Silicon Carbide Market Size & Growth Analysis Report, 2026-2034

REPORT DETAILS

REPORT DETAILS

Silicon Carbide Market Summary

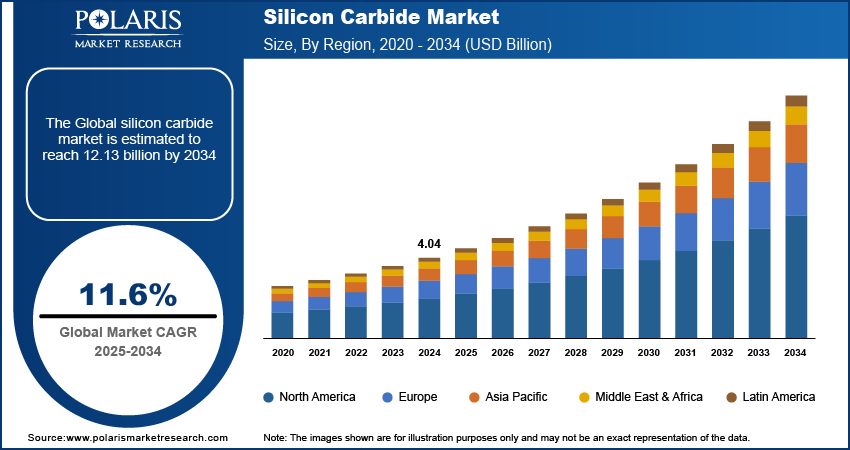

The global silicon carbide market is estimated at around USD 2.06 billion in 2025, with steady growth anticipated during 2026–2034. The market is projected to reach USD 3.11 billion by 2034, expanding at a CAGR of 4.68% during the forecast period. Market expansion is supported by rising adoption of silicon carbide power devices in electric vehicles, renewable energy systems, industrial power electronics, and high-efficiency semiconductor applications.

Market Statistics

Key Takeaways

- Asia Pacific dominated the silicon carbide market in 2025, accounting for approximately 41.80% of global revenue share, driven by strong semiconductor manufacturing capacity, expanding electric vehicle production, and growing investments in power electronics.

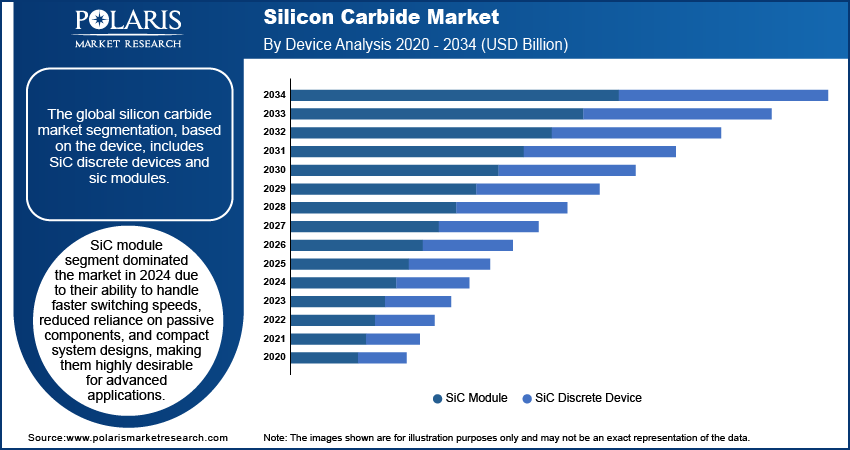

- The SiC modules segment dominated the market in 2025 with a revenue share of approximately 38.60%, supported by extensive use in automotive traction inverters, renewable energy systems, and industrial power applications.

- The automotive segment led the market in 2025, holding an estimated 44.30% revenue share, owing to rising deployment of silicon carbide devices in electric vehicle powertrains, onboard chargers, and fast-charging infrastructure.

- The above 150 mm wafer segment is projected to witness the fastest growth, registering a CAGR of 16.40% during the forecast period, driven by the industry's transition toward larger wafer diameters, improved manufacturing efficiency, and lower production costs.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observation

What is Silicon Carbide?

Silicon carbide is an artificial substance made of silicon and carbon. It has a great thermal conductivity, high voltage endurance, high switching efficiency, and high tolerance to severe temperatures. This product finds application in power semiconductors, powertrains of electric vehicles, energy technologies, motor drives in industry, aerospace products, and other fields that need ceramics with high heat resistance.

The value chain of silicon carbide starts with suppliers of raw materials, continues with companies producing silicon carbide crystals, companies producing wafers from crystals, suppliers of epitaxy services, semiconductor device manufacturers, companies developing modules from these devices, along with distributors and users.

Market growth is driven by the increasing trend towards electrification in transport, automation, and power infrastructure. Electric car companies are relying on silicon carbide-based components for their cars to maximize range and charging capabilities. Simultaneously, renewable energy firms, equipment manufacturers, and data centers are using silicon carbide technology for greater efficiency and reliability.

Source: Polaris Market Research Analysis

Industry Dynamics

- Rising adoption of silicon carbide devices in electric vehicle powertrains is supporting market expansion.

- Growth in renewable energy installations is increasing the use of silicon carbide power conversion systems.

- High manufacturing costs and complex crystal-growth processes continue to challenge industry participants.

- Expansion of 200 mm wafer production capacity is creating new revenue opportunities across the value chain.

AI Impact on Silicon Carbide Market

- The AI data centers are promoting the usage of silicon carbide power devices for power distribution units, server power supplies, and cooling systems.

- Systems powered by machine learning are making silicon carbide wafer inspection, defect identification, and yield management more efficient.

- The semiconductor design software, powered by artificial intelligence, is helping enhance SiC MOSFET and power module development.

- Predictive maintenance technology backed up by AI is increasing the reliability and lifespan of silicon carbide-based industrial power equipment.

- Increasing investments in AI hardware are generating more demand for power semiconductors, which favor the use of silicon carbide materials.

Silicon Carbide Market Driver Impact Analysis

| Silicon Carbide Growth Driver | Indicative CAGR Contribution | Primary Geographic Relevance | Impact Timeline |

| Adoption of SiC traction inverters in 800-volt EV platforms | +3.00% | China, Europe, U.S., South Korea | Short to medium term |

| Conversion from 150 mm to 200 mm SiC manufacturing | +2.30% | U.S., Europe, Japan, South Korea | Medium term (2–4 years) |

| Expansion of solar, storage, and grid power conversion | +1.80% | China, Europe, India, U.S. | Medium to long term |

| Higher-efficiency power supplies for AI data centers | +1.40% | U.S., East Asia, Western Europe | Short to medium term |

| Public subsidies for wide-bandgap semiconductor capacity | +1.20% | U.S., EU, Japan, China | Short term (ongoing) |

| Use of SiC ceramics in high-temperature industrial systems | +0.80% | Asia Pacific, Europe, North America | Long term (structural) |

* Indicative estimates based on market context and analyst judgment. Figures reflect relative driver weight, not additive CAGR contributions. Source: Polaris Market Research Analysis.

Silicon Carbide Market Drivers, Restraints and Opportunities

Rising Adoption of Silicon Carbide in Electric Vehicles

Increasing number of electric cars has led to a greater need for silicon carbide power semiconductors in automotive supply chains. According to data from the International Trade Agency, sales of electric cars were above 20 million units in 2025, which was 20% more than in the previous year, 2024(Source:www.iea.org).Silicon carbide technology helps save energy, lower power loss, and allows working at higher voltages. Silicon carbide semiconductors have been employed for the creation of inverters, charging stations, and DC/DC converters for automobiles in order to enhance their efficiency and increase their battery life.

Expansion of Renewable Energy and Power Electronics Infrastructure

Increasing demand for solar power, energy storage, industrial automation, and smart grids is expected to support wider adoption of silicon carbide solutions. According to the Renewable Energy Institute, global investments in energy sources will continue to grow and reach USD 3.4 trillion by the end of 2026, which is 5% higher compared to 2025(Source:www.semiconductors.org).Renewable energy power systems and industrial machinery need high-performance switching devices for harsh environments.

High Manufacturing Costs and Yield Constraints

Silicon carbide substrate manufacturing is an involved process entailing sophisticated crystal-growing techniques, specialized wafer manufacturing methods, and exacting quality demands. Defects in manufacturing, low yields in wafers, and capital-intensity of manufacture all lead to higher cost structures thus hindering the market growth.

Opportunity

Transition Toward Larger Diameter Silicon Carbide Wafers

Industry wide adoption of larger diameter silicon carbide wafers instead of conventional wafer formats opens up new opportunities for growth in the industry. Many manufacturers have been investing on developing capabilities to produce wafers of 200 mm and 300 mm in order to increase wafer utilization and increase device manufacturing. In January 2026, Wolfspeed launched single crystal silicon carbide wafer measuring 300 mm (12 inches)(Source:www.wolfspeed.com).Larger diameter wafers, allows semiconductor firms to boost productivity while meeting future demands from the automotive and energy industries.

Additional Market Trends

-

Vertical Integration Across the Supply Chain

Semiconductor manufacturers are seeking vertical integration of substrate manufacturing, epitaxy growth, device fabrication, and packaging processes. Vertical integration helps mitigate potential material shortages.

-

Long-Term Supply Agreements

Automobile manufacturers and semiconductor providers have been increasingly forming multi-year purchase agreements for silicon carbide products. The Semiconductor Industry Association reports that the U.S. companies in the semiconductor industry have initiated over 140 projects in 30 states in the past few years, for a total of over USD 645.3 billion worth of private investment(Source:www.semiconductors.org).These arrangements provide revenue visibility for manufacturers and reduce supply-chain uncertainty.

Source: Polaris Market Research Analysis

Segment and Regional Leaders at a Glance

According to Polaris Market Research, Asia Pacific leads the long-term care market while North America is the fastest-growing region.

- Dominant Region: Asia Pacific

- Fastest-Growing Region: North America

- Largest Device Segment: SiC Modules

- Largest Wafer Size Segment: Up to 150 mm Wafers

- Largest Application Segment: Automotive

Silicon Carbide Market Segmentation Analysis

The report offers detailed insights into the silicon carbide market by device type, wafer size, and application in order to identify lucrative and fast-growing segments in terms of revenue.

Silicon Carbide by Device

What is the Largest Device Segment in the Silicon Carbide Market?

The SiC modules segment dominated the market in 2025 with a revenue share of approximately 38.60% due to Its high popularity is related to increasing implementation of EVs, industrial drives, inverters in renewable energy applications, and railway electrification systems. SiC modules provide superior thermal performance, high power density, and improved efficiency in high-voltage applications.

Which Devices Segment is Growing Fastest in the Silicon Carbide Market?

SiC discrete devices segment is projected to grow at the fastest CAGR during the forecast period. Growing deployment of SiC MOSFETs and Schottky diodes in power conversion applications is supporting segment expansion. For example, in June 2026, ROHM Semiconductor introduced TSC3PAK, the new package with 4th generation of company's SiC MOSFET, which utilizes top-side cooling structure and allows 1200V voltage withstand and improved heat dissipation capability(Source:www.rohm.com).

Silicon Carbide by Wafer Size

What is the Largest Wafer Size Segment in the Silicon Carbide Market?

The up to 150 mm wafer segment held the largest market share in 2025 on account of its well-established ecosystem and high installed manufacturing capacity. The majority of existing SiC manufacturing plants continue to operate based on 150 mm wafer technology. The segment benefits from mature production processes, existing customer qualification programs, and strong supply chain integration.

Which Wafer Size Segment is Growing Fastest in the Silicon Carbide Market?

The above150 mm wafers is expected to grow at the highest CAGR during the forecast period. Industry players are making huge investments in the development of large-sized wafer slices to enhance efficiency in manufacturing and increase production levels.

Source: Polaris Market Research Analysis

Silicon Carbide by Application

What is the Largest Application Segment in the Silicon Carbide Market?

The automotive segment led the market in 2025, holding an estimated 44.30% revenue share, due to the incorporation of silicon carbide parts into the systems of electric vehicle manufacturers is important for efficient battery operations and fast charging abilities. SiC power devices are widely used in traction inverters, onboard chargers, and battery management systems.

Which Application Segment is Growing Fastest in the Silicon Carbide Market?

Energy and power segment is projected to grow at the fastest CAGR during the forecast period. Increasing investments in renewable-energy projects, battery energy storage systems, smart grid infrastructure, and utility-scale power conversion equipment are supporting segment expansion.

Segment Performance Summary

| Segment Dimension | Category | 2025 Status | Forecast Trend | Specific Growth Mechanism |

| By Device | SiC Modules | Largest segment, 26.56% share | CAGR 4.55% | High-power switching and automotive inverter adoption |

| By Device | SiC Discrete Devices | Emerging high-growth segment | CAGR 5.12% | Wider deployment of SiC MOSFETs and diodes |

| By Wafer Size | Up to 150 mm | Dominated the market in 2025 | CAGR 4.21% | Established manufacturing capacity |

| By Wafer Size | Above 150 mm | Fastest-growing category | CAGR 5.48% | Higher wafer output and improved manufacturing efficiency |

| By Application | Automotive | Largest segment, 43.12% share | CAGR 4.96% | EV powertrain and charging infrastructure deployment |

| By Application | Energy & Power | High-growth segment | CAGR 5.25% | Renewable energy and grid modernization investments |

The market is gradually shifting toward larger wafer formats and advanced power-device architectures. Car manufacturers keep representing the major sources of demand, while applications in renewable energy generation and power systems are becoming important drivers of growth.

Regional Analysis

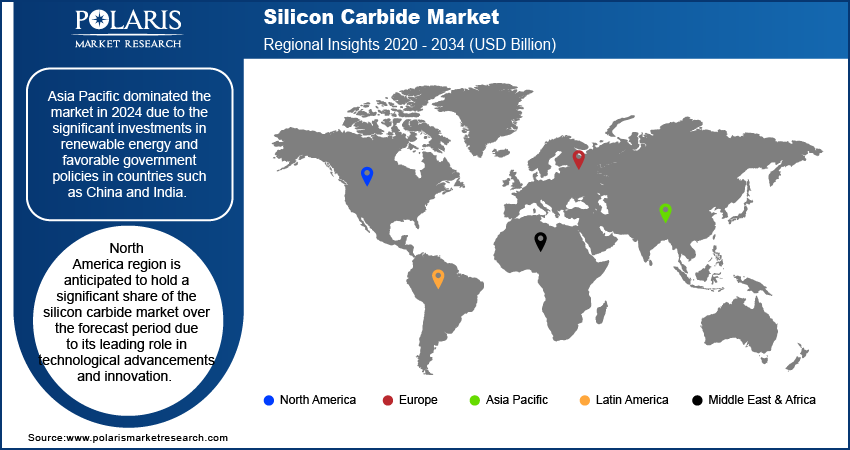

Asia Pacific Silicon Carbide Market Analysis

Asia Pacific dominated the silicon carbide market in 2025, accounting for approximately 41.80%. This is due to the region’s favorable conditions in terms of semiconductor manufacturing, electric vehicle production, and investments in power electronics. As reported by the Asian Development Bank, East and Southeast Asia contributed over 80% of global semiconductor production(Source:blogs.adb.org).China, Japan, South Korea, and Taiwan have continued to serve as prominent locations for the manufacturing of wafers and semiconductors.

China Silicon Carbide Market Insight

China is the largest contributor in Asia Pacific region due to its dominance in the manufacturing of electric vehicles, batteries, and power semiconductors. As per IEA, China still holds its position as the leading producer of electric cars globally with an 70% share of production in 2024(Source:www.iea.org).Local manufacturers are increasingly ramping up the manufacturing capabilities of silicon carbide wafers and devices in order to achieve supply chain independence. Growing investments in charging infrastructure, renewables, and industrial automation projects are further boost silicon carbide technology adoption in the region.

North America Silicon Carbide Market Assessment

North America contributed 19.21% to the global market share in 2025. Market growth is driven by high demand for electric vehicles, increase in semiconductor investments, and government policies related to local production. According to the Semiconductor Industry Association, the U.S. is projected to experience 203% increase in manufacturing capability of semiconductors between 2022 and 2032, the fastest among all countries globally.(Source:www.semiconductors.org).The US continue to dominated the industry driver by rising investment in silicon carbide wafers, power devices, and semiconductor research.

U.S. Silicon Carbide Market Insight

The US continue attracting large investments along the entire value chain of silicon carbide materials. Investments made by federal government programs and private companies into semiconductors are prompting the establishment of wafer fabrication and device production plants in the country. The growing use of silicon carbide products in electric vehicles, industrial power conversion equipment, and energy infrastructure applications will promote growth prospects for years to come.

Europe Silicon Carbide Market

The European region is expected to see large amounts of growth during the forecast period, propelled by increasing manufacturing of electric vehicles, growth of semiconductor facilities, and investments into renewable energy resources. As per reports from the International Energy Agency (IEA), Europe has been making greater strides toward investing in clean energy sources, totaling almost USD 390 billion in the year 2025(Source:www.iea.org).Germany, Italy, France, and the UK form important segments of the European market.

Germany Silicon Carbide Market Insight

Germany acts as an important hub in terms of automotive innovation and manufacturing. Germany’s established electric vehicle environment, along with investments in power electronics and semiconductors, is driving demand for silicon carbide. Companies involved in automotive original equipment manufacturer (OEM) production, as well as Tier-1 suppliers, are increasingly incorporating silicon carbide technology in new vehicles.

Latin America Silicon Carbide Market

Latin America is expected to experience steady market growth due to expanding renewable energy capacity and increasing industrial modernization efforts. Brazil and Mexico remain the primary markets within the region. Investments in solar energy projects, industrial automation systems, and power infrastructure upgrades are gradually increasing demand for advanced semiconductor technologies, including silicon carbide devices.

Middle East & Africa Silicon Carbide Market

The Middle East & Africa market is projected to expand at a moderate pace during the forecast period. Growth is supported by investments in renewable energy projects, industrial diversification initiatives, and power infrastructure development. As per the statistics of the International Energy Agency, investments made in the power generating systems of the Middle East region amounted to USD 44 billion in 2024 with an estimated increase of 50% up to 2035.(Source: www.iea.org)The nations of Saudi Arabia, United Arab Emirates, and South Africa plan to incorporate high-level power electronics in their systems for economic sustainability.

Regulatory Environment Heatmap

| Region/Country | Policy Environment | Program | Market Implication | Trend |

| US | Favorable | CHIPS and Science Act | Supports domestic wafer and device manufacturing | Expanding |

| European Union | Favorable | European Chips Act | Encourages semiconductor capacity growth | Expanding |

| Italy | Favorable | STMicroelectronics Catania Incentive Program | Supports 200 mm SiC production | Expanding |

| Germany | Favorable | Semiconductor State Aid Programs | Encourages automotive semiconductor investments | Expanding |

| China | Favorable | National IC Industry Investment Fund | Expands domestic SiC manufacturing | Expanding |

| Japan | Favorable | METI Semiconductor Programs | Supports power semiconductor production | Expanding |

| South Korea | Favorable | K-Semiconductor Strategy | Encourages semiconductor investments | Developing |

| India | Neutral to Favorable | India Semiconductor Mission | Supports future semiconductor ecosystem growth | Early Stage |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Competitive Landscape & Key Players

There is moderate concentration of players within the silicon carbide industry, and competition among the players revolves around manufacturing capacity, quality of the wafers, performance of the devices, and customer commitments. Companies are investing heavily in crystal-growth technologies, wafer production facilities, and semiconductor fabrication capabilities to strengthen market positions.

Major companies operating in the silicon carbide market include Coherent Corp., Fuji Electric Co., Ltd., Infineon Technologies AG, Microchip Technology Inc., Mitsubishi Electric Corporation, Nexperia B.V., onsemi, ROHM Co., Ltd., SK Siltron Co., Ltd., STMicroelectronics N.V. and others.

Competitive Market Snapshot

| Company | Market Position Tier | Primary Competitive Strength | Geographic Focus |

| STMicroelectronics N.V. | Market Leader | Vertically integrated SiC ecosystem | Europe, China |

| Infineon Technologies AG | Market Leader | Automotive-qualified CoolSiC portfolio | Europe, North America |

| Wolfspeed, Inc. | Leading Challenger | Wafer manufacturing leadership | Global |

| onsemi | Leading Challenger | EliteSiC automotive portfolio | North America, Europe |

| ROHM Co., Ltd. | Leading Challenger | Automotive and industrial modules | Japan, Europe |

| Mitsubishi Electric Corporation | Established Player | High-voltage power modules | Asia Pacific |

| Coherent Corp. | Established Player | Advanced substrate technologies | Global |

* Estimated market positioning based on revenue scale, geographic reach, and service breadth. Not ranked by precise market share percentage. Source: Polaris Market Research Analysis.

Key Players

- Coherent Corp.

- Fuji Electric Co., Ltd.

- Infineon Technologies AG

- Microchip Technology Inc.

- Mitsubishi Electric Corporation

- Nexperia B.V.

- onsemi

- ROHM Co., Ltd.

- SK Siltron Co., Ltd.

- STMicroelectronics N.V.

- Wolfspeed, Inc.

- X-FAB Silicon Foundries SE

Trends & Future Outlook

Sustainability

- Electric vehicle suppliers are leveraging silicon carbide semiconductors to achieve better efficiency and lower power losses in their vehicles.

- Energy technology providers in renewable energies are using silicon carbide-based power electronics for improved efficiency and achieving grid decarbonization targets.

Innovation

- The move towards 200 mm silicon carbide wafers will help enhance manufacturing efficiency and prepare for future capacity expansion.

- SiC MOSFET devices, high voltage modules, and advanced power conversion solutions can increase application opportunities.

Silicon Carbide Technology & Innovation Landscape

The market development for silicon carbide involves different steps starting from crystal growth to device manufacturing and integration into modules. Wafer diameter, power density, and device design developments influence industry competitiveness.

| Technology | Adoption Stage | Recent Development | Market Impact |

| 200 mm SiC Wafers | Growing Deployment | STMicroelectronics expanded 200 mm production initiatives (2025) | Higher manufacturing efficiency |

| Commercial 200 mm Materials | Growing Deployment | Wolfspeed commercialized 200 mm portfolio (2025) | Supports large-scale production |

| 300 mm SiC Wafers | Pilot Stage | Early-stage demonstrations reported (2026) | Long-term output potential |

| Bidirectional SiC Switches | Early Commercial | Infineon launched CoolSiC G2 Switch (2026) | Reduced component count |

| Advanced Automotive Inverters | Growing Deployment | onsemi-Schaeffler collaboration expansion (2025) | Higher vehicle efficiency |

| 10 kV SiC MOSFETs | Early Commercial | High-voltage industrial deployments | Expands utility-scale applications |

Source: Polaris Market Research Analysis

Near-term market development will be driven primarily by 200 mm wafer commercialization and automotive power-electronics adoption. Technologies such as 300 mm wafers remain in the early development stage and are not expected to contribute materially to industry revenues in the immediate future.

Silicon Carbide Buyer Use Cases & Market Entry Barriers

Buyer Use Cases

| Buyer Type | Primary Use Case | Key Insight Sought | Decision Horizon |

| Automotive OEMs | EV platform development | Device supply and pricing | 3–7 Years |

| Semiconductor Manufacturers | Capacity expansion | Wafer demand and utilization | 5–10 Years |

| Wafer Suppliers | Production planning | Diameter transition trends | 5–10 Years |

| Investors | Asset evaluation | Revenue growth and profitability | 3–7 Years |

| Renewable Energy Companies | Power system design | Efficiency and sourcing | 2–5 Years |

| Procurement Teams | Supplier benchmarking | Pricing and availability | 1–3 Years |

Source: Polaris Market Research Analysis

Market Entry Barriers

Silicon carbide business entails high costs of capital, skills in growing crystals, semiconductor expertise, and long qualification process. Customers in the automotive industry need to ensure that strict testing is carried out before vendors qualify.

Furthermore, yield optimization is yet another important obstacle to overcome. Operational expertise is key to production economics, which is determined by defect densities and yields in the wafers.

Premium Insights: Pricing & Investment Outlook

Cost & Pricing Benchmarking

| Product Type | Indicative Price Range (USD) | Primary Cost Driver | Complexity |

| Black Silicon Carbide Powder | USD 1–4/kg | Purity and energy input | Standard |

| Green Silicon Carbide Powder | USD 4–15/kg | Purity and processing | Premium |

| 150 mm SiC Wafer | USD 500–1,500/wafer | Defect density and grade | Semiconductor |

| 200 mm SiC Wafer | USD 1,500–4,000/wafer | Yield and production volume | Advanced Semiconductor |

| SiC MOSFET | USD 5–80/device | Voltage rating and packaging | Commercial |

| SiC Power Module | USD 150–1,500+/module | Power rating and qualification | High-Power |

* Costs vary materially by state, facility quality tier, and payer. Source: Polaris Market Research Analysis.

Pricing across the silicon carbide ecosystem varies significantly according to wafer diameter, defect density, qualification requirements, and customer agreements. Larger-diameter wafers remain more expensive than traditional formats due to lower production volumes and evolving yield profiles.

Investments have continued to be made in substrate and wafer manufacturing capabilities, and semiconductors for cars. Industry players are focusing on securing long-term supply and expanding capacity.

Industry Developments

- June 2026: Wolfspeed launched its Gen 5 silicon carbide (SiC) MOSFET technology, featuring the industry’s lowest RDS(ON) performance and up to 27% higher efficiency compared with previous generations (Source:www.wolfspeed.com).

- June 2026: Infineon Technologies launched the industry’s first silicon carbide bidirectional switch based on CoolSiC G2 technology, designed to improve power conversion efficiency and system integration in advanced energy applications(Source:www.infineon.com).

- June 2026: Bosch launched the third generation of its silicon carbide chips in India, offering about 20% more performance than previous-generation products(Source:www.bosch-presse.de).

Silicon Carbide Market Segmentation

By Device Outlook (Revenue, USD Billion, 2021–2034)

- SiC Modules

- SiC Discrete Devices

- SiC Bare Die

- Others

By Wafer Size Outlook (Revenue, USD Billion, 2021–2034)

- Up to 150 mm

- Above 150 mm

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Automotive

- Energy & Power

- Industrial

- Aerospace & Defense

- Consumer Electronics

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

North America

- US

- Canada

Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- South Korea

- Taiwan

- Australia

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East & Africa

Silicon Carbide Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 2.06 Billion |

| Market Size in 2026 | USD 2.15 Billion |

| Revenue Forecast by 2034 | USD 3.11 Billion |

| CAGR | 4.68% from 2026–2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR |

| Report Coverage | Revenue Forecast, Growth Factors, Competitive Landscape, Industry Trends, and Strategic Analysis |

| Segments Covered | By Device, By Wafer Size, By Application |

| Regional Scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Competitive Landscape | Company Profiling, Product Benchmarking, Financial Analysis, Market Developments, and Strategic Initiatives |

| Report Format | PDF + Excel |

| Customization | Available by Country, Region, and Segment |

FAQ's

• The global silicon carbide market was valued at USD 2.06 billion in 2025 and is projected to reach USD 3.11 billion by 2034.

• The market is projected to grow at a CAGR of 4.68% during 2026–2034.

• Asia Pacific dominated the silicon carbide market in 2025, accounting for approximately 41.80%

• The automotive segment led the market in 2025, holding an estimated 44.30% revenue share

• The SiC modules segment dominated the market in 2025 with a revenue share of approximately 38.60%

• Some of the key players in the market STMicroelectronics N.V., Infineon Technologies AG, Wolfspeed, Inc., onsemi, ROHM Co., Ltd., Mitsubishi Electric Corporation, and Coherent Corp., among others.

• Growth is promoted by the electrification of electric vehicles, growth of renewables, capacity expansions for semiconductors, and high-efficiency power electronics deployments.

• The above 150 mm wafer segment is projected to grow at the fastest CAGR during the forecast period.

Download Sample Report of Silicon Carbide Market

Please fill out the form to request a customized copy of the research report.