Obesity Treatment Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Obesity Treatment Market Summary

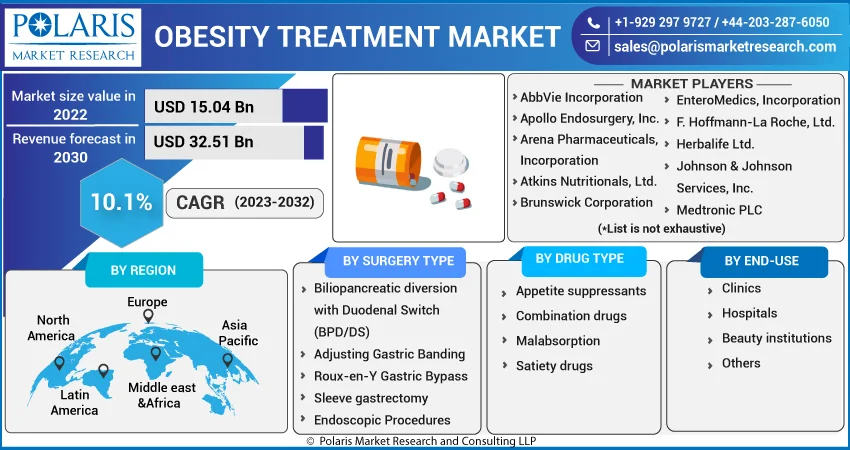

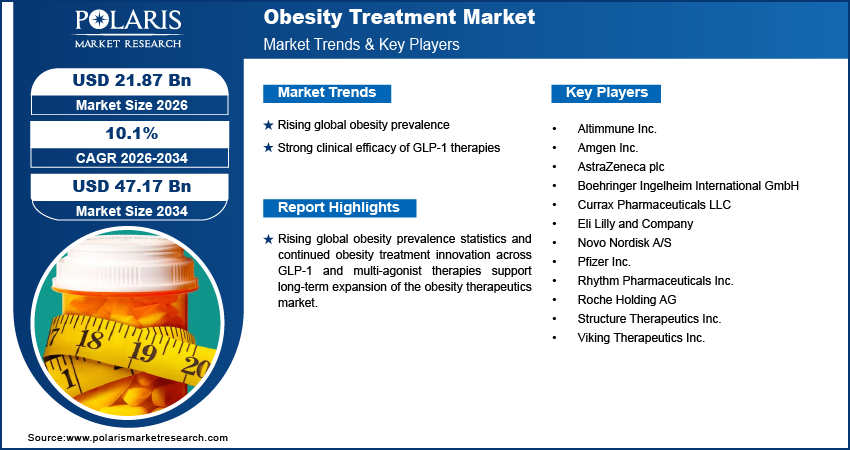

The global obesity treatment market is estimated around USD 19.90 billion in 2025, with consistent growth anticipated during 2026–2034. Growth is driven by rising obesity prevalence and rapid GLP-1 adoption. The market is projected to grow at a CAGR of 10.1% during the forecast period.

Market Statistics

Key Takeaways

- North America accounted for the largest regional share of around 42.6% in 2025, driven by high obesity prevalence, rapid GLP-1 adoption, advanced clinical infrastructure, and favorable reimbursement frameworks.

- By Treatment Type, Pharmacotherapy segment accounted for the largest share of approximately 64.8% in 2025, supported by strong clinical efficacy, reimbursement coverage, and recurring long-term prescription cycles.

- By Drug Class, GLP-1 Receptor Agonists segment accounted for the largest share of around 58.9% in 2025, driven by superior weight loss outcomes, cardiometabolic benefits, and widespread adoption of semaglutide-based therapies.

- By Route of Administration, Injectable segment accounted for the largest share of nearly 61.3% in 2025, supported by strong clinical outcomes, specialist-led prescriptions, and improved long-term treatment adherence.

- By Distribution Channel, Hospital Pharmacies segment is projected to grow at a CAGR of 6.1%, driven by institutional biologic dispensing and integration with comprehensive obesity management programs.

Industry Dynamics

- Rising global obesity prevalence expands the treatment population.

- Strong GLP-1 efficacy drives growth in the anti-obesity drugs market.

- High gene therapy cost and limited reimbursement restrict access.

- Oral pipeline expansion and digital care models create long term opportunities.

What Is the Obesity Treatment Market?

Obesity treatment refers to the structured medical and clinical management of obesity through pharmacotherapy, bariatric surgery, medical devices, behavioral therapy, and digital therapeutics. This scope defines the obesity therapeutics market, which focuses on clinically approved interventions for patients with a body mass index above defined threshold. Obesity treatment differs from general weight management, which includes lifestyle and fitness programs for non-clinical weight control. The weight loss treatment industry therefore centers on disease-focused care rather than cosmetic or short-term weight reduction solutions.

The market for obesity therapeutics is governed by strict clinical guidelines and regulatory approvals. This is due to anti-obesity medications need to undergo rigorous testing for cardiovascular and metabolic effects before being marketed. Bariatric surgery and implantable devices are governed by surgical and medical device regulations in principal countries like the US and Europe. Reimbursement policies, treatment practices, and post-marketing surveillance govern the global market for obesity management.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The weight loss treatment market is growing in a structured way due to the increasing number of obese people and the prevalence of chronic diseases such as diabetes and cardiovascular diseases. The anti-obesity drug market is growing at a rapid pace owing to the advancements in GLP-1 and combination therapies. The demand for bariatric surgeries and digital therapy platforms is increasing in developed healthcare systems. This structured clinical environment makes the global obesity management market a healthcare sector rather than a lifestyle market.

Drivers & Opportunities

Rising global obesity prevalence: The rising statistics of obesity prevalence continues to increase the eligible patient pool for treatment in the developed as well as emerging regions. According to WHO statistics, in 2022, 43% of the global adult population was overweight, and 16% of this population had obesity (2.5 billion people were overweight, and 890 billion people had obesity), and 37 billion children under 5 years and 390 billion children aged 5-19 years were overweight. Rising cases of obesity-related diseases like type 2 diabetes and cardiovascular diseases continue to fuel the demand for organized medical treatment, thus forming a major driving force for the obesity treatment market.

Strong clinical efficacy of GLP-1 therapies: Far superior weight loss efficacy and cardiometabolic effects have placed GLP-1 receptor agonists at the forefront of prescription growth. Clinical trials have shown average weight loss of between 10% and 20%, which is higher than traditional anti-obesity medications. Such efficacy supports rapid growth in the GLP-1 obesity drug market, with high growth seen in the semaglutide market size and tirzepatide obesity market. Physician preference for evidence-based pharmacotherapy continues to drive growth in the anti-obesity drugs market.

Restraints & Challenges

High annual therapy cost: The premium pricing of the branded GLP-1 products also hinders their affordability in the uninsured and underinsured patient population. The annual treatment cost in the US also tends to surpass several thousand dollars per patient, thus hindering patient access in the absence of widespread reimbursement for anti-obesity medications. The limitations imposed by the payers and prior authorization also moderate patient conversion rates.

Opportunity

Integration of AI-enabled care platforms: Integration of AI-powered monitoring systems and digital therapeutics enhances patient compliance and behavioral change. In August 2025, the FDA approved Signos' CGM system for weight loss, which includes a wearable device, mobile-based coaching, and integration with GLP-1 medications, making it the first FDA-approved indication for weight loss. Additionally, organized digital follow-through improves sustained weight loss and discontinuation rates, which are high in pharmacologic therapy. Real-world data collected through these platforms helps in discussions for outcomes-based reimbursement.

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the obesity treatment market by treatment type, drug class, route of administration and distribution channel to help readers identify the fastest expanding and most attractive demand segments.

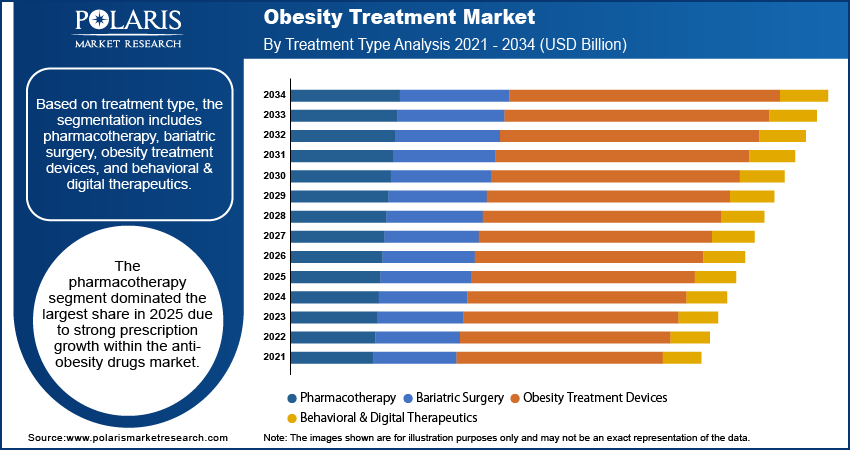

By Treatment Type

-

Pharmacotherapy

Pharmacotherapy has registered the largest revenue share in 2025 in the anti-obesity drugs market, driven by the swift adoption of GLP-1-based therapies. The potent clinical efficacy and risk reduction in cardiometabolic parameters enhance physician confidence in long-term prescription. The growing reimbursement support enhances patient accessibility in the developed market. The regular prescription cycle enhances long-term revenue visibility in the obesity therapeutics market.

-

Behavioral & Digital Therapeutics

Behavioral and digital platforms are anticipated to register the fastest growth rate, driven by the swift adoption of AI-based monitoring and telemedicine platforms. The intensifying focus on adherence and long-term weight management enhances the adoption rate. Employers and payers are integrating digital platforms into chronic disease management pathways. This development enhances scalable growth in the behavioral therapy obesity market.

By Drug Class

-

GLP-1 Receptor Agonists

GLP-1 receptor agonists led the GLP-1 receptor agonist market in 2025 due to its superior weight loss efficacy and favorable cardiometabolic effects. Injectable anti-obesity drugs in this category show robust clinical efficacy and widespread adoption. Increasing semaglutide use further reinforces revenue concentration in the anti-obesity drugs market. Established safety profiles underpin long-term strategic alignment.

-

Dual/Triple Agonists

Dual and triple pathway therapies are expected to register the fastest growth rate among multi-agonist anti-obesity drugs owing to its improved efficacy profiles. Progress in next-generation anti-obesity biologics further reinforces competitive differentiation. Favorable results from late-stage clinical trials underpin accelerated pipeline growth. This category is poised for high-impact growth in the anti-obesity drugs market.

By Route of Administration

-

Injectable Therapies

Injectable weight management medications had the largest market share in 2025, led by established GLP-1 franchises and strong clinical profiles. Dosing and established long-term efficacy support sustained market share. This route remains central to the injectable obesity therapeutics segment.

-

Oral Therapies

Oral therapies are anticipated to register the fastest growth in the oral obesity drugs market due to improved patient convenience and primary care adoption. Advancements often referred to as the year of oral GLP-1 are expanding treatment accessibility. Greater acceptance could lower barriers to entry. This trend will help drive long-term growth outside of injectable therapies.

By Distribution Channel

-

Hospital Pharmacies

Hospital pharmacy obesity medications had the largest market share in 2025, led by prescriptions from specialists and alignment with comprehensive obesity management. Institutional purchasing supports high-value biologic dispensing. This channel remains dominant within obesity drug distribution channels.

-

Online Pharmacies

Prescriptions for online weight management are expected to register the highest growth rate, driven by the development of telemedicine and online prescription services. Direct-to-consumer distribution enhances convenience and refill compliance. Technology integration facilitates scalable distribution. This channel strengthens growth across modern obesity drug distribution channels.

Source: Polaris Market Research Analysis

Regional Analysis

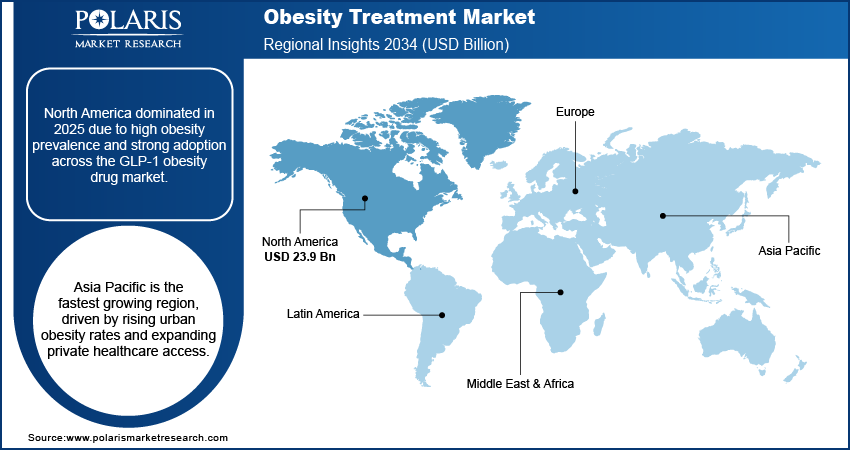

North America Market Assessment

North America obesity therapeutics market dominated in 2025, driven by high obesity prevalence and rapid adoption of GLP-1 based pharmacotherapy across the US and Canada. CDC reports indicate adult obesity rates at 35% or higher in 43 states for ages 40 to 59, 6 states for ages 18 to 39, and 4 states for those 60 and older. National average stands around 40%, peaking at 46% in middle age, with severe obesity affecting 9.4% of adults, particularly women. Additionally, strong clinical infrastructure and specialist-led care pathways strengthen revenue concentration across the anti-obesity drugs market.

Asia Pacific Obesity Treatment Market Insights

Asia Pacific obesity therapeutics market is expanding at the fastest pace due to urbanization and increasing metabolic disorder incidence in China, India, Japan, and South Korea. United Nations Human Settlements Programme stated that Asia's urban population exceeds 2.2 billion (54% of global total), projected to grow by 50% or 1.2 billion more by 2050. Over 60% of the region's people will live in cities by 2030. Obesity prevalence in urban populations continues to rise, expanding the addressable patient base. Moreover, growing private healthcare expenditure and digital health adoption improve access to pharmacotherapy and digital obesity management programs.

Europe Obesity Treatment Market Overview

Europe held the second largest share in obesity treatment market, owing to rising obesity prevalence and structured chronic disease management programs. According to EFPIA statistics, the prevalence of obesity in the EU increases with age, reaching 20% among 65-74-year-old individuals and 15% among 18-64-year-old individuals in 2022. In 2030, more than 30% of Europeans could be affected by obesity, which could cost healthcare systems up to USD 1,720 billion if left unaddressed. In addition, a steady expansion of coverage in Germany, the UK, and France enhances access to GLP-1 treatments.

Heat Map Analysis

| Region | Market Position | Growth Momentum | Regulatory Strength | Reimbursement Landscape | Clinical Adoption |

| North America | High | Moderate to High | High | High | High |

| Europe | Moderate | Moderate | High | Moderate | High |

| Asia Pacific | Moderate | High | Moderate | Developing to Moderate | Moderate |

| Latin America | Low to Moderate | Moderate | Moderate | Developing | Low to Moderate |

| Middle East & Africa | Low | Moderate | Low to Moderate | Limited | Low |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The obesity treatment industry has a concentrated competitive structure, with a limited number of multinational pharmaceutical companies controlling the majority share of the anti-obesity drugs market. Competitive intensity is shaped by clinical efficacy data, cardiovascular outcome evidence, and scale within the GLP-1 obesity drug market. Companies focus on expanding manufacturing capacity, strengthening payer negotiations, and advancing lifecycle management strategies to protect market position. Firms also invest in obesity treatment innovation across the obesity drug pipeline, including multi-agonists and oral formulations, to secure long-term differentiation.

Key players in the obesity treatment industry include Novo Nordisk A/S, Eli Lilly and Company, Pfizer Inc., Roche Holding AG, Amgen Inc., AstraZeneca plc, Boehringer Ingelheim International GmbH, Viking Therapeutics Inc., Structure Therapeutics Inc., Altimmune Inc., Rhythm Pharmaceuticals Inc., Currax Pharmaceuticals LLC, and others.

Future Outlook & Investment Landscape

Reimbursement & Pricing Evolution

Obesity treatment reimbursement trends are shifting toward broader payer inclusion as obesity gains recognition as a chronic disease. Ongoing obesity drug pricing analysis indicates pressure from payers to link coverage with long-term cardiometabolic outcomes. Patent expirations expected in the next decade may introduce biosimilar competition and moderate pricing levels. These dynamics create structured obesity treatment market investment opportunities tied to volume expansion and lifecycle management strategies.

Long-Term Sustainability of GLP-1 Market

Sustainability of the GLP-1 segment depends on adherence, lifetime therapy economics, and continued real world evidence generation. High discontinuation rates impact long-term revenue realization, even with high initial adoption rates. Firms are improving the commercialization models for obesity therapeutics by using outcome-based contracts and digital adherence programs. Use of AI in obesity treatment market platforms and telehealth ecosystems helps in patient monitoring and treatment engagement.

Key Players

- Altimmune Inc.

- Amgen Inc.

- AstraZeneca plc

- Boehringer Ingelheim International GmbH

- Currax Pharmaceuticals LLC

- Eli Lilly and Company

- Novo Nordisk A/S

- Pfizer Inc.

- Rhythm Pharmaceuticals Inc.

- Roche Holding AG

- Structure Therapeutics Inc.

- Viking Therapeutics Inc.

Industry Developments

- February 2026: Eli Lilly launched a new Zepbound obesity drug pen delivering one month of doses in a single multi-dose KwikPen device, available starting February 23, 2026, via LillyDirect for self-pay patients at $299 monthly for the starter dose.

- February 2026: Novo Nordisk partnered with Boston startup Vivtex, a spinout from MIT scientists to develop oral alternatives to injectable GLP-1 drugs for obesity and diabetes, intensifying rivalry with Eli Lilly in the weight loss market.

- January 2026: AstraZeneca entered a licensing deal with China's CSPC Pharmaceutical Group to develop and commercialize CSPC's oral GLP-1 receptor agonist for obesity and type 2 diabetes globally.

Obesity Treatment Market Segmentation

By Treatment Type Outlook (Revenue, USD Billion, 2021-2034)

- Pharmacotherapy

- Bariatric Surgery

- Obesity Treatment Devices

- Behavioral & Digital Therapeutics

By Drug Class Outlook (Revenue, USD Billion, 2021-2034)

- GLP-1 Receptor Agonists

- Dual/Triple Agonists

- Combination Therapies

By Route of Administration Outlook (Revenue, USD Billion, 2021-2034)

- Injectable Therapies

- Oral Therapies

By Distribution Channel Outlook (Revenue, USD Billion, 2021-2034)

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Obesity Treatment Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 19.90 Billion |

| Market Size in 2026 | USD 21.87 Billion |

| Revenue Forecast by 2034 | USD 47.17 Billion |

| CAGR | 10.1% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Obesity Treatment Market FAQ's

North America dominates due to high obesity prevalence, rapid GLP-1 adoption, and expanding reimbursement for obesity drugs.

The global market size was valued at USD 19.90 billion in 2025 and is projected to grow to USD 47.17 billion by 2034.

Major categories include pharmacotherapy within the anti-obesity drugs market, bariatric surgery, obesity treatment devices such as gastric balloons, and behavioral and digital therapeutics programs.

A few of the key players in the market are Novo Nordisk A/S, Eli Lilly and Company, Pfizer Inc., Roche Holding AG, Amgen Inc., AstraZeneca plc, Boehringer Ingelheim International GmbH, Viking Therapeutics Inc., Structure Therapeutics Inc., Altimmune Inc., Rhythm Pharmaceuticals Inc., Currax Pharmaceuticals LLC, and others.

Growth is driven by rising global obesity prevalence statistics and strong clinical efficacy observed in the GLP-1 obesity drug market.

Download Sample Report of Obesity Treatment Market

Please fill out the form to request a customized copy of the research report.