Printed Circuit Board Market Size, Share Global Analysis Report, 2026-2034

REPORT DETAILS

Printed Circuit Board Market Summary

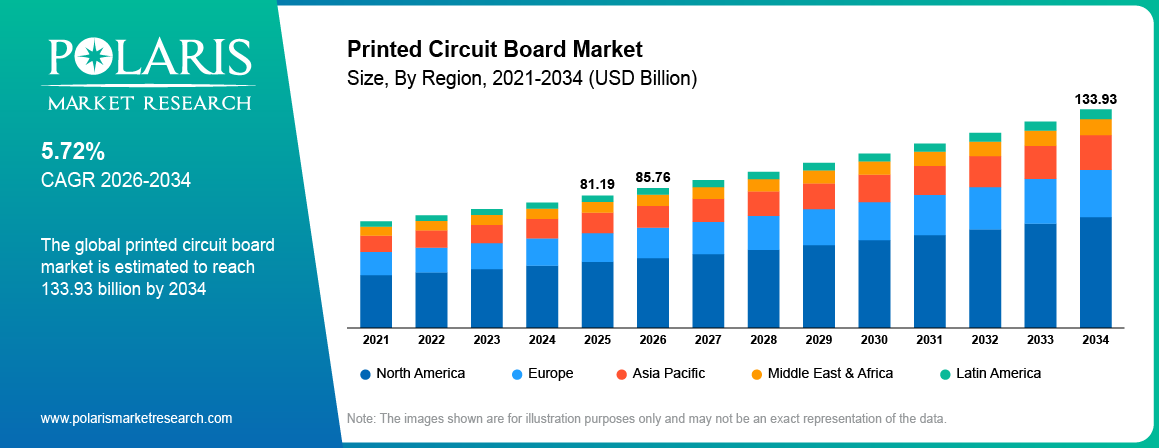

The global printed circuit board market is estimated to be around USD 81.19 billion in 2025,with consistent growth anticipated during 2026–2034. Growth is driven by rising demand for electronic devices and increasing adoption of advanced automotive and telecom systems. The market is projected to grow at a CAGR of 5.72% during the forecast period.

Market Statistics

Key Takeaways

- North America dominated revenue, accounting for approximately 38.70% market share due to strong demand for advanced electronics and data center infrastructure.

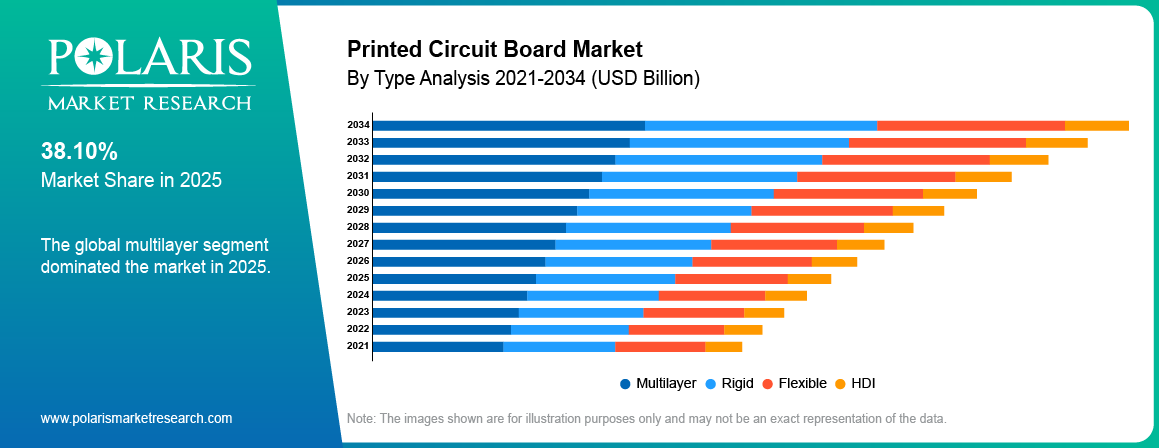

- Multilayered PCBs have a high adoption rate, holding approximately 36.45% market share due to compatibility with high-density circuits.

- Investment in HDI and flex PCBs is growing and is projected to register a CAGR of approximately 11.80% to enhance efficiency and miniaturization.

- Advanced materials are being researched by manufacturers, expected to grow at a CAGR of approximately 10.25% to improve efficiency in heat and electricity.

- Growing requirements for electric vehicles are driving PCB demand, projected to register a CAGR of approximately 12.60% for strong and efficient designs.

- Expansion of 5G infrastructure is creating demand for high-frequency PCBs, expected to witness a CAGR of approximately 13.40%.

Industry Dynamics

- Growth in consumer electronics is increasing demand for printed circuit boards.

- Increasing usage of electric vehicles is creating a need for efficient PCB solutions.

- The high cost of raw materials is affecting manufacturing and pricing.

- Integration of high-speed and high-frequency technologies is improving PCB performance.

What is the Printed Circuit Board Market?

A printed circuit board (PCB) refers to a foundational electronic component that mechanically supports and electrically connects electronic components using conductive pathways etched on a substrate. The main function of PCBs is to facilitate the transmission of signals and electricity, as well as integration of various components. Various products require the use of printed circuit boards including consumer products, automotive parts, industrial equipment, and telecommunication systems. The increase in production of electronic products has increased demand for efficient PCB solutions.

There exist various types of PCB technology according to the number of layers, materials used, and requirements for specific applications. There are single-sided and double-sided PCBs that facilitate basic circuits; there is also multilayered technology for more complicated and dense PCB design. Modern PCBs provide better heat dissipation and signal integrity, allowing for improved performance in high speed and frequency operations.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Rising demand for miniaturized and high-speed electronic devices is supporting PCB adoption across industries. Companies are investing in advanced manufacturing processes to improve precision and production efficiency. Increasing use of electric vehicles, 5G infrastructure, and IoT devices is strengthening demand for multilayer and high-density interconnect PCBs. These factors support growth in the global printed circuit board market.

Drivers & Opportunities

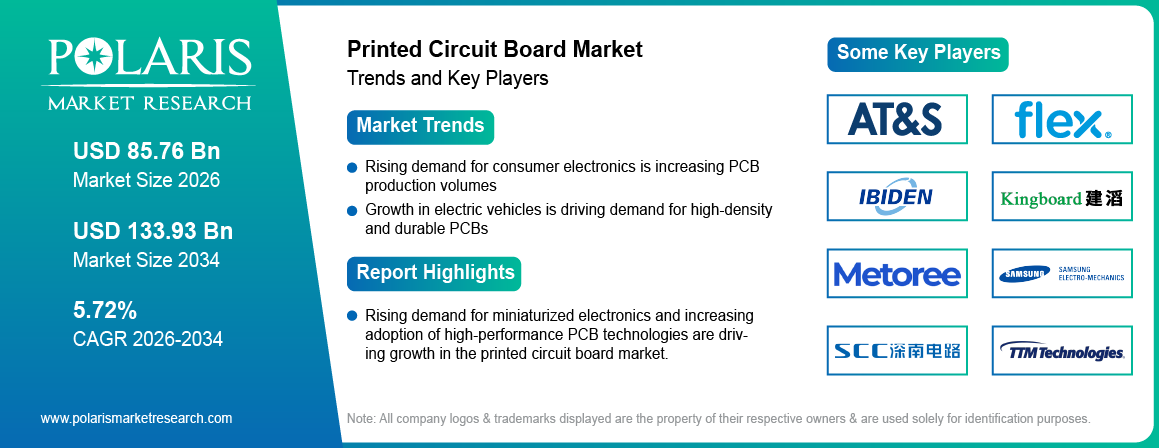

Rising demand for consumer electronics is increasing PCB production volumes: Rising production of smartphones, laptops, and home electronics is increasing demand for printed circuit boards. PCB production volumes are increasing to meet the demands of large-scale device manufacturing. In line with this development, the Government of India's Ministry of Electronics & Information Technology has sanctioned projects worth USD 4.64 billion under the Electronics Component Manufacturing Scheme to promote indigenous manufacturing and reduce dependency on imports.This development is helping boost capacity growth in the value chain of PCB manufacturing globally.

Growth in electric vehicles is driving demand for high-density and durable PCBs: As more electric cars are manufactured, there is a rising need for PCBs that can operate under harsh conditions, such as varying temperature levels and physical shock. The automotive sector needs PCBs with high durability and temperature tolerance. According to data from the International Energy Agency, sales of electric cars have surpassed 17 million units in 2024, accounting for more than 20% of global car sales.

Restraints & Challenges

Volatility in raw material prices is increasing PCB manufacturing costs: The variable prices of copper, laminates, and other special materials are contributing to the rise in the cost of production for PCB manufacturers. Variability in the cost of production is affecting the prices and profitability levels. This is creating difficulties in entering into long-term deals.

Opportunity

Growth in wearable electronics is supporting flexible PCB adoption: The increased use of wearable technology, fitness bands, and smart health devices is resulting in the growing acceptance of flexible PCBs. Such equipment needs lightweight and compact circuits. In October 2024, Murata have developed stretchable printed circuit technology that is capable of providing higher flexibility and reliability, allowing the development of advanced wearable medical equipment. Such trends are helping the growth and development of flexible and rigid-flexible PCBs.

Source: Polaris Market Research Analysis

Technology Trends & PCB Manufacturing Insights

Advanced PCB Technologies (HDI, Flexible, Rigid-Flex)

High-density interconnect printed circuit boards facilitate the creation of small-sized devices as well as enable fast signal transmission. The HDI printed circuit boards make use of microvias and fine traces to enhance the circuitry density. Flexible printed circuit boards allow for flexibility and efficient space utilization within small-sized equipment. Rigid-flex printed circuit boards are designed with stiffness and flexibility.

Comparison: HDI vs Multilayer PCB

| Parameter | HDI PCB | Traditional Multilayer PCB |

| Circuit Density | High | Moderate |

| Size | Compact | Larger |

| Cost | High | Moderate |

| Performance | High-speed | Standard |

| Application | Smartphones, EVs | Industrial, basic electronics |

Source: Polaris Market Research Analysis

PCB Materials & Substrates (FR-4, PTFE, Polyimide, Metal Core)

The material of the PCB influences its performance, longevity, and price. The most common material is FR-4, which has moderate performance at a low cost. PTFE is used for high-frequency operations, including 5G communication systems. Polyimide can withstand high temperatures in flexible printed circuit boards. Metal core PCBs ensure efficient thermal dissipation in power electronics. Material selection depends on the application and operating environment.

PCB Manufacturing Process & Automation Trends

The manufacturing process of a PCB involves designing, etching, drilling, plating, and assembly. SMT is commonly used in the assembly process. There have been advancements in automation, which increase production speed and reduce errors. Manufacturers are upgrading their machinery to meet high standards. Inspection using digital and artificial intelligence methods enhances efficiency.

Comparison: Rigid vs Flexible PCB

| Parameter | HDI PCB | Traditional Multilayer PCB |

| Structure | Solid | Bendable |

| Durability | High | Moderate |

| Space Efficiency | Low | High |

| Cost | Low | High |

| Application | Industrial systems | Wearables, medical devices |

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the printed circuit board market by type, substrate, and application to help readers identify the fastest expanding and most attractive demand segments.

By Type

-

Multilayer

Multilayer segment dominated the market in 2025, driven by rising demand for high-density and compact circuit designs across advanced electronic devices. For instance, in February 2026, Technotech has launched a high-precision multilayer PCB production facility in Russia to strengthen domestic advanced electronics manufacturing capabilities.Growing incorporation of advanced components in smartphones, automobiles, and telecommunications devices drives the segment’s demand.

-

HDI

The HDI segment is projected to grow at the fastest CAGR during the forecast period due to increasing demand for miniaturized and high-performance electronic products. HDI technology enables greater circuit density and superior signal performance. The growing usage of 5G products and electric vehicles will drive the growth of this segment.

By Substrate

-

FR-4

The FR-4 segment led the market in 2025, backed by its cost-effectiveness and broad applicability to typical electronic uses. The choice of FR-4 is favored due to its reliability and simple manufacturing process. High usage of consumer electronics and industrial machinery products is driving segment growth.

-

High-Speed Materials

The high-speed materials segment is projected to grow at the fastest CAGR during the forecast period due to increasing demand for high-frequency and high-speed data transmission. These materials support improved signal integrity in telecom and data center applications. Expansion of 5G infrastructure is driving segment adoption.

By Application

-

Consumer Electronics

The consumer electronics segment led the market in 2025, backed by growing manufacturing of smartphones, laptops, and other smart devices. Growing demand for small and efficient electronics is fueling PCB adoption. Continuous product innovation is strengthening segment demand.

-

Automotive

The automotive segment is projected to grow at the fastest CAGR during the forecast period due to increasing adoption of electric vehicles and advanced driver assistance systems. Vehicles require high-reliability PCBs for power control and connectivity systems. Growth in automotive electronics is accelerating segment expansion.

Source: Polaris Market Research Analysis

Regional Analysis

North America Market Assessment

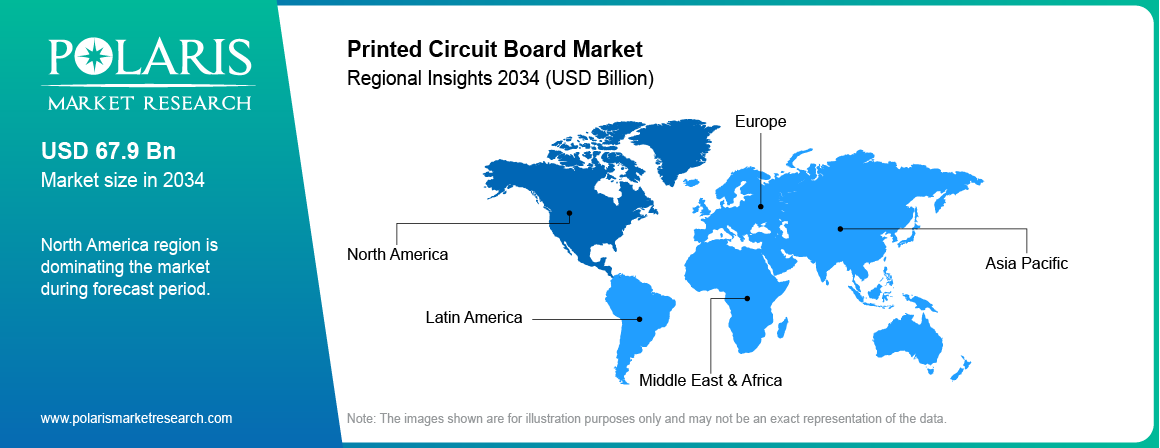

North America printed circuit board market dominated in 2025, due to strong demand for advanced electronics and automotive technologies. The US is contributing to the rising demand for high-performing PCBs that are used in data centers and EVs. The investments made in semiconductors and electronics manufacturing are expected to contribute to regional market growth. As per Semiconductor Industry Association (SIA), the US semiconductor investments have exceeded USD 540 billion in announced projects, driven by the CHIPS Act to expand domestic manufacturing and strengthen supply chain resilience.

Asia Pacific Printed Circuit Board Market Insights

Asia Pacific printed circuit board market is projected to grow at the fastest CAGR during the forecast period, driven by large-scale electronics manufacturing in China, Japan, South Korea, and Taiwan. The region benefits from strong supply chain networks and cost-efficient production. In January 2026, the Thai government has approved a USD 2 billion capital expenditure for Taiwanese firm ZDT to improve manufacturing efficiency, thus strengthening the presence of Southeast Asia as a producer of high-end PCBs.Furthermore, the growing demand for consumer electronics and telecom infrastructure is facilitating the growth of the market.

Europe Printed Circuit Board Market Overview

Europe printed circuit board market held the second-largest share, owing to increasing adoption of automotive electronics and industrial automation systems. Germany, France, and the UK are concentrating their efforts on electric mobility and smart manufacturing. The rising demand for quality PCBs is promoting regional market growth. For example, in August 2025, Polymatech has established a state-of-the-art PCB manufacturing plant in Europe to manufacture high-quality HDI PCBs for telecom, aerospace, and semiconductor applications.

Middle East & Africa Emerging Markets

The Middle East & Africa PCB market size is steadily rising owing to the increased construction of digital infrastructure and industrialization. In November 2025, Microsoft & G42 made an announcement about the expansion of the UAE data center power by 200 MW as part of their USD 15.2 billion investments to improve AI and cloud infrastructure, which will be operational by 2026.This is expected to boost the usage of advanced PCBs used in servers and data center equipment. Moreover, the increase in investments in telecommunication and smart city applications is also helping drive the growth of the market.

Source: Polaris Market Research Analysis

Competitive Landscape & Future Outlook

The printed circuit board market exhibits moderate fragmentation, with both multinational producers, regional producers, and specialty PCB producers involved in serving various application markets. The competition among the rivals will focus around factors like quality of products, precision, and advanced technologies. Market players are concentrating their efforts on cutting-edge PCB technologies, new materials, and manufacturing automation to enhance their competitive positions within the market.

Some of the notable players in the market include Zhen Ding Technology Holding Limited, Unimicron Technology Corporation, Nippon Mektron Ltd., TTM Technologies, Inc., AT&S Austria Technologie & Systemtechnik AG, Samsung Electro-Mechanics, Ibiden Co., Ltd., Shennan Circuits Company Limited, Compeq Manufacturing Co., Ltd., Tripod Technology Corporation, Kingboard Holdings Limited, Flex Ltd., and others.

Premium Insights & Analyst View

Strategic Developments

The PCB market shows moderate fragmentation, and competition is driven by cost, scale, and technology. Firms have been increasing production capacity and developing PCB technologies. Partnerships with automotive and electronics firms are strengthening supply chains. M&A activity is supporting technology access and portfolio expansion.

Future Outlook

The rise of AI and electric cars is boosting the demand for high-performing PCBs. PCB makers are concentrating on developing multilayered and high-density PCBs to accommodate advanced applications. The trend towards sustainability is fueling the use of environmentally friendly PCBs. Automation is improving production efficiency and quality.

Top Key Players

- AT&S Austria Technologie & Systemtechnik AG

- Compeq Manufacturing Co., Ltd.

- Flex Ltd.

- Ibiden Co., Ltd.

- Kingboard Holdings Limited

- Nippon Mektron Ltd.

- Samsung Electro-Mechanics

- Shennan Circuits Company Limited

- Tripod Technology Corporation

- TTM Technologies, Inc.

- Unimicron Technology Corporation

- Zhen Ding Technology Holding Limited

Industry Developments

- April 2026: TLB announced to raise USD 80.9 million through a rights issue to build a new plant in Vietnam and double its PCB production capacity to meet growing demand from AI and data center applications. [source: thelec.net]

- March 2026: Panasonic announced to invest USD 47.11 million to add a new MEGTRON circuit board material production line in China to support rising demand from AI servers and ICT infrastructure. [source: panasonic.com]

Printed Circuit Board Market Segmentation

By Type Outlook (Revenue, USD Billion, 2021-2034)

- Rigid

- Flexible

- HDI

- Multilayer

By Substrate Outlook (Revenue, USD Billion, 2021-2034)

- FR-4

- Polyimide

- Metal Core

- High-Speed Materials

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Consumer Electronics

- Automotive

- Telecom

- Healthcare

- Industrial

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Printed Circuit Board Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 81.19 Billion |

| Market Size in 2026 | USD 85.76 Billion |

| Revenue Forecast by 2034 | USD 133.93 Billion |

| CAGR | 5.72% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Printed Circuit Board Market FAQ's

The global market size was valued at USD 81.19 Billion in 2025 and is projected to grow to USD 133.93 Billion by 2034.

North America dominates the market due to strong demand for advanced electronics, data centers, and automotive technologies.

Major applications include consumer electronics, automotive systems, telecom infrastructure, healthcare devices, and industrial equipment.

A few of the key players in the market are Zhen Ding Technology Holding Limited, Unimicron Technology Corporation, Nippon Mektron Ltd., TTM Technologies, Inc., AT&S Austria Technologie & Systemtechnik AG, Samsung Electro-Mechanics, Ibiden Co., Ltd., Shennan Circuits Company Limited, Compeq Manufacturing Co., Ltd., Tripod Technology Corporation, Kingboard Holdings Limited, Flex Ltd., and others.

Key drivers include rising demand for electronic devices, growth in electric vehicles, and expansion of 5G infrastructure.

Major demand comes from consumer electronics, automotive, telecom, healthcare, and industrial sectors.

The market outlook remains strong due to growth in AI hardware, electric vehicles, and high-speed communication technologies.

Download Sample Report of Printed Circuit Board Market

Please fill out the form to request a customized copy of the research report.