Residual DNA Testing Market Size, Trends, Industry Report 2026 - 2034

REPORT DETAILS

Residual DNA Testing Market Summary

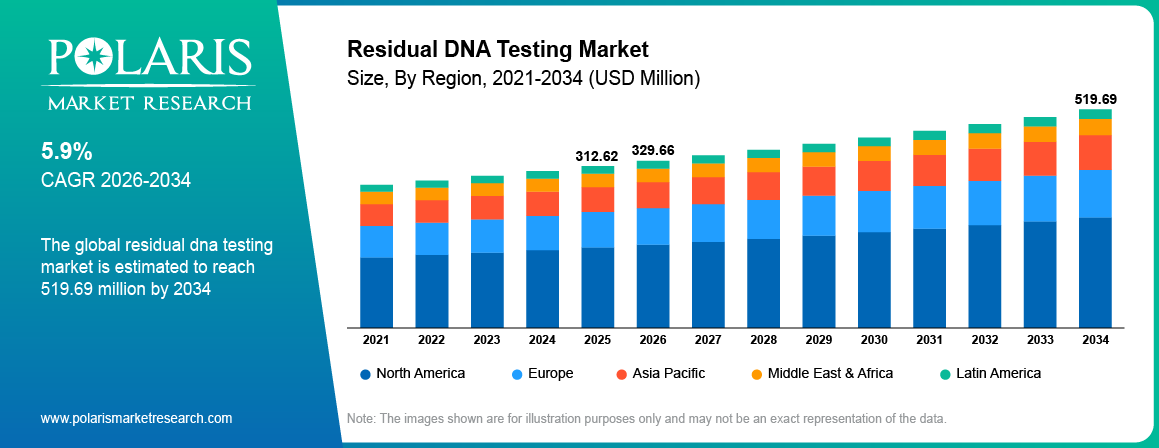

The global residual DNA testing market is estimated around USD 312.62 Million in 2025,with consistent growth anticipated during 2026–2034. Growth is driven by rising biologics and vaccine production along with increasing regulatory focus on product safety across global markets. The market is projected to grow at a CAGR of 5.9% during the forecast period.

Market Statistics

Key Takeaways

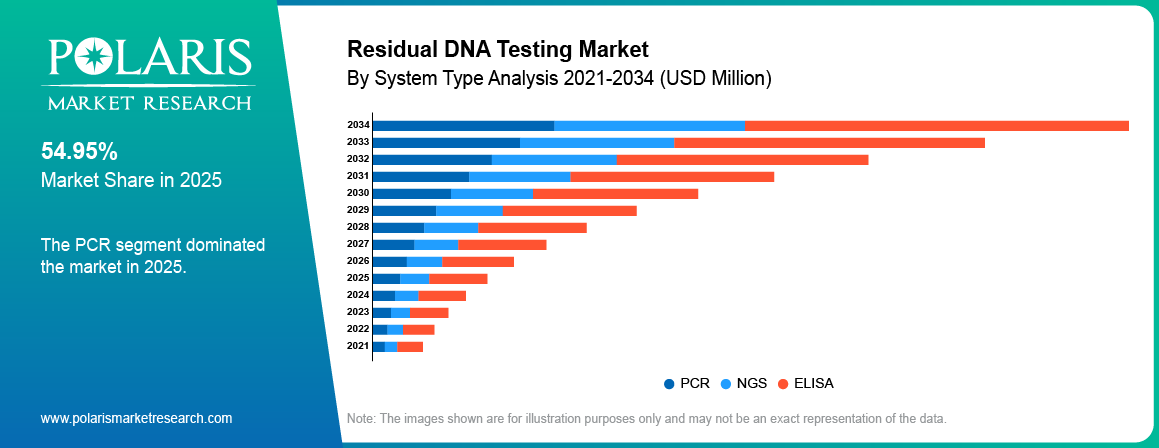

- In 2025, the PCR segment held a dominant share of 54.95% in the market due to the usage of qPCR residual DNA testing for quality control purposes.

- Kits accounted for substantial market share of 15.5% in 2025, owing to rising demand for standard and pre-packaged residual DNA testing kits.

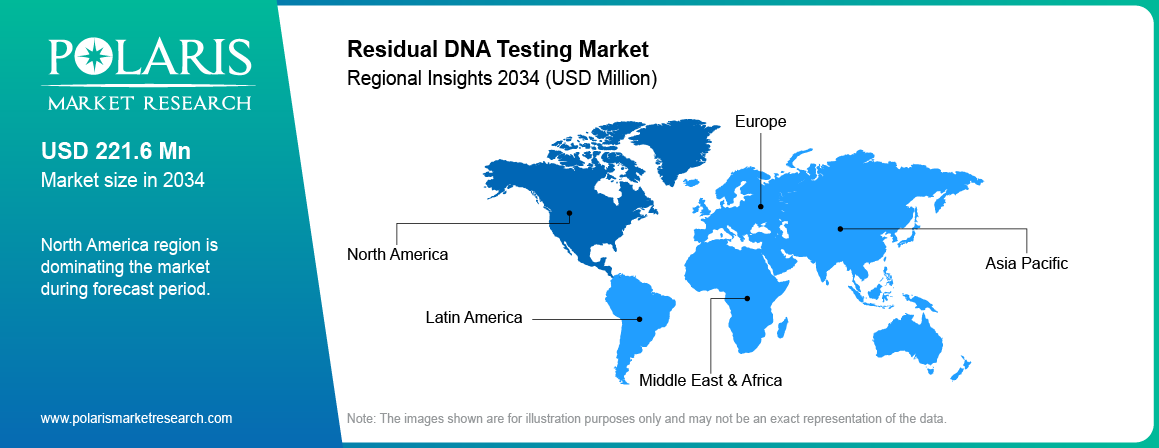

- North America residual DNA testing industry held 43.72% revenue market in 2025, driven by strong biologics production and strict regulatory requirements for product safety.

- US held approximately 80% of revenue share within North America region due to strong biopharmaceutical infrastructure and regulatory standards.

- Asia Pacific residual DNA testing industry is projected to grow at 6.5% CAGR during the forecast period, driven by rapid expansion of biologics and vaccine manufacturing.

Industry Dynamics

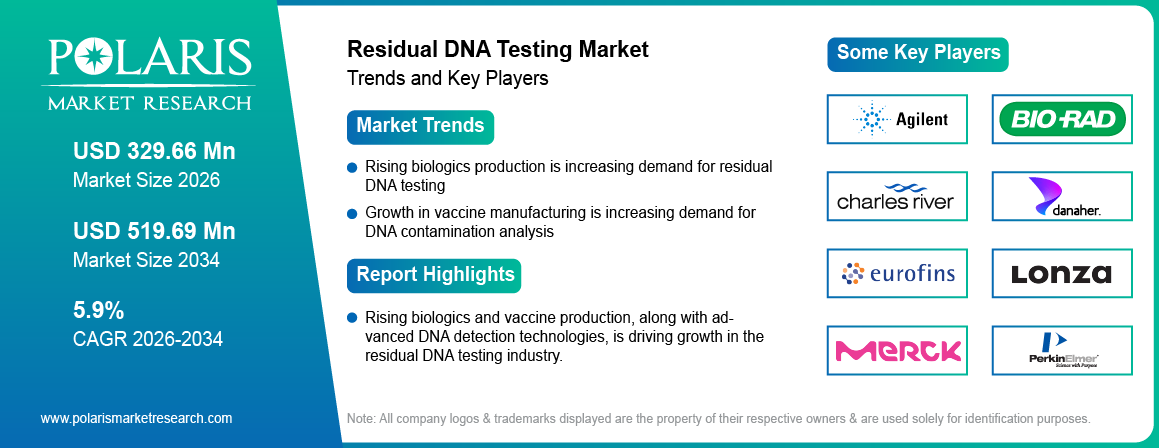

- Rising biologics production is increasing demand for residual DNA testing.

- Growth in vaccine manufacturing is increasing demand for DNA contamination analysis.

- High cost of advanced testing technologies is limiting adoption among small manufacturers.

- Adoption of digital and AI-based analytics is improving testing efficiency.

What is the Residual DNA Testing Market?

Residual DNA testing refers to the methods that are used to measure the presence and concentration of host-cell DNA in biopharmaceuticals. Residual DNA is genetic material of the host-cell culture used to produce pharmaceutical products; the host cells include mammalian Chinese hamster ovary cells, bacteria, and yeast cultures. Residual DNA testing finds application in the production of various biologics including monoclonal antibodies, vaccines, and gene therapies. The demand for residual DNA testing is growing as the market of biologics expands along with the increased demand for biologics and stringent regulations.

Residual host cell DNA analysis plays an important role in assuring biologic drug safety due to the presence of any unanticipated DNA fragments that are harmful to the patient. The regulatory bodies have established certain controls that govern the amount of residual DNA. It helps assure quality in the upstream and downstream processes. Biopharmaceuticals organizations are now giving priority to testing methods.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The need for residual DNA testing is increasing owing to the growing need for biologics, vaccines, and other advanced treatments like gene and cell therapy. The use of precise testing equipment has enhanced the accuracy and efficiency of DNA measurement. Biomanufacturing facilities and contract development companies have increased, which has resulted in greater testing requirements.

Drivers & Opportunities

Rising biologics production is increasing demand for residual DNA testing :The growth of biologics manufacturing is resulting in the requirement to detect any host-cell DNA contamination in their manufacturing process. Biopharmaceutical companies are now focusing more on purity and regulatory compliance. Testing procedures are incorporated throughout the entire process, from upstream to downstream. India’s National Biopharma Mission (i3) targets a USD 100 Million biotech industry and 5% global pharma share in 2025.[Press Information Bureau (PIB), 'Transforming India into a Global Biopharma Hub', pib.gov.in] Thus, this factor is supporting growth in the residual DNA testing industry.

Growth in vaccine manufacturing is increasing demand for DNA contamination analysis : Expansion in vaccine production is increasing the requirement for routine residual DNA testing. Global Health Press estimates annual vaccine production at 14.5 Million doses, with the market reaching USD 35 Million in 2024–2025.[International Drug Export Association, 'Global vaccine production – Estimated key figures (2025–2026)', id-ea.org] Producers are maintaining safety and uniformity in large batch production. Regulatory bodies enforce stringent DNA levels in vaccines. This aspect is driving the need for residual DNA testing services.

Restraints & Challenges

High cost of advanced testing technologies limits adoption among small manufacturers: Residual DNA testing requires advanced equipment and high technology. Small and medium sized companies face financial issues in adapting such high technology testing methods. Other costs such as those related to operation and validation of the technology further increase the burden on finances. This issue is acting as a barrier for market entry into price sensitive markets.

Opportunity

Adoption of digital and AI-based analytics is improving testing efficiency: Integration of digital tools and AI-based analytics enhances precision when analyzing quantities of DNA. The automated process minimizes errors made by human operators and cuts down processing time. There is emphasis by companies on data-driven quality assurance processes. For example, in January 2026, Google's DeepMind developed AlphaGenome artificial intelligence technology, making advancements in genetic studies.[Google DeepMind, 'AlphaGenome: AI for better understanding the genome', deepmind.google] This has had a considerable impact on the growth opportunities in the residual DNA testing market.

Source: Polaris Market Research Analysis

Technology & Methodology Landscape

qPCR vs Digital PCR vs NGS: Comparative Analysis

Methods used in residual DNA testing include qPCR residual DNA testing, digital PCR DNA quantification, and next generation sequencing DNA testing. qPCR continues to be the leading method in biopharmaceutical manufacturing owing to established procedures and acceptability by regulators. Digital PCR and NGS are becoming popular due to its greater sensitivity and accuracy when it comes to detecting DNA.

Sensitivity, Accuracy, and Cost Trade-offs

| Parameter | qPCR Residual DNA Testing | Digital PCR DNA Quantification | Next Generation Sequencing DNA Testing |

| Sensitivity | Moderate to high | Very high | Ultra-high |

| Accuracy | High | Very high | Very high |

| Turnaround Time | Short | Moderate | Longer |

| Cost | Low to moderate | Moderate to high | High |

| Validation Complexity | Low | Moderate | High |

Source: Polaris Market Research Analysis

qPCR continues to be dominant on account of lower costs, faster processing times, and fewer validation processes. Digital PCR is more accurate at low DNA concentrations while NGS provides deep sequence insights at higher costs and complexity in validation.

Automation & Next-Gen Analytical Platforms

Automation of testing equipment for residual DNA testing is increasingly becoming widespread. AI-based analyses are also becoming increasingly common. High-throughput systems are supporting large-scale biologics manufacturing. These advancements are increasing adoption of advanced DNA detection technologies across the industry.

Segmental Insights

This report offers detailed coverage of the residual DNA testing market by product and service, technology, sample type, application, and end user to help readers identify the fastest expanding and most attractive demand segments.

By Product & Service

-

Kits

Kits accounted for maximum market share in 2025, owing to rising demand for standard and pre-packaged residual DNA testing kits. Biopharmaceutical organizations are increasingly paying attention to standardization and validation of workflows. Testing kit adoption is gaining impetus with ease of use and regulatory compliance.

-

CRO Services

CRO services segment is projected to grow at the fastest CAGR during the forecast period, due to rising outsourcing of analytical testing activities. Organizations are working towards optimizing costs and ensuring efficiency. The development of contract testing facilities is helping in growing the segment.

By Technology

-

PCR

In 2025, the PCR segment held a dominant share in the market due to the usage of qPCR residual DNA testing for quality control purposes. Existing methods, along with reduced turnaround time, are fueling the segment's growth.

-

NGS

NGS segment is expected to grow with the highest CAGR over the forecast period, owing to the rising requirement for next generation sequencing technology for sensitive detection of DNA. Advanced sequencing is enhancing the efficiency of biologics testing. Increase in gene therapy will boost the acceptance of NGS method.

By Sample Type

-

In-Process

In-process segment held the largest share of the market in 2025, owing to rising emphasis on in-process monitoring in biologics testing. Early detection of DNA residuals is ensured by manufacturers through process optimization.

-

Final Product

Final product segment is projected to grow at the fastest CAGR during the forecast period, due to strict regulatory requirements for product release testing. Companies are focusing on ensuring safety and compliance before commercialization. This factor is supporting segment growth.

By Application

-

Biologics

Biologics segment dominated the market in 2025, driven by rising production of monoclonal antibodies and recombinant proteins. Residual DNA testing is essential for ensuring product purity. Expansion of biologics pipelines is supporting growth.

-

Gene Therapy

Gene therapy segment is projected to grow at the fastest CAGR during the forecast period, due to increasing development of advanced therapies. High sensitivity testing is required for complex genetic products. Growth in clinical pipelines is supporting segment adoption.

By End User

-

Biotech

Biotech segment captured the largest market share in 2025, owing to the intense emphasis on biologics and advanced therapy development. Quality control and regulatory compliance are being prioritized by companies, which are engaging themselves in R&D activities.

-

CDMOs

CDMOs segment is projected to grow at the fastest CAGR during the forecast period, due to rising outsourcing of biopharmaceutical manufacturing and testing. Service providers are expanding analytical capabilities. This factor is supporting growth in the segment.

Source: Polaris Market Research Analysis

Regional Analysis

North America Market Assessment

North America residual DNA testing industry dominated the global market in 2025, driven by strong biologics production and strict regulatory requirements for product safety. Stringent regulations for residual host-cell DNA have been imposed by the FDA in biologicals and vaccines in the US. Furthermore, the US market dominates the regional market owing to advanced infrastructure for biopharmaceuticals along with the high use of qPCR residual DNA analysis. Presence of major biotech companies and contract testing organizations is supporting market growth. In April 2025, Labcorp launched new molecular residual disease and liquid biopsy tests to support cancer detection and monitoring.[Labcorp, 'Labcorp launches molecular residual disease and liquid biopsy', ir.labcorp.com]

Asia Pacific Residual DNA Testing Market Insights

Asia Pacific residual DNA testing industry is projected to grow at the fastest CAGR during the forecast period, driven by rapid expansion of biologics and vaccine manufacturing. For instance, in May 2025, Gene Solutions collaborated with NEWCL to provide genetic testing solutions in Taiwan using next-generation sequencing (NGS) lab services.[Clival, 'Gene Solutions and NewCL partner to boost genetic testing in Taiwan', clival.com] India and China are developing biomanufacturing plants and quality control systems. Increasing government support and growth in CDMOs are improving testing demand.

Europe Residual DNA Testing Market Overview

Europe residual DNA testing market occupied the second-largest market share, backed by robust regulatory environment, along with rising production of biologics. The European Commission noted that the production of vaccines increased from 20 million to 300 million doses per month, and achieved 3 Million doses in one year.[European Commission, 'EU Vaccines Strategy', commission.europa.eu] Germany, France, and UK have steady demand for residual DNA tests owing to existing pharmaceutical manufacturing.

LATAM & MEA Emerging Markets

Latin America and Middle East & Africa Residual DNA Testing Industry is exhibiting steady growth due to improvements in healthcare facilities and increased investments in the biopharmaceuticals manufacturing sector. According to IQVIA, the total global pharmaceutical industry market is projected to grow at a rate of USD 2.32 trillion by 2028, whereas the Middle East & Africa market is expected to grow up to USD 64.1 Million.[IQVIA, 'Pharmaceutical Market Quarterly Report Q1 2024', iqvia.com] Brazil and South Africa are making improvements to their capacity for vaccine and biologics manufacturing. Contract manufacturing and slow but steady regulation developments are driving market growth.

Source: Polaris Market Research Analysis

Competitive Landscape & Strategic Insights

Key Players & Strategic Developments

The residual DNA testing industry is moderately concentrated, with players in the industry including providers of instruments, suppliers of reagents, and CROs. Competition centers around detection sensitivity, regulatory compliance, and turnaround time. The companies involved in the residual DNA testing industry have been concentrating their efforts toward the use of PCR and sequencing technology.

Some of the notable players in the market include Thermo Fisher Scientific Inc., Merck KGaA, Sartorius AG, Danaher Corporation, Bio-Rad Laboratories Inc., Agilent Technologies Inc., PerkinElmer Inc., Charles River Laboratories International Inc., Lonza Group AG, SGS SA, Eurofins Scientific SE, QIAGEN N.V., and others.

Future Competitive Outlook

The residual DNA testing industry will become highly competitive owing to the growth in the manufacture of biological drugs and stringent regulations. The emphasis has been put on sensitive test procedures and automation for better efficiency. Expansion of CRO and CDMO services is increasing competitive intensity. Strategic partnerships and technology advancements are supporting market positioning.

Premium Insights

The market for residual DNA testing is changing due to increased cell and gene therapy usage, improved regulations, and constant advancements in technology. The complex nature of modern therapies has led to higher demand for sensitive DNA testing techniques. Residual DNA regulations have become much stricter, which improves the quality control process.

Application of AI and automation technology is helping to improve the testing process and increase speed. Continuous bioprocessing is making it necessary to have real-time DNA tests. These trends are shaping the future of the residual DNA testing industry.

Key Players

- Agilent Technologies Inc.

- Bio-Rad Laboratories Inc.

- Charles River Laboratories International Inc.

- Danaher Corporation

- Eurofins Scientific SE

- Lonza Group AG

- Merck KGaA

- PerkinElmer Inc.

- QIAGEN N.V.

- Sartorius AG

- SGS SA

- Thermo Fisher Scientific Inc.

Industry Developments

- March 2026: Exact Sciences announced the presentation of new data on molecular residual disease and multi-cancer early detection. [source: exactsciences.com]

- September 2025 : Foundation Medicine launched a tissue-informed whole genome sequencing (WGS) molecular residual disease (MRD) test for research use to monitor cancer and detect recurrence across early to late-stage patients. [source: foundationmedicine.com]

Residual DNA Testing Market Segmentation

By Product & Service Outlook (Revenue, USD Million, 2021-2034)

- Kits

- Reagents

- Instruments

- CRO Services

By Technology Outlook (Revenue, USD Million, 2021-2034)

- PCR

- NGS

- ELISA

By Sample Type Outlook (Revenue, USD Million, 2021-2034)

- Raw Materials

- In-Process

- Final Product

- Fill-Finish

By Application Outlook (Revenue, USD Million, 2021-2034)

- Biologics

- Vaccines

- Gene Therapy

- Biosimilars

By End User Outlook (Revenue, USD Million, 2021-2034)

- Pharma

- Biotech

- CROs

- CDMOs

By Regional Outlook (Revenue, USD Million, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Residual DNA Testing Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 312.62 Million |

| Market Size in 2026 | USD 329.66 Million |

| Revenue Forecast by 2034 | USD 519.69 Million |

| CAGR | 5.9% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Residual DNA Testing Market FAQ's

The global market size was valued at USD 312.62 Million in 2025 and is projected to grow to USD 519.69 Million by 2034.

North America dominates the market due to strong biologics production and strict regulatory standards.

Major applications include biologics, vaccines, gene therapy, and biosimilars manufacturing.

A few of the key players in the market are Thermo Fisher Scientific Inc., Merck KGaA, Sartorius AG, Danaher Corporation, Bio-Rad Laboratories Inc., Agilent Technologies Inc., PerkinElmer Inc., Charles River Laboratories International Inc., Lonza Group AG, SGS SA, Eurofins Scientific SE, QIAGEN N.V., and others.

Key drivers include rising biologics production, growth in vaccine manufacturing, and increasing regulatory focus on product safety.

Major demand comes from pharmaceutical companies, biotechnology firms, and CDMOs.

The market outlook remains strong due to adoption of advanced DNA detection technologies and expansion of biologics pipelines.

Download Sample Report of Residual DNA Testing Market

Please fill out the form to request a customized copy of the research report.