Pharmaceutical Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Pharmaceutical Market Summary

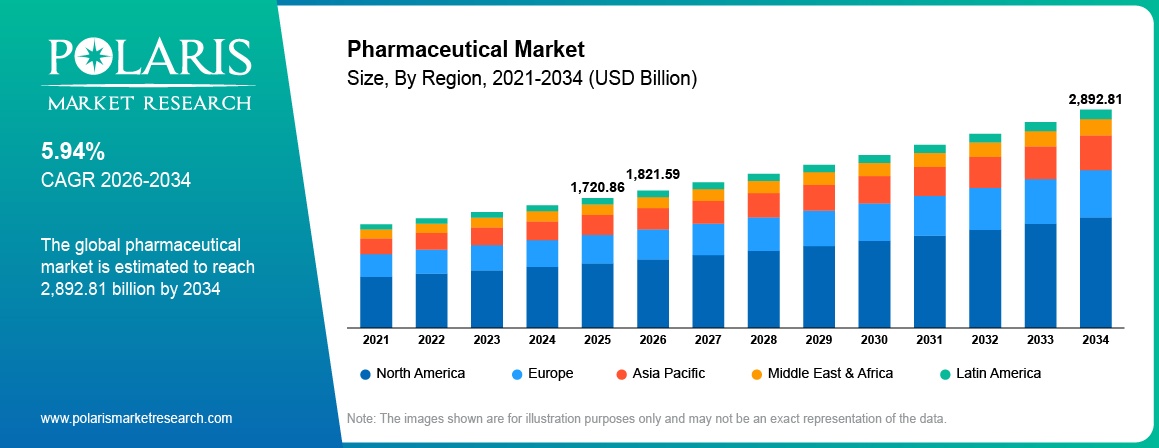

The global pharmaceutical market size was valued at USD 1,720.86 billion in 2025, growing at a CAGR of 5.94% from 2026–2034. Key factors driving demand include convergence with digital health technologies, use of AI in drug discovery, development of?precision medicine and gene therapies, and growing prevalence of chronic and ageing diseases.

Market Statistics

Key Takeaways

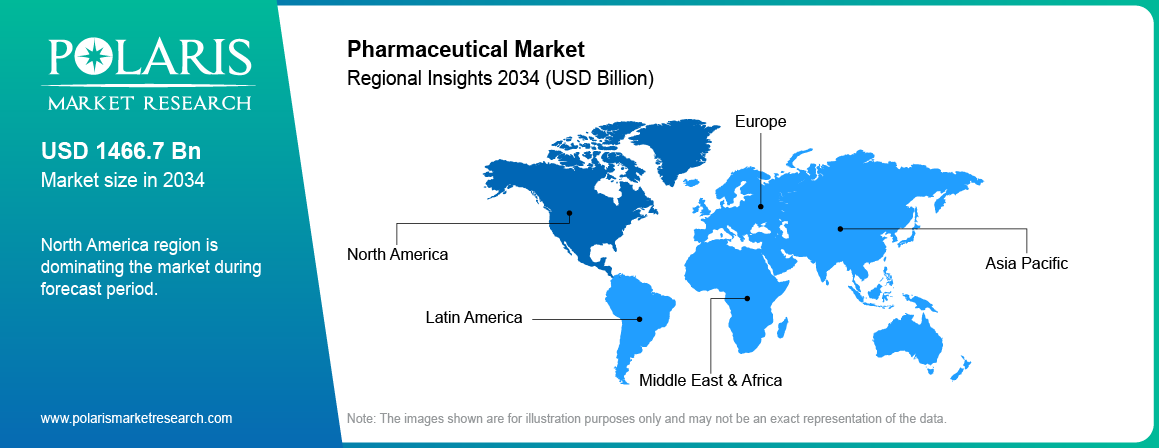

- North America led the global market in 2025, holding a 40.98% revenue share driven by the presence of advanced healthcare infrastructure, strong research capabilities and developed pharmaceutical industry ecosystem

- The pharmaceutical landscape in Asia Pacific is projected to witness the fastest growth during the forecast period at a CAGR of 6.92%. This is due to the increasing manufacturing, clinical research, and drug?discovery activities.

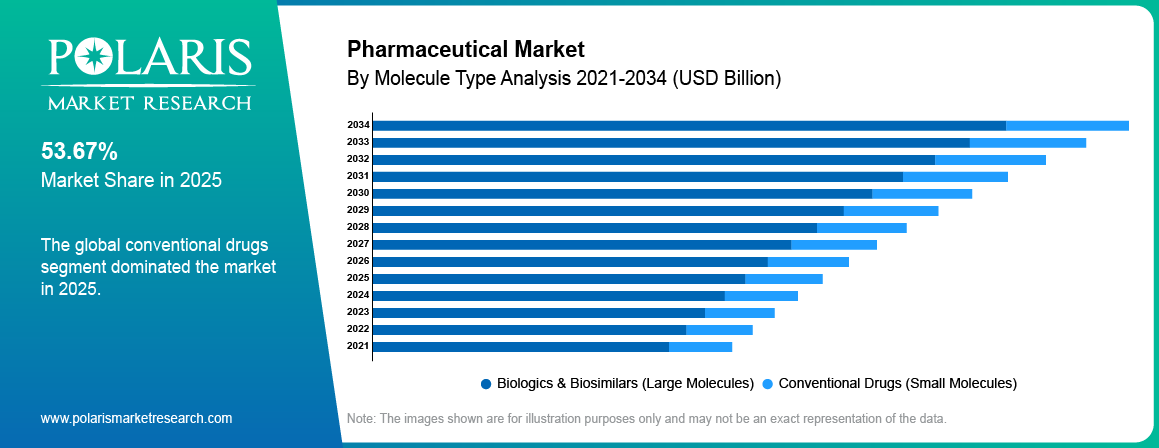

- Based on molecule type, conventional drugs segment accounted for 53.67% revenue share in 2025. This is due to their advantage of established manufacturing processes, well-established regulatory pathways, and cost-effective.

- Based on product, the generic segment is expected to witness the fastest growth during the forecast period at a CAGR of 6.94%. This is driven by increasing focus of healthcare systems on cost-effective treatment and improving access to medicines.

Industry Dynamics

- Advancements in precision medicine and gene therapies drives the growth due to their more precise and personalized methods of treatment.

- Rising prevalence of chronic and age-related diseases is due to increasing elderly populations, changes of living habits and expecting life years.

- Increasing pricing pressure and regulatory oversight, especially in the big markets, are tightening the profit margins for both branded and generic drug makers.

- Growing market expansion due to high demand from developing and underdeveloped nations is driven by increasing chronic disease rate and better access to healthcare.

What Does Pharmaceutical Market Includes?

Pharmaceuticals are a part of the life sciences industry dealing with the research, development, production, and marketing of drugs or pharmaceuticals used as medicines to diagnose, treat and prevent diseases. The impact of increasing patent expirations and the growth of the biosimilar market drives the market growth. In 2023, the pharmaceutical industry submitted 12,425 patent applications. Opportunities for biosimilar companies to bring highly similar therapies to market, emerges as patents on popular biologic and specialty drugs beginning to expire. This change can stimulate wider patient access to advanced therapies and promote a competitive environment. The pharmaceutical industry is evolving to redefine its product offerings as the need for product distinction through innovation, lifecycle management and development of next-generation biologics becomes crucial to cater this change. Hence, the changing biosimilar landscape is driving greater competition, cost-effectiveness and access to complex therapies for health care systems.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The pharmaceutical sector is moving towards convergence with digital health technologies and the use of artificial intelligence in drug discovery. Pharma is using sophisticated data analytics, machine learning models and digital platforms to increase the pace and quality of research and decision making across the drug discovery and development lifecycle. In March 2026, Iktos and Chemspeed partenered to integrate Iktos’ AI-based orchestration software Ilaka with Chemspeed’s automation solutions. The novel integrated approach automatizes the entire chemical synthesis process (from retrosynthesis to robotic execution) and can also be leveraged to explore new compounds with pharmaceutical partners at higher speed and efficiency. It enables earlier identification of potential drug targets, more informed design of clinical trials, and deeper data mining of large biomedical data sets. Moreover, digital health solutions that simultaneously feature connected monitoring devices and real-world data solutions are tapping into patients and enabling personalized medicine. Such advances in technology are driving greater research efficiencies and speed of innovation in the pharmaceutical industry as well as equipping these organizations with the capability to meet evolving healthcare needs.

Drivers & Opportunities

What are the Factors Driving the Market Growth?

Advancements in Precision Medicine and Gene Therapies: The development of precision medicine and gene therapies are major growth enablers for the pharmaceutical market by enabling more precise and personalized methods of treatment. Precision medicine is the study of how a person's unique genomic sequence, the nature of their disease, and other biological factors can be used to develop a medical treatment that is more likely to result in a successful outcome and/or with fewer side effects. At the same time, advances in gene therapy bring new opportunities to treat complicated, long-untreatable diseases at the level of their genes. Drugs companies are also putting more money into complex research platforms and specialized manufacturing processes that are required to develop these new kinds of treatments. In March 2026, Insilico Medicine announced a drug discovery collaboration with Eli Lilly, providing Lilly an exclusive license for novel oral therapeutics and integrating Insilico’s AI platform with Lilly’s development capabilities in a number of areas. This shift towards personalized and genetically-informed treatments is impacting traditional drug manufacturing, and opening new possibilities for very niche pharma products.

| Advancement | Key description | Example / context |

| Ultra‑rapid whole‑genome sequencing for acute care | New cloud‑based nanopore‑enabled workflows can diagnose critically ill infants in <8 hours, enabling rapid‑on‑set precision interventions (e.g., epilepsy, cardiac disorders). | Studies using nanopore‑based sequencing achieved diagnosis in ~7 hours 18 minutes in neonates. |

| CRISPR‑based & base‑editing gene therapies for monogenic diseases | Base‑editing and CRISPR‑corrected therapies have achieved functional cures in diseases such as sickle‑cell, hemophilia A, and rare neurogenetic disorders. | Single‑infusion lentiviral or AAV therapies for hemophilia show durable factor‑level correction and reduced bleeding over ≥5 years. |

| Next‑generation CAR‑T and cell therapies in oncology | Engineered CAR‑T cells and tumor‑infiltrating lymphocyte (TIL) therapies are now inducing deep remissions in glioblastoma, multiple myeloma, and relapsed leukemias with improved safety. | 2025 data show improved progression‑free survival in advanced blood cancers using personalized CAR‑T regimens. |

| Multi‑omics‑driven precision‑oncology and drug‑resistance profiling | Integration of genomics, proteomics, and spatial omics enables dynamic profiling of drug‑resistance mechanisms and secondary targets in solid tumors. | Multi‑omics platforms are used to identify bypass‑pathway mutations that drive resistance to targeted kinase inhibitors. |

| AI‑driven patient stratification and trial design | Machine‑learning models trained on large‑scale biobank and electronic‑health‑record data now optimize trial enrollment, predict treatment response, and de‑risk drug‑development pipelines. | AI‑tools are used to match patients with rare‑disease‑specific gene‑therapy trials using polygenic‑risk‑score and biomarker‑based clustering. |

Source: Polaris Market Research Analysis

Rising Prevalence of Chronic and Age-Related Diseases: The growing prevalence of chronic and ageing diseases boost the development of pharmaceutical industry. Cardiovascular diseases, diabetes, neurogenerative diseases and many types of cancers are on rise. In 2024, it is estimated by the International Diabetes Federation that 43% of the adults with diabetes, 252 billion people, are undiagnosed and 90% of them are residing in low- and middle-income countries. This is due to elderly populations, changes of living habits and expecting life years. In October 2025, the World Health Organization (WHO) stated that the 80 years or older population is expected to triple by 2050 to reach 426 billion. There is an increasing prevalence of these long-term diseases that require continuous care and management of the disease and innovation on more potent therapeutics. Thus, pharmaceutical companies are focusing on the development of medicines for complex chronic conditions with the potential for long-term patient advantages to enhance their product portfolios. Thus, with healthcare systems around the world focusing on early diagnosis, long-term disease management, and enhancement of patient’s quality of life, the need for innovative pharmaceutical treatments is expected to remain strong across global markets.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Segmental Insights

Which Segments Contributed to the Market Expansion?

Molecule Type Analysis

Based on molecule type, the segmentation includes biologics & biosimilars (large molecules) and conventional drugs (small molecules). The conventional drugs segment accounted for 53.67% revenue share in 2025. These drugs have the advantage of established manufacturing processes, well-established regulatory pathways, and cost-effective production and are used in various therapeutic areas. Also, small-molecule drugs are easier to develop and bring to the market as compared to complex biologic drugs. Their unqualified accessibility in branded or generics further pushes the mass adoption. Consequently, traditional medicines are still hugely relied upon worldwide in the pharmaceutical treatment regimens.

Product Analysis

In terms of product, the segmentation includes branded and generic. The generic segment is expected to witness the fastest growth during the forecast period at a CAGR of 6.94%. This is a result of increasing focus of healthcare systems on cost-effective treatment and improving access to medicines. Generics are therapeutic equivalents to branded drugs, but tend to have lower research and production costs. With this, the professionals and patients alike have access to the treatment they need at a fairer price. Furthermore, more and more of patent pharmaceuticals are introduced, thus directing the favor towards producers of generic drugs. Growing acceptance of generics among medical practitioners and regulatory agencies is consolidating the segment growth.

Disease Analysis

Based on disease, the segmentation includes cardiovascular diseases, cancer, diabetes, infectious diseases, neurological disorders, others. The cancer segment held the largest share of 17.96% in 2025. This is owing to the increasing focus on the development of drugs for oncology and the growing need for more advanced treatment options. Pharmaceutical companies are focusing their research efforts to bring new drugs to market that target intricate cancer biology and demonstrate improved outcomes for patients. Rising progress in targeted agents and immuno-oncology therapies is further broadening the therapeutic options in oncology. Moreover, the increasing focus on early diagnosis and long-term disease management is also driving the market for effective treatments against cancer. All these factors make the oncology segment a strong contributor in the pharmaceutical market.

Type Analysis

In terms of type, the segmentation includes prescription and OTC. The OTC segment is expected to grow at a CAGR of 7.28% during the forecast period. This is due to the increasingly shift towards adopting the convenient and more accessible health care solutions for the treatment of minor ailments and for preventive care. OTC drugs enable people to control their health and treat their common ailments without visit to doctor and are easily available at pharmacies and through other retail channels. Growing awareness towards self-care and preventive health management is also fueling demand for the products. Moreover, pharmaceutical companies are broadening their ranges of OTC products to tackle everyday health issues and to empower consumers to manage their own healthcare. This is also strengthening trend of OTC medicines as a significant share of the pharmaceutical market.

Source: Polaris Market Research Analysis

To Understand More About this Research: Request Customization

Regional Analysis

How Regions Affected the Overall Market Revenue?

North America Pharmaceutical Market

North America led the global market in 2025, holding a 40.98% revenue share. This is driven by the presence of advanced healthcare infrastructure, strong research capabilities and developed pharmaceutical industry ecosystem in the region. According to the OECD in 2024, average per capita health spending was nearly USD 6,000, and the U.S., with spending over USD 14,880 per person dominated the region. The region has a presence to several large pharmaceutical companies and numerous small and mid-sized ones, as well as having a highly developed regulatory environment that is conducive to drug development and commercialization. High levels of healthcare expenditure and a relatively strong pace of adoption of novel therapies also contributed to the region’s leading market position. The increasing focus on new methodologies of treatment such as biologics, specialty medicines also impart the growth of the pharmaceuticals. The region's ability to lead the global pharmaceutical market is further sustained by its continuous investments in research and clinical development.

Asia Pacific Pharmaceutical Market

The pharmaceutical landscape in Asia Pacific is projected to witness the fastest growth during the forecast period at a CAGR of 6.92%. This is due to the developing healthcare infrastructure and rising demand for available and affordable drugs. The region dominates in pharmaceutical manufacturing, clinical research, and drug discovery activities. Increasing awareness about health, better healthcare services, and high demand for sophisticated therapeutic solutions are the key factors driving the market growth. China is a major contributor driven by its numerous patients and the region’s fastest developing healthcare industry. The nation is witnessing rising capital inflow into drug innovation, local production abilities and regulatory reforms, which are all strengthening its role as a major growth contributor in the regional pharma landscape. The International Trade Administration estimated that China's pharmaceutical market will reach to USD 298 billion in 2025, growing at a CAGR of 7.8%. Furthermore, pharmaceutical giants are expanding their manufacturing facilities in the region and collaborating for research. Growing focus to enhance healthcare systems and pharmaceutical production capabilities in the region will fuel the market growth in Asia Pacific.

Source: Polaris Market Research Analysis

To Understand More About this Research: Request Customization

Key Players & Competitive Analysis Report

Some of the major corporations participating in the pharmaceutical industry include: AbbVie; AstraZeneca; Bristol Myers Squibb; Eli Lilly and Company; Johnson & Johnson; Merck & Co.; Novartis; Pfizer; Roche; Sanofi. The worldwide pharmaceutical market is characterized by traditional large-cap and highly innovative companies. Pfizer, Roche and J&J are well-known diversified companies in pharmaceuticals, medtech and consumer health with stability of scale. Merck & Co., Bristol Myers Squibb and AstraZeneca are major players treating cancer and the immune systems, which drives growth through their products and targeted biologics. Novartis and Sanofi combine legacy brands with next-generation gene therapies and vaccines. AbbVie is building that business and expanding in neuroscience and aesthetics. Meanwhile, Eli Lilly and Company emerges as a growth contributor in neuroscience and metabolic disorders, diabetes and obesity. This is a R&D competitive environment, with M&A to diversify pipelines and affected by biosimilars, pricing pressures in major markets.

Key Players

- AbbVie

- AstraZeneca

- Bristol Myers Squibb

- Eli Lilly and Company

- GSK

- Johnson & Johnson

- Merck & Co.

- Novartis

- Pfizer

- Roche

- Sanofi

Industry Developments

- February 2026: Bora Pharmaceuticals and GSK collaborated to a five-year manufacturing partnership, providing GSK with access to multiple Bora sites, including a new oral solid dose site located in Minnesota.

- December 2025: Eli Lilly invested USD 6 billion in a new manufacturing facility in Huntsville, Alabama, by December 2025. The site will manufacture synthetic and peptide drugs, such as orforglipron, an oral GLP-1 receptor agonist that is anticipated to be filed for regulatory approval for obesity.

Pharmaceutical Market Segmentation

By Molecule Type Outlook (Revenue, USD Billion, 2021–2034)

- Biologics & Biosimilars (Large Molecules)

- Monoclonal Antibodies

- Vaccines

- Cell & Gene Therapy

- Others

- Conventional Drugs (Small Molecules)

By Product Outlook (Revenue, USD Billion, 2021–2034)

- Branded

- Generic

By Type Outlook (Revenue, USD Billion, 2021–2034)

- Prescription

- OTC

By Disease Outlook (Revenue, USD Billion, 2021–2034)

- Cardiovascular diseases

- Cancer

- Diabetes

- Infectious diseases

- Neurological disorders

- Others

By Route of Administration Outlook (Revenue, USD Billion, 2021–2034)

- Oral

- Topical

- Parenteral

- Inhalations

- Other

By Age Group Outlook (Revenue, USD Billion, 2021–2034)

- Children & Adolescents

- Adults

- Geriatric

By Distribution Channel Outlook (Revenue, USD Billion, 2021–2034)

- Hospital Pharmacy

- Retail Pharmacy

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Pharmaceutical Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 1,720.86 Billion |

| Market Size in 2026 | USD 1,821.59 Billion |

| Revenue Forecast by 2034 | USD 2,892.81 Billion |

| CAGR | 5.94% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The global market size was valued at USD 1,720.86 billion in 2025 and is projected to grow to USD 2,892.81 billion by 2034.

The global market is projected to register a CAGR of 5.94% during the forecast period.

North America led the global market in 2025, holding a 40.98% revenue share.

A few of the key players in the market are AbbVie; AstraZeneca; Bristol Myers Squibb; Eli Lilly and Company; Johnson & Johnson; Merck & Co.; Novartis; Pfizer; Roche; Sanofi.

The conventional drugs segment accounted for 53.67% revenue share in 2025.

The generic segment is expected to witness the fastest growth during the forecast period at a CAGR of 6.94%.

Download Sample Report of Pharmaceutical Market

Please fill out the form to request a customized copy of the research report.