U.S. Lithium Market Growth Opportunities, Industry Revenue, 2026-2034

REPORT DETAILS

REPORT DETAILS

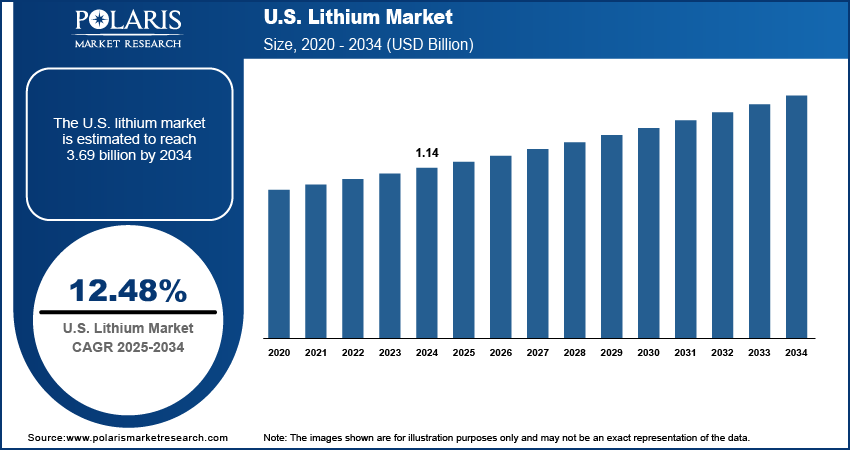

U.S. Lithium Market Summary

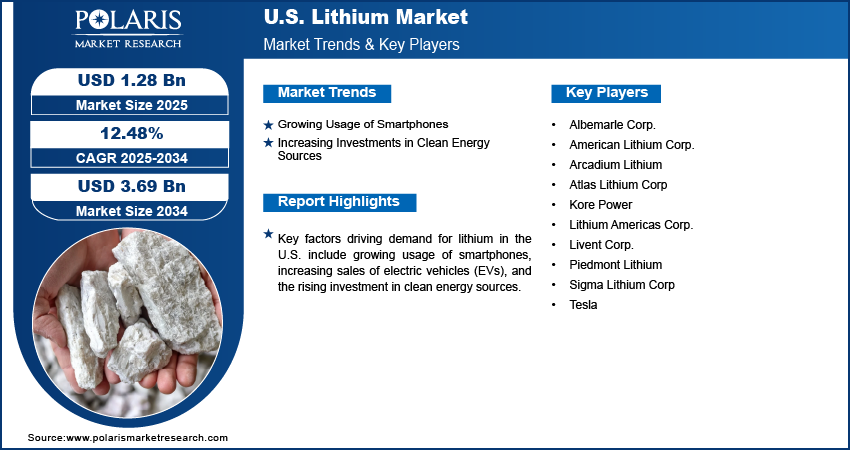

The U.S. lithium market size was valued at USD 1.28 billion in 2025, growing at a CAGR of 12.48% from 2026 to 2034. Key factors driving demand for the lithium in the U.S. include growing usage of smartphones, increasing sales of electric vehicles (EVs), and the rising investments in clean energy sources

Market Statistics

Key Takeaways

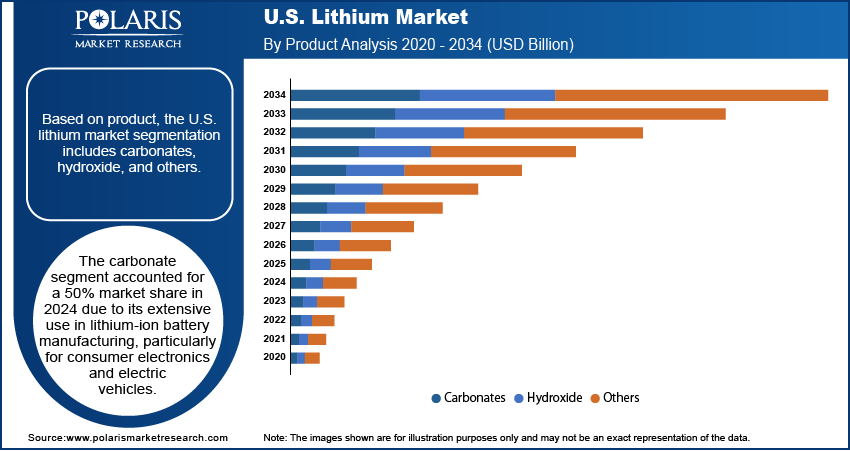

- The carbonate segment accounted for a 50.12% U.S. lithium market share in 2025 due to its use in lithium-ion battery manufacturing.

- The consumer electronics segment is expected to grow at the fastest CAGR of 15.9% from 2026 to 2034, owing to the growing usage of laptops, wearables, and other connected devices.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The growing usage of smartphones is driving the demand for lithium as every smartphone relies on a lithium-ion battery.

- The increasing investment in clean energy sources is fueling the U.S. lithium market, as clean energy sources such as solar and wind power need large-scale battery storage to store energy during periods of low sunlight or wind.

- The strict carbon emission norms are expected to create a lucrative market opportunity during the forecast period.

- The high capital cost required for lithium production hinders the market growth.

Artificial Intelligence (AI) in U.S. Lithium Market

- Artificial intelligence enhances the U.S. lithium market by optimizing exploration and mining operations through predictive analytics that identify high-yield reserves.

- It improves battery manufacturing efficiency by monitoring production lines in real time and reducing defects.

- AI also supports recycling by enabling advanced sorting and recovery of lithium from used batteries.

- AI strengthens demand forecasting and supply chain management, helping companies reduce costs and mitigate shortages.

What is Lithium?

Lithium is a lightweight, highly reactive alkali metal known for its silvery-white appearance and exceptional electrochemical properties. It occurs naturally in minerals such as spodumene and lepidolite and in brines. Lithium is classified into two main types: lithium carbonate and lithium hydroxide, both of which serve distinct industrial purposes. Lithium carbonate is widely used in pharmaceuticals, ceramics, and glass production, while lithium hydroxide plays a critical role in manufacturing high-performance lithium-ion batteries. The metal’s lightweight nature and high energy density make it crucial in electric vehicles, consumer electronics, and renewable energy storage systems.

In the U.S., lithium plays a strategic role in advancing clean energy initiatives and reducing dependence on fossil fuels. The demand for lithium-ion batteries has surged in the U.S. with growing adoption of electric vehicles and renewable energy storage. The country focuses on expanding domestic lithium production to reduce reliance on imports, particularly from South America and Australia. The U.S. lithium resources, concentrated in Nevada and North Carolina, are being actively developed, supported by federal investments and private sector partnerships.

Source: Polaris Market Research Analysis

The U.S. lithium market demand is driven by the increasing sales of electric vehicles (EVs). According to the International Energy Agency, the electric car sales increased to 1.6 million in 2024 in the U.S. This drove the adoption of lithium as each electric vehicle requires a large battery pack that contains significant amounts of lithium to ensure high energy density, long driving range, and faster charging. Government in the country is also supporting EV adoption through subsidies and emission regulations, further accelerating lithium demand. Hence, as consumers shift from gasoline-powered cars to EVs, manufacturers increase battery production, which propels the need for raw lithium.

Drivers & Opportunities

Growing Usage of Smartphones: The rising use of smartphones is driving the demand for lithium as every smartphone relies on a lithium-ion battery. These batteries power the device, offering high energy density, longer life, and lighter weight compared to older battery technologies. Smartphones with larger screens or faster processors are also creating the need for powerful and efficient lithium-ion batteries. Additionally, the rapid turnover of smartphones, with consumers upgrading every few years, is boosting lithium consumption. According to consumeraffairs, over 98% of Americans owned a cellphone in 2024, compared with 81% in 2015. Therefore, as more people in the country buy smartphones, the number of lithium-powered batteries produced each year surges.

Increasing Investments in Clean Energy Sources: Clean energy sources such as solar and wind power need large-scale battery storage to store energy during periods of low sunlight or wind, and lithium-ion batteries remain the most efficient solution for this purpose. The push for cleaner transportation and energy grids is also leading to the development of lithium batteries, for which the extraction of lithium is increasing to meet the soaring requirements, contributing to the market growth. Therefore, as governments and companies in the country invest in expanding renewable energy capacity, they also invest in massive battery storage projects, all of which require substantial amounts of lithium.

Source: Polaris Market Research Analysis

Segmental Insights

Product Analysis

Based on product, the segmentation includes carbonates, hydroxide, and others. The carbonate segment accounted for a 50.12% U.S. lithium market share in 2025. The dominance is attributed to its extensive use in lithium-ion battery manufacturing, particularly for consumer electronics and electric vehicles. The surge in EV adoption, supported by government incentives and automaker commitments to electrification, created strong demand for lithium carbonate. Additionally, the pharmaceutical and glass industries added to the demand, as carbonate compounds serve as essential raw materials in drug formulations and specialty glass production.

The hydroxide segment is expected to grow at a rapid pace from 2026 to 2034, owing to its superior compatibility with high-nickel cathode chemistries such as NCM 811, which deliver higher energy density and longer battery life. Automakers in the U.S. increasingly favor these chemistries to extend driving ranges and reduce charging frequencies, directly driving hydroxide consumption. Moreover, large-scale investments in domestic battery gigafactories and strategic partnerships between miners and battery manufacturers are ensuring greater supply security, further boosting hydroxide demand. The shift toward renewable energy storage systems that require high-performance batteries is also accelerating the segment’s expansion.

Comparison Matrix: Lithium Carbonate vs Lithium Hydroxide

| Parameter | Lithium Carbonate (Li₂CO₃) | Lithium Hydroxide (LiOH) |

| Battery Performance | Suitable for standard lithium-ion and LFP batteries with stable cycle life and safety performance | Preferred for high-performance EV batteries due to improved thermal stability and enhanced electrochemical performance |

| Cost | Generally lower production and refining cost, making it more economical for mass-market battery applications | Higher processing cost due to additional refining steps and higher purity requirements |

| Key Applications | Widely used in LFP batteries, consumer electronics, ceramics, glass, lubricants, and pharmaceuticals | Primarily used in high-nickel NMC and NCA batteries for electric vehicles and advanced energy storage systems |

| Compatibility with High-Nickel Cathodes | Less suitable for high-nickel cathode chemistries because of higher calcination temperatures and lower reactivity | Highly compatible with high-nickel cathodes (NMC 811, NCA) due to better synthesis efficiency and lower processing temperatures |

| Energy Density | Supports moderate energy density batteries commonly used in stationary storage and entry-level EVs | Enables higher energy density, longer driving range, and fast-charging capabilities in premium EV batteries |

| Industrial Usage | Extensively utilized across battery manufacturing, ceramics, specialty chemicals, and medical industries | Commonly used in EV battery production, aerospace applications, lubricating greases, and CO₂ absorption systems |

| Market Demand Trend | Strong demand driven by LFP battery expansion and consumer electronics manufacturing | Rapidly growing demand due to increasing adoption of high-nickel EV batteries in the U.S. automotive sector |

| Handling & Storage | Easier and safer to handle with lower caustic properties | More caustic and hygroscopic, requiring stricter handling and storage conditions |

Source: Polaris Market Research Analysis

Application Analysis

In terms of application, the segmentation includes automotive, consumer electronics, grid storage, glass & ceramics, and others. The automotive segment held the largest U.S. lithium market share in 2025 due to rising EV production to meet stringent emission regulations and to align with national clean energy goals. Federal and state-level incentives for EV purchases, along with major investments in domestic battery manufacturing facilities, further strengthened the dominance of the segment. The rapid expansion of charging infrastructure also encouraged consumers to shift toward electric mobility, creating sustained demand for battery materials such as lithium.

The consumer electronics segment is expected to register the highest CAGR of 15.9% from 2026 to 2034, owing to the growing usage of smartphones, laptops, wearables, and other connected devices. Rising dependence on portable gadgets, combined with the rollout of 5G technology and increasing adoption of smart home products, is estimated to accelerate the consumption of compact, high-energy-density lithium batteries. Remote work and digital learning trends are also fueling long-term demand for devices powered by rechargeable lithium batteries. Additionally, innovations in consumer electronics, such as foldable phones, advanced gaming consoles, and AI-integrated gadgets, are projected to push manufacturers to secure a reliable lithium supply.

Technological Advancements in Lithium Market

The market is witnessing an increasing adoption of advanced extraction, recycling, and battery technologies. The technologies enhance efficiency, sustainability, and supply chain security. These innovations support the rapid growth of electric vehicles, renewable energy storage, and next-generation battery applications.

| Technology | Short Description | Benefits |

| Direct Lithium Extraction (DLE) | Advanced extraction methods recover lithium directly from brines using membranes, adsorption, and ion-exchange systems. | Faster extraction, higher recovery rates, lower water usage, and reduced environmental impact. |

| Advanced Battery Chemistries | Development of high-nickel cathodes, solid-state batteries, and improved lithium-ion technologies enhances battery efficiency and performance. | Higher energy density, longer battery life, faster charging, and improved EV range. |

| Lithium Recycling Innovations | Modern hydrometallurgical and closed-loop recycling technologies recover lithium and other valuable metals from used batteries. | Reduces raw material dependency, lowers emissions, and supports sustainable battery supply chains. |

| Lithium-Sulfur Battery Development | Next-generation lithium-sulfur batteries use sulfur-based cathodes to increase energy storage capacity. | Lightweight batteries, lower material costs, and significantly higher energy density. |

| AI & Smart Manufacturing | AI-powered monitoring and automation improve lithium refining and battery production processes. | Better production efficiency, lower waste generation, and improved quality control. |

| Sustainable Refining Technologies | Eco-friendly refining methods reduce chemical usage and carbon emissions during lithium processing. | Cleaner production processes and improved sustainability across the lithium value chain. |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis

The U.S. lithium market is rapidly evolving as domestic production becomes a strategic priority amid rising EV demand and supply chain security concerns. Industry leaders such as Albemarle Corp. and Livent Corp. dominate with integrated refining capabilities. Emerging players such as Lithium Americas Corp. and Piedmont Lithium are advancing new projects to reduce reliance on imports. Sigma Lithium and Atlas Lithium Corp. explore additional U.S. opportunities, while battery makers such as Kore Power and automakers such as Tesla invest in localized supply chains. The Inflation Reduction Act’s critical minerals incentives further intensify competition, though permitting delays and ESG challenges persist. China’s influence in processing looms large, pushing U.S. firms to innovate in lithium extraction and recycling to secure a sustainable foothold.

A few major companies operating in the U.S. lithium market include Albemarle Corp., American Lithium Corp., Arcadium Lithium, Atlas Lithium Corp, Kore Power, Lithium Americas Corp., Livent Corp., Piedmont Lithium, Sigma Lithium Corp, and Tesla.

Key Companies

- Albemarle Corp.

- American Lithium Corp.

- Arcadium Lithium

- Atlas Lithium Corp

- Kore Power

- Lithium Americas Corp.

- Livent Corp.

- Piedmont Lithium

- Sigma Lithium Corp

- Tesla

U.S. Lithium Industry Developments

April 2026: Atlas Lithium Corporation signed contracts with four Brazilian engineering and construction firms. With this initiative, the company aims to implement its fully-owned Neves Project. The project is its flagship lithium mining development in Minas Gerais, Brazil. (Source: yahoo.com)

U.S. Lithium Market Segmentation

By Product Outlook (Revenue, USD Billion, Volume, Kilotons, 2021–2034)

- Carbonates

- Hydroxide

- Others

By Application Outlook (Revenue, USD Billion, Volume, Kilotons, 2021–2034)

- Automotive

- Consumer Electronics

- Grid Storage

- Glass & Ceramics

- Others

U.S. Lithium Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 1.28 Billion |

| Market Size in 2026 | USD 1.49 Billion |

| Revenue Forecast by 2034 | USD 3.69 Billion |

| CAGR | 12.48% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion, Volume in Kilotons, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The market size was valued at USD 1.28 billion in 2025 and is projected to grow to USD 3.69 billion by 2034.

The market is projected to register a CAGR of 12.48% during the forecast period.

A few of the key players in the market are Albemarle Corp., American Lithium Corp., Arcadium Lithium, Atlas Lithium Corp, Kore Power, Lithium Americas Corp., Livent Corp., Piedmont Lithium, Sigma Lithium Corp, and Tesla.

The carbonate segment dominated the market with 50.12% share in 2025.

The consumer electronics segment is expected to witness the fastest growth of CAGR 15.9% during the forecast period.

Download Sample Report of U.S. Lithium Market

Please fill out the form to request a customized copy of the research report.