Lentiviral Vector Market Opportunity and Global Report, 2026-2034

REPORT DETAILS

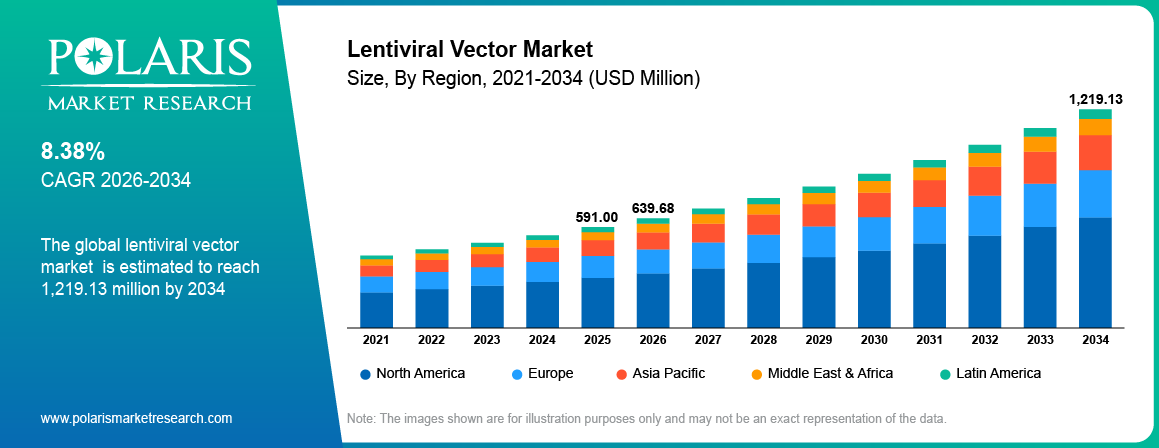

Lentiviral Vector Market Summary

The global lentiviral vector market is estimated around USD 591.00 million in 2025,with consistent growth anticipated during 2026–2034. Growth is driven by rising genetic disorders and increasing adoption of gene and cell therapies across global markets. The market is projected to grow at a CAGR of 8.38% during the forecast period.

Market Statistics

Key Takeaways

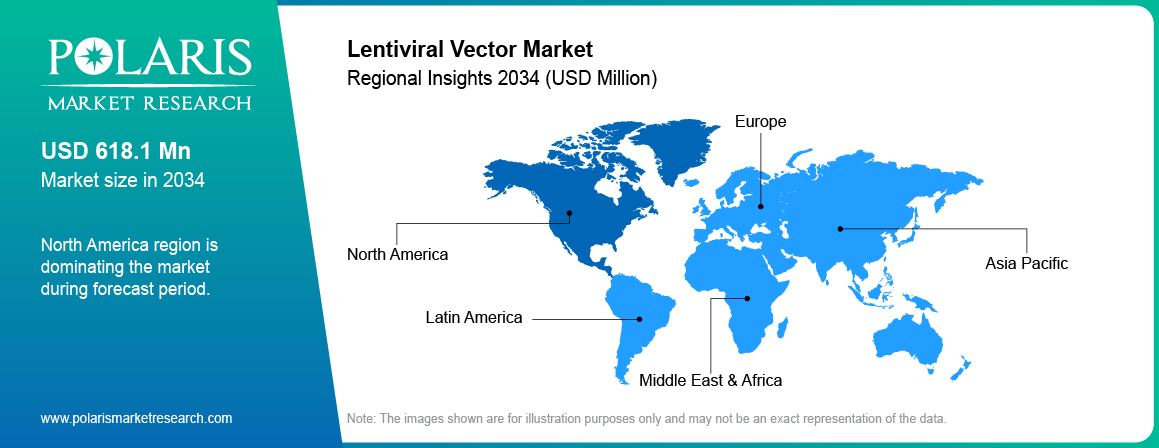

- North America dominated the lentiviral vector market, accounting for approximately 41.80% market share due to strong biotech ecosystem and advanced gene therapy research.

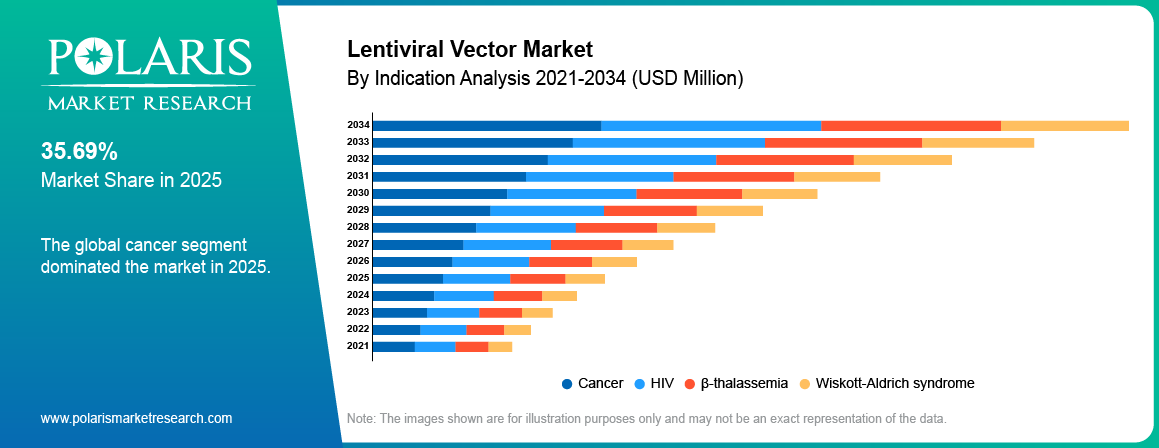

- The cancer segment led the market in 2025, holding approximately 38.25% market share due to rising prevalence and increasing adoption of gene-based oncology therapies.

- The β-thalassemia segment is projected to grow at the fastest CAGR of approximately 15.60% due to increasing focus on rare disease treatment and gene therapy advancements.

- Gene therapy segment dominated the market in 2025, contributing approximately 44.10% market share due to growing clinical approvals and expanding therapeutic applications.

- Biotech & pharmaceutical companies segment held the largest share in 2025, accounting for approximately 39.70% market share due to high R&D investments and increasing pipeline development activities.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Rise in the incidence of genetic disorders boosts treatment demand.

- Increasing number of clinical trials supports vector production requirements.

- High production costs limit large-scale commercialization.

- Increasing demand for CAR-T therapies creates growth potential.

What Are Lentiviral Vector?

Lentiviral vectors refers to gene delivery systems responsible for delivering genetic information into host cells for various research and clinical purposes. These vectors are commonly employed in gene therapy, cell therapy, and vaccine development procedures. Lentiviral vectors contribute towards stable expression of genes and can be employed in treatment of genetic and cancerous diseases. This group of vectors encompasses vectors employed for both research purposes and for clinical use. Demand for these products has been fuelled by rising interest in advanced therapies.

The value chain of the lentiviral vector includes the designing, manufacturing, and delivery of plasmids to the research and clinical settings. Vector manufacturers aim at developing high titer vector production methods for the increasing needs in the market. Many organizations are working towards increasing their manufacturing capabilities to accommodate gene and cellular therapies manufacturing at commercial scale.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

Increasing investments in gene and cell therapies have fueled the demand for lentiviral vectors. An increasing number of clinical trials for the treatment of genetic diseases and oncology has boosted the adoption of lentiviral vectors. There has been a steady development of more efficient manufacturing processes to increase yield and lower manufacturing cost. The move towards developing better therapeutic products has contributed positively to the growth of the global lentiviral vector market.

Drivers & Opportunities

Increasing prevalence of genetic disorders drives treatment demand: The prevalence of genetic diseases is increasing, creating a need for novel treatments. According to WHO, about 7.9 million babies per annum, which is roughly 6% of all newborns, have some form of genetic and partly genetic diseases; for instance, haemoglobinopathies such as thalassemia and sickle cell anaemia. The healthcare industry is looking towards more therapeutic treatments that will cater to their unmet medical needs, hence driving the development of gene therapies that use viral vectors. With an increase in the number of patients, the demand for vector therapies is increasing.

Increasing number of clinical trials supports vector production requirements: Increasing number of clinical studies requires better availability and quality of vectors. The number of biopharmaceutical firms conducting studies on their product pipeline continues to grow, which involves gene and cellular therapies for various applications. For instance, in March 2025, scientists from the Children’s Hospital of Philadelphia discovered a new type of lentivirus vector for treating patients with an extremely rare neurological disorder, thus improving efficacy and reducing risks. The tendency calls for an increasing need for consistent production of vectors for early and late phase studies.

Restraints & Challenges

High production costs limit large-scale commercialization: Expensive raw materials and advanced manufacturing technologies contribute to higher production costs. There is a challenge for companies when it comes to the cost-effectiveness of vector production at a large scale. This issue will play a role in determining the prices of treatments, thereby making them unaffordable. Therefore, the process of commercializing becomes difficult due to several reasons.

Opportunity

The growing need for CAR-T treatments presents an opportunity for growth: The growing adoption of CAR-T cell therapy treatment leads to an increase in the usage of lentivirus vectors for cell engineering processes. Companies emphasize expansion in the CAR-T pipeline in biopharma for the treatment of cancers. For instance, in April 2025, QIAGEN expanded its line of digital PCR products by introducing new lentivirus products to improve the quality control of the CAR-T cell therapy manufacturing process. Such trends will drive the need for more efficient methods of gene delivery technology. With the increasing uptake of therapy, the market opportunities for vector manufacturers will also grow.

Source: Polaris Market Research Analysis

Technology, Manufacturing & CDMO Landscape

Lentiviral Vector Generations & Technology Evolution

The lentivirus vectors have come a long way from their first-generation counterparts to current self-inactivating vectors that provide enhanced safety features. These new vectors minimize the possibility of insertional mutagenesis and offer enhanced control over gene expression. There is an emphasis on designing vectors that can enhance the efficiency of transduction.

Manufacturing Workflow

Lentiviral vectors are produced through upstream manufacturing where plasmids are transfected into the producer cells to produce vectors. Plasmid preparation is very important in ensuring that there is a consistent flow of plasmid used in producing lentivirus-based vectors. The downstream process involves purification techniques such as filtering and chromatography to ensure that impurities are removed and the vectors obtained have a high concentration. Testing ensures that the vectors are potent, sterile, and safe for use.

CDMO & Outsourcing Trends in Viral Vector Production

Production of GMP viral vectors necessitates unique equipment and skillful personnel who are more suited to work under contract manufacturing organizations. Lonza Group and Catalent are some of the manufacturers of viral vectors in the market. High capital investment and scalability challenges encourage outsourcing across biotech firms. CDMOs support process development, scale-up, and regulatory compliance, which helps companies accelerate commercialization timelines.

Segmental Insights

This report offers detailed coverage of the lentiviral vector market indication, application, and end user to help readers identify the fastest expanding and most attractive demand segments.

By Indication

-

Cancer

The cancer segment led the market in 2025 owing to the increasing uptake of genetically modified cell therapies in cancer treatments. As per the WHO, the number of cancer patients stood at 20 million in 2022 with 9.7 million deaths, which are expected to reach over 35 million by 2050, thereby indicating a rise of 77%.Increasing focus on targeted cancer therapies increases demand for lentiviral vectors in gene delivery processes. Biopharmaceutical companies expand pipelines for advanced oncology therapies, which supports segment growth.

-

β-thalassemia

The β-thalassemia segment is projected to grow at the fastest CAGR during the forecast period, due to increasing clinical success of gene therapy in treating inherited blood disorders. Rising focus on curative treatment approaches increases demand for lentiviral vectors in this segment.

By Application

-

Gene therapy

Gene therapy segment dominated the market in 2025, driven by increasing approvals and clinical development of gene-based treatments. The growing need for effective gene transfer techniques drives up the uptake of lentiviral vectors used in the field of therapy. Businesses emphasize expansion of the pipeline of gene therapies, which promotes market growth in this segment.

-

CAR-T cell therapy

The CAR-T cell therapy market is estimated to have the highest CAGR during the forecast period, driven by growing use of customized cancer therapy solutions. Asimov reached a 10 times higher lentiviral production in April 2024 and developed a stable cell line creation solution, which makes the process more scalable, affordable, and simplified. Growth in approvals of CAR-T therapy increases the need for lentivirus vectors in cell engineering applications.

By End User

-

Biotech & Pharmaceutical Companies

Biotech & pharmaceutical companies segment held the largest share in the year 2025 owing to growing investments in the research and development of gene and cell therapy. In the manufacturing of vectors, there is more concentration towards both in-house and contract vector manufacturing to meet the demand from clinics and markets. The trend will lead to greater involvement in lentiviral vector manufacturing services.

-

CROs and CDMOs

It is expected that the CROs & CDMOs segment will experience the highest CAGR over the forecast period due to rising outsourcing of production of viral vectors. Service providers specialize in dealing with complexities of manufacturing processes, which boosts the segment’s growth.

Source: Polaris Market Research Analysis

Regional Analysis

North America Market Assessment

North America dominated in the lentiviral vector market owing to the favorable regulatory environment and the development of advanced biopharmaceutical ecosystem in the region. For example, in January 2026, AGC Biologics assisted in facilitating FDA and EMA approval processes for Waskyra, a lentiviral-based gene therapy drug administered to patients suffering from Wiskott-Aldrich Syndrome. Furthermore, there are numerous key players in North America that specialize in gene therapy, hence contributing to the demand for lentiviral vectors during clinical and commercial manufacturing stages.

Asia Pacific Lentiviral Vector Market Insights

Asia Pacific is projected to grow at the fastest CAGR, due to expanding biopharmaceutical manufacturing capacity and rising clinical research activity. In March 2023, BioViros created the first lentiviral vector CDMO facility in New Zealand to develop custom viral vectors used in cell and gene therapies, solving the problem of insufficient production capabilities and speeding up early-stage research. The growing financial commitment by local biotech firms facilitates the development of gene and cell therapies.

Europe Lentiviral Vector Market Overview

Europe represents a mature market, fueled by increasing focus on rare disease treatment and gene therapy development. According to EURORDIS, around 30 million people in 48 European countries live with a rare disease.Favorable regulatory pathways for advanced therapies improve product approvals across key countries. Growing collaboration between research institutes and biotech firms increases demand for lentiviral vectors.

Source: Polaris Market Research Analysis

Competitive Landscape & Key Players

The lentivirus vector industry consists of moderate consolidation in terms of CDMOs and specialized biotech firms competing with one another when it comes to vector production for both research and therapeutic uses. The following points are some examples of factors that influence the lentivirus vector market. These include production capability, quality of vectors, scalability, and regulatory issues.

The key players in the industry are Lonza Group, Catalent, Inc., Thermo Fisher Scientific, Merck KGaA, FUJIFILM Biotechnologies, Oxford Biomedica, Sartorius AG, Charles River Laboratories International, Inc., WuXi Advanced Therapies, Takara Bio Inc., GenScript Biotech Corporation, Aldevron LLC, and others.

Premium Insights

Regulatory Framework

The regulations that govern gene therapy set standards for the safety, quality, and efficacy of lentivirus vectors. Organizations such as the FDA and EMA ensure that vector production is well-regulated to guarantee safe and effective vector production processes. This organization will have to observe GMPs and also provide all information on the efficiency and safety of the vector being used.

Key Risks Associated With Lentiviral Vector Industry

Some of the regulatory concerns regarding the use of lentiviral vector-mediated therapy include the dangers involved in the use of replicating vectors. Testing for replicative capacity is done by the manufacturers to make sure that the vectors do not replicate and are safe to use. The regulatory bodies insist on a follow-up of patients for possible adverse effects.

Strategic Insights

Trends in the development of lentiviral vectors indicate substantial capital inflows in the gene and cell therapy sectors worldwide. Investors tend to invest in those companies that possess scalable manufacturing systems and regulatory proficiency. Scalability and high manufacturing costs present critical barriers to growth. The future of the market lies in automation, vector design optimization, and increasing the scope of CDMO operations.

Key Players

- Aldevron LLC

- Catalent, Inc.

- Charles River Laboratories International, Inc.

- FUJIFILM Biotechnologies

- GenScript Biotech Corporation

- Lonza Group

- Merck KGaA

- Oxford Biomedica

- Sartorius AG

- Takara Bio Inc.

- Thermo Fisher Scientific

- WuXi Advanced Therapies

Industry Developments

- April 2026: OXB has announced a rapid CDMO program for viral vectors to speed up their development and manufacturing process, cutting the time taken to get to Good Manufacturing Practice production down by 50%. [source: oxb.com]

- November 2025: Vector BioMed has increased its LENTIVERSE product portfolio and created a fresh brand image to facilitate access to cellular and gene therapies, providing comprehensive services for lentiviral vector engineering and CAR-T manufacturing. [source: vectorbiomed.com]

Lentiviral Vector Market Segmentation

By Indication Outlook (Revenue, USD Million, 2021-2034)

- HIV

- β-thalassemia

- Wiskott-Aldrich syndrome

- Cancer

By Application Outlook (Revenue, USD Million, 2021-2034)

- Gene therapy

- CAR-T cell therapy

- Oncology treatments

- Rare disease therapies

By End User Outlook (Revenue, USD Million, 2021-2034)

- Biotech & Pharmaceutical Companies

- CROs and CDMOs

- Academic Research Institutes

By Regional Outlook (Revenue, USD Million, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Lentiviral Vector Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 591.00 Million |

| Market Size in 2026 | USD 639.68 Million |

| Revenue Forecast by 2034 | USD 1,219.13 Million |

| CAGR | 8.38% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Lentiviral Vector Market FAQ's

The global market size was valued at USD 591.00 million in 2025 and is projected to grow to USD 1,219.13 million by 2034.

North America dominates the market due to strong regulatory framework and advanced biopharmaceutical infrastructure.

Major applications include gene therapy, CAR-T cell therapy, oncology treatments, and rare disease therapies.

A few of the key players in the market are Lonza Group, Catalent, Inc., Thermo Fisher Scientific, Merck KGaA, FUJIFILM Biotechnologies, Oxford Biomedica, Sartorius AG, Charles River Laboratories International, Inc., WuXi Advanced Therapies, Takara Bio Inc., GenScript Biotech Corporation, Aldevron LLC, and others.

Key drivers include rising genetic disorders, increasing clinical trials, and growing investment in gene therapy.

Major demand comes from biotech and pharmaceutical companies, CDMOs, and research institutes.

The market outlook remains strong due to expansion of advanced therapies and increasing commercialization of gene therapies.

Download Sample Report of Lentiviral Vector Market

Please fill out the form to request a customized copy of the research report.