Pipeline Integrity Management Market Research Report, 2026-2034

REPORT DETAILS

Pipeline Integrity Management Market Summary

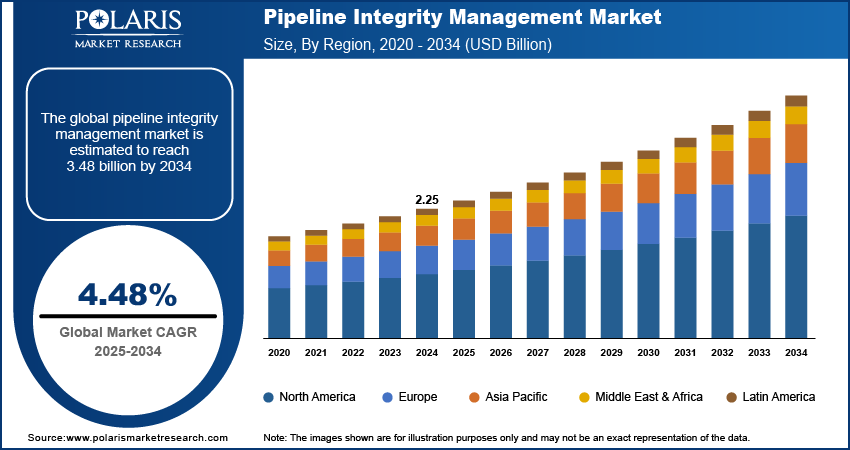

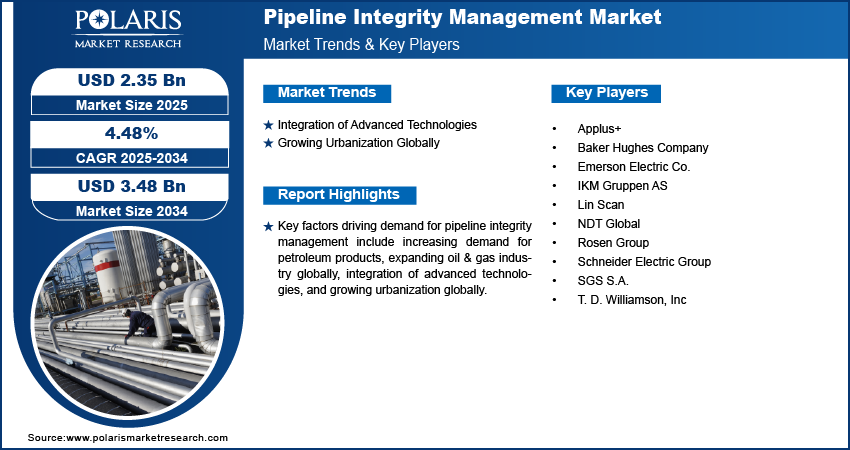

The global pipeline integrity management market size was valued at USD 2.35 billion in 2025. The market is projected to grow at a CAGR of 4.48% from 2026 to 2034. Key factors driving demand for pipeline integrity management include increasing demand for petroleum products and the expanding oil & gas industry globally. The market is also benefiting from the integration of advanced technologies and growing urbanization worldwide.

Market Statistics

Key Takeaways

- North America accounted for a 39.2% market share in 2025. This is attributed to its aging pipeline infrastructure and stringent regulatory requirements.

- Europe is projected to witness rapid growth at a 5.1% CAGR. This is owing to its extensive pipeline network and stringent EU regulations.

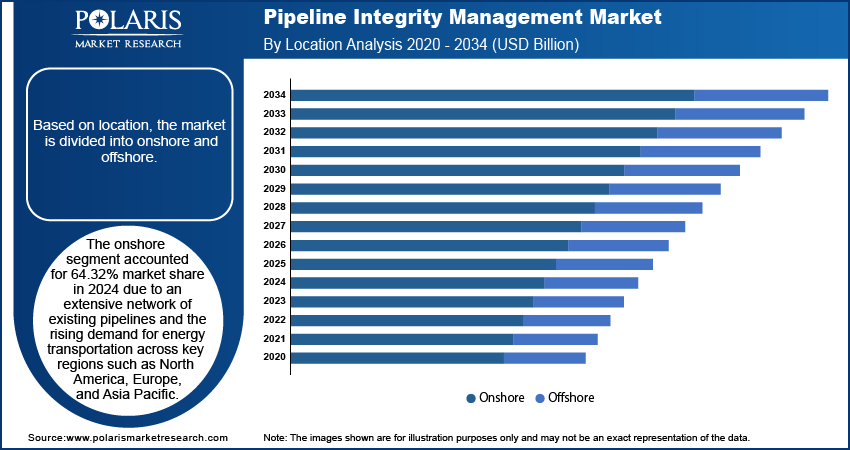

- The onshore segment accounted for a 72.8% market share in 2025. The rising demand for energy transportation across key regions contributes to the segment’s leading position.

- The offshore segment is projected to grow at a robust 5.4% CAGR. This is due to the increasing deepwater exploration activities and investments in offshore oil & gas infrastructure.

The inspection service segment held the largest share of 41.6% in 2025. The increasing need for proactive maintenance and regulatory compliance across aging pipeline networks drives the segment’s leading position.

Industry Dynamics

- The rising integration of pipeline integrity management solutions with advanced technologies is shaping the market landscape.

- Growing urbanization globally has created increased demand for pipelines to deliver natural gas, LNG, and other petroleum products.

- The shift towards green energy is expected to create several market opportunities.

- Cybersecurity risks associated with digital monitoring may present challenges.

AI Impact on Pipeline Integrity Management Market

- AI enables operators to locate pipeline leakages, corrosion, and other weaknesses in pipelines much faster than using traditional inspection techniques.

- It is capable of detecting early indicators of malfunctioning equipment before they result in any major problems.

- The AI technique speeds up the process of pipeline inspections since it processes high volumes of monitoring data in shorter periods.

- This increases safety and ensures smooth operations for companies.

What is Pipeline Integrity Management?

Pipeline integrity management is a systematic and comprehensive approach used by pipeline operators to ensure the safe, reliable, and efficient operation of pipelines throughout their entire lifecycle, from design and construction to operation, maintenance, and decommissioning. The core objective of the management is to prevent failures, leaks, and other incidents that may result in environmental harm, public safety hazards, or major disruptions to the supply of critical resources such as oil and gas.

The increasing demand for petroleum products such as LNG, LPG, and others is driving the market growth. According to the US Energy Information Administration, in the US, propane (a specific type of LPG) consumption reached 1.48 million barrels per day (b/d) in January 2025, the highest January consumption on record since January 2005. This increase in consumption is driving companies to expand their pipeline networks and ensure existing infrastructure operates at higher capacities, which increases the risk of leaks, corrosion, or failures. Pipeline integrity management solutions help operators to tackle these risks or challenges by monitoring, assessing, and maintaining pipelines. Therefore, as demand for petroleum products such as LNG and LPG increases, the adoption of pipeline integrity management solutions also spurs.

The pipeline integrity management demand is driven by the expanding oil & gas industry globally. The oil & gas industry in India is expected to attract US$ 25 billion in investment in exploration and production activities in the coming years. This expansion is leading to the construction of additional pipelines to transport crude oil, natural gas, LNG, and LPG to refineries, processing plants, and export terminals. These new pipelines are usually located in challenging terrains such as deepwater offshore locations, Arctic environments, or seismically active zones, necessitating the use of pipeline integrity management solutions to prevent structural failures. Regulatory agencies worldwide are also tightening compliance requirements with the expanding oil & gas industry, mandating more frequent inspections, risk assessments, and preventive maintenance, leading to market growth.

Traditional Pipeline Maintenance vs Smart Integrity Management

Parameter | Conventional Pipeline Inspection | Advanced Integrity Management System |

| Approach to Monitoring | Periodic checks | Real-time monitoring |

| Detection of Faults | Largely reactive | Largely predictive and preventive |

| Source of Data | Human and manual | Digital and automated |

| Approach to Maintenance | Based on schedules | Based on condition |

| Downtime Risk | Greater chances of unpredictable downtime | Lower chances of downtime due to predictive capabilities |

| Risk of Safety Issues | Dependent on regular inspection | Minimized with advanced tools |

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Industry Dynamics

Integration of Advanced Technologies

Integration of pipeline integrity management solutions with IoT sensors and AI-driven predictive analytics allows operators to detect micro-leaks, corrosion, and structural weaknesses in real time, reducing the risk of catastrophic failures, thereby leading to their high adoption. Additionally, integration with machine learning and deep learning technology is expanding the capabilities of pipeline integrity management solutions as machine learning algorithms process historical and real-time data to predict failure risks. These expanded capabilities are encouraging pipeline operators to adopt machine learning powered pipeline integrity management solutions. Therefore, the integration of pipeline integrity management solutions with advanced technologies is driving the market expansion.

Growing Urbanization Globally

Urban regions heavily depend on pipelines to deliver synthetic natural gas, LPG, and other petroleum products for heating, electricity generation, and industrial use, making pipeline integrity management solutions an essential tool to prevent failures far more disruptive and dangerous. Municipalities and utility companies in the urban areas are adopting PIM solutions to prevent leaks, explosions, and service interruptions. Urban expansion also forces pipelines to navigate complex underground environments crowded with water lines, electrical cables, and transit systems, increasing the risk of damage and requiring advanced integrity management technologies such as GIS mapping, acoustic sensors, and real-time threat detection systems. Stricter safety regulations in urban areas are further pushing energy providers to adopt pipeline integrity management tools to ensure compliance and maintain public trust. World Economic Forum, in its 2022 report, stated that the share of the world’s population living in cities is expected to rise to 80% by 2050, from 55% in 2022. Therefore, as urbanization expands, the need for safe, efficient, and resilient pipeline networks makes pipeline integrity management a crucial investment for sustainable urban development.

Source: Polaris Market Research Analysis

Segmental Insights

By Location Analysis

The onshore segment accounted for 72.8% market share in 2025 due to an extensive network of existing pipelines and the rising demand for energy transportation across key regions such as North America, Europe, and Asia Pacific. The expansion of shale gas production, particularly in the US, and the need to maintain aging infrastructure, drove investments in inspection, maintenance, and monitoring solutions at onshore locations. Governments and operators further prioritized onshore locations as they are more accessible and cost-effective to manage compared to offshore alternatives.

The offshore segment is projected to grow at a robust pace of 5.4% in the coming years, owing to the increasing deepwater exploration activities and the development of new oil and gas fields in regions such as the North Sea, Gulf of Mexico, and West Africa. Harsh environmental conditions at offshore locations and stricter regulatory standards are pushing operators to adopt pipeline integrity assessment tools. Additionally, the growing focus on renewable energy integration, such as offshore wind farms connected via subsea pipelines, is projected to fuel demand for robust integrity management solutions for offshore locations.

By Service Analysis

The inspection service segment held the largest share of 41.6% in 2025 due to the increasing need for proactive maintenance and regulatory compliance across aging pipeline networks. Advanced technologies such as smart pigging, drones, and satellite-based monitoring gained traction, enabling operators to detect corrosion, cracks, and other defects with higher accuracy. Governments in North America and Europe imposed stricter safety standards, mandating frequent inspections to prevent leaks and spills, particularly in high-risk areas. Additionally, the rise of digitalization and predictive analytics allowed companies to optimize inspection schedules, reducing downtime while enhancing safety, which further contributed to the dominance of the segment.

The repairs & refurbishment segment is projected to hold 22.13% market share in 2034 due to the shifting focus from detection to corrective actions. Many pipelines worldwide are reaching the end of their operational lifespan, requiring extensive repairs & refurbishment to extend usability. Innovations in composite repair systems and robotic welding technologies are reducing costs and downtime, making refurbishment more efficient. Furthermore, the increasing adoption of renewable energy sources, such as hydrogen and biofuels, is necessitating pipeline modifications to handle new types of transportation systems, contributing to segment growth.

Source: Polaris Market Research Analysis

Regulatory Compliance and Safety Standards

Regulatory compliance and safety standards play an essential role in the management of pipeline integrity. Governments and organizations within the pipeline industry set out strict regulations in order to ensure pipeline safety, environmental protection, and effective operation. Operators of the pipeline are required to comply with regulatory provisions for pipeline inspection, leak detection, corrosion protection, risk assessment, and emergency response, as well as regular maintenance of pipelines. All these activities are aimed at reducing the risk of pipeline failure and associated threats. Due to growing concerns about aged pipelines and their impact on public safety, investments are being made by companies in developing advanced monitoring and pipeline assessment techniques.

Regional Analysis

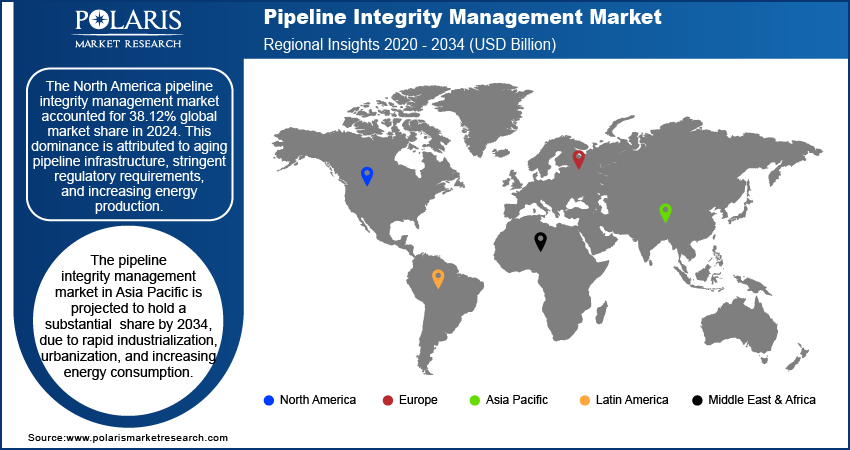

The North America pipeline integrity management market accounted for 39.2% global market share in 2025. This dominance is attributed to aging pipeline infrastructure, stringent regulatory requirements, and increasing energy production. The US and Canada have vast pipeline networks, many of which are decades old, necessitating regular inspections and maintenance to prevent leaks and ruptures. Regulations such as the Pipeline and Hazardous Materials Safety Administration (PHMSA) mandated strict compliance, pushing operators to adopt advanced pipeline integrity management solutions. Additionally, the growth in shale gas and oil production in the region increased the need for reliable pipelines and their management solutions.

US Pipeline Integrity Management Market Insight

The pipeline integrity management market in the US captured 75.6% share in 2025, as it is heavily influenced by federal and state regulations, particularly those enforced by PHMSA under the Pipeline Safety Act. The increasing frequency of pipeline incidents has led to public and governmental pressure for stricter oversight, leading to market growth. The expansion of natural gas pipelines, driven by the shale boom, further propelled demand for pipeline management solutions. Tools such as inline inspection tools and predictive analytics are being widely adopted in the country to enhance monitoring and reduce risks, supporting market dominance.

Europe Pipeline Integrity Management

The pipeline integrity management market in Europe is projected to grow at a robust pace of 5.1% in the coming years, owing to the extensive pipeline network, along with stringent EU regulations aimed at ensuring safety and environmental protection. The European Union’s Third Energy Package and the Gas and Oil Pipeline Safety Directives are imposing rigorous inspection and maintenance requirements, fueling market revenue. Additionally, Europe’s shift toward renewable energy and hydrogen transportation is necessitating modifications in existing pipelines, driving the need for advanced integrity management solutions.

UK Pipeline Integrity Management Market Overview

The demand for pipeline integrity management in the UK is driven by a combination of aging infrastructure, stringent regulatory frameworks, and evolving energy transition initiatives. The UK’s extensive pipeline network, including critical oil and gas transmission systems, requires continuous monitoring and maintenance to prevent leaks, corrosion, and catastrophic failures. Additionally, the UK’s shift toward low-carbon energy, including hydrogen blending and carbon capture and storage (CCS) projects, is necessitating modifications to existing pipelines, further propelling the need for robust pipeline integrity management solutions. The growing emphasis on energy security and reducing methane emissions is further boosting pipeline integrity management tools adoption in maintaining the reliability of pipeline infrastructure.

Asia Pacific Pipeline Integrity Management Market

The pipeline integrity management market in Asia Pacific is projected to grow at a CAGR of 6.28% by 2034, due to rapid industrialization, urbanization, and increasing energy consumption. United Nations Human Settlements Programme in its report stated that by 2050, the urban population in Asia is expected to grow by 50%. Countries such as China, India, and Australia are expanding their oil and gas pipeline networks to meet growing energy needs, necessitating the need for integrity management solutions. Government regulations in the region are further mandating regular inspections and risk assessments, thereby driving the market. Additionally, the rise of liquefied natural gas (LNG) infrastructure and cross-border pipelines, such as those between China and Russia, is further emphasizing the need for advanced pipeline integrity management solutions in the region to ensure operational safety and efficiency.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The pipeline integrity management (PIM) market is highly competitive, with key players leveraging product portfolio expansion, strategic partnerships, and mergers and acquisitions (M&A) to strengthen their positions. Major companies such as Baker Hughes, Schlumberger, and Emerson are continuously broadening their service offerings through technological innovation and product diversification. These expansions are allowing firms to offer end-to-end solutions, from inspection to maintenance, enhancing customer retention and attracting new clients. Strategic partnerships are another critical growth strategy, enabling companies to combine expertise and access new regions. These partnerships further help companies fill technological gaps and reduce R&D costs.

Applus+; Baker Hughes Company; Emerson Electric Co.; IKM Gruppen AS; Lin Scan; NDT Global; Rosen Group; Schneider Electric Group; SGS S.A.; and T. D. Williamson, Inc. are among the major companies operating in the pipeline integrity management market.

Key Players

- Applus+

- Baker Hughes Company

- Emerson Electric Co.

- IKM Gruppen AS

- Lin Scan

- NDT Global

- Rosen Group

- Schneider Electric Group

- SGS S.A.

- T. D. Williamson, Inc.

Industry Developments

- April 2026: KROHNE showcased its next-gen pipeline monitoring and leak detection systems at the 21st Pipeline Technology Conference in Berlin 2026. It also highlighted how modern LDS approaches enable operators to achieve efficient, cost-effective monitoring. (source: krohne.com) .

Pipeline Integrity Management Market Segmentation

By Location Outlook (Revenue, USD Billion, 2021–2034)

- Onshore

- Offshore

By Service Outlook (Revenue, USD Billion, 2021–2034)

- Inspection Service

- Cleaning Service

- Repairs & Refurbishment

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Netherlands

- Asia Pacific

- China

- India

- Japan

- South Korea

- Indonesia

- Malaysia

- Latin America

- Argentina

- Brazil

- Mexico

- Middle East & Africa

- UAE

- Saudi Arabia

- Israel

- South Africa

Pipeline Integrity Management Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 2.35 Billion |

| Market Size in 2026 | USD 2.49 Billion |

| Revenue Forecast by 2034 | USD 3.48 Billion |

| CAGR | 4.48% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Pipeline Integrity Management Market FAQ's

The global market size was valued at USD 2.35 billion in 2025 and is projected to grow to USD 3.48 billion by 2034.

The global market is projected to register a CAGR of 4.48% during the forecast period.

North America dominated the market with 39.2% share in 2025.

A few of the key players in the market are Applus+; Baker Hughes Company; Emerson Electric Co.; IKM Gruppen AS; Lin Scan; NDT Global; Rosen Group; Schneider Electric Group; SGS S.A.; and T. D. Williamson, Inc.

The onshore segment dominated the market with 72.8% share in 2025.

The repairs & refurbishment segment is expected to witness the fastest growth during the forecast period.

Pipeline integrity management is a systematic approach ensuring safe, reliable, and efficient pipeline operation throughout its lifecycle, preventing failures, leaks, and incidents that could cause environmental harm or public safety hazards.

Key trends include IoT and AI-driven predictive analytics integration, rising petroleum demand, expanding oil and gas infrastructure globally, stricter regulatory compliance requirements, and growing urbanization driving advanced pipeline inspection and maintenance solutions.

Download Sample Report of Pipeline Integrity Management Market

Please fill out the form to request a customized copy of the research report.