Waste Management Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

REPORT DETAILS

Waste Management Market Summary

The global waste management market size was valued at USD 1.52 trillion in 2025. According to our waste management market forecast, the market is projected to grow at a CAGR of 5.5% from 2026 to 2034. The waste management market covers activities such as the collection, transport, treatment, recycling, and disposal of waste from municipal, industrial, commercial, and healthcare sources. Waste management is an essential part of urban infrastructure and environmental protection systems.

Market Statistics

Key Takeaways

- The MSW/household segment accounted for the largest market share in 2025. This is primarily due to increasing household consumption worldwide.

- The recycling waste management market segment is growing at the fastest CAGR. Circular-economy goals and sustainability initiatives drive the segment’s growth.

- The North America waste management market held the largest market share in 2025. Stringent regulations and mature recycling frameworks drive the regional market dominance.

- The U.S. competitive landscape comprises highly advanced separation technologies and landfill reduction technologies.

- The Asia Pacific waste management market is expected to grow at the fastest CAGR. This is due to investments in green technology and population concentration in major economies across the region.

- China is growing steadily. The country is experiencing increased industrial waste generation and government-supported waste-to-energy projects.

The demand for waste management solutions is being driven by growing urbanization and the introduction of strict sustainability policies. Measures such as higher landfill diversion targets, extended producer responsibility (EPR) programs, and circular economy requirements are encouraging greater investment in recycling, waste-to-energy, and smart waste management systems.

Industry Dynamics

- Urbanization and industrialization have also led to an increase in urban, industrial, and commercial waste. This has resulted in an increased need for more advanced waste treatment and disposal technologies and methods.

- The waste management sector is undergoing a significant shift through sustainability mandates that promote enhanced recycling and material recovery. Landfill diversion targets and extended producer responsibility policies have been set through government policies to encourage comprehensive waste management strategies.

- Digital platforms and IoT waste management solutions are increasing efficiency. Additionally, they improve waste management compliance reporting for entities. The AI-based sorting technology simplifies material recovery.

- High costs and weak infrastructure for segregation in developing regions limit the adoption of modern systems.

The growth of the waste management industry is aided by services like connected collection networks, advanced recycling facilities, management of landfills, waste-to-energy plants, and monitoring services. These measures improve efficiency and effectiveness. They counter the rise in waste in developed and developing countries. Their role in sustainable city planning and conservation of nature also supports long-term social goals in relation to public health and infrastructure.

Highly efficient waste-to-energy and recycling plants can utilize waste materials for their intended uses and for clean energy generation. Landfilling projects intend to create conditions for safe waste disposal and management. Digital and IoT-based platforms have become effective for cities and companies for waste stream monitoring and analysis. Robotics and automation in waste sorting plants improve efficiency and reduce reliance on manual labor and operational costs. For instance, ANDRITZ teamed up with the ReWaste F project in Austria to open a smart waste management plant in June 2024. The constructed smart waste management plant uses IoT technology and computerized shredding to improve recylcing rates.

The waste management sector is emerging due to governments implementing stringent environmental policies. The focus and investment in the circular economy approach are increasing, thus driving the adoption of recycling solutions.

Drivers and Opportunities

Global Urbanization Trends Driving Higher Waste Generation

Urbanization globally has volumes of municipal, commercial, and industrial waste. The United Nations estimates that the global urban population is expected to increase by 2.5 billion by 2050. Population growth increases solid waste, while rapid industrialization generates toxic waste, overloading current infrastructure. Increased consumer expenditure and urban development generate enormous volumes of packaging, plastics, and demolition waste. These patterns are compelling municipalities and private operators to adopt new waste technologies and integrated service concepts.

Waste Reduction Sustainability Mandates by Governments and International Agreements

Government sustainability mandates and international agreements set the backdrop for waste management activities in developed and developing markets. Higher landfill diversion targets are enforced by regulatory authorities and, in parallel, are pushing recycling, waste-to-energy, and other resource recovery initiatives. According to these regulatory changes, the investments are also diverted toward building treatment plants and smaller decentralized systems. Furthermore, international climate agreements highlight waste management as key to achieving emission reductions. Therefore, governments are increasingly working with the private sector to increase treatment capacity. These are steps taken to advance circular economy principles for long-term market development.

Impact of E-Waste Recycling on the Waste Management Market

The e-waste management market is a significant part of the waste management sector. This is due to the increasing disposal of electronic items such as mobile phones, computers, and batteries. Electronic waste recycling is essential because it enables the reuse of valuable materials like gold and rare earths. Battery recycling also mitigates the dangers posed by toxic materials such as lead and mercury.

The rising demand for electric cars is driving increased recycling of lithium-ion batteries. IoT-based collection infrastructure and decentralized recycling plants are being used to make recycling more efficient. Public-private partnerships are also helping to improve recycling capacity in major cities. The following table lists a few trends and opportunities in the industry.

| Trends and Opportunities | Description |

| Advancements in Recycling Technologies | Hydrometallurgy, chemical recycling, and pyrolysis for enhanced metal recovery |

| IoT and Smart Collection | Smart bins and tracking for effective collection |

| Battery Recycling | Higher demand for lithium-ion battery recycling with the increase in the use of electric vehicles |

| Public-Private Partnerships | Partnerships between governments and private recyclers to improve efficiency |

| Decentralized Recycling Units | Small-scale e-waste plants in urban areas to cut down transport charges |

Waste Management Cost Structure and Pricing Dynamics

The cost structure of the market for waste management is dominated by the operating cycle, from collection to final disposal. Fuel prices, staffing costs, waste collection transportation costs, and treatment facility operational expenditures are the major factors contributing to higher treatment costs. Moreover, environmental regulations and equipment development also increase treatment costs.

The prices charged depend on the nature and amount of the waste. The pricing for the residential sector is usually based on fixed fees. There may also be subscription charges. Commercial and industrial customers are billed based on the weight of the waste or specific services needed. Additionally, market variables such as fuel prices and recycling mandates influence costs. However, due to the growing focus on sustainability, prices are increasingly linked to waste-reduction targets.

Regulatory Landscape and ESG Compliance

The waste management industry is highly dependent on government legislation for setting sustainability standards. Countries and international legislation set standards on the collection, movement, treatment, and disposal methods to ensure public and environmental safety. The standards entail aspects like recycling, landfill sites application, hazardous waste management, and emissions.

Issues about compliance with ESG are gaining momentum. Organizations demand that practices be implemented that minimize negative environmental impact and keep workers safe. Focus has also increased on processes that enable business transparency. Waste management, circular economy, and sustainability reporting have become an intrinsic part of strategies for winning the confidence of clients and markets. Companies following the path of ESG practices remain competitive with their compliance.

Segmental Insights

Waste Type Analysis

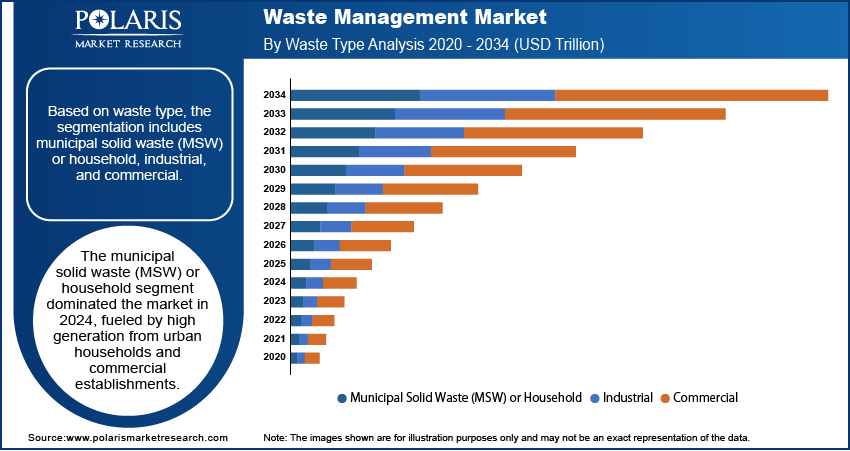

Based on waste type, the market segmentation includes municipal solid waste (MSW) or household, industrial, and commercial waste. The municipal solid waste (MSW) or household segment dominated in 2025, driven by rapid city expansion and rising household consumption. Large amounts of waste from food, plastics, paper, and glass produced by urban populations require structured collection and disposal systems. In response, governments are now discouraging the use of landfills and promoting recycling and waste-conversion projects.

The industrial segment is expected to grow at the fastest rate, driven by rising waste from manufacturing, construction, and agriculture. Increasing demolition activity is therefore adding to overall waste generation. Regulatory frameworks are also demanding that industries seek advanced treatment solutions.

Service Type Analysis

In terms of service type, the segmentation includes collection, transportation, and disposal. The collection segment led the market, locally supported by rapid urban population growth and rising waste volumes. Well-structured collection systems lead to better segregation and timely disposal.

The disposal segment is anticipated to grow fastest due to increasingly stringent policies on landfill diversion. Governments have directed the disposal of hazardous and even non-hazardous waste using safer technologies. Advanced disposal technology, especially for healthcare and industrial sector applications, is needed to prevent contamination.

Waste Treatment Analysis

Based on waste treatment, the market is segmented into composting, incineration, controlled landfill, uncontrolled landfill, sanitary landfill, open dump, and recycling. The sanitary landfill segment held the majority in 2025 because it remained the most mechanical way to dispose of municipal solid waste. UNEP estimated that landfill volumes worldwide could increase from 0.64 billion tonnes in 2020 to 1.09 billion tonnes by 2050. Better protective liners, gas capture systems, and leachate control are improving environmental safety.

The recycling segment is expected to witness the highest growth during the forecast period. Recycling is part of circular-economy models that provide industries with reusable raw materials. Further, a rise in consumer appreciation for greener products and packaging fuels the segment’s expansion.

Regional Analysis

In 2025, the North America waste management market account for the largest market share. This is due to stringent regulations and mature recycling frameworks. The U.S. Environmental Protection Agency (EPA) has strict regulations on landfills and hazardous waste. This leads to increased demand for treatment and disposal facilities. There is support for growth in waste-to-energy projects, along with digital tracking technologies.

The U.S. Waste Management Market Insight

The U.S. retained the largest share of the market due to the high volume of municipal waste and strong recycling efforts in North America. According to the Global Waste Index 2025, the U.S. generates approximately 951 kilograms of waste per capita annually (around 2.6 kilograms per day). Such federal and state regulations that encourage landfill safety, material recovery, and waste-to-energy facilities contribute significantly to its growth.

Europe Waste Management Market

The Europe waste management market is projected to hold a considerable share by 2034. This is primarily due to ambitious directives in the EU, which include recycling 55% of household waste by 2025, 60% by 2030, and 65% by 2035, with landfilling restricted to no more than 10%. The packaging recycling targets are set at 70%. Thus, member states are forced to accelerate the development of advanced recycling and treatment infrastructure.

Asia Pacific Waste Management Market

The Asia Pacific waste management market is expected to witness the highest CAGR during the forecast period, driven by rapid urbanization and population concentration in countries such as China and India. To address rising municipal and industrial waste volumes, governments and private players are making significant investments in recycling infrastructure and waste-to-energy facilities.

China Waste Management Market Overview

Chinese market growth is due to huge municipal waste generation and stricter landfill policies. The government is working on the promotion of waste segregation at the household level and also investing in waste-to-energy infrastructure. In March 2024, the State Council launched a plan to establish a nationwide recycling system, targeted for completion by 2025 and projected to have an annual market value of USD 697 billion.

Key Players and Competitive Landscape

The waste management market competitive landscape is moderately fragmented. Major players are diversifying their portfolios to include collection, recycling, and waste-to-energy. The focus is also on digital waste monitoring. There have been ongoing mergers and acquisitions to expand the geographic footprint and achieve economies of scale. This shift is especially prevalent in North America and Europe.

A few of the leading waste management companies include Waste Management, Inc., Veolia Environnement S.A., Republic Services, Remondis, Waste Connections, Inc., GFL Environmental, PreZero, FCC Group, Clean Harbors, China Everbright Environment Group (CHFFF), Paprec, and Stericycle, Inc.

List of Key Companies

- China Everbright Environment Group (CHFFF)

- Clean Harbors

- FCC Group

- GFL Environmental

- Paprec

- PreZero

- Remondis

- Republic Services

- Stericycle, Inc.

- Veolia Environnement S.A.

- Waste Connections, Inc.

- Waste Management, Inc.

Industry Developments

In July 2025, SUEZ and SIAAP inaugurated France’s largest biogas production facility at the Seine Aval wastewater treatment plant near Paris. The unit processes 130,000 tonnes of sludge annually, generating 350 GWh of renewable energy, which meets over half of the plant’s energy requirements. The €401 million project reinforces sustainable and energy-efficient wastewater management in the region.

In June 2025, Veolia planned to increase hazardous waste treatment by 530,000 tonnes by 2030, with 100,000 tonnes already operational, backed by acquisitions in the United States, Japan, and Brazil.

In April 2025, SUEZ and CNRS entered into a five-year cooperation to drive decarbonization, resource recovery, and circular water and waste solutions, such as sludge-to-gas, PFAS reduction, and AI-based recycling.

In November 2024, Waste Management finalized its $7.2 billion acquisition of Stericycle on November 4. As a result, Stericycle will continue its operation under the WM Healthcare Solutions business, which is anticipated to generate more than $125 million in cost synergies. It is expected to improve WM's medical waste management and information destruction capabilities.

Waste Management Market Segmentation

By Waste Type Outlook (Revenue, USD Trillion, 2021–2034)

- Municipal Solid Waste (MSW) or Household

- Food

- Paper and Cardboard

- Plastic

- Glass

- Metal

- Others

- Industrial

- Manufacturing Waste

- Construction & Demolition Waste

- Agriculture Waste

- Other Industrial waste

- Commercial

By Service Type Outlook (Revenue, USD Trillion, 2021–2034)

- Collection

- Transportation

- Disposal

By Waste Treatment Outlook (Revenue, USD Trillion, 2021–2034)

- Composting

- Incineration

- Controlled Landfill

- Uncontrolled Landfill

- Sanitary Landfill

- Open Dump

- Recycling

By Regional Outlook (Revenue – USD Trillion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Waste Management Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 1.52 trillion |

| Market Size in 2026 | USD 1.60 trillion |

| Revenue Forecast by 2034 | USD 2.45 trillion |

| CAGR | 5.5% |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD trillion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Waste Management Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The market is projected to reach USD 2.45 trillion by 2034. It is expected to account for a CAGR of 5.5% between 2026 and 2034.

The municipal solid waste (MSW) or household segment accounted for the major share in 2025, driven by the increasing urbanization and residential waste in the urban areas.

The recycling segment is expected to have the highest growth rate as it is driven by circular economy strategies and sustainable development policies.

Improved sorting technologies, waste-to-energy facilities, automated collection systems, composting plants, and anaerobic digesters are making waste management more efficient and sustainable.

North America led the market in 2025 due to its highly advanced waste collection systems. Environmental regulations are also stringent. The Asia Pacific region is experiencing the highest growth rate.

The recycling segment is projected to grow at the fastest CAGR, due to circular economy initiatives and government sustainability mandates.

Download Sample Report of Waste Management Market

Please fill out the form to request a customized copy of the research report.