Industrial Control Systems (ICS) Security Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Industrial Control Systems (ICS) Security Market Summary

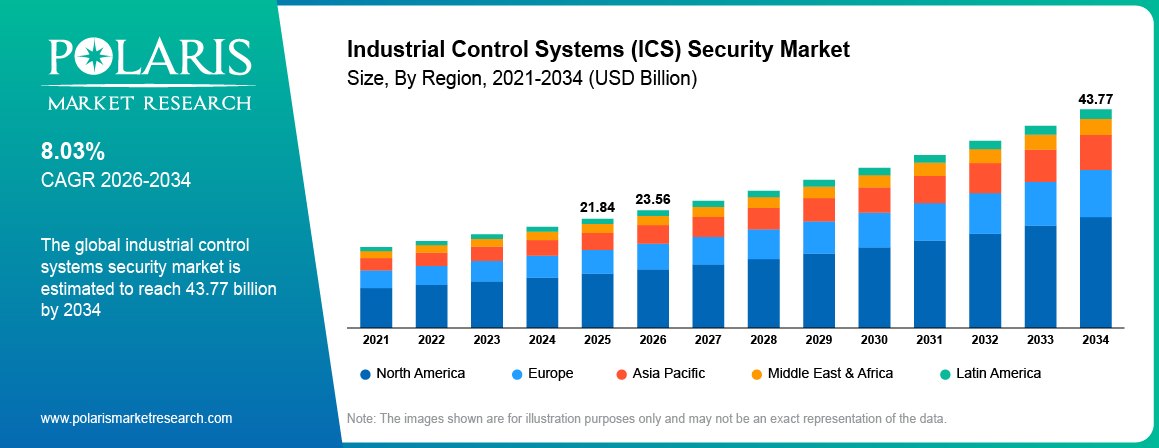

The global industrial control systems (ICS) security market size was valued at USD 21.84 billion in 2025, growing at a CAGR of 8.03% from 2026–2034. Key factors driving demand include strict government regulations and compliance mandates and increasing cyberattacks on critical infrastructure.

Market Statistics

Key Takeaways

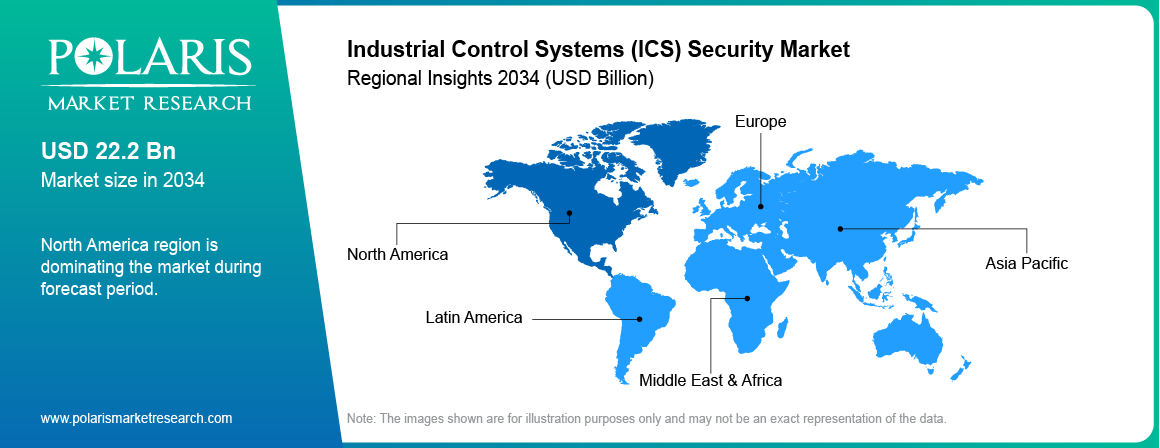

- North America led the global market in 2025, holding a 38.0% revenue share due to the availability of refined industrial infrastructure and early adoption of digital technologies.

- The industrial control systems (ICS) security landscape in Asia Pacific is projected to witness the fastest growth during the forecast period at a CAGR of 9.3%. This is driven by the industrialization and increasing use of digital manufacturing technologies.

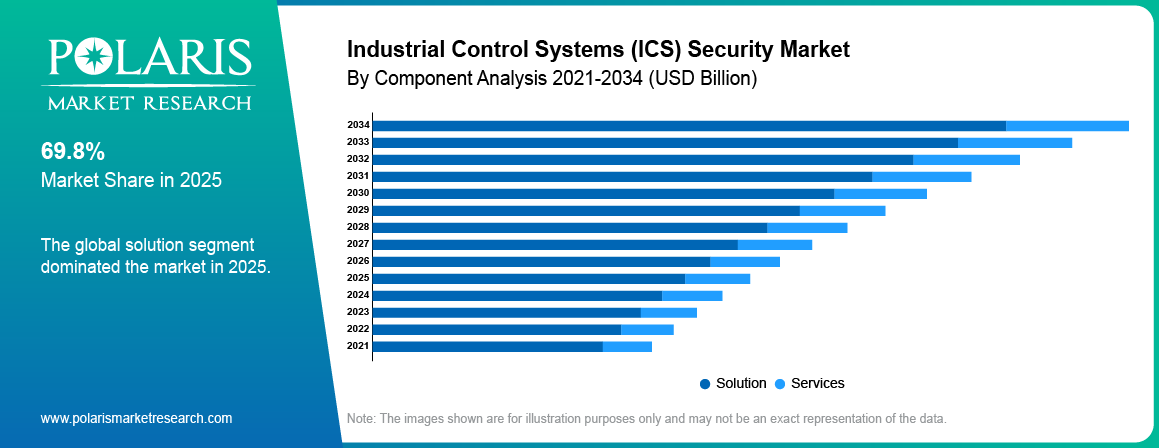

- Based on component, the solution segment accounted for 69.8% revenue share in 2025 driven by increasing demand for sophisticated cyber security solutions.

- Based on solution, the encryption segment is expected to witness substantial growth during the forecast period at a CAGR of 8.5% due to the environments are increasingly reliant on the sharing of operational data.

- Based on security type, the network segment dominated the market accounting for USD 8.68 billion in 2025 as they are the means of communications among programmable logic controllers, supervisory control systems, sensors, and enterprise applications.

Note- Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Strict government regulations and compliance mandates is driving the market growth

- Increasing cyberattacks on critical infrastructure is driven by critical infrastructure which is becoming more digitized and interconnected.

- Securing legacy ICS assets not built with native security features create challenges.

- IT/OT convergence enabling AI-driven real-time threat detection and response provides an opportunity to expand.

What Does Industrial Control Systems (ICS) Security Market Includes?

The industrial control systems (ICS) security is a subset of cybersecurity that focuses on applying security controls to protect industrial control systems (ICS) such as SCADA, DCS, and PLC from cyberattacks and other threats to operational stability. Growing convergence of IT and OT networks has created new challenges in securing industrial environments. Operational technology (OT) security systems were traditionally air-gapped from the enterprise network, but digital convergence is bringing industrial assets on to the enterprise IT infrastructure, cloud platforms, and remote monitoring systems. This interconnection offers more visibility and efficiency of activity, but also exposes critical infrastructure to vulnerabilities traditionally associated with an IT environment. According to an April 2026, report from the U.S. EPA, for FY 2027, the EPA will invest USD 19.1 million and 12.3 full-time equivalents (FTE) in information security efforts, in which USD 9.6 million and 1.5 FTE are related to new activities. Therefore, energy producers, manufacturers and utilities are putting ICS security frameworks at the top of their agenda to keep the lights on and avoid cyber incidents that could cause interruptions in production or compromise highly-sensitive operational data.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

Furthermore, the role of ICS security for the industry 4.0 modernization plays an important role for protecting legacy infrastructures as organizations transition into Industry 4.0 and Industrial Internet of Things (IIoT), ICS Security within the increasingly digitalized industrial operations. In July 2024, Maryland MEP, RMI, and the Maryland Department of Commerce introduced the Maryland Manufacturing 4.0 Grant Program offering small manufacturers 75% of the costs and mid-sized manufacturers 50%. Allowable projects were big data & analytics, robots/autonomous equipment, IIoT implementation and more. Many industrial facilities still use control systems that are decades old and were not designed with cybersecurity in mind, which are facing issues. The convergence of smart factories, automated production lines, and sensor-based industrial networks is expected to bring about the convergence of communication protocols, connected devices, and real-time data analytics platforms. These technologies enhance productivity and provide greater operational intelligence. They also open up even more cyber vulnerabilities throughout industrial environments. As a result, enterprises are seeking ICS security solutions that can protect the modernized industrial ecosystem and enable safe and resilient operational performance through network monitoring, intrusion detection, asset visibility, and threat management.

Drivers & Opportunities

What are the Factors Driving the Market Growth?

Strict Government Regulations and Compliance Mandates: This is due to the importance of safeguarding critical infrastructure against cyber-attacks which is gaining recognition among regulators worldwide. Energy, utilities, manufacturing, transportation and water management are all essential to national security and economic stability, and as such they have been a focus of regulatory attention in the industrial sector. Governments and regulators are also introducing tighter cybersecurity mandates for the protection of OT networks and industrial control systems environments. In 2023, the Government of Canada funded USD 2.5 million for three years, in collaboration with Public Services and Procurement Canada and National Defense for the Canada Program for Cyber Security Certification (CPCSC). The regulations also establish cybersecurity requirements defense contractors must meet to secure sensitive information and be able to share work with allies. These tend to more focus toward continuous monitoring, access control, vulnerability management and incident response. Companies find themselves forced to spend more dollars on the specialized ICS security products to keep up with regulatory requirements as well as with ensuring operational resilience with increasing complexity in compliance. This is leading to industrial owners and operators becoming more advanced in cybersecurity techniques to protect their critical infrastructure.

Increasing cyberattacks on critical infrastructure: The increasing number of cyberattacks and the level of these attacks on critical infrastructure of the economy such as energy, water treatment, transportation, and manufacturing become more digitized and interconnected. They provide appealing, high-value targets for threat actors who want to disrupt society or simply make money. A single successful breach could lead to operational downtime, environmental destruction, and a reduction in public trust for the national safety institutions. As a result, asset holders are advancing from reactive compliance to proactive, risk-based security posture. This transition requires ongoing commitment to a wide variety of specialized ICS security products, such as network monitoring, endpoint protection, and anomaly detection, to protect both legacy and future industrial assets. Moreover, the ever-evolving threat environment requires operational technology environments to be continuously tested and hardened, and as such cyberattack mitigation will remain a major enabler for market growth.

-security-market-size-to-reach-usd-43.77-billion-by-2034-.webp)

Source: Polaris Market Research Analysis

Segmental Insights

Which Segments Contributed to the Market Expansion?

Component Analysis

Based on component, the segmentation includes solution and services. The solution segment accounted for 69.8% revenue share in 2025. This is owing to the increasing demand for sophisticated cyber security solutions that can offer a direct protection to the industrial control systems against advanced cyber-attacks. Industrial operators are starting to depend on dedicated security solutions, including the use of intrusion detection systems, specialized network monitoring tools, and threat intelligence products to the protection of critical infrastructure and ongoing operations. The solutions offer real-time monitoring of industrial networks, allowing organizations to identify anomalies and respond to potential cyber events in a more proactive manner. Moreover, the demands for integrated all in one security solution that can easily been integrated into the existing control system is well promoted with the increasing interconnected and digitalized of industrial environment. Also, the growing complexity of industrial networks has driven organizations to implement security platforms that are scalable, enabling them to secure both legacy systems and new devices as they come online within the operational environment.

Solution Analysis

In terms of solution, the segmentation includes anti-malware/antivirus, DDOS mitigation, encryption, firewall, IAM, others. The encryption segment is expected to witness substantial growth during the forecast period at a CAGR of 8.5%. This is essential to an important function of protecting sensitive industry data and communication over connected systems. Industrial environments are increasingly reliant on the sharing of operational data between control systems, sensors, cloud platforms, and enterprise applications. Encryption standards contribute to this by helping protect data from being accessed, intercepted or manipulated by an unauthorized party during transmission or while in storage. Furthermore, protecting data integrity is also becoming essential for ensuring operational reliability as industrial firms increase their deployment of connected devices and remote monitoring platforms. Increasing emphasis on protection of intellectual property, production data and system commands is also driving the use of encryption solutions in the industrial control arena.

Security Type Analysis

Based on security type, the segmentation includes network, endpoint, application, and database. The network segment dominated the market accounting for USD 8.68 billion in 2025. This is owing to the importance of network infrastructure to industrial devices, control systems, and operational technologies. Industrial networks are the means of communications among programmable logic controllers, supervisory control systems, sensors, and enterprise applications. These communication channels require protection to prevent eavesdropping, dissemination of malicious code, and denial-of-service attack. Network security solutions such as, firewalls, intrusion detection systems (IDS), and network sniffers also help identify abnormal traffic patterns and protect the industrial network from potential cyber events. Protecting these networks is at the top of the priority list for organizations that are aiming for the integrity, availability, and safety of their critical operational processes in an era of increasing connectivity in industrial environments through remote access and digital monitoring tools.

Source: Polaris Market Research Analysis

Regional Analysis

How Regions Affected the Overall Market Revenue?

North America Industrial Control Systems (ICS) Security Market

North America led the global market in 2025, holding a 38.0% revenue share. This is attributed to the availability of refined industrial infrastructure, early adoption of digital technologies, and greater level of cybersecurity awareness among the operators of critical infrastructures. Industries such as power, water, manufacturing and oil and gas in the region are increasingly adopting connected industrial control systems, raising demands for layered security frameworks to secure operational environments. Organizations are giving higher priority to implementing advanced threat detection, network monitoring and access control solutions to protect their most critical industrial assets. The region also takes advantage of established regulatory requirements and a mature cybersecurity community that enables operational technology environments to be protected. Furthermore, the increasing integration of cloud monitoring platforms and remotely operated systems is also driving the demand for ICS security solutions in industrial applications. In February 2025, Cyolo released AI-driven cyber security for cyber-physical and OT spaces. Built with NVIDIA technologies, its Cyolo PRO platform delivers identity-first Zero Trust Network Access, helping to harmonize secure remote access for the manufacturers, energy, and other critical infrastructure industries.

U.S. is the major contributor in the region due to the extensive usage of industrial automation and digital infrastructure in various critical industries. The country's industrial operators are progressively adopting more sophisticated cybersecurity measures to protect complex IT and OT environments. Therefore, continued technology advances and major cybersecurity solution vendors in place also boost growth of the U.S. ICS security market.

Asia Pacific Industrial Control Systems (ICS) Security Market

The industrial control systems (ICS) security landscape in Asia Pacific is projected to witness the fastest growth during the forecast period at a CAGR of 9.3%. This is driven by growth in industrialization and increasing use of digital manufacturing technologies in developing nations. Nations throughout the region are fast-tracking smart manufacturing strategies and increasingly adopting automation solutions and industrial connectivity platforms to drive manufacturing efficiency and operational intelligence. Related to these trends, the growing integration of Industrial Internet of Things (IIoT) devices and advanced analytics solutions with industrial operations has made industrial networks increasingly vulnerable to cyber threats. This enabled the ICS security solutions to be more cost effective and have less compromising impact on operational systems, and thus more acceptable by the end-users.

Furthermore, growing critical infrastructure projects and increasing digitization of manufacturing ecosystems also helping for advanced cybersecurity technology adoption across the region. China has a substantial share in the regional market as the country has large manufacturing base and is focused on industrial modernization and automation. The nation is increasingly adopting smart factory solutions and connected industrial systems, thus raising the need to secure operational technology environments. Consequently, industrial companies in China are prioritizing cybersecurity to a greater degree, in order to protect industrial networks, critical infrastructure, and connected manufacturing ecosystems.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

Some of the major corporations participating in the industrial control systems (ICS) security industry include: ABB Group; BAE Systems; Check Point; Cisco Systems; DarkTrace; Fortinet; Honeywell International Inc.; IBM Corporation; Kaspersky Labs; Microsoft Corporation; Nozomi Networks. The ICS security market is driven by combination of OT-focused specialists and massive IT-centric companies. Nozomi Networks and DarkTrace are the leading AI driven OT network visibility and anomaly detection solutions, favored by critical infrastructure operators. Fortinet and Cisco Systems build on strong networking backgrounds to provide IT/OT convergence with ICS security, including solid firewalls and segmentation. Microsoft and IBM distinguish themselves with cloud-native SIEM/XDR platforms by Microsoft Defender for IoT, and IBM QRadar that consume OT telemetry. Kaspersky Labs and Check Point have very good endpoint and gateway protection for the industrial sector. Honeywell and ABB provide profound expertise in industrial process control and security is built-in from the start to their operational technology. BAE Systems focuses on high-assurance government and defense industrial bases. Although IT-centric vendors dominate scalability and threat intelligence, OT-native vendors lead in protocol awareness and minimal impact deployment. The market is consolidating around unified platforms providing visibility, Zero Trust access, and swift response.

Key Players

- ABB Group

- BAE Systems

- Check Point

- Cisco Systems

- Claroty

- DarkTrace

- Fortinet

- Honeywell International Inc.

- IBM Corporation

- Kaspersky Labs

- Microsoft Corporation

- Nozomi Networks

Industry Developments

- April 2026: Claroty added Visibility Orchestration to its Claroty xDome SaaS platform. The capability translates esoteric visibility into measurable value, enabling industrial, healthcare, and public sector customers to enhance data quality, security posture, and orchestrated risk reduction for cyber-physical systems. [Source: https://claroty.com/]

- May 2025: Honeywell collaborated with Nutanix to deliver the Honeywell Integrated Control and Safety System on a secure, scalable hybrid cloud infrastructure. The solution combines Nutanix platform with Honeywell's Experion PKS and enables industrial customers to transform control while increasing cybersecurity and operations efficiency. [Source: https://www.honeywell.com/us/en]

Industrial Control Systems (ICS) Security Market Segmentation

By Component Outlook (Revenue, USD Billion, 2021–2034)

- Solution

- Services

By Solution Outlook (Revenue, USD Billion, 2021–2034)

- Anti-malware/Antivirus

- DDoS Mitigation

- Encryption

- Firewall

- IAM

- Others

By Security Type Outlook (Revenue, USD Billion, 2021–2034)

- Network

- Endpoint

- Application

- Database

By Vertical Outlook (Revenue, USD Billion, 2021–2034)

- Power

- Energy and Utility

- Transportation Systems

- Manufacturing

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Industrial Control Systems (ICS) Security Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 21.84 billion |

| Market Size in 2026 | USD 23.56 billion |

| Revenue Forecast by 2034 | USD 43.77 billion |

| CAGR | 8.03% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Industrial Control Systems (ICS) Security Market FAQ's

The global market size was valued at USD 21.84 billion in 2025 and is projected to grow to USD 43.77 billion by 2034.

The global market is projected to register a CAGR of 8.03% during the forecast period.

North America dominated the global market in 2025, holding a 38.0% revenue share.

A few of the key players in the market are ABB Group; BAE Systems; Check Point; Cisco Systems; DarkTrace; Fortinet; Honeywell International Inc.; IBM Corporation; Kaspersky Labs; Microsoft Corporation; Nozomi Networks

The solution segment dominated the market accounting for 69.8% revenue share in 2025.

The encryption segment is expected to witness substantial growth during the forecast period at a CAGR of 8.5%.

Download Sample Report of Industrial Control Systems (ICS) Security Market

Please fill out the form to request a customized copy of the research report.