Offshore Decommissioning Market Size, Share & Trends Analysis 2026 - 2034

REPORT DETAILS

Offshore Decommissioning Market Summary

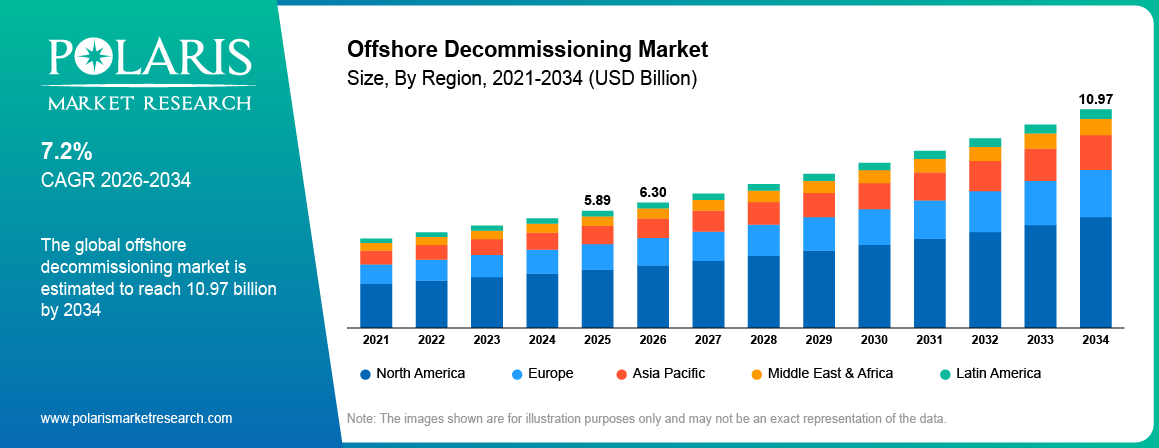

The global offshore decommissioning market is estimated around USD 5.89 Billion in 2025,?with consistent growth anticipated during 2026–2034. Expansion is driven by the increasing number of aging offshore oil and gas assets, strict environmental regulations, and rising focus on responsible asset retirement. The market is projected to grow at a CAGR of 7.2%during the forecast period.

Market Statistics

Key Takeaways

- North America dominated with a market share of approximately 43.60% in 2025, supported by a large base of aging offshore infrastructure and strict regulatory requirements for asset retirement in the Gulf of Mexico

- Full-scope offshore decommissioning held a market share of nearly 37.25% in 2025, driven by increasing adoption of integrated project execution across all lifecycle stages

- Well plugging and abandonment services accounted for a market share of approximately 33.80% in 2025, supported by regulatory mandates and high technical importance in offshore asset closure

- Oil and gas operators segment held a share of nearly 39.45% in 2025, driven by a large base of aging offshore infrastructure across mature basins

- Shallow water decommissioning accounted for a market share of approximately 35.10% in 2025, supported by a high number of fixed platform removal projects

- Subsea pipeline decommissioning is projected to register a CAGR of nearly 12.70% during 2026–2034, driven by increasing volumes of aging subsea infrastructure

Industry Dynamics

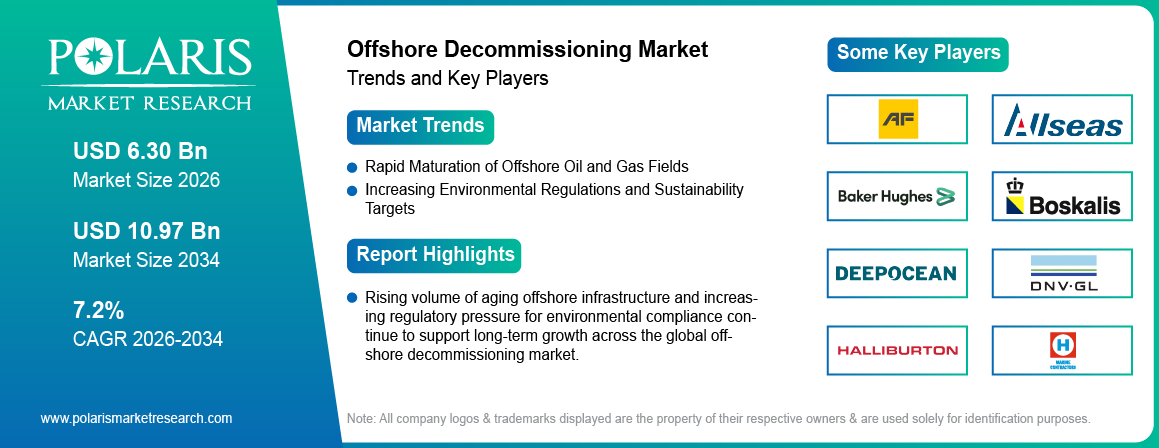

- Rapid maturation of offshore oil and gas fields is increasing demand for large-scale decommissioning services across global basins.

- Stringent regulations on environment are boosting demand for compliant offshore dismantling and site restoration.

- High capital costs and operational intricacy are posing barriers to smaller operators.

- Adoption of digital technologies and integrated project management platforms is unlocking new opportunities in offshore execution.

What is included in the Offshore Decommissioning market?

The offshore decommissioning market is an essential sector within the energy services domain, with its main activities centered on the removal, dismantling, and disposal of older offshore oil and gas installations. Offshore decommissioning is an activity centered on retiring offshore oil and gas fields, pipelines, and wells, with activities conducted related to environmental regulations.

The offshore decommissioning industry analysis is based on increasing level of activities, with this sector fueled by large number of older offshore oil and gas fields in key locations such as the North Sea, Gulf of Mexico, and Asia Pacific. The offshore decommissioning industry is responsible for all activities, apart from those conducted for production, with this sector indicating an engineering and environmental service domain.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

Decommissioning in the offshore industry has a high level of strategic importance, considering the fact that energy companies seek to ensure responsible closure and environmental care. Decommissioning in the offshore industry ensures regulatory compliance, minimizes environmental risks, and optimizes the use of marine space. Demand for decommissioning in the offshore industry depends on the number of old offshore fields and requirement for sophisticated engineering skills to deal with complex offshore structures.

Drivers & Opportunities

Rapid Maturation of Offshore Oil and Gas Fields Globally: Large number of offshore oil rigs nearing the end of their useful life, especially in mature oil fields such as the North Sea or the Gulf of Mexico, thus fueling the market growth. According to the World Economic Forum, thousands of the world’s 12,000 oil platforms are nearing retirement, which is why there is a structural pipeline of decommissioning work. The aging oil rigs need well plugging, structure removal, and seabed remediation, which will continue to fuel service demand in the offshore oil and gas decommissioning market.

Environmental Concerns and Sustainability Targets: Regulatory authorities in areas such as the North Sea are enforcing stringent environmental compliance for asset retirement operations. Governments have set targets for the removal of outdated infrastructure in its entirety or in part in order to minimize environmental hazards and rejuvenate the ecosystem. Oil and gas operators in the Gulf of Mexico are currently faced with high standards set for well abandonment operations. This increases the decommissioning time and scope, thereby enhancing service requirements and ongoing investment in compliance-based dismantling solutions.

Restrain

High Offshore Decommissioning Cost Challenges: Offshore decommissioning is characterized by complex logistics, the need for special vessels, and heavy lift operations, which are costly in terms of capital costs and operating expenses. Financial planning is essential for subsea well plugging, topsides removal, and waste disposal. Besides, the regulations are very stringent, especially in the North Sea, which adds to the overall cost.

Opportunity

Digital Transformation in Offshore Dismantling: The adoption of digital technology in offshore dismantling projects has been positively transforming the industry. Industrial AI, prediction technologies, and integrated enterprise technologies have been effectively implemented to optimize resources. In December 2025, Dixstone adopted IFS Cloud to transform and consolidate offshore operations across 10 countries, including decommissioning.

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the offshore decommissioning market by process, services, and depth & structure to help readers identify the fastest expanding and most attractive demand segments.

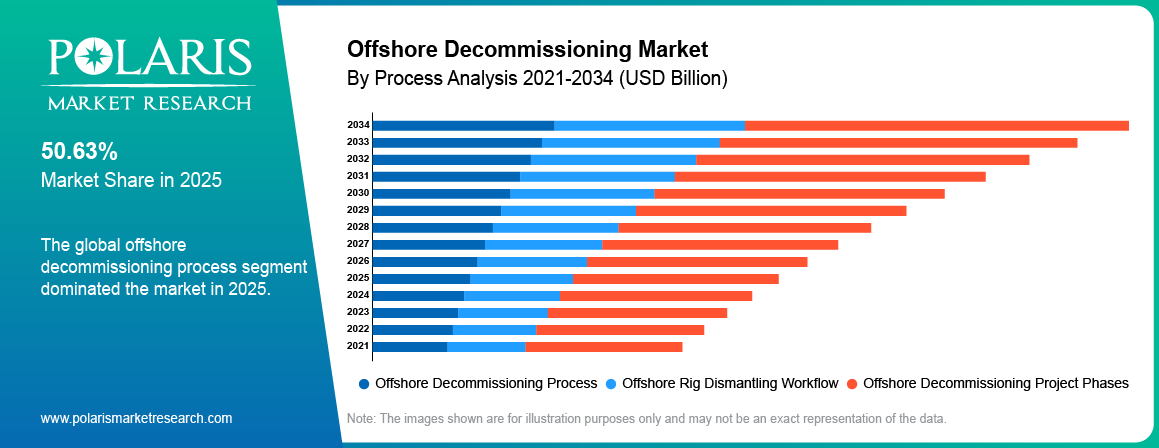

By Process

-

Offshore Decommissioning Process

Offshore decommissioning process (full lifecycle projects) held the largest share as operators increasingly adopt integrated execution across all offshore decommissioning project phases. The process moves from planning and regulatory approvals to well plugging, topside removal, subsea disconnection, and site clearance.

-

Offshore Rig Dismantling

Offshore rig dismantling workflow optimization is the fastest-growing segment due to rising focus on reducing offshore time and project costs. Contractors are standardizing step-by-step dismantling through modular removal, heavy-lift coordination, and digital planning. This technique improves safety, repeatability, and efficiency for all multi-asset decommissioning projects.

By Services

-

Well Plugging and Abandonment Services Offshore

Well plugging and abandonment services offshore held the largest share in the market due to the critical and cost-intensive nature of this activity. This service involves the permanent plugging and abandonment of wells with the aid of cement.

-

Subsea Pipeline Decommissioning Process

Subsea pipeline decommissioning process is witnessing the fastest growth due to the increasing volume of aging subsea infrastructure. Activities include cleaning, disconnection, removal or in-situ decommissioning, and seabed restoration.

By Depth & Structure

-

Shallow Water Offshore Decommissioning Market

Shallow water offshore decommissioning market accounted for the largest share due to a high number of mature fixed offshore platform removal projects. This facilitates simpler operations, reduced timelines, and lower costs using conventional vessels. This makes the complete removal cost-effective.

-

Deepwater Decommissioning Market

Deepwater decommissioning market projected to grow at fastest growth rate as more complex assets approach the end of their life. These projects involve FPSO decommissioning market dynamics and extensive subsea systems. They demand advanced technologies and higher investment. Compared to shallow water projects, deepwater projects experience higher costs but more large-scale opportunities.

Source: Polaris Market Research Analysis

Regional Analysis

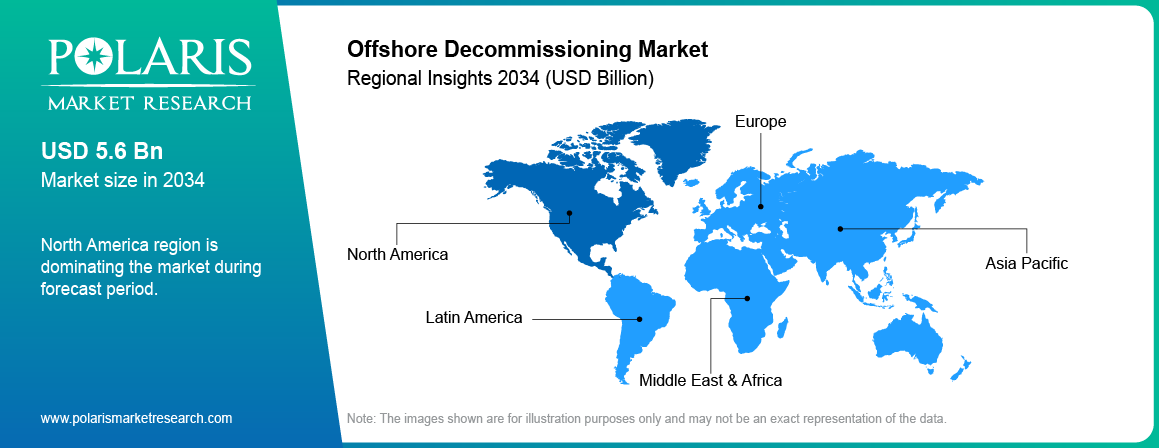

North America Offshore Decommissioning Market Assessment

North America offshore decommissioning market remained strong due to extensive offshore activity and a large base of aging infrastructure in the US Gulf of Mexico. US Gulf of Mexico decommissioning trends are largely influenced by the rigorous regulatory demands on well plugging and platform removal projects for steady stream of work. There is increasing emphasis on late-life asset management system by operators as the assets age in the US Gulf of Mexico. In 2024, BP America is one of the leading producers in the US offshore sector, aiming for over 400,000 barrels of oil equivalent per day by 2030.

Europe Offshore Decommissioning Market Overview

Europe offshore decommissioning market has grown steadily driven by high investments in asset retirement and environmental restoration activities. The North Sea is the major factor for the Europe offshore decommissioning market due to high regulatory standards set by the government of the UK and Norway, which demand a well-structured approach to decommissioning old infrastructure. The analysis of the UK offshore decommissioning market shows that it is driven by a high number of projects related to old oil fields, while the offshore decommissioning market in Norway is growing due to high regulatory standards and operator accountability.

Asia Pacific Offshore Decommissioning Market Insight

Asia Pacific offshore dismantling market is projected to grow at a rapid pace, due to increasing offshore exploratory activities and rise in the number of aging offshore assets in Southeast Asia. Countries like Indonesia and Malaysia are increasing upstream activities while gradually developing decommissioning regulations. The Indonesian government's intention to award 54 blocks in the oil and gas sector between 2024 and 2028 suggests the presence of a pipeline of assets in the country waiting to be decommissioned. Changes in regulations and the increase in offshore infrastructure contribute to the growth of the decommissioning industry.

Middle East and Latin America Offshore Decommissioning Market Assessment

Middle East offshore removal market and Brazil offshore decommissioning projects are developing with increasing emphasis on asset lifecycle management and regulatory compliance. Brazil has a well-developed decommissioning pipeline associated with its mature offshore fields, and Middle East countries are gradually enhancing environmental regulations for offshore asset decommissioning.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The competitive profile of the offshore decommissioning industry reflects robust participation by integrated offshore EPC companies, subsea engineering companies, and environmental consultancies providing complete dismantling and restoration services. Leading offshore dismantling contractors compete on the basis of their capabilities in well plugging and abandonment, heavy lift removal, subsea infrastructure decommissioning, and recycling.

Key companies operating in the offshore decommissioning market include AF Gruppen ASA, Allseas Group SA, Baker Hughes Company, Boskalis Westminster N.V., DeepOcean Group Holding BV, DNV Group AS, Halliburton Company, Heerema Marine Contractors, John Wood Group PLC, Oceaneering International, Inc., Petrofac Limited, Ramboll Group AS, Saipem S.p.A., Schlumberger Limited, and Subsea 7 S.A.

Cost Structure of Offshore Decommissioning

Offshore decommissioning has a multi-stage cost structure. Therefore, offshore decommissioning cost analysis varies significantly. The cost components involved in offshore decommissioning include well plugging and abandonment, topside removal, subsea dismantling, transportation, and disposal. The cost component with the maximum share in offshore decommissioning cost is well plugging and abandonment.

The cost of offshore rig removal depends on the depth of the water, level of complexity in the platform, and distance from the shore. The deeper the water, the more the cost of offshore rig removal.

Technology Trends (AI, Robotics, ROVs)

The use of industrial robotics in the decommissioning of offshore oil rigs, including ROVs, increases accuracy in subsea inspections and dismantling operations while minimizing the risk of injury to personnel. This increases efficiency, reducing the time required for the entire operation.

AI in oil rig dismantling helps in the planning, predictive maintenance, and optimization of operations. AI tools optimize the entire operation, reducing costs while minimizing downtime. This increases efficiency in the execution of the entire operation.

Environmental & Regulatory Impact

Offshore decommissioning environmental impact depends on the approach used in removal process. The full removal approach has minimal long-term seabed impact but has more emissions and cost.

Reefing has the advantage of reducing carbon footprint in the offshore oil rig removal process and promotes marine habitats. The reuse approach supports sustainable offshore decommissioning technologies by reusing the infrastructure. Regulations emphasize the need to carry out environmental assessments, thus encouraging low impact and cost-efficient offshore decommissioning.

Premium Insights

- Installations in shallow water have recorded high activity in terms of decommissioning due to the age factor, while installations in deep water are seen as the next phase of expansion.

- Stringent regulatory compliance in mature oil & gas regions is speeding up projects, thereby adding mandatory activities in the decommissioning process.

- The use of high technology is an improvement in the efficiency of execution phase, thereby changing the cost analysis of offshore decommissioning projects.

- North America maintains market leadership supported, while Asia Pacific is witnessing rapid growth driven by increasing offshore developments and policy evolution.

Key Players

- AF Gruppen ASA

- Allseas Group SA

- Baker Hughes Company

- Boskalis Westminster N.V.

- DeepOcean Group Holding BV

- DNV Group AS

- Halliburton Company

- Heerema Marine Contractors

- John Wood Group PLC

- Oceaneering International, Inc.

- Petrofac Limited

- Ramboll Group AS

- Saipem S.p.A.

- Schlumberger Limited

- Subsea 7 S.A.

Industry Developments

- March 2026: Global Maritime appointed for assisting in the decommissioning of the TetraSpar floating wind demonstrator in Norway, which is a significant project in decommissioning next-generation offshore renewable structures.

- February 2026: AF Offshore Decom announced its latest offshore decommissioning project, that involves dismantling and recycling of aging offshore structures utilizing advanced engineering and responsible environmental practices.

Offshore Decommissioning Market Segmentation

By Process Outlook (Revenue, USD Billion, 2021-2034)

- Offshore Decommissioning Process

- Offshore Rig Dismantling Workflow

- Offshore Decommissioning Project Phases

By Services Outlook (Revenue, USD Billion, 2021-2034)

- Well Plugging And Abandonment Services Offshore

- Offshore Platform Removal Services

- Subsea Pipeline Decommissioning Process

By Depth & Structure Outlook (Revenue, USD Billion, 2021-2034)

- Shallow Water Offshore Decommissioning Market

- Deepwater Decommissioning Market Trends

- FPSO Decommissioning Market

- Fixed Offshore Platform Removal

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Offshore Decommissioning Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 5.89 Billion |

| Market Size in 2026 | USD 6.30 Billion |

| Revenue Forecast by 2034 | USD 10.97 Billion |

| CAGR | 7.2% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Offshore Decommissioning Market FAQ's

The global market size was valued at USD 5.89 Billion in 2025 and is projected to grow to USD 10.97 Billion by 2034.

North America led the market due to extensive offshore oil and gas activity, a high volume of mature assets, and well-defined regulatory frameworks across the US Gulf of Mexico.

Oil and gas operators account for the largest share due to increasing need for safe retirement of offshore platforms and subsea infrastructure.

Key companies include Baker Hughes Company, Halliburton Company, Schlumberger Limited, Saipem S.p.A., Subsea 7 S.A., and others.

Trends include digital project tools, integrated services, deepwater project expansion, and focus on cost efficiency and sustainability.

Growth is driven by increasing number of aging offshore platforms, strict environmental regulations, rising decommissioning mandates, and growing focus on asset lifecycle management.

Key services include well plugging and abandonment, platform removal, subsea removal, pipeline decommissioning, and seabed clearance.

P&A refers to sealing wells permanently to prevent leakage and ensure environmental safety after production ends.

Pipelines are cleaned, disconnected, and either removed or left in place based on regulatory requirements.

Download Sample Report of Offshore Decommissioning Market

Please fill out the form to request a customized copy of the research report.