Third-Party Risk Management Market Share & Growth Report 2026 - 2034

REPORT DETAILS

Third-Party Risk Management Market Summary

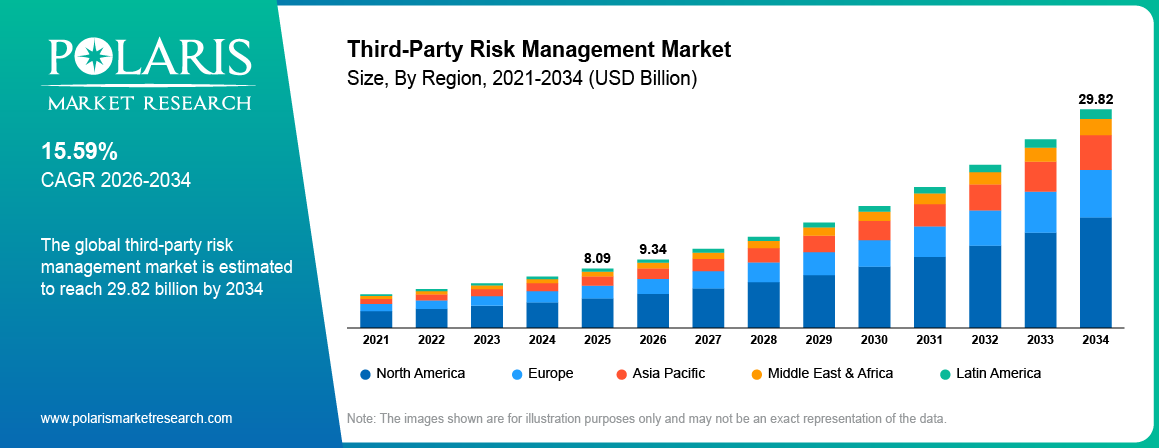

The global third-party risk management market is estimated around USD 8.09 Billion in 2025,?with consistent growth anticipated during 2026–2034. Growth is driven by rising cyber threats across vendor ecosystems and increasing focus on regulatory compliance across industries. The market is projected to grow at a CAGR of 15.59% during the forecast period.

Market Statistics

Key Takeaways

- North America dominated with a market share of 36% in 2025, attributed to strong regulatory frameworks and high cybersecurity investment

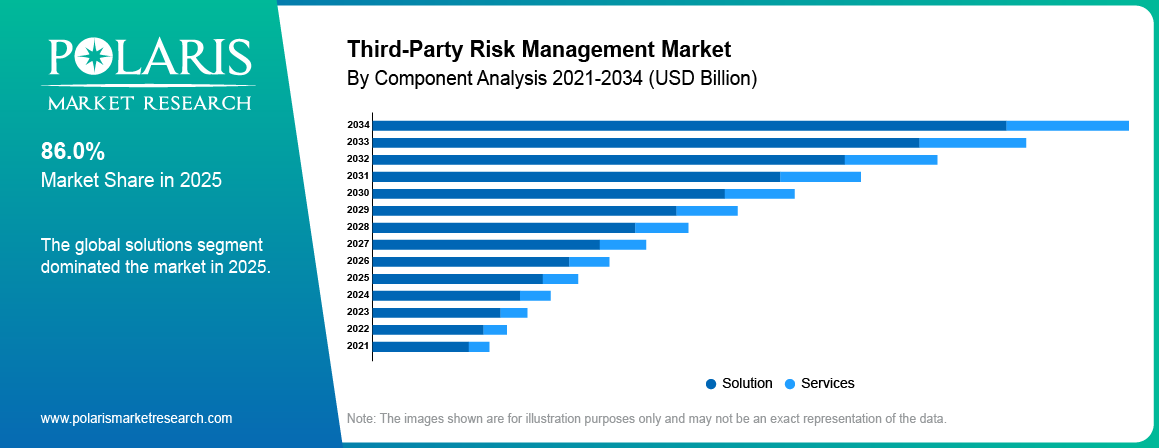

- Solutions segment dominated with a market share of 42% in 2025, driven by rising demand for automated risk assessment and continuous monitoring

- TPRM providers are expected to grow at a CAGR of 14.8% during 2026–2034, supported by increasing investment in AI and analytics for predictive risk detection

- Cloud-based platforms segment accounted for 47% market share in 2025, owing to scalability and real-time risk monitoring capabilities

- Centralized vendor risk management solutions held a share of 39% in 2025, as enterprises focus on improving compliance and operational control

- Automation integration is projected to register a CAGR of 13.5% over the forecast period, strengthening continuous monitoring across third-party networks

Industry Dynamics

- Rising frequency of cyberattacks is increasing demand for third-party risk management solutions

- Strict regulatory frameworks are increasing compliance requirements across industries and strengthening adoption of TPRM platforms

- High implementation cost is creating challenges for adoption among small and mid-sized enterprises

- Advancements in AI-driven analytics and automation are creating long-term growth opportunities in the TPRM market

Market Definition & Scope

What is Third-Party Risk Management (TPRM)?

Third-party risk management (TPRM) refers to a structured process used by organizations to identify, assess, monitor, and reduce risks linked to external vendors, suppliers, and partners. It covers financial, operational, compliance, and cybersecurity risks that may arise when a business depends on third parties. The third-party risk lifecycle includes vendor onboarding, risk assessment, due diligence, continuous monitoring, and risk mitigation.

TPRM has become critical in modern enterprises due to increased reliance on outsourcing and digital ecosystems. Third-party cyber risk has increased with the rise in cloud adoption and data sharing across vendors. Vendor risk management meaning focuses on evaluating vendor reliability and compliance, while supplier risk relates to supply chain disruptions. TPRM seeks to bring all these areas under one umbrella to enhance the organization's visibility and control over the risks.

Why TPRM is Critical in Modern Enterprises

TPRM is very important in the organization as the organization relies on several third-party vendors for its operations. The organization faces risks such as data breaches, regulatory violations, and business disruptions. Third-party cyber risks remain a significant challenge in the organization. The vendors have access to the organization's sensitive systems and data.

Regulatory bodies have introduced strict compliance requirements, which increases the need for strong third-party risk management practices. Companies are adopting automated TPRM solutions to improve risk assessment and monitoring efficiency. A well-defined third-party risk lifecycle supports better decision-making, reduces financial losses, and improves overall enterprise risk management strategies.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

Drivers & Opportunities

Rising frequency of cyberattacks on third-party vendors increases enterprise focus on TPRM adoption: Rising incidents of cyberattacks targeting third-party vendors are increasing enterprise focus on third-party risk management solutions. Organizations are identifying vulnerabilities across vendor networks, which is increasing demand for structured risk assessment and monitoring tools. The exposure of third-party cyber risks has continued to grow due to the increase in data sharing between the organization and its external partners. According to Cybersecurity Ventures, the cost of cybercrime in the world reached USD 10.5 trillion in 2025. The cost has been rising at 15% every year from USD 3 trillion in 2015.

Strict regulatory frameworks increase compliance requirements across industries: Tight regulatory guidelines lead to an increase in compliance needs across industries: Tight regulatory guidelines such as GDPR and HIPAA have led to an increase in compliance needs across industries. It is essential for organizations to ensure compliance among vendors with regard to data privacy. This is where the need for risk management solutions is growing among vendors in terms of audits, reporting, and documentation. This is pressurizing organizations to adopt a formal TPRM framework to mitigate legal and financial risks.

Restraints & Challenges

High implementation costs limit adoption among small and mid-sized enterprises: Implementation cost is hindering the adoption rate among small and mid-sized enterprises: The high implementation cost related to TPRM platforms and integration processes is hindering the adoption rate among small and mid-sized enterprises. Budget constraints are affecting the adoption rate of risk management solutions. The adoption rate is impacted by the budget constraints. The absence of skilled resources to carry out implementation and monitoring has slowed the adoption rate.

Opportunity

Integration of AI and analytics enhances predictive risk assessment capabilities in TPRM platforms: The integration of AI and analytics has improved the predictive risk assessment capabilities in the TPRM system: The integration of AI and analytics has improved the predictive risk assessment capabilities in the TPRM system. Advanced tools in the field of analytics have enabled the early identification of the risks associated with the vendors and the potential threats. For instance, in March 2026, apexanalytix introduced its Risk Response Agent, which uses AI and has the capability to automate action in real time. This has improved the speed and efficiency in the management of third-party risks. This development is improving decision-making and reducing operational risk exposure.

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the third-party risk management market by component, deployment, organization size, and industry vertical to help readers identify the fastest expanding and most attractive demand segments.

By Component

-

Solutions

The solutions segment accounted for the highest share in the market in 2025. This is due to the increased demand for automated risk management and monitoring platforms. Organizations are adopting integrated TPRM solutions to enhance the management of risks associated with the vendors. Additionally, the increased focus on the implementation of a centralized framework for managing risks has positively impacted the segment.

-

Services

Services segment is expected to witness the highest CAGR during the forecast period. The increasing need for consulting, implementation, and managed services is contributing to this growth. Today, there is an increased need for external expertise to manage vendor ecosystems. This is supporting the growth of TPRM service providers.

By Deployment

-

Cloud

Cloud segment held the largest share of the market in 2025. The segment is growing due to an increased need for flexible risk management platforms. Cloud-based solutions support real-time monitoring and data integration across vendor networks. Rising demand for remote access and centralized control is supporting segment growth.

-

On-Premises

On-premises segment is expected to grow at a steady rate during the forecast period. The need for data security and control is providing impetus to this growth. Organizations in regulated industries need on-premise solutions for data privacy.

By Organization Size

-

Large Enterprises

The large enterprises segment had the largest share in the market in 2025, owing to the high complexity in the ecosystems of the vendors and the associated third-party risks. They are using advanced technology in TPRM to efficiently manage the high volume of information associated with the vendors.

-

SMEs

SMEs segment is projected to grow at the fastest CAGR during the forecast period, due to increasing awareness of third-party cyber risks. Small and mid-sized enterprises are adopting cost-effective TPRM technology to gain better visibility over risks. Availability of cloud technology is boosting the small and mid-sized enterprises segment.

By Industry Vertical

-

BFSI

The BFSI segment held the highest share in the market in 2025, driven by the need for regulatory compliance and high data sensitivity. Financial institutions need to continuously monitor risks posed by vendors. Increasing cyber threats are raising demand for TPRM solutions. Strong compliance frameworks are supporting segment growth.

-

Healthcare

Healthcare segment is projected to grow at the fastest CAGR during the forecast period, due to rising focus on patient data security and compliance requirements. Increasing use of third-party service providers is expanding risk exposure. Organizations are adopting TPRM platforms for vendor monitoring. Regulatory pressure is supporting segment growth.

Source: Polaris Market Research Analysis

Regional Analysis

North America Market Assessment

North America third-party risk management market dominated the global market in 2025, driven by strict regulatory enforcement and high cybersecurity risk exposure. The Federal Bureau of Investigation has reported that the total cybercrime cases in the U.S. in 2024 were 859,532. These cases also include close to 4,900 cybercrime attacks on the U.S. critical infrastructure sectors such as manufacturing and healthcare. Additionally, the US has the strongest position in the TPRM industry globally, thanks to the presence of financial institutions and digital infrastructure. Enterprises are investing in automated TPRM platforms to manage complex third-party ecosystems and reduce cyber risk exposure.

Asia Pacific Third-Party Risk Management Market Insights

Asia Pacific third-party risk management market is projected to grow at the fastest CAGR during the forecast period, driven by rapid digital transformation and increasing outsourcing activities. For instance, in April 2026, Microsoft’s USD 5.5 billion investment in Singapore enhances AI and cloud infrastructure, improving cybersecurity and enabling stronger third-party risk management through more secure vendor ecosystems. Moreover, countries such as China and India have also been building a strong vendor ecosystem in the field of IT and financial services. Cybercrime has been on the rise, and the importance of third-party cyber risk assessment and compliance has been gaining more and more traction. Cloud-based TPRM solutions have been gaining traction in the industry.

Europe Third-Party Risk Management Market Overview

Europe's third-party risk management market has significant share. The region has robust regulatory environments and data protection regulations. Data protection regulations such as GDPR are pushing the accountability of third-party data handling and compliances. Countries such as Germany, France, and the UK are focusing on the implementation of continuous monitoring systems in the field of vendor risk audits. The financial sector in these countries is focusing on meeting the regulatory requirements.

Middle East & Africa and Latin America Market Overview

Middle East & Africa and Latin America third-party risk management market are emerging regions, driven by increasing regulatory awareness and cybersecurity investments. Countries in the Middle East region are focusing on improving data protection regulations and vendor risk governance. The region in the Latin American region is witnessing the implementation of compliance-driven third-party risk management practices in the banking and telecom industries. The expansion of digital infrastructure in the region is creating the need for structured third-party monitoring systems.

Source: Polaris Market Research Analysis

Competitive Landscape & Pricing Analysis

The third-party risk management industry exhibits a moderately fragmented market structure. There are cybersecurity-focused vendors, compliance-focused vendors, and integrated GRC vendors. Cybersecurity vendors are focused on threat detection and continuous monitoring. Compliance-focused vendors are focused on audit and reporting compliance. Integrated GRC vendors are focused on integrated risk and compliance management solutions.

New entrants in the market are introducing AI-based risk scoring and due diligence solutions. Predictive analytics is improving early risk detection across vendor networks. Future drivers of growth include AI, automation, and ESG-based risk models. Supply chain risk and Gen AI risk are creating opportunities for advanced TPRM solutions.

Some of the notable companies in the market include RSA Security, BitSight Technologies, SecurityScorecard, OneTrust, NAVEX, SAI360, ProcessUnity, Prevalent, Archer Technologies, MetricStream, LogicGate, UpGuard, and others.

TPRM Framework, Lifecycle & Risk Types

TPRM Lifecycle: Onboarding → Monitoring → Offboarding

The process of third-party risk management follows a lifecycle. Third-party onboarding, continuous monitoring, and offboarding form the lifecycle. Vendor onboarding involves a process of due diligence, risk classification, and compliance. These processes aim to assess the reliability of the vendor. Before the start of the contract, the organization assesses the financial stability and cybersecurity posture of the vendor. This step reduces exposure to high-risk vendors at the entry stage.

The continuous monitoring in TPRM involves the continuous tracking of the performance, security, and compliance of the vendors throughout the term of the contract. This is achieved by utilizing technology that has the capability of detecting changes in risk and alerting accordingly. In TPRM, offboarding refers to the termination of access for the vendors and verification of the handling of the data. This is important for effective supply chain risk management.

Types of Third-Party Risks (Cyber, Operational, Financial, ESG)

The types of third-party risk are categorized as cyber risk, which involves issues like breaches and unauthorized access through the vendor’s systems. Then there is operational risk, which involves issues like disruption in service and failure in delivery by the vendor. Lastly, there is financial risk, which involves issues like vendor instability and bankruptcy.

ESG risk is becoming significant in the business world due to increased focus on environmental, social, and governance standards by regulators. Vendors are assessed based on sustainability standards, ethical business practices, and compliance standards. They are incorporated into the risk management framework for better transparency.

Best Practices for Effective TPRM Implementation

There is a need for a structured approach throughout the vendor lifecycle for TPRM implementation. Organizations are opting for a centralized platform to manage vendor information, risk scores, and compliance. The standardization of risk assessment for vendor onboarding helps to maintain consistency in risk evaluation. Clear risk classification models enable faster decision-making processes.

Continuous monitoring TPRM solutions enable better identification of risks. The incorporation of AI and analytics helps to improve risk reporting. Good governance practices and collaboration help in the efficient management of supply chain risks. These practices help in the efficient management of third-party risks.

Key Players

- Archer Technologies

- BitSight Technologies

- LogicGate

- MetricStream

- NAVEX

- OneTrust

- Prevalent

- ProcessUnity

- RSA Security

- SAI360

- SecurityScorecard

- UpGuard

Industry Developments

- March 2026: Covéa has selected Shift Technology as its strategic partner in the quest to enhance fraud detection and risk management using AI analytics and automated claims assessment.

- February 2026: CanDeal has partnered with six major banks in Canada to develop a platform for managing third-party risk in a more efficient manner by standardizing vendor due diligence and eliminating redundant compliance processes.

Third-Party Risk Management Market Segmentation

By Component Outlook (Revenue, USD Billion, 2021-2034)

- Solutions

- Services

By Deployment Outlook (Revenue, USD Billion, 2021-2034)

- Cloud

- On-Premises

By Organization Size Outlook (Revenue, USD Billion, 2021-2034)

- SMEs

- Large Enterprises

By Industry Vertical Outlook (Revenue, USD Billion, 2021-2034)

- BFSI

- Healthcare

- IT & Telecom

- Manufacturing

- Retail

- Energy

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Third-Party Risk Management Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 8.09 Billion |

| Market Size in 2026 | USD 9.34 Billion |

| Revenue Forecast by 2034 | USD 29.82 Billion |

| CAGR | 15.59%from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Third-Party Risk Management Market FAQ's

The global market size was valued at USD 8.09 Billion in 2025 and is projected to grow to USD 29.82 Billion by 2034.

North America dominates the market due to strong regulatory enforcement and high adoption of cybersecurity and risk management solutions.

Major applications include vendor risk assessment, compliance management, cybersecurity risk monitoring, supply chain risk management, and audit reporting.

A few of the key players in the market are RSA Security, BitSight Technologies, SecurityScorecard, OneTrust, NAVEX, SAI360, ProcessUnity, Prevalent, Archer Technologies, MetricStream, LogicGate, UpGuard, and others.

Key drivers include rising cyber threats, strict regulatory requirements, and increasing vendor dependencies.

Major demand comes from BFSI, healthcare, IT and telecom, manufacturing, retail, and energy sectors.

The market outlook remains strong due to increasing adoption of AI-driven analytics, automation in risk monitoring, and integration of predictive risk assessment tools.

Download Sample Report of Third-Party Risk Management Market

Please fill out the form to request a customized copy of the research report.