Dc Distribution Network Market Analysis Report, 2026-2034

REPORT DETAILS

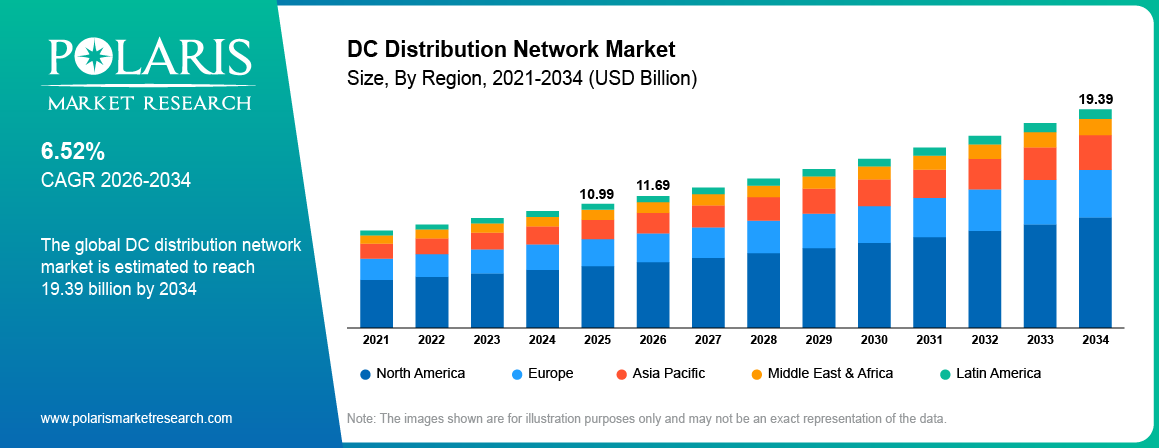

DC Distribution Network Market Summary

The global DC distribution network market is estimated around USD 10.99 Billion in 2025,with consistent growth anticipated during 2026–2034. Expansion is driven by increasing demand for energy-efficient power systems, rapid growth of AI-driven data centers, and rising deployment of EV charging infrastructure and renewable energy systems. The market is projected to grow at a CAGR of 6.52% during the forecast period.

Market Statistics

Key Takeaways

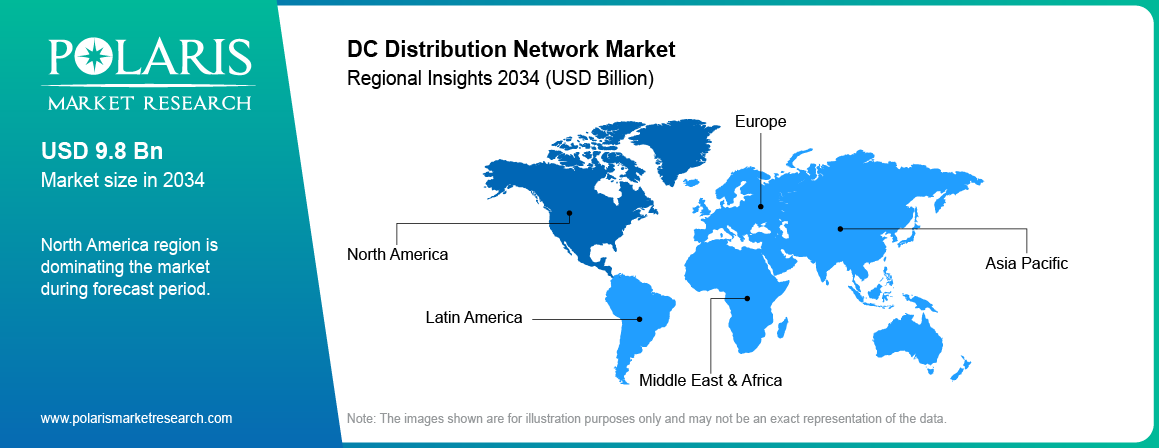

- North America is dominating the DC distribution market, accounting for approximately 38.90% market share due to advanced infrastructure and high data center investments.

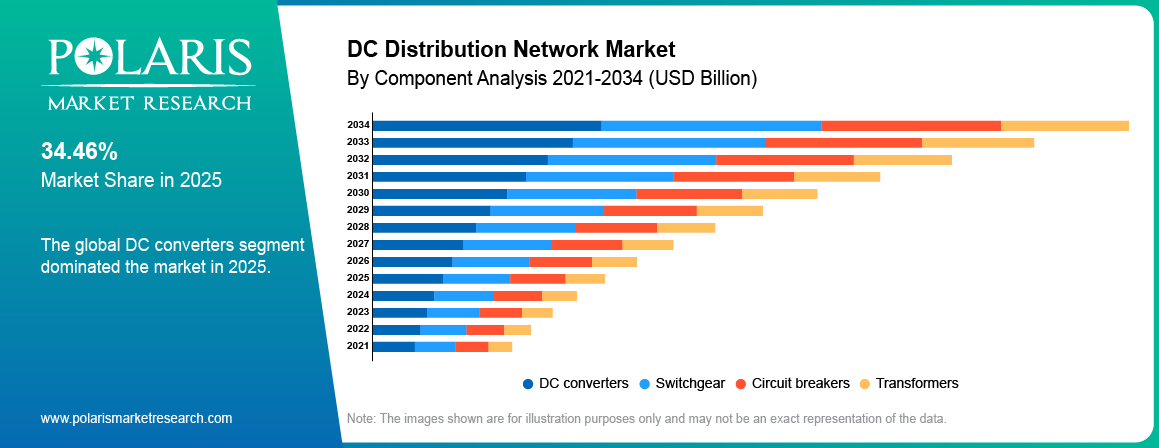

- DC Converters & Inverters was the dominant segment, holding approximately 36.75% market share due to critical role in power conversion and efficiency.

- Low voltage DC (LVDC) was the largest share in the market, contributing approximately 41.20% market share due to wide adoption in commercial and telecom applications.

- New installations dominated the market, accounting for approximately 44.35% market share due to increasing deployment of modern DC systems.

- Data centers accounted for the leading market share, holding approximately 39.80% due to rising demand for energy-efficient power distribution.

- IT & telecom held the largest share, contributing approximately 37.60% market share due to continuous expansion of digital infrastructure.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Increasing focus on energy efficiency is strengthening adoption of DC distribution networks across modern infrastructure.

- Development of EV charging stations is increasing the need for power supplies based on DC systems.

- Expensive installation and need for infrastructure modification are restricting the development of such solutions.

- The emergence of smart grids, microgrids, and AI data centers is creating new opportunities for the market.

What is the DC Distribution Network Market?

DC distribution network is defined as an electric power network that transmits electrical energy in the form of direct current through a simplified architecture whereby the power source, such as solar panels and batteries, feeds the load without any conversion process. The design of dc distribution network architecture saves on energy as there is no alternating direct current conversion.

Differences in estimates within the global dc distribution systems market come from the voltage range used, whether microgrid is considered, and applications covered. DC distribution networks offer the option of transmitting electrical energy in the form of direct current through buildings, data centers, electric vehicles, and renewables.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The growth of the dc distribution network market is gaining momentum due to changes in the way electricity is consumed and produced. Increasing use of AI-powered data centers, development of EV charging stations, and implementation of solar and battery technologies are contributing to the demand. DC systems require less energy to perform than AC systems by removing several conversion steps. Such benefits helps DC systems emerge as an attractive option for the future.

Drivers & Opportunities

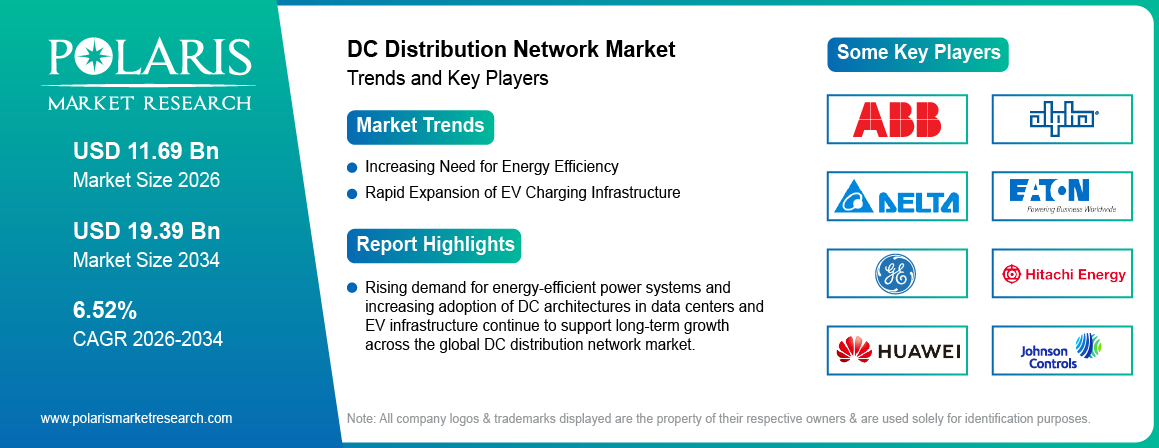

Increasing Need for Energy Efficiency: Growing need to minimize loss of energy during transmission and enhance efficiency in power conversion is boosting the usage of DC distribution networks. DC systems eliminate multiple AC-DC conversion stages, which reduces energy loss in applications such as data centers, renewable integration, and industrial power systems. According to the IEA, global efforts to double energy efficiency improvements by 2030 are driving infrastructure upgrades. This trend is making DC grids popular in high-efficiency locations where power stability plays an important role in reducing costs.

Rapid Expansion of EV Infrastructure: Growth of EV charging infrastructure are increasing the demand for power distribution based on the use of direct current driven by the ability to charge batteries and use fast charging services. Direct current fast chargers use high-power DC energy, which contribute to the development of DC distribution networks within charging stations and cities. According to the International Energy Agency, more than 20 percent of all cars purchased in the world were electric in 2024, totaling 17 million cars.This expansion is driving investment in DC grid architecture to support high-load EV charging and reduce conversion inefficiencies.

Restraints & Challenges

High Initial Installation Costs: The installation process for DC grids involves use of DC switchgears, protection devices, and converters. This results in expensive installation and redesign costs, especially when upgrading from the current AC system, thus hindering the growth of the market.

Opportunity

Emergence of Smart Grids, Microgrids, and AI-driven Data Centers: The rise of renewable sources of power generation, edge computing, and dense data centers is projected to drive the adoption of power grids that are efficient and highly scalable. DC microgrids enable better integration of photovoltaic cells, battery storage, and DC loads, thus increasing their efficiency. The AI-based data center needs to be powered by highly dense and dependable sources of energy, which makes DC power supply preferable to AC as it leads to lower losses.

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the DC distribution network market by component, voltage range, installation type, application, and end-user to help readers identify the fastest expanding and most attractive demand segments.

By Component

-

DC converters

DC Converters & Inverters was the dominant segment owing to its fundamental importance in the field of power conversions in dc grids. Such devices regulate ac to dc and dc to dc conversion which allows for an effective transfer of energy in dc distributions in data centers, electric vehicle charging stations, and renewable energy sources.

-

Circuit

Circuit breakers technology is the fastest-growing segment, owing to high demand for advanced protection in dc grids. DC fault interruption is a highly complicated process compared to AC fault interruption which led to innovations in the field.

By Voltage Range

-

Low voltage DC

Low voltage DC (LVDC) was the largest share in the market owing to its usage in buildings, telecommunication infrastructure, and dc distribution in data centers. LVDC helps to deliver power efficiently from sources like lighting, servers, and other electronic equipment.

-

Medium voltage DC

Medium voltage DC (MVDC) are projected to witness the highest growth in the market propelled by the applications in industrial equipment, electric vehicle charging stations, and renewable energy generation. MVDC facilitates increasing power transmission at an enhanced efficiency rate and it is ideal for next-gen dc distribution renewable energy systems.

By Installation Type

-

New installations

New installations dominated the market as most DC distribution networks are deployed in greenfield projects such as data centers, EV charging stations, and renewable plants. These projects allow optimized DC architecture design from the outset.

-

Retrofit installations

Retrofit installations are the fastest-growing segment driven by dc grid modernization efforts. The existing AC systems are now replaced or updated with hybrid or DC systems without the need to change the entire infrastructure, thus minimizing energy losses while improving efficiency.

By Application

-

Data centers

Data centers accounted for the leading market share as the use of DC distribution in data centers helps save energy by reducing the power conversion levels. The hyperscale centers are using DC technology owing to operational cost benefits and better power efficiency.

-

EV charging

EV charging anticipated to grow rapidly as dc power used in EV charging allows for quick deployment of the infrastructure. The demand for MVDC networks and converters arises from the use of high-power DC fast chargers.

By End-User

-

IT & telecom

IT & telecom held the largest share due to high reliance on stable and efficient DC power systems. DC networks telecom infrastructure and data centers require uninterrupted power supply, making DC distribution a preferred architecture.

-

Utilities

Utilities are the fastest-growing segment driven by dc power utilities sector transformation and grid modernization initiatives. Utilities are exploring DC systems for integrating renewables, storage, and microgrids.

Source: Polaris Market Research Analysis

Regional Analysis

North America DC Distribution Network Market Assessment

North America is dominating the DC distribution market in 2025 driven by strong data center infrastructure and rising hyperscale cloud investments in the US. Data centers are embracing DC power distribution as an effective means of improving energy efficiency while minimizing losses due to conversion. In April 2026, Microsoft expanded its data center activities in Cheyenne, Wyoming, purchasing about 3,200 acres. Investments in the project were expected to exceed USD 68 million and would allow for the provision of extensive cloud computing capacity. Expansion in such facilities is a reflection of the growing need for energy-efficient power distribution in data centers.

Europe DC Distribution Network Market Overview

Europe DC grid market growth is primarily attributed to stringent renewable energy policy goals and incorporation of distributed energy systems. Under the Renewable Energy Directive, which was amended to EU/2023/2413, the continent must achieve a minimum 42.5% renewable energy supply in 2030, while the target stands at 45%.Such developments are creating increasing opportunities for energy-efficient DC systems to ensure the incorporation of solar, wind, and storage technology.

Asia Pacific DC Distribution Network Market Insight

Asia-Pacific is projected to grow at a rapid pace during the forecast period, fueled by increasing adoption of electric vehicles and growing industrial application of electricity in China and India. DC is extensively applied in EV charging stations and energy storage based on batteries. The International Energy Agency reported the sales of electric vehicles rose by almost 40% in China during 2024, making it a stronger market player internationally. This rapid EV expansion is driving demand for DC distribution networks across transport, manufacturing, and energy sectors in the region.

Middle East & Africa DC Distribution Network Market Assessment

DC distribution in the Middle East & Africa is gaining momentum because of increasing attention paid to renewable energy solutions and projects involving intelligent infrastructure. In the Middle East, countries are investing in solar energy production facilities and energy-efficient systems, which promotes deployment of DC distribution systems. Similarly, in Africa, there is growing implementation of decentralized energy systems to ensure electricity generation in rural areas.

Source: Polaris Market Research Analysis

Competitive Landscape

Key Players & Strategic Developments

The competitive scenario within the DC distribution network industry shows considerable engagement by the international manufacturers of electric equipment and power electronics, as well as new players that specialize in DC grids and work towards developing future-oriented solutions for power distribution. The main competitors within the market leverage their expertise in areas such as DC switchgear, energy storage, and smart grids.

Key players operating in the market include ABB Ltd., Alpha Technologies Inc., Delta Electronics, Inc., Eaton Corporation PLC, General Electric Company, Hitachi Energy Ltd., Huawei Digital Power Technologies Co., Ltd., Johnson Controls, Inc., Mitsubishi Electric Corporation, Nextek Power Systems Inc., Phoenix Contact GmbH & Co. KG, Robert Bosch GmbH, Schneider Electric SE, Secheron SA, and Siemens AG.

Premium Insights & Future Outlook

Future of DC Distribution Networks

The future of dc distribution networks is shaped by rising electrification, renewable integration, and efficiency requirements. DC systems are gaining relevance in data centers, EV infrastructure, and microgrids due to lower conversion losses and better compatibility with renewable energy sources. The dc network outlook 2034 indicates gradual but accelerating adoption as standards mature and interoperability improves.

Investment Opportunities & Growth Areas

Some of the most important investment and growth opportunities for the dc grid market are expected in EV chargers, data centers, telecommunication services, and building-based microgrids. In addition, there has been significant investment in power electronics, DC converters, and protection systems.

Factors such as falling costs of DC systems, enhanced safety regulations, and compatibility with renewable-rich grids are projected to boost widespread adoption. The high cost of infrastructure required initially and lack of standardization are among the challenges faced.

Key Adoption Trends (AI, EVs, smart grids)

The development of DC distribution networks is highly associated with the evolution of AI-powered energy management systems, electric vehicle ecosystems, and smart grids. The use of AI allows for efficient management of loads and predictive maintenance, making networks more effective.

The rapid adoption of electric vehicles is anticipated to increase the need for DC fast charging solutions, whereas intelligent grids will ensure distributed and flexible electricity supply. These factors will speed up the implementation of DC networks, especially in energy-hungry and digital societies.

Key Players

- ABB Ltd.

- Alpha Technologies Inc.

- Delta Electronics, Inc.

- Eaton Corporation PLC

- General Electric Company

- Hitachi Energy Ltd.

- Huawei Digital Power Technologies Co., Ltd.

- Johnson Controls, Inc.

- Mitsubishi Electric Corporation

- Nextek Power Systems Inc.

- Phoenix Contact GmbH & Co. KG

- Robert Bosch GmbH

- Schneider Electric SE

- Secheron SA

- Siemens AG

Industry Developments

- April 2026: Siemens released its Electrification X “E-RA” DC product range, featuring innovative DC distribution systems that enhance energy efficiency, grid reliability, and incorporation of renewable energy generation systems. [source: press.siemens.com]

- September 2025: U.S. Department of Energy initiated the “Feeder of the Future” Challenge to develop modern electricity distribution feeder systems that can manage fluctuating loads, distributed energy sources, and dynamic grid interaction systems. [source: www.distributech.com]

DC Distribution Network Market Segmentation

By Component Outlook (Revenue, USD Billion, 2021-2034)

- DC converters

- Switchgear

- Circuit breakers

- Transformers

By Voltage Range Outlook (Revenue, USD Billion, 2021-2034)

- LVDC

- MVDC

- HVDC distribution

By Installation Type Outlook (Revenue, USD Billion, 2021-2034)

- New

- Retrofit

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Data centers

- EV charging

- Telecom

- Renewables

- Buildings

By End-User Outlook (Revenue, USD Billion, 2021-2034)

- IT & telecom

- Industrial

- Utilities

- Transportation

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

DC Distribution Network Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 10.99 Billion |

| Market Size in 2026 | USD 11.69 Billion |

| Revenue Forecast by 2034 | USD 19.39 Billion |

| CAGR | 6.52% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Dc Distribution Network Market FAQ's

The global market size was valued at USD 10.99 Billion in 2025 and is projected to grow to USD 19.39 Billion by 2034.

North America dominated the market due to strong data center infrastructure and increasing hyperscale cloud investments.

IT & telecom accounts for the largest share due to high demand for reliable and efficient power systems.

A few of the key players in the market are ABB Ltd., Alpha Technologies Inc., Delta Electronics, Inc., Eaton Corporation PLC, General Electric Company, Hitachi Energy Ltd., Huawei Digital Power Technologies Co., Ltd., Johnson Controls, Inc., Mitsubishi Electric Corporation, Nextek Power Systems Inc., Phoenix Contact GmbH & Co. KG, Robert Bosch GmbH, Schneider Electric SE, Secheron SA, and Siemens AG.

Growth is driven by energy efficiency demand, EV expansion, and increasing adoption in data centers and renewable systems.

Trends includes smart grids, DC microgrids, AI-enabled data centers, and renewable energy adoption.

DC distribution is the method of delivering power in direct current, whereas AC involves multiple steps of conversion to power modern electronics.

It helps to reduce energy waste, improvise efficient, and streamline power infrastructure in densely packed data centers.

IT & telecom, electric vehicles, renewable energy industry, and industrial sector use DC distribution systems.

Download Sample Report of Dc Distribution Network Market

Please fill out the form to request a customized copy of the research report.