Automotive Aramid Fiber Market Future Prospects, Trends, Growth, Key Player 2026-2034

REPORT DETAILS

Market Statistics

Overview

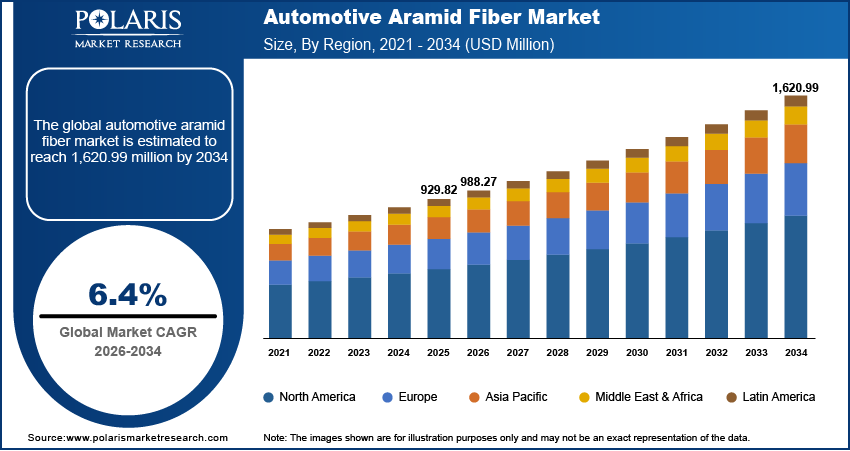

The global automotive aramid fiber market is estimated around USD 929.82 million in 2025, with consistent growth anticipated during 2026–2034. The market is projected to grow at a 6.4% CAGR during the forecast period. This is propelled by rising EV adoption and thermal management needs along with rising demand for high-performance materials.

Future Demand Scenarios

- Base scenario: Faster adoption rates in the electric and autonomous vehicles accelerate demand, driven by the increasing utilization of aramid fibers in electric battery thermal management, lightweight safety parts, and advanced composite structures.

- Upside scenario: Faster adoption in electric and autonomous vehicles accelerates demand, driven by wider use of aramid fibers in battery thermal protection, lightweight safety components, and advanced composite structures.

- Conservative scenario: Slower automotive output, cost pressure from alternative fibers, and delayed EV platform rollouts temper demand growth, limiting expansion to core, safety-critical applications only.

Key Insights

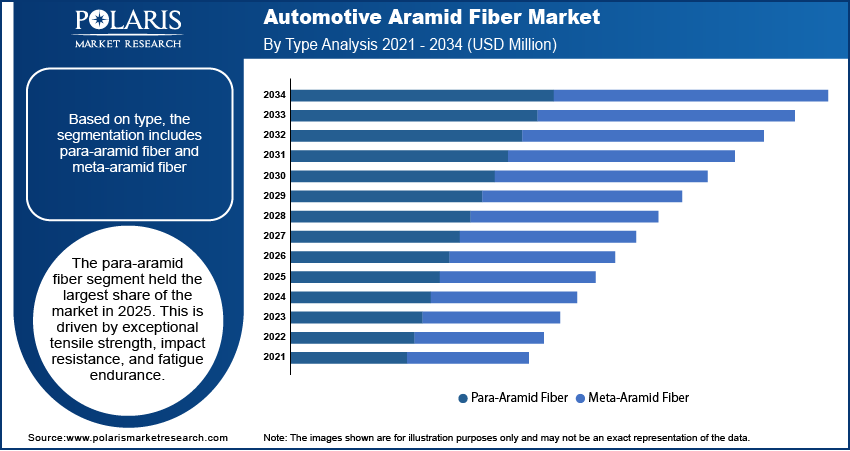

- The para-aramid fiber segment held the largest share of the market in 2025 attributed to their high tensile strength, impact properties, and fatigue endurance.

- Brake pads and clutch facings are an important application category, as there is a lot of interest in high-temperature properties, fade resistance, and the resultant friction behavior.

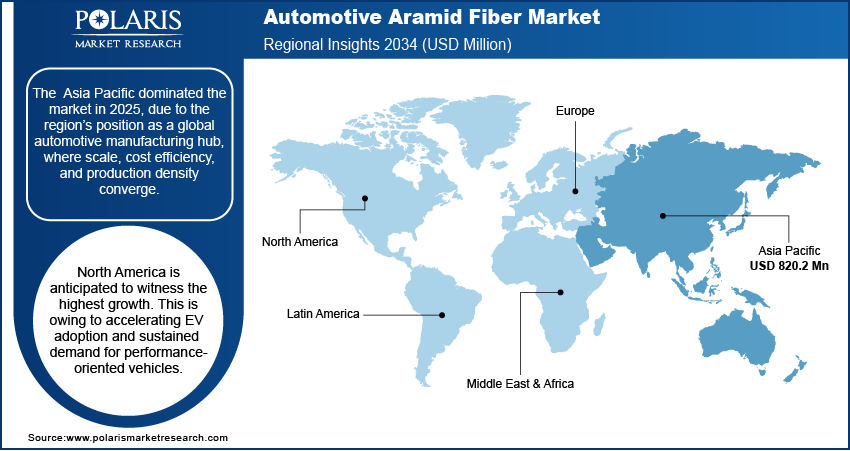

- The Asia Pacific dominated the market in 2025 driven by the region’s position as a global automotive manufacturing hub, where scale, cost efficiency, and production density converge.

- North America is anticipated to witness the highest growth. This is due to the accelerating EV adoption and sustained demand for performance-oriented vehicles.

Industry Dynamics

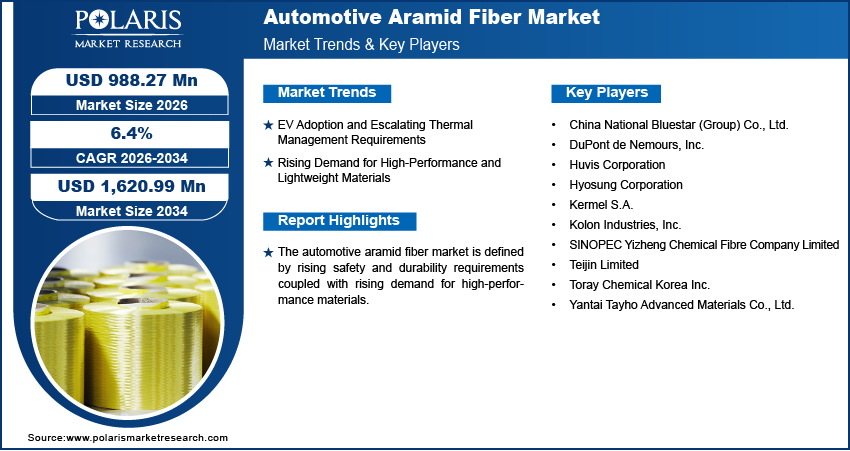

- EV adoption and thermal management needs

- Rising demand for high-performance materials

- High production and processing costs restraining the market

- Recyclable and sustainable aramid fiber development creating opportunities

Market Statistics

- 2025 Market Size: USD 929.82 million

- 2034 Projected Market Size: USD 1,620.99 million

- CAGR (2026-2034): 6.4%

- Asia Pacific: Largest market in 2025

What is Automotive Aramid Fiber and Why It Matters

Aramid fibers help in the growth of modern vehicle designs with high strength, thermal stability, and lightness in safety-critical components. The use of aramid fibers in the automobile sector meets all thermal and strength conditions simultaneously in components such as tires, brake systems, hoses, belts, and composite reinforcement. The use of aramid fibers in the vehicle meets the need for lightness and reduced emissions without affecting the strength of the vehicle. The market for automotive aramid fibers globally is growing steadily with increased growth in the market size of automotive aramid fibers.

Source: Polaris Market Research Analysis

Drivers & Opportunities

EV Adoption and Escalating Thermal Management Requirements

The increasing adoption of EVs propels the demand for aramid fibers in the automotive industry as electric engines bring higher thermal resistance and tougher safety criteria. Worldwide electric vehicle sales have topped 17 million in the year 2024, based on the International Energy Agency report, showing more than 25% growth. Battery packs, power electronics, and high-voltage cabling require materials that tolerate heat, resist flame propagation, and maintain dimensional stability under stress. Aramid fibers meet these requirements while supporting weight reduction targets. This cause-and-effect dynamic pushes OEMs to specify aramid-based components in insulation, shielding, and reinforcement layers. The market implication follows closely thereafter. The use of lightweight materials for EVs achieves priority status, and aramid penetration is increasing despite the constraints imposed on the aramid market for automotive aramid fibers due to cost sensitivity and qualification times.

Rising Demand for High-Performance and Lightweight Materials

Increasingly stricter emission rules and fuel efficiency requirements increase the need for lightweight materials in the automotive industry, that withstand extreme environments. The effect is substitution away from metals and conventional fibers toward aramid solutions with higher tensile strength and thermal resistance. Aramid fibers facilitate durability in brake systems, hoses, gaskets, and structural reinforcement without adding mass to the vehicle. The result is a higher specification footprint across performance-critical components. Automotive aramid fiber markets emerge out of the balance of OEMs for safety, efficiency, and life cycle performance, even as procurement teams weigh cost pressures and supply constraints intrinsic in the restraints landscape of automotive aramid fiber markets.

Restraints & Challenges

High Production and Processing Costs

Higher inputs from advanced polymer synthesis routes and energy-intensive processing raise the cost base across the automotive aramid fiber market restraints landscape. These higher input costs translate into elevated component prices for insulation layers, reinforcement fabrics, and protective elements used in vehicles. OEMs respond by limiting aramid adoption to safety-critical or thermally exposed zones rather than broad structural use. The result is selective penetration. Although aramid fibers continue to remain irreplaceable in certain applications within the automotive sector, cost sensitivity dampens volume growth across mass-market programs.

Competition from Alternative Reinforcement Materials

Competition from alternatives such as carbon fiber, glass fiber, and steel cord exerts substitution pressure in the automotive aramid fiber market restraints. Many of their applications involve acceptable strength-to-weight ratios at lower or more predictable costs. Carbon fiber is used by automakers in premium segments, while glass fiber or steel cord is used in cost-driven designs. This gives aramids a narrow application area in which heat resistance, cut resistance, or fatigue performance cannot be compromised. Strong technical performance, therefore, results in constrained share growth.

Emerging Opportunities

Expanding Use in Lightweight Composite Architectures

Vehicle electrification and emission targets improve the demand for automotive lightweight materials that manifest strength with thermal stability. This creates automotive aramid fiber market opportunities within composite structures used for battery protection, underbody shielding, and reinforced panels. Aramid fibers improve resistance to impact and durability with very little addition of mass, nicely satisfying the requirements for lightweight materials from EVs. The growth of composites across electric and hybrid platforms also boost aramid integration from niche reinforcement to system-level design input as part of an overall market uptake.

Development of Recyclable and Sustainable Aramid Fiber Solutions

Sustainability targets and material circularity initiatives reshape procurement priorities across the automotive sector. This drives automotive aramid fiber market opportunities centered on recyclable grades with lower-impact production pathways. Development of better fiber recovery, resin compatibility, and lifecycle optimization improves the sustainability profile of aramid-based components. Automakers are investigating such solutions that help meet regulatory and ESG targets without sacrificing performance. The result to reinforce the positioning of aramid in next-generation vehicle platforms, particularly where EV lightweight material requirements call for durability with associated environmental accountability.

Source: Polaris Market Research Analysis

Segmental Insights

The report offers in-depth analysis of the market for aramid fibers in automobiles by type, fiber form enabling users to understand the growth and profit potential of each demand segment.

By Type

-

Para-Aramid Fiber in Automotive

Para-aramid fiber automotive applications account for the larger share within automotive aramid fiber by type, due to the high tensile strength, impact resistance, and resistance to fatigue that these fibers possess. These characteristics make para-aramid fibers useful for applications involving components of automobiles that experience high stresses and where resistance to failure is low. The applications of these fibers occur largely in tires and braking components.

-

Meta-Aramid Fiber in Automotive

Meta-aramid fiber automotive demand is shaped by thermal stability and inherent flame resistance rather than mechanical strength. Meta-aramid fibers possess resistance to high temperatures, which makes them useful in the production of insulation, heat shields, and components for the engine compartment. Car manufacturers use meta-aramid materials in areas where there is a constant heat flow, that could cause degradation of polymers or metals.

Para vs. Meta Decision Matrix

| Decision Parameter | Para-Aramid Fiber | Meta-Aramid Fiber |

| Primary Performance Focus | Mechanical strength and impact resistance | Thermal stability and flame resistance |

| Tensile Strength | Very high; supports load-bearing and reinforcement roles | Moderate; not intended for structural load transfer |

| Heat & Flame Resistance | Limited at sustained high temperatures | Excellent; maintains integrity under continuous heat exposure |

| Typical Automotive Applications | Tires, brake pads, clutch facings, structural composites | Heat shields, insulation layers, under-hood components |

| Role in EV Platforms | Lightweight reinforcement for durability and efficiency | Thermal insulation around batteries and power electronics |

| Cost Positioning | Higher, justified by mechanical performance | Medium–high, driven by thermal compliance needs |

| Material Selection Trigger | Impact resistance and fatigue endurance required | Fire safety and heat protection required |

Source: Polaris Market Research Analysis

By Fiber Form

-

Aramid Pulp

Aramid fibers used for the pulp in automotive parts are used in friction materials, especially in the form of brake pads and clutch facings. The fibrillated form of the fibers increases the bonding in resin formulations and improves their heat-resistance properties.

-

Staple Fiber

The staple fibers are used in making non-woven insulation mats and thermal barriers. The staple shape allows for uniform distribution and thermal performance in under hood and vehicle cabin insulation applications.

-

Yarn & Fabric

The usage of Aramid fiber yarn in the automotive industry includes tire cords, protective fabrics, and reinforced hoses. The woven and knitted patterns give directionality and dimensional stability to the material.

-

Chopped Fiber

Chopped fibers are blended into composite matrices to improve impact resistance and crack propagation control. Their use is growing in injection-molded automotive components where localized reinforcement is required without complex layup processes.

By Application

-

Brake Pads & Clutch Facings

Aramid fiber in brake pads is driven by thermal stability, fade resistance, and consistent friction performance. The use of aramid fibers replaces asbestos in braking systems and offers improved friction cycles. The fibers’ ability to withstand high temperatures ensures smooth processing with passenger and sports cars.

-

Tires & Tire Reinforcement

Aramid fiber in tires improves durability, cut resistance, and rolling performance. High tensile strength properties make the layers thinner promoting fuel efficiency. The tensile strengths of aramid fibers are better than other materials. Aramids are more effective at high speeds and it provides greater stability to the tire.

-

Hoses, Belts & Gaskets

Aramid fibers find used in hoses, belts, and gaskets owing to their abrasion and chemical resistance. However, their interaction with oil, coolant, and vibration requires a reinforcement technology that withstand such environments. Aramid-reinforced technology increases the reliability of critical systems by prolonging the time and reducing the rates of failure.

-

Heat Shields & Insulation

Automotive thermal insulation materials increasingly incorporate aramid fibers for under-hood protection and electric vehicle thermal management. These materials limit heat transfer to sensitive components while maintaining low mass. Meta-aramid fibers are especially favored where prolonged heat exposure and fire resistance are required.

-

Automotive Composites & Structural Components

Aramid fiber composites automotive applications focus on impact resistance and energy absorption rather than maximum stiffness. While carbon fiber offers high stiffness, aramid fibers provide better toughness and resistance properties and are used accordingly for protected panels. The application is selective in nature due to cost factors.

Application Mapping by Fiber Form

| Aramid Fiber Form | Key Automotive Components | Functional Role in Component | Primary Performance Benefit |

| Aramid Pulp | Brake pads, clutch facings | Reinforcement within friction material matrix | Thermal stability, wear resistance, friction consistency |

| Staple Fiber | Under-hood insulation mats, thermal liners, acoustic panels | Nonwoven reinforcement and heat barrier | Heat resistance, vibration damping, noise reduction |

| Yarn & Fabric | Tire cords, reinforced hoses, belts, protective wraps | Load-bearing and dimensional reinforcement | High tensile strength, fatigue resistance, durability |

| Chopped Fiber | Injection-molded plastic parts, composite housings, protective panels | Dispersed reinforcement within polymer matrices | Impact resistance, crack control, weight efficiency |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Regional Analysis

Asia Pacific Automotive Aramid Fiber Market Assessment

Asia Pacific dominated the automotive aramid fiber market in 2025. This growth is attributed to the fact that a significant portion of the world’s automobile manufacturing takes place in the Asia Pacific. Regions such as China, South Korea, India, and other countries in this geography are major centers where a large volume of automobile manufacturing takes place. This thereby leads to a significant adoption of these materials. International Energy Agency reported that China continued to lead global electric car manufacturing in 2024, accounting for more than 70% of total production. The growing usage of safety-critical components, thermal-resistant components, and reinforcement drivers propels the demand for aramid fiber pull-through.

North America Automotive Aramid Fiber Market Insights

North America is projected to grow at a rapid pace during the forecast period, owing to the increasing adoption of EVs and the strong demand for performance-focused variants. According to the International Council on Clean Transportation, more than 1.2 million new light-duty electric vehicles were sold in the US through the first three quarters of 2025, marking a record pace of adoption, with EVs accounting for nearly 12% of total vehicle sales in the third quarter. Electrification changes the temperature and mechanical load curves, which increases the need for materials with endurance to temperature, vibration, and mechanical loads in a compact configuration. Aramid fibers address these pressures across battery protection, reinforcement components, and safety systems. High-value vehicle platforms and innovation-driven procurement further reinforce the automotive aramid fiber market North America, positioning the region as a technology-led contributor to the global automotive materials market.

Europe Automotive Aramid Fiber Market Overview

Europe’s automotive aramid fiber market advances through regulatory force rather than sheer volume expansion. Growth is driven by stringent light weighting mandates, emissions thresholds, and vehicle efficiency targets enforced across Germany, France, and the UK. In December 2025, the European Commission introduced Automotive Package to accompany the transition toward clean mobility, providing a policy framework flexible but ambitious enough to reach climate neutrality by 2050 while reinforcing the sector's strategic independence. These necessitate compression in material options and heighten the demand for high-strength, low-mass reinforcement across structural, braking, and safety systems. This regulatory architecture keeps the automotive aramid fiber market going in Europe, pushing aramid use deeper into advanced vehicle design cycles within the global automotive materials market.

Rest of the World Automotive Aramid Fiber Market Insights

Latin America and the Middle East present a measured but improving growth outlook, driven by the modest expansion of automotive assembly, an increase in localized component production, and improving vehicle safety standards. Infrastructure development and selective investment in regional manufacturing increase material adoption where durability and lifecycle performance carry procurement weight. These trends incrementally lift aramid fiber usage across commercial and passenger vehicles, extending the geographic footprint of the global automotive materials market beyond established production centers.

Heat Map Analysis

| Region | Demand Intensity | Automotive Production Base | Regulatory & Lightweighting Pressure | EV & Performance Vehicle Adoption | Growth Momentum |

| Asia Pacific | Very High | Very High | Medium | Medium–High | High |

| Europe | High | High | Very High | Medium | Medium–High |

| North America | Medium–High | Medium–High | Medium | Very High | High |

| Rest of the World | Medium | Medium | Low–Medium | Low–Medium | Medium |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The automotive aramid fiber market is moderately competitive, with the competitive landscape automotive materials shaped by performance requirements related to light weighting, heat resistance, and durability. Major market participants of the global aramid fibers market for automobiles and other associated industries and applications, such as safety components, reinforcing materials, friction components, and thermal protection systems for modern automobiles, are major players of the aramid fibers market for vehicles. The competition for manufacturers of aramid fibers for automobiles derives from innovations and developments in aramid materials, the stability of aramid fibers, and the ability of aramid fibers to fully support the requirements of vehicle manufacturers.

Key players operating in the global automotive aramid fiber market include China National Bluestar (Group) Co., Ltd., DuPont de Nemours, Inc., Huvis Corporation, Hyosung Corporation, Kermel S.A., Kolon Industries, Inc., SINOPEC Yizheng Chemical Fibre Company Limited, Teijin Limited, Toray Chemical Korea Inc., and Yantai Tayho Advanced Materials Co., Ltd.

Key Players

- China National Bluestar (Group) Co., Ltd.

- DuPont de Nemours, Inc.

- Huvis Corporation

- Hyosung Corporation

- Kermel S.A.

- Kolon Industries, Inc.

- SINOPEC Yizheng Chemical Fibre Company Limited

- Teijin Limited

- Toray Chemical Korea Inc.

- Yantai Tayho Advanced Materials Co., Ltd.

Differentiation by Performance, Pricing, Geography

| Company | Performance Positioning | Pricing Positioning | Geographic Strength |

| DuPont de Nemours, Inc. | High-strength, high-heat aramid fibers for safety-critical uses | Premium | Strong in North America, Europe, and Asia Pacific |

| Teijin Limited | Lightweight, high-performance fibers for EV and friction systems | Premium to upper-mid | Japan, wider Asia Pacific, and Europe |

| Toray Chemical Korea Inc. | Consistent-performance specialty aramid fibers | Upper-mid | Korea with expanding Asia Pacific reach |

| Kolon Industries, Inc. | Reliable aramid fibers for reinforcement applications | Mid-range | South Korea and Asia |

| Hyosung Corporation | Performance-balanced aramid fibers | Mid-range | Asia Pacific focused |

| China National Bluestar (Group) Co., Ltd. | Mass-market grade aramid fibers | Cost-competitive | Strong in China with regional exports |

| SINOPEC Yizheng Chemical Fibre Company Limited | Standard automotive-grade aramid fibers | Cost-competitive | Primarily China |

| Yantai Tayho Advanced Materials Co., Ltd. | Improving-grade aramid fibers | Value to mid | China and Asia Pacific |

| Huvis Corporation | Niche automotive aramid fibers | Mid-range | Korea-centric |

| Kermel S.A. | High-temperature specialty aramid fibers | Premium (niche) | Europe-focused |

Source: Polaris Market Research Analysis

Automotive Aramid Fiber Market Outlook & Future Trends

Technology Trends

Material development in the automotive sector continues to move toward layered performance rather than single-property optimization. Emerging trends in advanced automobile materials involve the combination of aramid fibers with resins, metals, and thermoplastics in order to develop high strength composites that withstand heat, friction, and repeated loads. Hybrid material systems are also on the rise as manufacturers look for an equilibrium solution. Aramid fibers reinforce high-stress areas in vehicles, while other materials control costs.

EV & Autonomous Vehicle Impact

Electrification introduces new stress points where aramid fibers fit naturally. Battery packs have requirements related to thermal insulation, flame resistance, hence the application of aramid papers or composites in the thermal management of batteries. On the contrary, the advent of autonomous or electric vehicle platforms focuses on the development of lightweight safety solutions that balance the weight of batteries, along with the susceptibility of the electronics.

Long-Term Market Outlook (to 2034)

- The automotive aramid fiber market forecast indicates steady, application-led expansion rather than widespread material substitution across vehicles.

- Adoption accelerates primarily in components where performance benefits clearly justify higher material costs.

- Key risk factors include volatility in raw material pricing, competition from alternative high-performance fibers, and uneven vehicle production cycles across regions.

- Upside potential strengthens with tighter safety regulations, scaling of EV platforms, and broader use of hybrid composite systems.

- The future of automotive aramid fiber remains anchored in selective, high-value integration, supporting stable demand growth through 2034 rather than rapid market acceleration.

Industry Developments

- November 2025: Teijin Aramid unveiled Twaron NEXT; Teijin Aramid’s next-generation para-aramid fiber with improved performance properties and processability and enhanced sustainability. The product’s announcement had a significant impact on the market of automotive aramid fibers as it made lighter and stronger materials available for use in vehicle safety and weight reduction.

Automotive Aramid Fiber Market Segmentation

By Type Outlook (Revenue, USD Million, 2021-2034)

- Para-Aramid Fiber

- Meta-Aramid Fiber

By Fiber Form Outlook (Revenue, USD Million, 2021-2034)

- Aramid pulp

- Staple fiber

- Yarn & fabric

- Chopped fiber

By Application Outlook (Revenue, USD Million, 2021-2034)

- Brake Pads & Clutch Facings

- Tires & Tire Reinforcement

- Hoses, Belts & Gaskets

- Heat Shields & Insulation

- Automotive Composites & Structural Components

By Regional Outlook (Revenue, USD Million, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Automotive Aramid Fiber Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 929.82 Million |

| Market Size in 2026 | USD 988.27 Million |

| Revenue Forecast by 2034 | USD 1,620.99 Million |

| CAGR | 6.4% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Automotive Aramid Fiber Market FAQ's

The global market size was valued at USD 929.82 million in 2025 and is projected to grow to USD 1,620.99 million by 2034.

The?Asia Pacific region holds the largest share in the automotive aramid fiber market, due to the region’s position as a global automotive manufacturing hub, where scale, cost efficiency, and production density converge.

Brake Pads & Clutch Facings are the leading application, driven by thermal stability, fade resistance, and consistent friction performance.

A few of the key players in the market are China National Bluestar (Group) Co., Ltd., DuPont de Nemours, Inc., Huvis Corporation, Hyosung Corporation, Kermel S.A., Kolon Industries, Inc., SINOPEC Yizheng Chemical Fibre Company Limited, Teijin Limited, Toray Chemical Korea Inc., and Yantai Tayho Advanced Materials Co., Ltd.

Key factors include EV adoption and thermal management needs coupled with safety and durability requirements.

Key factors include EV adoption and thermal management needs coupled with safety and durability requirements.

Download Sample Report of Automotive Aramid Fiber Market

Please fill out the form to request a customized copy of the research report.