GLP-1 drug shortage has persisted since late 2022. It prompted major manufacturers to significantly expand global production and manufacturing capacities.

A few risks in the market are safety concerns and side effects, and strict regulatory scrutiny. Also, high treatment costs, supply constraints, and increasing competition from new obesity and diabetes therapies hinder the market.

Regulatory restrictions on compounded GLP-1 drugs limit unapproved alternatives, strengthening demand for branded products. They ensure safety standards and improve revenue prospects for approved pharmaceutical manufacturers.

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research & Consulting, Inc. uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

1. Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

2. Data Collection

We gather information from both public and verified sources:

3. Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

| Region | Segment | VolumeUnits | Avg PriceUSD | RevenueUSD Mn | Share % |

|---|---|---|---|---|---|

| North America | Product A | 250 | 2.5 | 500 | 15% |

| Product A | XX | XX | XX | XX | |

| Product A | XX | XX | XX | XX | |

| Consistent methodology applied across regions | |||||

4. Market Estimation

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Forecasting

Step 6:

At Polaris Market Research & Consulting, Inc., we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Validation & Triangulation

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Triangulation Framework

Estimates are cross-verified across three sources:

Company-level data

• Primary inputs from industry participants

• Secondary benchmarks and published data

Variance maintained within +5-10%

Adjustments applied to align estimates

Segment values validated against overall market structure

Data Consistency & Integrity

Segment totals validated to 100%

Regional estimates aligned with global market size

Historical trends compared against forecast outputs

Assumptions reviewed for cross-segment and regional alignment

Final Outputs

Deliverables

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements

Download Sample Report of GLP-1 Market

Please fill out the form to request a customized copy of the research report.