Medical Device Contract Manufacturing Market Size, Share, Growth Analysis Report, 2026-2034

REPORT DETAILS

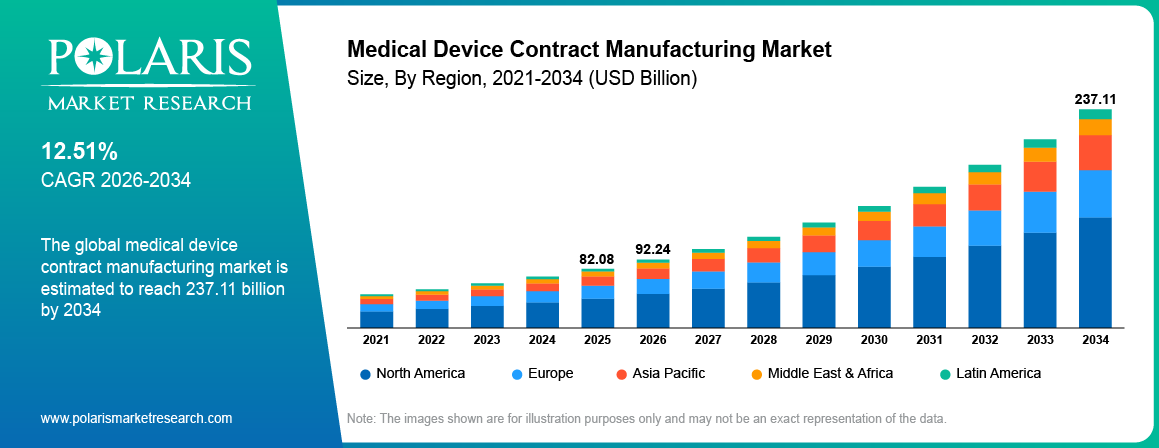

Medical Device Contract Manufacturing Market Summary

The global medical device contract manufacturing market is estimated around USD 82.08 Billion in 2025, with consistent growth anticipated during 2026–2034. Growth is driven by rising chronic disease burden and increasing aging population across global markets. The market is projected to grow at a CAGR of 12.51% during the forecast period.

Market Statistics

Medical Device Contract Manufacturing Market Summary

- North America medical device outsourcing market holds the leading share, accounting for approximately 40.75%, due to advanced healthcare infrastructure, strong OEM presence, and high outsourcing adoption.

- European medtech contract manufacturing sector witnesses robust growth, registering a CAGR of approximately 11.90%, driven by regulatory support, innovation, and expanding contract manufacturing capabilities.

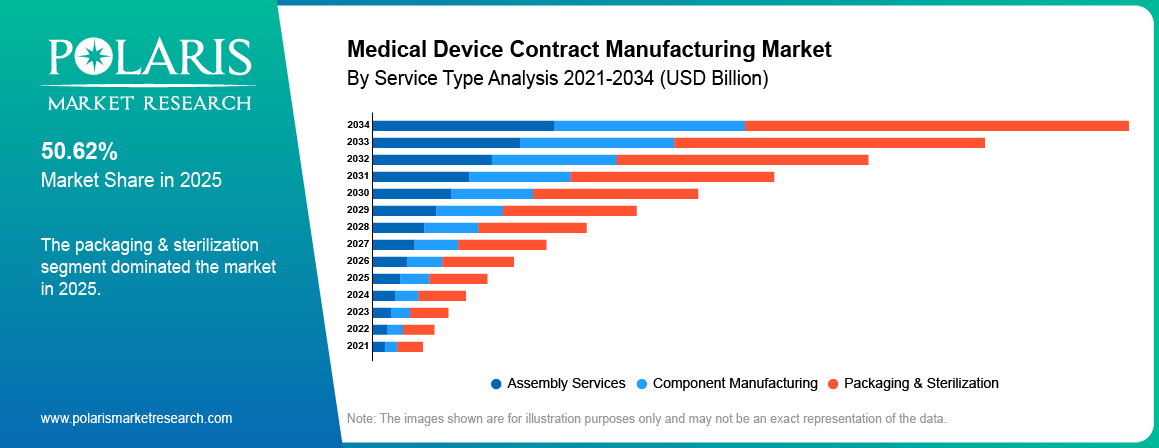

- Services segment dominated the market in 2025, holding approximately 38.60%, due to rising demand for design, testing, and regulatory compliance outsourcing services.

- The surgical devices segment was the leading segment in 2025, contributing approximately 35.45%, due to increasing surgical procedures and demand for precision-engineered medical devices globally.

- The diagnostics / IVD industry was the leading segment in 2025, accounting for approximately 33.80%, due to rising demand for early disease detection and diagnostic testing solutions.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Increasing prevalence of chronic diseases is driving demand for advanced medical device manufacturing.

- Rising aging population is increasing production requirements for healthcare devices.

- Strict regulatory approvals delay production timelines and impact product commercialization.

- Rising adoption of digital manufacturing and automation improves efficiency and supports scalable production in the medical device contract manufacturing market.

What is Medical Device Contract Manufacturing?

Medical device contract manufacturing implies that the manufacture of the device, its development and design is outsourced by specialized CDMOs to third-party entities. CDMOs offer the services to OEMs throughout all stages of the product life cycle. This strategy is used for all sorts of medical devices including diagnostic devices, surgical tools, and dental implants among others. Unlike in-house manufacturing, medical device contract manufacturing implies that OEMs do not perform manufacturing on their own but turn to a specialized entity for help. Increasing product complexity and regulatory requirements are supporting the adoption of contract manufacturing in the medical device industry.

The medical device outsourcing value chain covers end-to-end activities from product design and prototyping to full-scale manufacturing, assembly, and packaging. The CDMOs offer technical assistance, raw materials procurement, precision engineering, sterilization, and packaging of the end product. The OEMs take advantage of these services to shorten time to market and ensure quality consistency. The service companies are increasingly developing their competencies in advanced manufacturing processes and compliance management.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The growing emphasis on cost reduction and efficiency improvement is forcing OEMs to seek external partners for manufacturing functions. Growing requirements for expertise in manufacturing processes and scalability are helping the trend gain momentum. CDMO services provide greater flexibility in manufacturing and faster market introduction at lower capital expenditure for OEMs. Unlike the conventional method of manufacturing, contract manufacturing provides an integrated approach covering all functions along the value chain.

Drivers & Opportunities

Growth in Chronic Diseases Increases Demand for Advanced Medical Devices: The rising incidence of chronic diseases such as cardiovascular disease, diabetes, and respiratory disease contributes to the growing demand for advanced medical equipment. As per a report from the World Health Organization, chronic diseases that include heart disease, cancer, diabetes, and respiratory diseases, are predicted to be responsible for 86% of the 90 million deaths every year by 2048 if the current scenario continues. This factor leads to an increasing need for manufacturing advanced medical devices. Original equipment manufacturers tend to outsource more to contract development and manufacturing organizations to cope with the rising demands.

Aging Population Increases Demand for Medical Devices and Related Manufacturing: The growing proportion of the aging population will lead to an increase in demand for medical devices employed in care, monitoring, and surgery operations. According to the WHO report, in 2030, one out of six persons in the world will be over the age of 60. There will be a population growth from one billion in 2020 to 1.4 billion in 2030 and 2.1 billion in 2050. Also, the population of over 80 years old will triple from 141 million in 2019 to 426 million in 2050. As a result, there is likely to be a rise in output across all types of medical devices including implants, diagnostic devices, and home health care medical devices.

Restraints & Challenges

Strict Regulatory Approvals Delay Production Timelines and Product Launches: The existence of stringent regulations results in prolonged timelines for device approvals, affecting the manufacturing process. Regulatory compliance varies regionally, making the manufacturing process and its documentation more complex. The OEMs experience delays in the commercialization of their products since validation and certification take more time. CDMOs should be ready to invest in regulatory knowledge and quality control processes.

Opportunity

Rising Adoption of Digital Manufacturing and Automation Improves Production Efficiency: With increasing adoption of technological advancements in digital manufacturing processes like automation, robotics, and data-based production, efficiency is gained in the manufacture of medical devices. In February 2026, Made Scientific, a CDMO firm, entered into an agreement with Streamline Bio to use AI and robotic technology in cell therapy manufacturing. Digital manufacturing tools increase precision, minimize human error in the process, and ensure volume manufacturing is achieved. CDMOs adopt digitalized manufacturing processes to increase efficiency and achieve OEM demands.

Source: Polaris Market Research Analysis

Technology & Innovation Trends in Medical Device Manufacturing

Role of AI, Automation, and Smart Manufacturing

Medtech manufacturing through AI enhances process precision and minimizes human interference. The use of automation and robotics during the manufacture of medical devices boosts productivity and ensures quality assurance. Healthcare smart manufacturing systems allow for real-time tracking and predictive maintenance. Such technological advancements minimize costs and promote scalability in production processes. Modern CDMOs have a competitive edge by offering faster product delivery and improved production efficiency.

Impact of Additive Manufacturing and 3D Printing

The fabrication of medical devices using 3D printing is an innovative approach that facilitates rapid prototype development and custom design of intricate devices. The application of additive manufacturing technology in medical devices minimizes waste materials and shortens production time. This method caters to low-volume and highly precise production demands. CDMOs implementing such technologies increase production flexibility and lower costs.

Digital Transformation and Connected Device Production

Technological advancements within the field of medical device manufacturing have led to the increasing use of digital technology within the production process. The use of IoT technology, together with data analytics, has contributed to improving visibility in the production process and better quality control. In addition, digital technology contributes to coordination within the design, manufacturing, and packaging processes. Consequently, CDMOs that implement connected manufacturing systems experience greater efficiency and higher levels of customer retention.

Segmental Insights

This report offers detailed coverage of the medical device contract manufacturing market by service type, device type, and application to help readers identify the fastest expanding and most attractive demand segments.

By Service Type

-

Packaging & Sterilization

Services segment dominated the market in 2025, driven by rising outsourcing of medical device contract manufacturing activities by organizations and healthcare providers. There is an increase in the amount of sample collection, which has increased the dependence on customized testing services. The development of workplace and forensic testing programs has been fueling the need for service-based approaches.

-

Design & Development

The design & development segment is projected to grow at the fastest CAGR during the forecast period, due to increasing complexity of medical devices and rising demand for faster product commercialization. The OEMs will outsource the initial development process to save time and improve efficiencies. The CDMOs can then contribute through their engineering and prototyping capabilities as well as regulatory assistance.

By Device Type

-

Surgical Devices

The surgical devices segment was the leading segment in the global medical manufacturing market during 2025 due to the increasing number of surgeries being performed and continuous demand for accurate instruments. The OEMs outsource more products due to the increasing volume of production required and maintaining the quality. For example, in December 2025, Quvara Medical was formed into a CDMO through acquiring a factory belonging to Becton Dickinson situated in the UK for the mass manufacture of drug delivery devices. CDMOs offer scalability in manufacturing products.

-

Wearable Medical Devices

Wearable medical devices segment is projected to grow at the fastest CAGR during the forecast period, due to increasing adoption of remote monitoring and connected healthcare devices. Demand for compact and sensor-based devices increases need for flexible manufacturing. CDMOs support rapid design changes and scalable production.

By Application

-

Diagnostic / IVD

The diagnostics / IVD industry was the leading segment in the market during 2025, owing to growing demand for early diagnosis and high test volume. The OEMs delegate the manufacturing process in order to maintain steady supply and compliance with regulations.

-

Implantable Devices

The market for implantable devices is anticipated to witness the highest CAGR during the forecast period, owing to the rising requirement for sustained therapy methods and innovations in implants. Rising complexity in products leads to increasing dependency on professional manufacturing companies. CDMOs offer precise manufacturing services and compliance assistance.

Source: Polaris Market Research Analysis

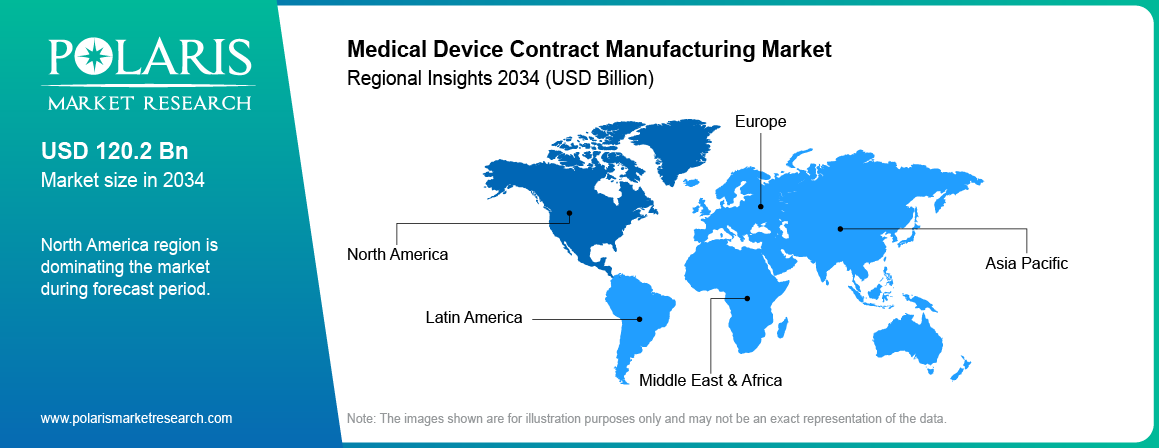

Regional Analysis

North America Market Assessment

North America medical device outsourcing market holds the leading share, driven by strong presence of OEMs and advanced healthcare infrastructure. With the emphasis on innovation and the use of AI technology, there will be an increasing need for specialized contract manufacturing organizations. In February 2026, MGS (a CDMO company) has inaugurated its new facility for the production of drug delivery devices with an area of 300,000 sq. ft. The company has established the plant to cater to its client base globally, with an increase in demand for combination products. Also, strict regulatory guidelines make the industry more dependent on seasoned contract manufacturers.

Asia Pacific Medical Device Contract Manufacturing Market Insights

Asia Pacific CDMO for medical devices is growing rapidly owing to cost effectiveness and increasing manufacturing capabilities. An example of this is the construction of a new Thailand-based manufacturing site by Quasar Medical in June 2025. This company is enhancing its capacity to manufacture CDMOs through micro-assembly and manufacturing capabilities for medical devices. In addition, the Chinese contract manufacturing of medical devices market receives support owing to large-scale manufacturing capabilities and government backing. The Indian medical device manufacturing outsourcing industry continues to grow thanks to skilled labor and increasing investment.

Europe Medical Device Contract Manufacturing Market Overview

European medtech contract manufacturing sector witnesses robust growth fueled by strict regulations like those set forth under the MDR and Regulation (EU) 2017/746 guidelines.Increasing outsourcing by OEMs helps them comply with regulation requirements and simplifies operations. Demand for precision manufacturing fuels contract manufacturing development. Outsourcing in Europe comes from Germany, France, and the UK primarily.

Source: Polaris Market Research Analysis

Competitive Landscape & Key Players

The medical devices contract manufacturing industry demonstrates a moderate level of fragmentation, where global CDMOs compete against regional players in terms of services. The primary determinants of competition in the industry involve compliance with regulations, precise manufacturing processes, and cost advantages. The top firms strive to build their capabilities and upgrade manufacturing technology for competitive advantage. Collaboration with OEMs helps secure long-term deals.

The major industry participants include Flex Ltd., Jabil Inc., Plexus Corp., Sanmina Corporation, Integer Holdings Corporation, TE Connectivity Ltd., Gerresheimer AG, West Pharmaceutical Services Inc., Celestica Inc., Freudenberg Medical, LLC, Phillips-Medisize (Molex), Nortech Systems Inc., and others.

Regulatory Landscape & Compliance Framework

Medical device manufacturing laws make a manufacturer more dependent on outsourcing due to the increasing cost of compliance. The need to comply with the FDA’s guidelines and standards and implement QMSR makes it necessary for manufacturers to seek outsourced companies with experience.

The adoption of the EU MDR/IVDR leads to a need for more documentations and clinical validations. The growing complexities lead to greater out-sourcing of these tasks to companies that have experience in handling the regulations in Europe.

Compliance with ISO 13485 is necessary for accessing the international market. Companies opt for proven CDMOs to ensure compliance to FDA medical devices and avoid unnecessary approvals.

Investment, Cost & Strategic Insights

Expensive nature of medical devices contract manufacturing in in-house facilities leads to the increasing trend of outsourcing owing to the expensive nature of the required manufacturing facility and regulations involved. In medtech, outsourcing offers improved ROI through lower capital requirements and faster time to market.

The rising trend of investments in medical devices CDMOs is indicative of the confidence held by investors, evidenced by higher levels of mergers and acquisitions (M&A) as well as capacity expansions by prominent players like Jabil Inc. and Flex Ltd.

A successful OEM outsourcing approach boosts cost effectiveness and agility. Businesses collaborate with skilled CDMOs to streamline manufacturing processes, reduce regulatory risks, and expedite time-to-market.

Key Players

- Freudenberg Medical, LLC

- Celestica Inc.

- Flex Ltd.

- Gerresheimer AG

- Integer Holdings Corporation

- Jabil Inc.

- Nortech Systems Inc.

- Phillips-Medisize (Molex)

- Plexus Corp.

- Sanmina Corporation

- TE Connectivity Ltd.

- West Pharmaceutical Services Inc.

Industry Developments

- January 2026: Agenus closed a USD 141 million collaboration with Zydus Lifesciences to advance BOT+BAL immunotherapy, securing U.S. biologics manufacturing capacity while supporting clinical development and commercialization readiness. [source: agenusbio.com]

- July 2025: Eramol announced a new sterile manufacturing facility in the UK, strengthening its CDMO capabilities for small to medium batch sterile injectables. [source: pharmasource.global]

Medical Device Contract Manufacturing Market Segmentation

By Service Type Outlook (Revenue, USD Billion, 2021-2034)

- Assembly Services

- Component Manufacturing

- Packaging & Sterilization

By Device Type Outlook (Revenue, USD Billion, 2021-2034)

- Surgical Devices

- Imaging Devices

- Wearable Medical Devices

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Cardiovascular

- Orthopedic

- Diagnostic / IVD

- Implantable Devices

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Medical Device Contract Manufacturing Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 82.08 Billion |

| Market Size in 2026 | USD 92.24 Billion |

| Revenue Forecast by 2034 | USD 237.11 Billion |

| CAGR | 12.51% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Medical Device Contract Manufacturing Market FAQ's

The global market size was valued at USD 82.08 Billion in 2025 and is projected to grow to USD 237.11 Billion by 2034.

North America dominates the market due to strong OEM presence, advanced manufacturing capabilities.

Major applications include diagnostic devices, surgical instruments, wearable devices, and implantable products.

A few of the key players in the market are Flex Ltd., Jabil Inc., Plexus Corp., Sanmina Corporation, Integer Holdings Corporation, TE Connectivity Ltd., Gerresheimer AG, West Pharmaceutical Services Inc., Celestica Inc., Freudenberg Medical, LLC, Phillips-Medisize (Molex), Nortech Systems Inc., and others.

Key drivers include rising device complexity, increasing outsourcing by OEMs, and growing demand for cost-efficient manufacturing solutions.

Major demand comes from healthcare providers, medtech companies, diagnostic firms, and implantable device manufacturers.

The market outlook remains strong due to increasing demand for advanced devices and expansion of end-to-end CDMO services.

Download Sample Report of Medical Device Contract Manufacturing Market

Please fill out the form to request a customized copy of the research report.