Automotive Repair And Maintenance Market Size, Share, Growth | Trends, 2026-2034

REPORT DETAILS

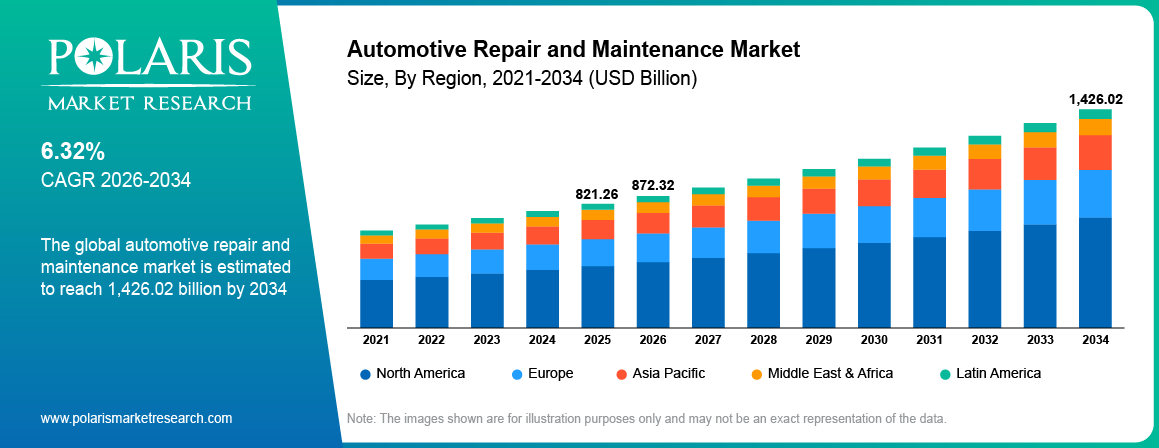

Automotive Repair and Maintenance Market Summary

The global automotive repair and maintenance market is estimated around USD 821.26 Billion in 2025,?with consistent growth anticipated during 2026–2034. Expansion is driven by aging vehicle fleets, increasing vehicle complexity, and rising demand for preventive and predictive maintenance services. The market is projected to grow at a CAGR of 6.32% during the forecast period.

Market Statistics

Key Takeaways

- North America automotive repair market is mature, accounting for approximately 37.80% market share due to high vehicle parc and established service networks.

- Asia Pacific auto repair market is the fastest growing, registering a CAGR of approximately 12.95% driven by rising vehicle ownership and expanding aftermarket services.

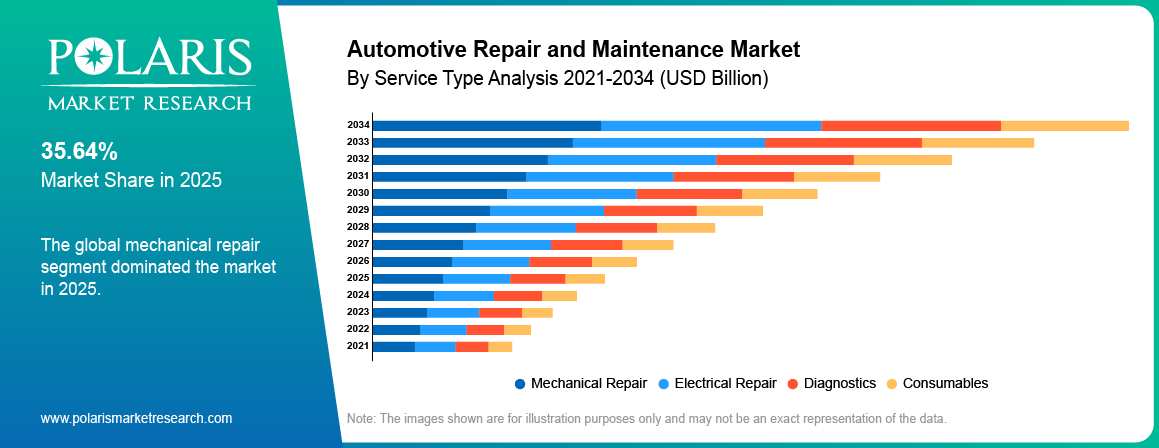

- Mechanical repair dominated the automotive repair and maintenance market, holding approximately 42.30% market share due to frequent wear and tear components.

- Passenger vehicles dominated the passenger car repair market segment, contributing approximately 45.60% market share due to large global vehicle base.

- Independent garages accounted for the largest share, holding approximately 39.40% market share due to cost-effective services and widespread availability.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Increasing average vehicle age is strengthening demand for repair, replacement parts, and routine maintenance.

- Rising complexity of vehicles, including ADAS and EV systems, is increasing demand for advanced diagnostics and skilled technicians.

- Diagnosis and servicing are expensive and have acted as a deterrent in price-sensitive environments.

- Integration of AI, automotive telematics, and predictive maintenance is opening new opportunities in intelligent automotive servicing.

What is the Automotive Repair and Maintenance Market?

Automotive repair refers to fixing or replacing faulty components such as engines, brakes, and transmissions after failure. Maintenance comprises the regular maintenance practices like change of oil, rotating tires, inspections, and preventive servicing to guarantee vehicle functionality. The market scope refers to servicing labor, diagnosis, and replacement parts for the automotive service industry, whereas the aftermarket value consists of parts and service provided by independent and authorized providers.

Estimations of market size will differ depending on the sources used as they include different coverage, ranging from independent garages, OEMs workshops, and whether parts or labor income is considered. The automotive aftermarket service market continues to expand as vehicle parc ages and ownership cycles extend, supporting steady vehicle maintenance market growth.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

Drivers & Opportunities

Aging Vehicle Fleet: Increasing average vehicle age is extending the lifecycle of vehicles on the road, which raises demand for repair, replacement parts, and routine maintenance. Older vehicles demand more maintenance in engines, braking system, and suspension parts. According to S&P Global Mobility, the average age of a car in the US was 12.8 years in 2025. This trend is expanding service volumes for independent workshops and OEM service networks, strengthening steady revenue generation in the automotive repair and maintenance market.

Rising Repair Complexity (ADAS, EV, electronics): Integration of advanced driver assistance systems, electric powertrains, and connected vehicle electronics is increasing diagnostic and repair complexity. A modern car needs special equipment, software calibration, and professionals to be serviced accurately. According to JATO Dynamics, ADAS penetration stood at 8.3% in H1 2025, showing how fast the market grew with its innovative features. This level of complexity is boosting the demand for specialized services, pushing value-added repairs among garages.

Restraints & Challenges

High Diagnostic Costs: ADAS and electric vehicle components necessitate advanced diagnostic equipment and software, thereby raising the cost of repair work. Calibration work on these systems is time-consuming and costly, thus making it difficult to conduct frequent servicing in price-sensitive markets.

Opportunity

Predictive Maintenance and AI Diagnostics: The increase in use of sensor technologies and telematics is promoting predictive maintenance practices that help predict problems in advance. The implementation of AI-based diagnostic systems in real-time vehicle data analysis enhances the efficiency of diagnosing faults and minimizing downtime. In December 2025, YOUCANIC introduced the ability to perform diagnostics with the use of artificial intelligence through its UCAN-II-C scanner, which facilitates the real-time analysis of problem codes along with repairing instructions. This will help improve the efficiency of the diagnosis process while encouraging adoption of smarter repair solutions.

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the automotive repair and maintenance market by service type, vehicle type, and service provider to help readers identify the fastest expanding and most attractive demand segments.

By Service Type

-

Mechanical Repair

Mechanical repair dominated the automotive repair and maintenance market due to its high frequency and essential nature across vehicle lifecycles. Engine repair market segment and brake system maintenance services generate consistent revenue as wear-and-tear components require periodic replacement.

-

Diagnostics

The diagnostics segment is the fastest-growing sector owing to the rising complexity of automobiles, along with increased electronics in the vehicles. Modern vehicles cannot be diagnosed without advanced diagnostic equipment.

By Vehicle Type

-

Passenger Vehicles

Passenger vehicles dominated the passenger car repair market segment in terms of size due to their high production and ownership. High maintenance needs as well as frequent servicing contribute to consistent demand and account for most revenue. As per Society of Indian Automobile Manufacturers (SIAM), the number of passenger vehicles sold in India during March 2026 increased by 14.1% compared to last year, reaching 376,268 vehicles, which is a record sale, adding to the demand for after-sales service.

-

Electric Vehicles (EVs)

Electric vehicles are experiencing an explosive increase in sales, being the fastest-growing segment. Electric vehicles have special diagnostic and battery maintenance requirements, resulting in additional sources of revenue. Based on the data of International Energy Agency, more than 17 million electric vehicles were sold throughout the world in 2024, up more than 25% from the previous year.

By Service Provider

-

Independent Garages

The independent garage accounted for the largest share in the OEM against independent garage market owing to its pricing benefits and ease of access. The independent garage provides services related to vehicle servicing and repair at lower prices and flexible conditions, thus attracting many customers, especially those who do not have vehicles under the warranty period.

-

Mobile Car Repair Services

Mobile car repair services are the fastest growing segment owing to the convenience factor as well as the rising trend of on-demand servicing. Mobile car repair service companies are gaining momentum as consumers prefer to have their vehicles fixed without having to drive anywhere.

Comparative Insight (OEM vs independent):

The OEM service center companies specialize in working with particular vehicle brands and use authentic spare parts, leading to higher costs, but consumers find them highly reliable for repairing their new vehicles. The independent garages hold an edge owing to affordability and convenience.

Source: Polaris Market Research Analysis

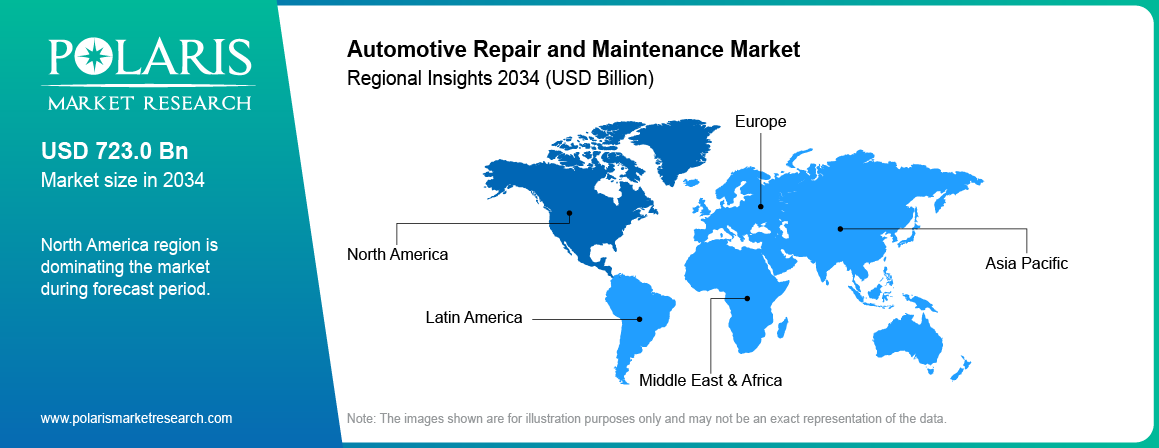

Regional Analysis

North America Automotive Repair and Maintenance Market Assessment

North America automotive repair market is mature and high-value due to a large and aging vehicle fleet in the US and a well-established service infrastructure. The region boasts a robust distribution of OEM service centers, independent garages, and franchised repair shops. Car maintenance US market is boosted by longer product life cycles and the complexity of today's automobiles. According to the International Energy Agency, there were over 1.6 million electric vehicles sold in the US during 2024, representing more than 10 percent of the country's market share.The trend boosts the market demand for specialized diagnostics and repair, fueling growth in the automotive service sector of the US.

Europe Automotive Repair and Maintenance Market Overview

Europe vehicle maintenance market is influenced significantly by tough regulatory requirements for the vehicles safety and emissions levels. The legislative environment in the European Union dictates the need for inspections and repairs to comply with regulations, contributing to higher demand for automotive repair services. The aging vehicle fleet provides further impetus for steady aftermarket consumption. Germany and France are the countries boasting robust aftermarkets for the automotive industry with highly qualified personnel working in the repair facilities.

Asia Pacific Automotive Repair and Maintenance Market Insight

Asia Pacific auto repair growth is the fastest due to rapid urbanization and rising vehicle ownership across China and India. An increase in disposable incomes and a growth in middle-class populations are stimulating car purchases and operations. According to UN-Habitat, Asia’s urban population is expected to grow by 50% by 2050, adding around 1.2 billion people.The Chinese automotive aftermarket industry is growing, due to a substantial car parc and increased service networks. India vehicle maintenance market is also rising with increasing demand for organized service providers. This expanding vehicle base continues to support strong aftermarket services across the region.

Rest of the World Automotive Repair and Maintenance Market Assessment

Automotive repair market emerging regions in Latin America, the Middle East, and Africa are witnessing steady growth due to rising vehicle penetration and improving infrastructure. The Middle East region will experience more demands for vehicle maintenance due to high levels of vehicle ownership and expensive vehicle maintenance requirements. In Latin America, there are more opportunities for vehicle repairs due to more sales of second-hand vehicles. In Africa, there are prospects for the growth of vehicle maintenance activities due to urbanization and infrastructure development.

Source: Polaris Market Research Analysis

Competitive Landscape

Key Players & Strategic Developments

The automotive repairs and servicing industry is moderately fragmented with a combination of OEM affiliated repair shops, aftermarket services from independent companies, and specialized repair shops in operation. Automotive repair market key players compete based on service quality, turnaround time, pricing models, and expanding digital service capabilities.

Key players operating in the market include Asbury Automotive Group, Inc., Belron International Limited, Bridgestone Corporation, CarMax, Inc., Continental AG, Denko Corporation, Driven Brands Holdings Inc., Firestone Complete Auto Care, Halfords Group Plc, Jiffy Lube International, Inc., LKQ Corporation, Mobivia Groupe, Monro, Inc., Robert Bosch GmbH, and TVS Motor Company Limited.

Future Outlook & Premium Insights

Market forecast (2034 outlook)

The automotive repair market forecast indicates steady expansion driven by aging vehicle fleets, increasing vehicle parc, and rising complexity in automotive systems. In the future, the automotive servicing will move into the realm of technology-based diagnosis and repairs especially that for electric vehicles and connected vehicles.

High-growth opportunity areas

The main growth drivers are growth in EV repairs, diagnostics, and fleet maintenance services. With more connected vehicles on the roads, the need for predictive maintenance will grow significantly due to faults can be detected before there is any major downtime.

Fleet companies and mobility platforms will fuel demand, whereas independent service shops can achieve growth by offering specialty services and digital services.

Disruptive trends

-

Future of EV servicing

EV servicing is expected to revolutionize the industry due to reduced wear on mechanical parts but greater requirements for battery diagnosis, software updates, and power electronics maintenance.

-

Digital transformation of workshops

Workshops are increasingly using digital technologies and artificial intelligence diagnostics, as well as automated workshop management systems.

-

Subscription-based maintenance models

Servicing subscription services and packages are becoming more popular because of their predictability and high customer retention rates.

In the next 10 years, we should expect a growing share of servicing using digital and technological innovations in the automotive market, including opportunities in EVs and fleet maintenance.

Key Players

- Asbury Automotive Group, Inc.

- Belron International Limited

- Bridgestone Corporation

- CarMax, Inc.

- Continental AG

- Denko Corporation

- Driven Brands Holdings Inc.

- Firestone Complete Auto Care

- Halfords Group Plc

- Jiffy Lube International, Inc.

- LKQ Corporation

- Mobivia Groupe

- Monro, Inc.

- Robert Bosch GmbH

- TVS Motor Company Limited

Industry Developments

- March 2026: AutoTechIQ introduced AutoQuoteIQ, an artificial intelligence-based solution that is expected to help automate the process of creating repair estimates. [Source: www.prnewswire.com]

- November 2025: Revv unveiled a number of enhancements to its platform such as Claims Builder, Advanced Billing System, and an Integrations Ecosystem for repair workflows.[source: www.prnewswire.com]

Automotive Repair and Maintenance Market Segmentation

By Service Type Outlook (Revenue, USD Billion, 2021-2034)

- Mechanical Repair

- Electrical Repair

- Diagnostics

- Consumables

By Vehicle Type Outlook (Revenue, USD Billion, 2021-2034)

- Passenger Vehicles

- Commercial Vehicles

- EVs

- Luxury Vehicles

By Service Provider Outlook (Revenue, USD Billion, 2021-2034)

- OEM service centers

- Independent garages

- Franchise workshops

- Mobile repair services

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Automotive Repair and Maintenance Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 821.26 Billion |

| Market Size in 2026 | USD 872.32 Billion |

| Revenue Forecast by 2034 | USD 1,426.02 Billion |

| CAGR | 6.32% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Automotive Repair And Maintenance Market FAQ's

The global market size was valued at USD 821.26 Billion in 2025 and is projected to grow to USD 1,426.02 Billion by 2034.

North America dominated the market share due to a large aging vehicle fleet, strong aftermarket ecosystem, and advanced service infrastructure.

Passenger vehicle owners account for the largest share due to high vehicle volume and frequent servicing requirements.

A few of the key players in the market are Asbury Automotive Group, Inc., Belron International Limited, Bridgestone Corporation, CarMax, Inc., Continental AG, Denko Corporation, Driven Brands Holdings Inc., Firestone Complete Auto Care, Halfords Group Plc, Jiffy Lube International, Inc., LKQ Corporation, Mobivia Groupe, Monro, Inc., Robert Bosch GmbH, and TVS Motor Company Limited.

Growth is driven by aging vehicles, increasing repair complexity, and rising demand for preventive maintenance services.

Trends include predictive maintenance, AI-based diagnostics, EV servicing, and digital service platforms.

Costs include labor charges, replacement parts, diagnostic fees, and overhead expenses such as equipment and facilities.

Telematics enables real-time vehicle monitoring, predictive maintenance, and early fault detection.

Opportunities include EV servicing, mobile repair services, digital platforms, and AI-based diagnostics.

Download Sample Report of Automotive Repair And Maintenance Market

Please fill out the form to request a customized copy of the research report.