Edge Computing Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

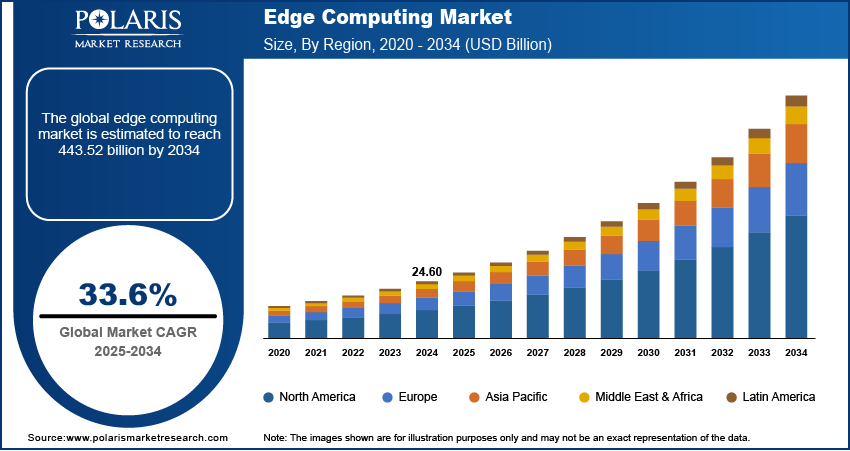

Edge Computing Market Summary

The global edge computing market was valued at USD 32.75 billion in 2025 and is expected to grow at a CAGR of 33.6% during the forecast period. The growing demand for the edge computing market is driven by the rising adoption of smart devices and industrial IoT, increasing expenditure for autonomous vehicles, and growing demand for deployment of a 5G network.

Market Statistics

Key Takeaways

- North America dominated the market with the largest share of 35% in 2025 due to the high adoption of IoT and smart devices, as well as an advanced 5G infrastructure.

- Asia Pacific is projected to account for a significant growth rate of 17.99% CAGR in the global market due to rapid digitalization, the rollout of 5G networks, and a rising number of IoT devices.

- The U.S. dominated the North American regional market with an 87% revenue share in 2025. The availability of robust digital infrastructure and the rising adoption of next-generation technologies contributed to the region's dominance.

- The large enterprises segment is expected to witness significant growth at a CAGR of 33.6% during the forecast period due to the increased demand for data security and growing cloud-based data traffic.

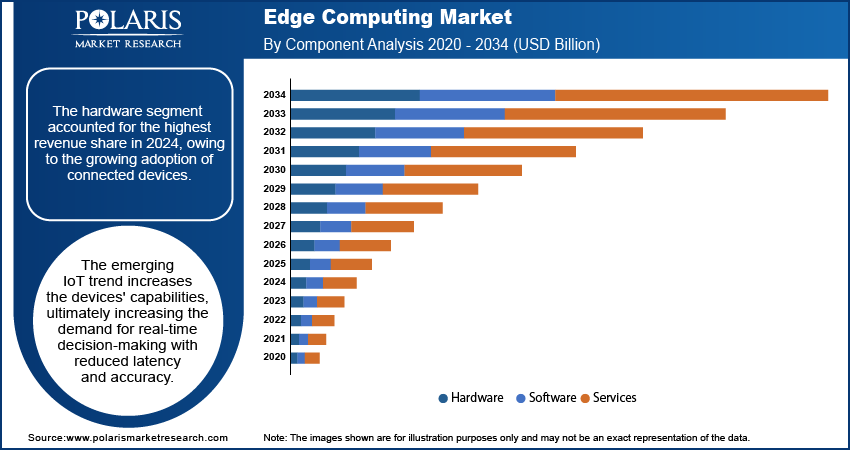

- The hardware segment accounted for the largest share in 2025 of 50%, driven by the growing adoption of connected devices and the need for high-performance edge processing units.

Industry Dynamics

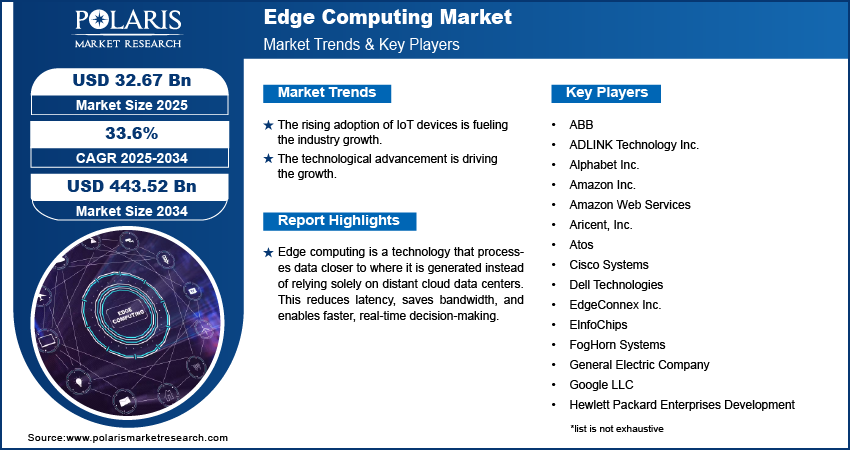

- The rising adoption of IoT devices is fueling the industry growth.

- The rising data volume in traditional data center infrastructure is boosting the industry growth.

- The technological advancement is driving the growth.

- High infrastructure cost and complexity of deployment across diverse and remote environments limits the growth.

Source: Polaris Market Research Analysis

Impact of AI on Industry

- Reduce latency, improve responsiveness, and support real-time applications.

- Improve privacy and data security by processing sensitive data locally

- Reduce bandwidth and cut the cost. It also reduces cloud storage and computation expenses.

Edge computing is a technology that processes data closer to where it is generated instead of relying solely on distant cloud data centers. This reduces latency, saves bandwidth, and enables faster, real-time decision-making. It is especially useful for applications like IoT, autonomous vehicles, smart cities, and industrial automation.

The rapid growth of connected devices is generating massive volumes of data, which traditional data center infrastructures often struggle to handle. Emerging technologies and the widespread adoption of computing devices across various industries are driving the generation of decentralized data. Processing data closer to its source, rather than relying solely on centralized data centers, reduces latency and inefficiencies. This shift is a key factor driving the demand for edge computing. Simultaneously, the rise of these massive data volumes is fueling growth in the Next-Generation Data Storage Market, as organizations seek advanced storage solutions that are faster, more scalable, and capable of supporting real-time data analytics and optimized system performance.

Edge vs Cloud vs Fog Computing – Comparison Table

| Parameter | Edge Computing | Cloud Computing | Fog Computing |

| Definition | Data processing occurs close to the data source (devices/sensors) | Centralized computing in large remote data centers | A distributed layer between edge and cloud for intermediate processing |

| Processing Location | On/near devices (e.g., sensors, gateways) | Centralized cloud data centers | Local network nodes between edge and cloud |

| Latency | Very low (real-time processing) | Higher due to data travel to distant servers | Low to moderate (optimized between edge and cloud) |

| Bandwidth Usage | Low (less data sent to cloud) | High (large data transfer to cloud) | Moderate (filters data before sending to cloud) |

| Scalability | Limited by local device capacity | Very high scalability | High, through distributed fog nodes |

| Best Suited For | Real-time applications (autonomous vehicles, IoT, smart factories) | Big data analytics, storage, enterprise applications | Large-scale IoT systems, smart cities, industrial networks |

| Infrastructure | Edge devices, local servers, gateways | Cloud platforms (AWS, Azure, Google Cloud) | Fog nodes, routers, edge gateways, local servers |

| Data Handling | Processes critical data locally | Stores and processes all data centrally | Filters, aggregates, and forwards relevant data |

| Security Approach | Data stays closer to sources. It enables reduced exposure | Centralized security controls | Multi-layer security across network nodes |

| Use Cases | Self-driving cars, AR/VR, smart cameras | Web hosting, enterprise SaaS, data lakes | Smart grids, connected healthcare systems, smart transportation |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Industry Dynamics

Growth Drivers

The global edge computing market is driven by the rising adoption of IoT devices, which creates a huge amount of data that needs to be processed and analyzed. In addition, organizations shifting from cloud computing and storage systems to edge computing owing to its better bandwidth and low latency for analysis is an essential factor fueling the market growth. Furthermore, edge computing brings computation closer to IoT devices. As a result, data is more secure, and network latency is decreased due to a reduction in the distance for data transfer. This enables edge computing to optimize IoT applications requiring real-time responses, supporting market growth.

For instance, Klika Tech partnered with the tinyML foundation to solve real business issues by integrating machine learning models, software, and hardware. Moreover, the partnership is based on empowering tinyML to expand its business using resource-limited devices to become better, smarter, and more responsive, which is projected to propel the market growth.

Edge Computing Market – Key Trends

| Trend | Description | Market Impact | Applications |

| Edge AI Adoption | Integration of AI models directly into edge devices for real-time analytics and decision-making | Reduces latency, enables autonomous systems, and increases efficiency of real-time operations | Autonomous vehicles, predictive maintenance, smart surveillance |

| IoT-Driven Edge Expansion | Growing use of IoT devices is generating massive data processed at the edge | Reduces cloud dependency, improves data handling efficiency | Smart homes, industrial IoT, wearable health devices |

| 5G-Enabled Edge Computing | Deployment of 5G networks supporting ultra-low latency edge processing | Enhances connectivity, enables high-speed real-time applications | AR/VR, smart cities, remote healthcare, autonomous mobility |

| Distributed Edge Architecture | Shift toward decentralized computing models across multiple edge nodes | Improves scalability, reliability, and fault tolerance | Content delivery networks, smart grids, enterprise IT systems |

Source: Polaris Market Research Analysis

Report Segmentation

The market is primarily segmented based on component, application, organization size, verticals, and region.

| By Component | By Application | By Organization Size | By Verticals | By Region |

|

|

|

|

|

Source: Polaris Market Research Analysis

Hardware segment accounted for the largest share in 2025

The hardware segment accounted for the highest revenue share in 2025, owing to the growing adoption of connected devices. The emerging IoT trend increases the devices' capabilities, ultimately increasing the demand for real-time decision-making with reduced latency and accuracy. Additionally, with the increasing volume of data, hardware is deployed to relieve the burdens from data and cloud centers, which is anticipated to support segment growth. Furthermore, businesses are opting for hardware that is robust, compact, has enough storage capacity, offers a variety of connectivity choices to operate over a wide power range, and also meets the requirement for which it is used. This hardware is mostly used in situations where it must perform reliably and optimally, increasing its demand in the military and defense sector; such factors influence segment growth.

Source: Polaris Market Research Analysis

Large enterprises are expected to witness faster growth

The demand for edge computing in large enterprises is expected to surge significantly over the forecast period due to the increased demand for data security and growing cloud-based data traffic. Many large enterprises are adopting advanced technologies such as artificial intelligence and machine learning to improve the overall productivity of their firms. Additionally, these firms generate a large amount of raw data which needs to be processed and analyzed, which increases the demand for edge computing. Moreover, many end-use industries are deploying edge computing as it enables data retrieval more quickly as keeps data near the devices that are using it, which guarantees real-time data utilization. Also, large enterprises create a lot of data that needs to be confidential and free from threat; edge computing improves the privacy and security of the generated data, which drives segment growth.

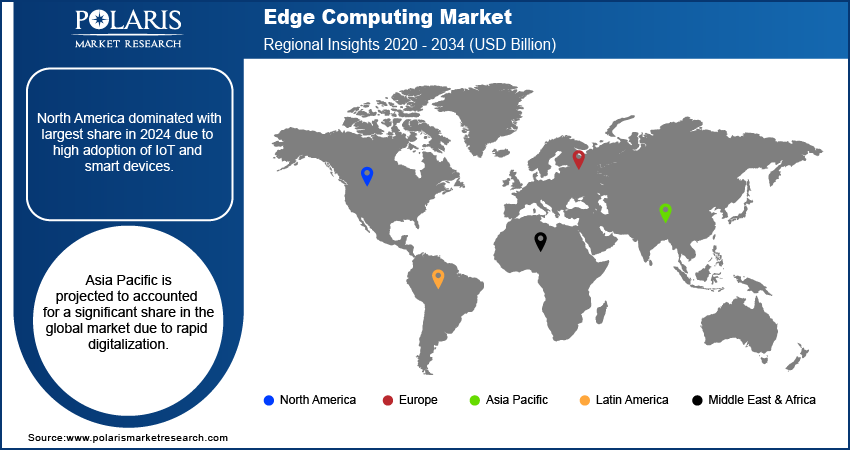

Regional Insights

North America dominated with largest share in 2025

The North America dominated with largest share in 2024 due to presence of mature cloud infrastructure and high internet penetration. Both urban as well as rural areas in the region has strong access to internet. This strong access to internet increases the number of connected devices and data generation which fuels the need for edge computing to process data locally and reduce latency. Moreover, the governments in the region are increasingly investing in the smart city infrastructure, which further fuels the demand for the edge computing. Edge computing enables real time data processing from cameras, sensors, and IoT devices which are used in traffic management, thereby driving the growth in the North America.

Asia Pacific is expected to witness the fastest growth over the forecast period

Asia Pacific is expected to witness faster growth over the forecast period owing to the rapid digitalization, innovation in technologies, and expansion of connected devices across developing nations such as China, India, Japan, and South Korea. In addition, the presence of major telecom players and increasing IT investments to deploy edge computing support regional growth. Furthermore, rising government funding to empower digitization and the increasing need for many businesses to store and process data contribute to market growth. Moreover, emerging IoT applications across smart cities create huge amounts of data. The increasing demand for processing and analyzing data at a comparatively low cost compared to cloud computing to produce information and enhance real-time decision-making near the data source drives segment growth.

Source: Polaris Market Research Analysis

Some of the major players operating in the global market include:

- ABB

- ADLINK Technology Inc.

- Alphabet Inc.

- Amazon Inc.

- Amazon Web Services

- Aricent, Inc.

- Atos

- Cisco Systems

- Dell Technologies

- EdgeConnex Inc

- ElnfoChips

- FogHorn Systems

- General Electric Company

- Google LLC

- Hewlett Packard Enterprises Development

- Honeywell International Inc.

- Huawei Technologies Co. Ltd

- IBM Corporation

- Intel Corporation

- Juniper Networks

- Microsoft Corporation

- Rockwell Automation, Inc

- Saguna Networks

- SAP SE

- Schneider Electric SE

- Siemens AG

Recent Developments

In June 2025: VAST Data and Cisco expanded their collaboration by integrating VAST’s Operating System with Cisco UCS servers, Nexus switches, and Hyperfabric AI to deliver a ready-to-deploy, zero-trust infrastructure blueprint. This setup connects data pipelines from edge to core to cloud, simplifies enterprise AI deployment, and accelerates real-time intelligent decision-making globally. (Source: vastdata.com)

In May 2025: AWS launched a Wavelength Zone within Verizon’s 5G network in Lenexa, Kansas, integrating EC2, EBS, VPC, and other services at the network edge. This joint site enables Midwest customers to run latency-sensitive finance, healthcare, gaming, and public-sector workloads locally while meeting data residency and resiliency requirements. (Source: aws.amazon.com)

Edge Computing Market Report Scope

| Report Attributes | Details |

| Market size value in 2025 | USD 32.75 billion |

| Market size value in 2026 | USD 43.55 billion |

| Revenue forecast in 2034 | USD 443.52 billion |

| CAGR | 33.6% from 2026 - 2034 |

| Base year | 2025 |

| Historical data | 2021 - 2024 |

| Forecast period | 2026 - 2034 |

| Quantitative units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Segments covered | By Component, By Application, By Organization Size, By Verticals, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

| Key Companies | ABB, ADLINK Technology Inc., Alphabet Inc., Amazon Inc, Amazon Web Services, Aricent, Inc., Atos, Cisco Systems, Dell Technologies, EdgeConnex Inc, ElnfoChips, FogHorn Systems, General Electric Company, Google LLC, Hewlett Packard Enterprises Development, Honeywell International Inc., Huawei Technologies Co. Ltd, IBM Corporation, Intel Corporation, Juniper Networks, Microsoft Corporation, Rockwell Automation, Inc, Saguna Networks, SAP SE, Schneider Electric SE, and Siemens AG |

Source: Polaris Market Research Analysis

Edge Computing Market FAQ's

• The market size was valued at USD 32.75 Billion in 2025 and is projected to grow to USD 443.52 Billion by 2034.

• The market is projected to register a CAGR of 33.6% during the forecast period.

• A few of the key players in the market are ABB, ADLINK Technology Inc., Alphabet Inc., Amazon Inc, Amazon Web Services, Aricent, Inc., Atos, Cisco Systems, Dell Technologies, EdgeConnex Inc, ElnfoChips, FogHorn Systems, General Electric Company, Google LLC, Hewlett Packard Enterprises Development, Honeywell International Inc., Huawei Technologies Co. Ltd, IBM Corporation, Intel Corporation, Juniper Networks, Microsoft Corporation, Rockwell Automation, Inc, Saguna Networks, SAP SE, Schneider Electric SE, and Siemens AG.

• The hardware accounted for the largest market share in 2025.

• The large enterprises segment is expected to record significant growth.

Download Sample Report of Edge Computing Market

Please fill out the form to request a customized copy of the research report.