Software Defined Security Market Size, Share, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Software Defined Security Market Summary

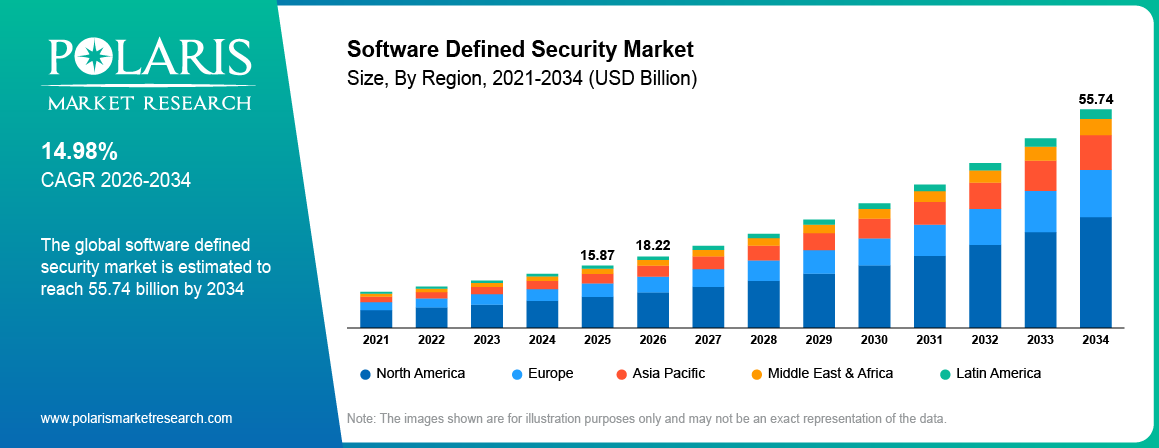

The global software defined security market is estimated around USD 15.87 Billion in 2025,?with consistent growth anticipated during 2026–2034. Expansion is driven by increasing adoption of cloud computing, rising cybersecurity threats, and growing implementation of zero trust architectures. The market is projected to grow at a CAGR of 14.98% during the forecast period.

Market Statistics

Key Takeaways

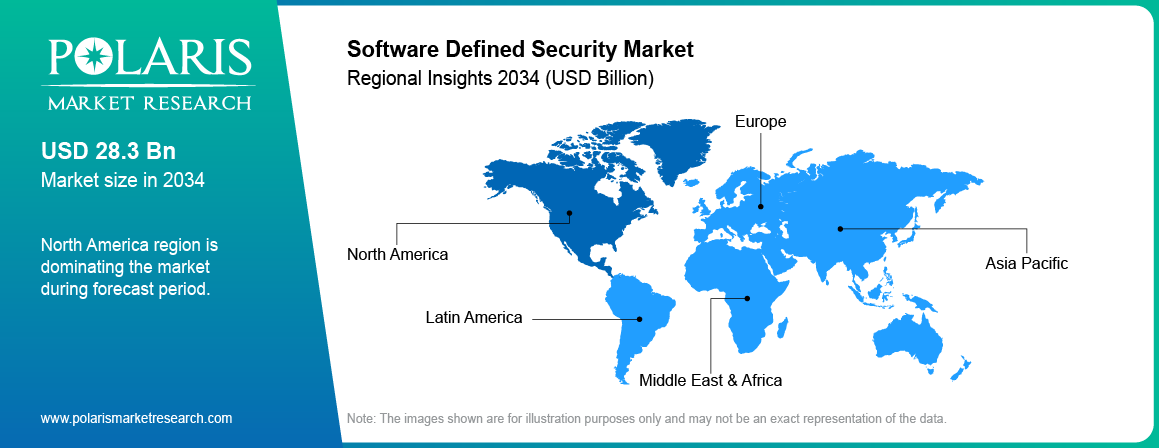

- North America dominated the market, accounting for approximately 38.90% market share, supported by advanced IT infrastructure and strong cybersecurity regulations.

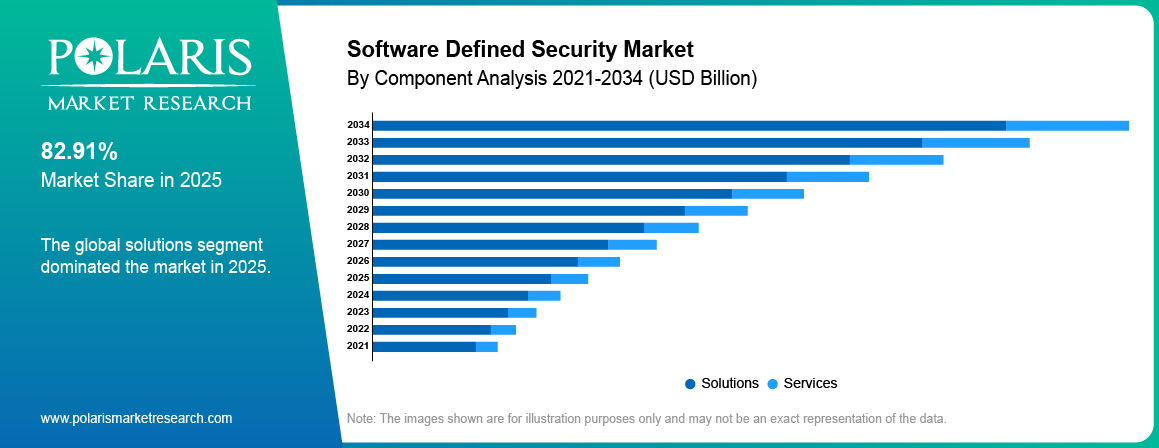

- SDS solutions gained strong traction, accounting for approximately 32.45% market share due to their ability to deliver centralized and policy-driven security across distributed environments.

- Software defined security remains widely used, holding approximately 35.20% market share due to its scalability, automation, and compatibility with cloud-native architectures.

- BFSI dominates demand, contributing approximately 28.75% market share supported by the need for advanced data protection and regulatory compliance.

- Cloud-based deployment remains the largest segment, accounting for approximately 41.60% market share due to rapid migration of workloads to cloud environments.

- Hybrid deployment is witnessing rapid growth and is projected to register a CAGR of approximately 14.85% driven by the need to secure both legacy and cloud infrastructure.

Industry Dynamics

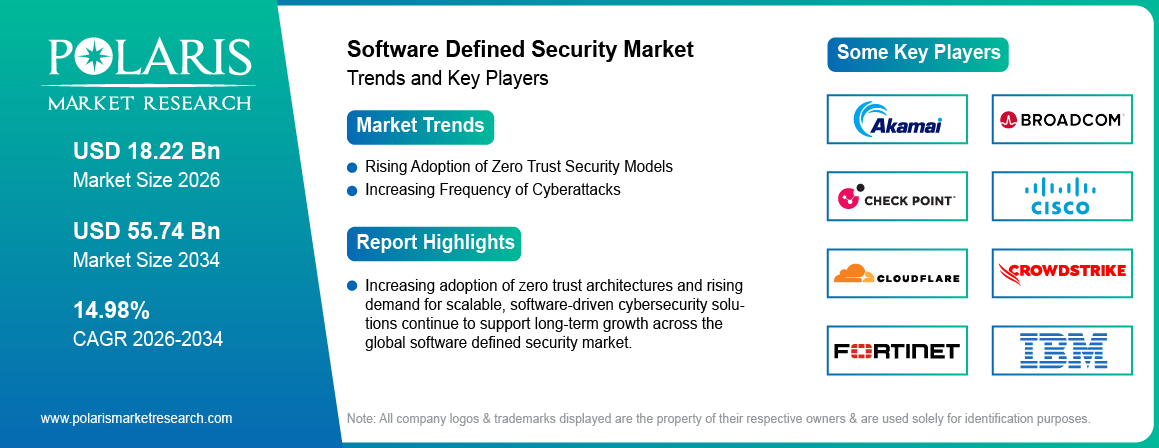

- Rising adoption of zero trust security models is increasing demand for identity-based and policy-driven security frameworks.

- Increasing frequency and sophistication of cyberattacks is strengthening demand for automated and real-time threat detection systems.

- Lack of trained cybersecurity experts and difficulty in integration are some of the barriers hindering market growth.

- Increasing use of AI, edge computing, and 5G networks is expected to create new avenues for SDS.

What is the Software Defined Security Market?

Software-defined security refers to the cybersecurity segment that deals with cybersecurity solutions which are software-driven and based on policies independent of hardware. Software defined security meaning includes a software-defined approach to managing access controls, firewalling, and segmentations. Software defined security architecture entails implementation with network virtualization security. Software defined security market examples include software-defined perimeter (SDP), micro-segmentation, and native cloud security solutions.

The difference between SDS and conventional security is based on static hardware-driven controls, while SDS provides adaptive security. The difference between SDS and SASE/SSE is that SDS functions as an underlying architecture, while SASE/SSE provides the service itself. Zero trust vs SDS implies that SDS provides enforcement and segmentation, while zero trust represents an access model. Software-defined perimeter SDP runs inside SDS, providing identity-driven access control and smaller attack surfaces.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The market for software-defined security is booming fueled by cloud migration, workloads distribution, and changing cyber-attacks. Rising trend towards adopting DevSecOps, necessitates implementing security in software-defined infrastructures. Remote working and hybrid IT models have intensified this requirement further propelling the market growth.

Drivers & Opportunities

Growth of Zero Trust Security Frameworks: Distributed information technology (IT) structures and telecommuting are eroding conventional network boundaries. These trends are leading to an surge in the deployment of software-defined security (SDS) to govern identity-driven access and verification. Zero Trust framework needs a central management system for policy enforcement and dynamic authorization, and the SDS model supports such capabilities in both cloud and hybrid ecosystems. As per the International Journal of Engineering Research & Technology, 67% of the organizations adopted Zero Trust by 2024.This growing trend is pushing enterprises towards implementing SDS technologies based on scalability and policy-based security.

Increasing Number and Complexity of Cyberattacks: The rise in attacks like phishing, ransomware, and cyber frauds are increasing vulnerabilities in static cybersecurity architectures. Businesses are increasingly adopting automated and AI-based systems to tackle cybersecurity issues in real-time. According to the Global Cybersecurity Outlook 2026, roughly 77% of respondents experienced an increase in cyber fraud.This environment is driving the adoption of SDS, which uses analytics and automation capabilities.

Restraints & Challenges

Integration Complexity and Skills Shortage: SDS deployment requires integration with legacy infrastructure, which creates compatibility issues and increases implementation timelines. Security architecture design and migration of tasks increases risk during operation. Shortage of cybersecurity experts adds to that risk. In such cases, adoption becomes difficult, particularly in businesses where modernization of the existing structure is necessary.

Opportunity

AI, Edge Computing, and 5G Security Expansion: The proliferation of edge computing devices, Internet of Things infrastructure, and 5G services is creating new attack vectors, necessitating the development of dynamic and flexible security frameworks. AI and ML-powered SDS solutions enable proactive security approaches through threat identification and mitigation in a highly dispersed and dynamic environment.

Technology and Architecture Analysis

-

SDS Architecture: Control Plane vs Data Plane

In software-defined security architecture, the control plane takes care of visibility and policy formulation. This plane is responsible for making security decisions while the data plane, applies these decisions to protect the network.

Software-defined security allows for policy-based security, which means that the security decisions are dynamically formulated and distributed.

-

Role of Micro segmentation, SDP & Policy Engines

Micro segmentation offers a way to isolate workloads and limit lateral movements by threats. The software-defined perimeter (SDP) implements access control based on identities, in line with the zero-trust concept.

The policy engine serves as the central authority for making decisions based on context and enforces policies using API-based security.

-

Integration with Cloud, Containers & DevSecOps

Cloud-native security SDS works with cloud infrastructure, container technologies, and DevSecOps approaches. It ensures security as part of the application deployment process by leveraging API orchestration. NFV security uses SDS to implement network security services in a virtualized environment.

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the software defined security market by component, deployment, and end-use industry to help readers identify the fastest expanding and most attractive demand segments.

By Component

-

Solutions

Solutions held the largest share in the Software Defined Security (SDS) market as enterprises prioritize centralized, policy-driven security platforms. SDS solutions versus services comparison illustrates that companies implement SDS solutions as an approach to provide micro-segmentation, identity access control, and threat enforcement in real time.

-

Services

Services represent the fastest-growing category propelled by growing complexities associated with SDS deployment and management. Companies use consulting, integration, and managed services to design a zero-trust architecture and optimize policies in a hybrid environment.

By Deployment

-

Cloud-based

Cloud-based SDS held largest share in the market as more businesses adopt cloud services for their operations. Cloud-based SDS provided the ability to implement scalable and API-based enforcement of security policies on multiple clouds.

-

Hybrid

Hybrid model of SDS deployment projected to grow at a rapid pace due to increasing demand for security of legacy on-premise solutions and cloud solutions. Enterprises embrace hybrid models to retain control of their sensitive information while using SDSs.

By End-Use Industry

-

BFSI

BFSI was the major contributor of the SDS market owing to the need for sophisticated security measures in financial institutions. The application of SDS technology in BFSI provides benefits such as micro-segmentation of the network, fraud detection, and compliance-driven security.

-

Telecom

Telecommunications projected to grow rapidly during the forecast period, fueled by rapid rise of network virtualization and 5G. SDS telecom security helps secure network slicing and edge computing environments. As per International Energy Agency, 5G’s share of mobile data traffic is projected to rise to nearly 70% by 2028, up from around 17% in 2022.This increase in data volume is expected to further escalate the need for software-defined, automatic security systems within telecommunication networks.

Source: Polaris Market Research Analysis

Regional Analysis

North America Software Defined Security Market Assessment

North America software defined security market accounted for the largest share in 2025 due to high concentration of technology firms, advanced IT infrastructure, and stringent cybersecurity measures. Companies in the region rely on software-defined security to protect complex, cloud-driven infrastructure. The new cybersecurity laws in the US that came into effect in 2026 require 72-hour reporting under the CIRCIA framework, adherence to the NIST CSF 2.0 framework, and higher CMMC requirements for military contractors.These frameworks are accelerating SDS adoption US and strengthening the North America cybersecurity market.

Europe Software Defined Security Market Overview

Europe was the second largest market in software defined security driven by strict data protection laws such as GDPR and NIS2. SDS technology is used by firms to help ensure compliance, data protection, and security within their digital operations. The adoption of cybersecurity SDS in Europe has been growing among enterprises that deal with cross-border data management and cloud computing. Regulatory forces have compelled firms to embrace software-based security architectures.

Asia Pacific Software Defined Security Market Insight

Asia Pacific SDS market is projected to grow at a rapid pace during the forecast period, due to rapid digital transformation and rising cybersecurity investments across China, India, and Japan. Enterprises are adopting SDS solutions to secure expanding cloud infrastructure and digital services. According to the International Trade Administration, the India SDS market is experiencing robust growth. The market is expected to grow from USD 5.6 billion in 2025 to USD 12.9 billion in 2030 at a CAGR of 18.3%.SDS implementation in China is witnessing growth due to focus of the government on cybersecurity infrastructures. Increasing digital economy and cybersecurity threats are fueling the growth of the SDS market in the APAC region.

Source: Polaris Market Research Analysis

Competitive Landscape & Pricing Analysis

Key Players & Strategic Developments

The competitive landscape of the software defined security market reflects strong participation from established cybersecurity vendors and cloud-native security providers delivering policy-driven, scalable protection frameworks. Key competitors in the software-defined security market include zero trust, SASE, and artificial intelligence-based threat detection in securing enterprise environments.

Key players operating in the software defined security market include Akamai Technologies, Inc., Broadcom Inc., Check Point Software Technologies Ltd., Cisco Systems, Inc., Cloudflare, Inc., CrowdStrike Holdings, Inc., Fortinet, Inc., IBM Corporation, Illumio, Inc., Juniper Networks, Inc., Palo Alto Networks, Inc., Proofpoint, Inc., Trend Micro Incorporated, VMware, Inc. (Broadcom), and Zscaler, Inc.

Future Outlook & Premium Insights

-

Future of SDS Market (2026–2034)

The future of software defined security reflects strong expansion driven by cloud adoption, zero-trust frameworks, and increasing network complexity. Market prediction in the SDS industry reveals a growing need for scalable security management that is driven by policy-based security measures that accommodate hybrid and multi-cloud platforms.

Policy as code is evolving as a vital trend that allows businesses to develop, manage, and implement security policies in software development workflows, thus increasing deployment consistency and speed.

-

Role of AI, Automation & Predictive Security

Artificial intelligence in SDS is driving the emergence of automated security measures. AI models in machine learning cybersecurity SDS use network behavior analysis, anomaly detection, and response automation.

Predictive security analytics predicts security attacks using artificial intelligence algorithms. This reduces response time and strengthens resilience, particularly in dynamic cloud-native environments.

-

Emerging Trends (Edge, 5G, Quantum Security)

SDS is expanding into edge computing and 5G networks, where distributed architectures require lightweight, scalable security enforcement. Real-time, policy enforcement on the edge is becoming increasingly important for applications that require low latencies.

The shift in emphasis towards quantum-resistant encryption and advanced cryptography techniques is projected to significantly impact future SDS systems. As threat environments change, future SDS platforms need to incorporate sophisticated automation, decentralization, and flexible policy mechanisms.

Key Players

- Akamai Technologies, Inc.

- Broadcom Inc.

- Check Point Software Technologies Ltd.

- Cisco Systems, Inc.

- Cloudflare, Inc.

- CrowdStrike Holdings, Inc.

- Fortinet, Inc.

- IBM Corporation

- Illumio, Inc.

- Juniper Networks, Inc.

- Palo Alto Networks, Inc.

- Proofpoint, Inc.

- Trend Micro Incorporated

- VMware, Inc. (Broadcom)

- Zscaler, Inc.

Industry Developments

- May 2025: Network Innovations announced the launch of Argus, a Software Defined Security Platform intended to integrate satellite, wireless, and land-based networks through a central management system. [Source: blog.networkinnovations.com]

- April 2025: Darktrace announced an enhancement of its NDR product line that is intended to provide protection for modern enterprise infrastructures such as remote or hybrid workforces. This platform leverages self-learning technology and behavior analysis in detecting and automating threat responses. [Source: www.darktrace.com]

Software Defined Security Market Segmentation

By Component Outlook (Revenue, USD Billion, 2021-2034)

- Solutions

- Services

By Deployment Outlook (Revenue, USD Billion, 2021-2034)

- Cloud

- On-Premise

- Hybrid

By End-Use Industry Outlook (Revenue, USD Billion, 2021-2034)

- BFSI

- Healthcare

- Telecom

- Government

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Software Defined Security Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 15.87 Billion |

| Market Size in 2026 | USD 18.22 Billion |

| Revenue Forecast by 2034 | USD 55.74 Billion |

| CAGR | 14.98%from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Software Defined Security Market FAQ's

The global market size was valued at USD 15.87Billion in 2025 and is projected to grow to USD 55.74 Billion by 2034.

North America dominated the market due to strong cybersecurity frameworks, advanced IT infrastructure, and early adoption of cloud technologies.

BFSI and telecom sectors account for the largest share due to high security requirements and digital infrastructure expansion.

A few of the key players in the market are Akamai Technologies, Inc., Broadcom Inc., Check Point Software Technologies Ltd., Cisco Systems, Inc., Cloudflare, Inc., CrowdStrike Holdings, Inc., Fortinet, Inc., IBM Corporation, Illumio, Inc., Juniper Networks, Inc., Palo Alto Networks, Inc., Proofpoint, Inc., Trend Micro Incorporated, VMware, Inc. (Broadcom), and Zscaler, Inc.

Growth is driven by cloud adoption, rising cyber threats, and increasing demand for scalable security solutions.

Trends include zero trust adoption, AI-driven security, edge protection, and integration with DevSecOps.

SDS provides centralized control, scalability, automation, and real-time threat response.

Challenges include integration complexity, high implementation costs, and shortage of skilled professionals.

BFSI, telecom, healthcare, and IT sectors are major adopters of SDS solutions.

Download Sample Report of Software Defined Security Market

Please fill out the form to request a customized copy of the research report.