Marine Battery Market Share, Size, Trends, Industry Analysis Report, 2026- 2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Marine Battery Market Summary

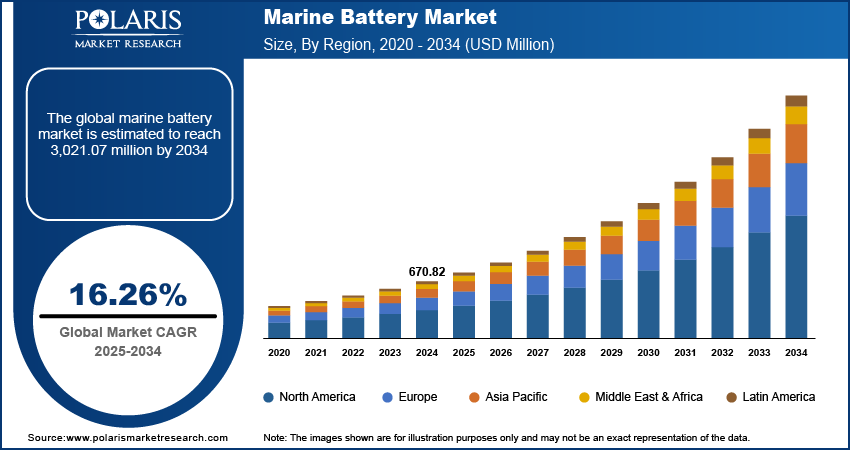

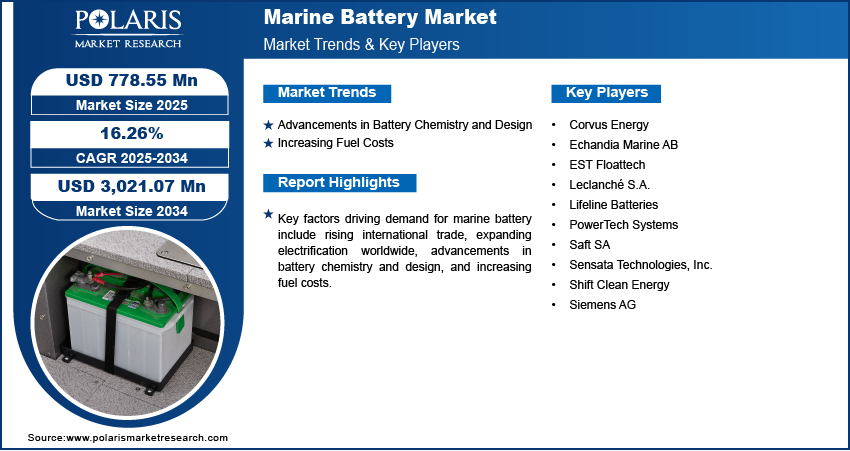

The global marine battery market was valued at USD 778.55 million in 2025. It is expected to account for a compound annual growth rate of 16.26% from 2026 to 2034. Key drivers of marine batteries include global maritime trade growth, technological advancements in marine batteries, and rising fuel prices.

Market Statistics

Key Takeaways

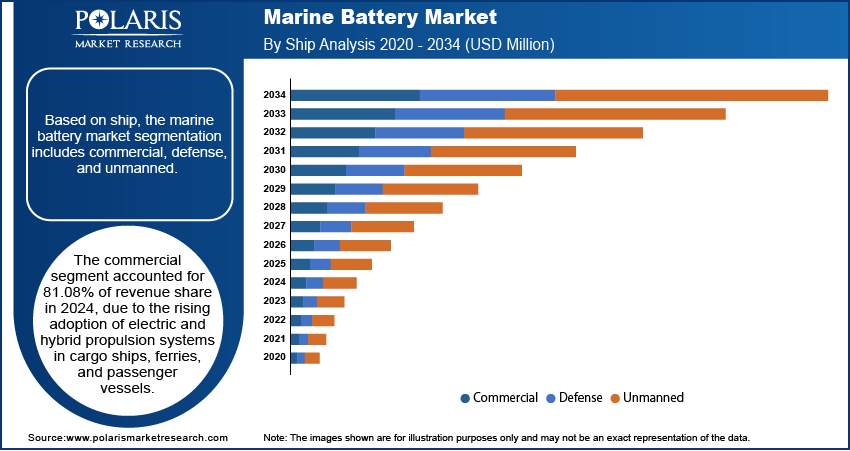

- The commercial segment accounted for 81.08% of the market revenue share in 2025. The segment’s growth is driven by the rising adoption of hybrid and electric propulsion systems in passenger and cargo ships.

- The deep-cycle batteries segment dominated with 33.21% market share in 2025. This is because deep-cycle batteries offer consistent power over extended periods.

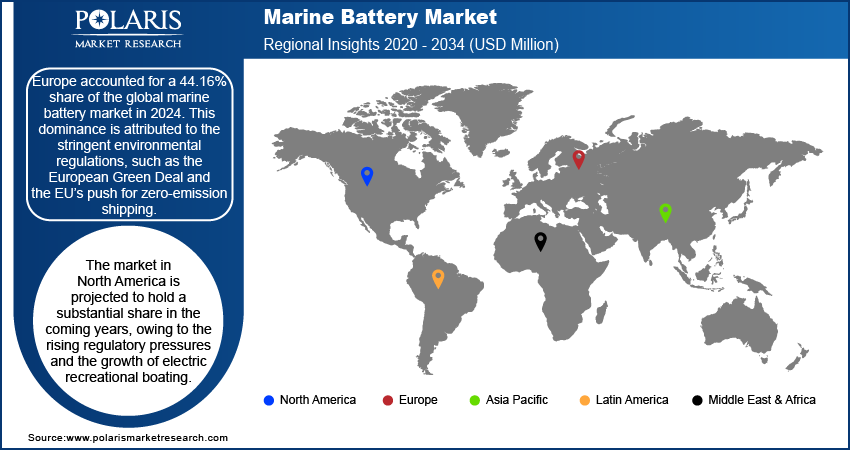

- Europe accounted for a 44.16% share of the global marine battery market in 2025. The presence of stringent emission regulations drives the leading market share of the region.

- The UK held 17.79% of the revenue share in the Europe marine battery landscape in 2025, primarily due to increasing decarbonization targets in the country.

- The market in North America is projected record the growth rate of CAGR 16.9% in the coming years. Rising regulatory pressures drive the expansion of the regional market.

Industry Dynamics

- There have been continuous advancements in lithium iron phosphate (LFP) and solid-state marine battery technologies. Such technologies are becoming more adaptable for rough conditions.

- Increasing fuel costs are accelerating the shift towards battery-powered marine propulsion. This can reduce operational costs in the long term.

- The expansion of maritime tourism and recreational boating is expected to create marine battery market opportunities.

- The high investment required in marine batteries hinders growth.

What Is A Marine Battery?

A marine battery is a specialized battery type intended for use in marine conditions on ships and yachts. Unlike the batteries in automobiles, marine batteries are created to withstand marine conditions. The marine conditions include high vibrations, water, saltwater, and wave actions. The battery is designed to make ferry transport safe and efficient. Marine batteries play an essential role in marine activities. These include recreational and commercial marine transport.

Modern marine batteries use advanced technologies such as battery management systems, temperature control systems, and waterproof enclosures. These batteries are designed and built to support the operation of electric propulsion systems and energy-intensive marine electronics.

The increasing international trade is fueling the growth of the marine battery market. The World Trade Organization reported that as of 2024, the average annual growth of world trade volume and value since 1995 has expanded 4% and 5%, respectively. This rising demand for international trade is encouraging shipowners to increase their investments in commercial marine vessels such as ships, ferries, and container ships to cater to this ever-growing need for logistics. These marine vehicles require efficient and environmentally friendly power supply systems. So, there is a rising demand for marine batteries. Furthermore, shipowners are now focusing on battery-powered ships to improve power efficiency and comply with environmental requirements and constraints, thereby increasing demand for marine batteries.

The demand for marine batteries is driven by the growth of the marine electrification market. Governments are investing in electric infrastructure for sustainable transport. This has led shipbuilders and operators to turn to battery-powered vessels to reduce dependence on fossil fuels. Secondly, confidence in marine battery technology has increased due to growing interest in electric mobility across many sectors. So, the use of marine batteries has increased in commercial and recreational boats.

Real-World Examples of Marine Battery Applications

| Application Area | Real-World Example | Battery Type Used |

| Electric Ferries | Fully electric passenger ferries operating on short coastal routes for zero-emission transport | Lithium |

| Hybrid Ships | Cargo vessels and offshore support ships are using hybrid propulsion systems to reduce fuel consumption and emissions | Lithium/Fuel Cells |

| Recreational Boats | Yachts, speedboats, and leisure boats using batteries for propulsion, lighting, and onboard electronics | Lead Acid/Lithium |

| Fishing Vessels | Small and medium fishing boats using batteries for engine starting, navigation, and auxiliary systems | Lead Acid |

| Naval and Defense Vessels | Submarines and naval ships require reliable backup power and mission-critical energy systems | Nickel Cadmium/Fuel Cells |

| Port and Harbor Operations | Harbor tugboats and service vessels are adopting battery-powered systems for cleaner short-distance operations | Lithium/Sodium-Ion |

Market Dynamics

Advancements in Battery Chemistry and Design

Manufacturers are focusing on the development of next-generation batteries. Next-generation batteries can charge quickly and last longer. In addition, the batteries can withstand harsh sea conditions. This has led to an increase in the use of such batteries. New technologies such as solid-state and lithium iron phosphate batteries are reducing the risk of overheating. They are also improving efficiency. Such features are encouraging boat operators to install marine batteries to power their systems.

Increasing Fuel Costs

The operational costs of diesel-powered vessels are rising significantly, driven by rising fuel costs. This promotes the adoption of battery-powered vessels and drives market expansion. Marine batteries provide a cost-effective solution by reducing dependence on fuel and lowering long-term expenses through improved energy efficiency and reduced maintenance requirements. This financial incentive, along with stricter environmental regulations, is driving the rapid adoption of battery-powered propulsion.

Ship Analysis

By ship, the segmentation includes commercial, defense, and unmanned. The commercial segment accounted for 81.08% of revenue in 2025. This is due to the rising adoption of electric and hybrid propulsion systems across cargo ships, ferries, and passenger vessels. Shipbuilders and commercial operators have increasingly adopted low-emission technologies and electric ferries in response to international environmental regulations, such as the IMO's 2020 sulfur regulations. Besides, the rapid electrification of commercial vessels, particularly those operating over short distances such as ferries and support ships, has been due to their generally predictable routes and regular docking. This has made battery recharging easy. The high energy demand from these ships created a strong market for high-capacity, long-cycle lithium-ion battery systems, which contributed to their dominance. Furthermore, short-sea shipping and predictable ferry routes have made commercial marine battery market systems particularly viable. This supports sustained growth.

The unmanned market is expected to grow rapidly over the next few years. The naval and maritime industry is increasingly using unmanned surface and underwater vessels for applications such as surveillance, research, logistics support, and inspection. These unmanned crafts use electric propulsion extensively to minimize noise and size. Moreover, the naval and maritime industry is increasingly benefiting from the growing availability of remote battery management systems for unmanned crafts.

Type Analysis

By type, the marine battery market segmentation includes lithium, lead acid, nickel cadmium, sodium-ion, and fuel cells. The lithium battery type led the market in 2025, as this type has higher energy density and lower weight than other types of batteries. Ship owners are gradually adopting lithium battery systems in both the commercial and military markets. Lithium battery systems ensure improved performance and lower maintenance costs. They also allow for strict compliance with environmental laws. Demand for lithium batteries has grown rapidly as ferries and offshore service vessels move toward electrification. Manufacturers have also favored lithium solutions for their scalability and compatibility with most modern battery management systems. Their use enables efficient monitoring and energy control.

Marine Battery Types and Applications

| Battery Type | Key Applications |

| Lithium | Electric propulsion systems, hybrid ferries, yachts, offshore support vessels, and onboard energy storage for navigation and communication systems |

| Lead Acid | Engine starting batteries, backup power systems, lighting circuits, small fishing boats, and conventional marine auxiliary power |

| Nickel Cadmium | Emergency backup systems, naval vessels, offshore platforms, heavy-duty propulsion support, and high-reliability marine equipment |

| Sodium-Ion | Emerging electric vessels, coastal ferries, renewable-powered marine storage, low-cost hybrid propulsion systems, and sustainable marine backup power |

| Fuel Cells | Hydrogen-powered ships, zero-emission ferries, submarines, long-range commercial vessels, and auxiliary clean energy systems for ports and vessels |

Function Analysis

In terms of function, the segmentation includes starting batteries, deep-cycle batteries, and dual purpose batteries. The deep-cycle batteries segment dominated the market share in 2025. This is due to its ability to deliver consistent power over extended periods. So, they are suitable for propulsion and onboard energy systems in electric and hybrid vessels. Ship operators choose deep-cycle systems to support auxiliary functions such as lighting, navigation, refrigeration, and communication, particularly in commercial and recreational vessels that require sustained energy delivery rather than quick bursts. Unlike starting batteries, which provide short, high-current outputs, deep-cycle variants withstand frequent charge and discharge cycles, offering better reliability and longevity in marine environments. The rising adoption of electric propulsion systems has further propelled demand for deep-cycle technologies, especially among short-distance ferries, offshore service vessels, and yachts.

Capacity Analysis

In terms of capacity, the segmentation includes < 100 AH, 100–250 AH, and > 250 AH. The 100–250 AH segment is likely to exhibit the highest CAGR during the forecast period. The 100–250 AH capacity is most applicable to mid-sized vessels. These include ferries, fishing boats, and recreational crafts. Ship operators are looking for this capacity range because it offers a mix of power and cost-efficiency. It can also be applied to both propulsion and auxiliary systems in electric and hybrid platforms. Moreover, compact and modular battery systems are available in this capacity range. They can be installed in existing onboard configurations without performance or space utilization losses, which has led to their high adoption.

Regional Analysis

Europe accounted for the largest share of the global marine battery market, with 44.16% in 2025. The dominance of the Europe marine battery market can be attributed mainly to the strong environmental policies, such as the European Green Deal and the EU's target of zero-emission ships. Europe is also majorly investing in electrification, primarily for inland water transport, ferries, and short-sea transport. Norway, along with Germany and the Netherlands, has been at the forefront of hybrid and fully electric ships, which they have begun using because of the subsidies they provide. Europe is also heavily focused on offshore wind farms and zero-emission ships powered by batteries.

UK Marine Battery Market Insight

The UK accounted for 17.79% of the revenue share in the European marine battery market in 2025. This is due to the rise in decarbonization ambitions, including the Clean Maritime Plan, which aims to achieve zero-emission maritime transport by 2050. Additionally, the UK has an extensive offshore energy market, which is promoting marine batteries, as it uses battery-driven vessels for maintenance and personnel transfer. Additionally, government funding and collaboration with battery manufacturers have encouraged the adoption of sustainable maritime technology.

North America Marine Battery Market Trends

North America is likely to occupy a significant position in the years to come. This is due to increased regulatory pressures and the rise of electric recreational boating. The U.S. and Canada have introduced stricter emissions regulations for commercial and passenger boats, mostly in ecologically sensitive regions like the Great Lakes and coastline. Electric ferry boats have gained popularity in New York and Seattle, and an increasing trend is being witnessed towards hybrid technology for working boats. The shift toward electric yachts and sports boats also contributes to this demand.

U.S. Marine Battery Market Overview

In the U.S., the growth of marine batteries is driven by initiatives from the U.S. government. The initiatives include the EPA's Clean Ports Program, as well as state regulations on air emissions, especially those of California. This has led to increased adoption of hybrid and electric propulsion technology by the U.S. military and the shipping industry, thereby promoting growth. The recreation boating industry is also driving the market, led by companies such as Brunswick.

Asia Pacific Marine Battery Market Analysis

Asia Pacific is expected to have the highest CAGR from 2025 to 2034, driven by the expansion of ferry networks, governments’ focus on electrification initiatives, and increased investment in green maritime. Asia Pacific is led by countries such as China, Japan, and South Korea, with China as the leading producer of batteries for e-ships. Additionally, the offshore wind and fish farming sectors in the Asia Pacific are driving market revenue growth. Also, Southeast Asia is showing an inclination towards e-ferries, backed by funding and initiatives from governments and global agencies.

Key Players and Competitive Analysis

The marine battery market is highly competitive, and major players such as Corvus Energy, Echchandia Marine AB, EST Floattech, Leclanché SA, Lifeline Batteries, PowerTech Systems, Saft SA, Sensata Technologies, Shift Clean Energy, and Siemens AG are competing to introduce innovative energy storage solutions for the maritime sector. Among these, Corvus Energy leads the market due to its high-capacity lithium-ion batteries used in hybrid and fully electric ferries, offshore ships, and even navy ships. Echchandia Marine AB specializes in customized batteries for short-sea shipping, leveraging its expertise in fast-charging batteries. EST Floattech focuses on modular batteries, which are more suitable for inland waterways and workboats. Leclanché SA offers marine-type-approved lithium-ion batteries that are highly focused on longevity and safe operation.

Key Players

- Corvus Energy

- Echandia Marine AB

- EST Floattech

- Leclanché S.A.

- Lifeline Batteries

- PowerTech Systems

- Saft SA

- Sensata Technologies, Inc.

- Shift Clean Energy

- Siemens AG

Marine Battery Industry Developments

March 2025: Corvus Energy received approval from the UK-based classification society Lloyd’s Register (LR) for its Dolphin NxtGen Energy marine battery system, (Source: offshore-energy.biz)

February 2024: EST-Floattech, a developer of maritime battery systems, received an investment of EUR 4 million from Energy Transition Fund Rotterdam and existing shareholders for the development of maritime battery systems. (Source: marinelink.com)

Marine Battery Market Segmentation

By Ship Outlook (Revenue, USD Million, 2021–2034)

- Commercial

- Defense

- Unmanned

By Type Outlook (Revenue, USD Million, 2021–2034)

- Lithium

- Lead Acid

- Nickel Cadmium

- Sodium-Ion

- Fuel Cells

By Function Outlook (Revenue, USD Million, 2021–2034)

- Starting Batteries

- Deep-Cycle Batteries

- Dual Purpose Batteries

By Capacity Outlook (Revenue, USD Million, 2021–2034)

- < 100 AH

- 100–250 AH

- > 250 AH

By Propulsion Outlook (Revenue, USD Million, 2021–2034)

- Conventional

- Hybrid

- Fully Electric

By Ship Power Outlook (Revenue, USD Million, 2021–2034)

- < 75 KW

- 75–150 KW

- 150–745 KW

- 745 KW & Above

By Design Outlook (Revenue, USD Million, 2021–2034)

- Solid State

- Liquid/ Gel Based

By Energy Density Outlook (Revenue, USD Million, 2021–2034)

- <100 WH/Kg

- 100–500 WH/Kg

- >500 WH/Kg

By Regional Outlook (Revenue – USD Million, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Future of Marine Battery Market

The future of the marine battery industry is strongly fueled by the electrification of ships and the global emphasis on zero-emission maritime transport. Governments and shipping companies are investing in electric ferries, hybrid vessels, and hydrogen-powered ships. They are taking these efforts to meet stricter environmental regulations and carbon reduction targets. Advancements in lithium-ion, sodium-ion, and fuel cell technologies are improving energy density, safety, and charging efficiency for marine applications. Growing adoption of smart ports and shore-to-ship power systems is expected to support battery integration across commercial and recreational marine operations

Marine Battery Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 778.55 million |

| Market Size in 2026 | USD 903.90 million |

| Revenue Forecast by 2034 | USD 3,021.07 million |

| CAGR | 16.26% |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD million, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Marine Battery Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The marine battery market was valued at USD 778.55 million in 2025 and is estimated to reach USD 3,021.07 million by 2034, growing at a CAGR of 16.26%.

Lithium batteries have the largest market share. This is because they offer high energy density and have a long lifespan. They are also compatible with boat battery management systems.

Marine batteries power commercial ships, defense ships, and unmanned watercraft. They find applications in propulsion systems, navigation, illumination, refrigeration, communication, and auxiliary services.

Europe dominates the global market for marine batteries due to its strong environmental policies and high investments in vessel electrification.

The market drivers include rising global trade, increasing electrification, evolving battery technology, rising fuel costs, and environmental policies that encourage environmentally sustainable maritime transport alternatives.

The unmanned segment is expected to witness the fastest growth during the forecast period.

Download Sample Report of Marine Battery Market

Please fill out the form to request a customized copy of the research report.