Lithium Metal Market Size, Industry Report, 2026 - 2034

REPORT DETAILS

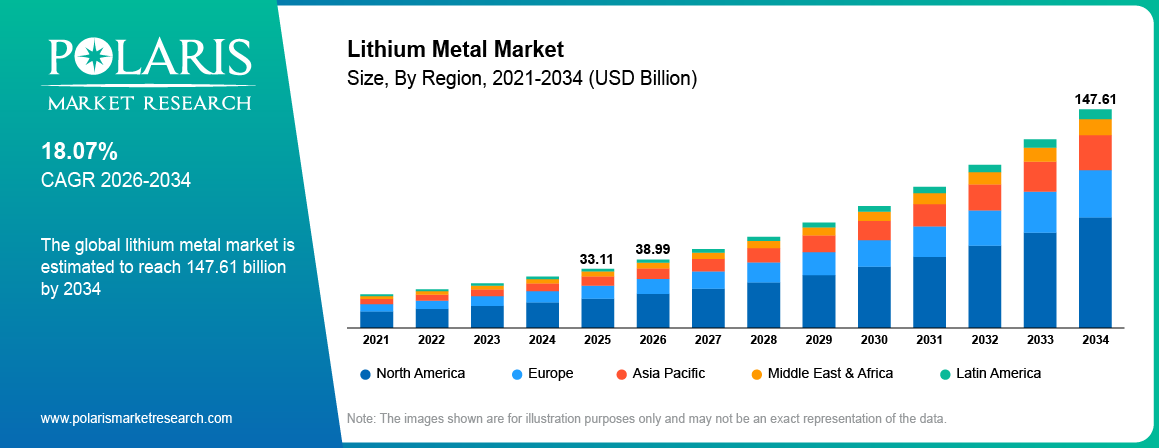

Lithium Metal Market Summary

The global lithium metal market is estimated around USD 33.11 Billion in 2025,?with consistent growth anticipated during 2026–2034. Expansion is driven by rising demand for high-energy-density batteries, increasing electric vehicle production, and growing deployment of renewable energy storage systems. The market is projected to grow at a CAGR of 18.07% during the forecast period.

Market Statistics

Key Takeaways

- Asia Pacific lithium metal market leads, accounting for approximately 44.30% market share due to strong battery manufacturing base and rising EV production.

- Lithium ores / hard-rock sources constitute the dominant portion, holding approximately 39.85% market share due to established mining infrastructure and supply availability.

- Li-ion anode material / next-gen battery applications dominated the market, contributing approximately 42.60% market share due to growing demand for high-energy-density batteries.

- The batteries segment held the major market share, accounting for approximately 46.75% due to increasing adoption of lithium metal in advanced battery technologies.

- The aerospace & defense segment is expected to be the fastest-growing segment, registering a CAGR of approximately 13.95% driven by demand for lightweight and high-performance energy systems.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Growth of electric vehicles is driving the requirement for lithium metal to serve as the next-generation battery material.

- Shift towards solid-state batteries is creating fresh prospects for the use of lithium metal in batteries.

- Issues of safety regarding dendrite growth and limitations in the supply chain are hindering full-scale commercialization.

- Transition toward solid-state batteries is opening new opportunities for lithium metal adoption.

What is the Lithium Metal Market?

The market consists of a highly pure lithium market that is part of the entire lithium value chain. The lithium metal market deals specifically with pure metallic lithium as compared to lithium carbonate and lithium hydroxide that are forms of lithium chemicals. Pure metallic lithium is considered the pure metallic form of lithium, while lithium carbonate and lithium hydroxide represent intermediate chemical forms of lithium.

Lithium metal is unique when compared to other types of lithium due to its unique performance and applications. Lithium metal has high energy density, making it vital in applications using lithium metal batteries, solid-state batteries, and lithium sulfur batteries. Lithium metal is different from other lithium markets because the latter involves lithium used in lithium-ion batteries. Lithium metal market trends emphasize the rise in research and development spending as well as the development of new types of batteries on a pilot scale.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

In the market forecast, significant growth prospects are expected owing to the rising use of high-capacity batteries and electric power systems. Furthermore, aerospace, military, and electronic applications are on the rise. The market forecast is backed by improvements in battery technology and efforts to develop energy-efficient storage devices. This has led to the continued rise in the market share in the dynamic world of energy materials.

Drivers & Opportunities

Rapid Expansion of The Electric Vehicle Industry: Increasing manufacturing of electric vehicles results in high demand for battery materials with high energy density, such as lithium metal which can be considered as the anode material of the future. Energy density is greater than in graphite anodes. The International Energy Agency stated that electric vehicle sales were more than 17 million units in 2024, recording an increment of 25 percent from the previous year. With this trend, there has been an intensification of research efforts on innovative battery systems such as solid-state and lithium-sulfur batteries, thereby escalating the demand for lithium metal.

Growing Deployment of Renewable Energy Systems: The increasing utilization of renewable energy sources has led to a growing demand for energy storage systems. Among the features of lithium metal batteries are high efficiency and high energy density; therefore, lithium metal batteries can support grid energy storage and intermittency sources. According to the International Energy Agency, the share of renewables in the generation of energy across the world in the year 2024 was about 32%, and this figure is expected to go up to 43% by 2030. These factors have been causing the demand for more efficient batteries to increase, which means that lithium metal will be an important part of batteries in the future.

Restraints & Challenges

Safety Concerns and Supply Chain Constraints: However, lithium metal batteries have a disadvantage in that they are associated with safety issues such that dendrites will lead to electrical shorts and even thermal runaway. At the same time, lithium supply is concentrated in a few regions, creating procurement risks and price volatility. The manufacturing processes and refinement difficulties hinder the expansion of production capabilities and availability to battery manufacturers.

Opportunity

Transition Toward Solid-State Batteries: Solid-state battery technology is forcing high demands on lithium metal as the most appropriate anode material in solid-state batteries. Compared to lithium-ion batteries, solid-state batteries have superior safety, energy density, and lifecycle performance. In July 2025, Tailan New Energy debuted a smart solid-state battery powered by artificial intelligence technology with built-in sensor capabilities. This is fueling the commercialization of solid-state batteries using lithium metal.

Source: Polaris Market Research Analysis

Segmental Insights

The report provides comprehensive information about the market by source, type, application, and end-use sector in order to assist readers in finding the areas that have the most potential.

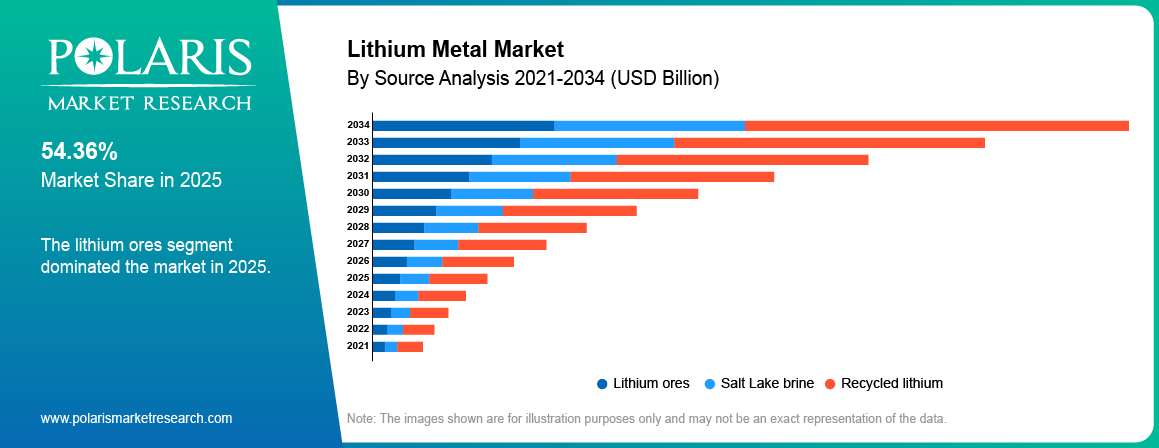

By Source

-

Lithium ores

Lithium ores / hard-rock sources constitute the dominant portion due to their better quality and availability compared to lithium ores versus lithium from brines. This is due to hard-rock-based lithium is easier to purify compared to lithium from ores and brine.

-

Recycled lithium

Recycled lithium / secondary supply is the fastest growing type owing to environmental sustainability and security of supply considerations. Recycled lithium metal supply from battery scrap and end-of-life cells reduces dependence on mining and lowers environmental impact.

By Application

-

Li-ion anode material

Li-ion anode material / next-gen battery applications dominated the market due to rising lithium metal use in batteries. The growth in the demand for lithium metal as the anode material can be attributed to its capacity to store high energy content. The next generation of batteries sees heavy investments in this segment.

-

Intermediates and Specialty Chemical

Intermediates and specialty chemical/pharma uses are the fastest-growing segment as lithium metal intermediates are used in organic synthesis and lithium metal pharmaceutical applications. The demand is fueled by specialty chemicals, premium pharmaceutical products, and unique industrial processes where the chemical properties of lithium offer some process benefits.

By End-Use Industry

-

Batteries

The batteries segment held the major market share owing to lithium metal as an energy source and EV batteries, which create mass-level demand. With the rising trend in battery technology, there is an increased demand for lithium metal due to its high energy density and efficiency.

-

Aerospace & Defense

The aerospace & defense segment is expected to be the fastest-growing segment owing to the growing utilization of lithium metal in aerospace for the purpose of lightweight alloys and advanced energy sources.

Source: Polaris Market Research Analysis

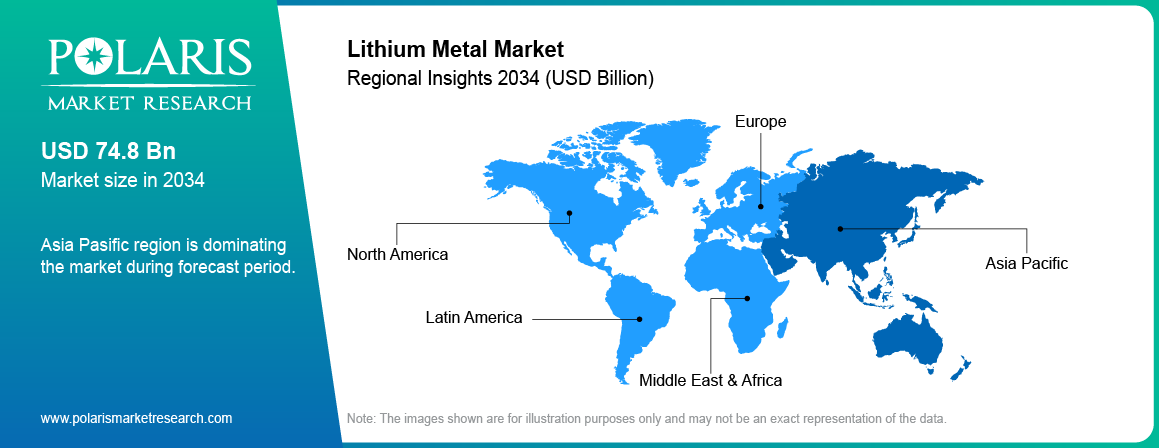

Regional Analysis

Asia Pacific Lithium Metal Market Assessment

Asia Pacific lithium metal market leads due to a strong battery manufacturing ecosystem and deep supply chain integration across China, Japan, and South Korea. The China lithium metal market leads the battery production and demand worldwide. According to the International Energy Agency, over 75% of the total batteries manufactured worldwide are made in China, with 30% decline in the price of batteries in 2024, hence efficiencies. The adoption of electric vehicles (EVs), advanced processing, and exports still impact the demand for lithium metals in the Asia Pacific region.

North America Lithium Metal Market Overview

In the North America lithium metal market, the growth is mainly driven by increased investment in the manufacturing of batteries and supply chain localization policies. For the US lithium metal market, increased investment in batteries is due to critical mineral strategy as well as gigafactory expansions. In April 2026, Apogee Power plans to invest USD 16 million to establish battery manufacturing and assembly at Kansas. The facility will be used in manufacturing lithium-ion phosphate batteries starting from 2026.

Europe Lithium Metal Market Assessment

In Europe, the market demand for lithium metal depends significantly on legislation, as well as environmental consciousness. This has made lithium metal very much in demand, owing to the policies of the government regarding electric vehicles (EVs) and batteries. In July 2025, the European Commission released guidelines aimed at improving recycling and recovery of materials from waste batteries.This strategy seeks to guarantee adequate supplies of crucial materials while promoting a circular economy. Some nations like Germany are moving towards developing advanced batteries and recycling technologies.

Rest of the World Lithium Metal Market Assessment

Latin America and the Middle East & Africa have become a promising opportunity for the market due to resource abundance. Latin America is home to robust lithium deposits and helps sustain international supplies via mining operations and exports. On the flip side, the Middle East and Africa have increasingly been focusing on processing and collaborations. These two regions are therefore poised for future growth.

Source: Polaris Market Research Analysis

Competitive Landscape

Key Players & Strategic Developments

The competitive nature of the market can be seen with the active involvement of lithium manufacturers, lithium refiners/processors, lithium battery materials producers, and technology providers developing new approaches to produce high purity lithium to meet future lithium batteries demands. Competitiveness within the market includes capacity additions, battery grade lithium purity, and vertical lithium chain integration.

Key players operating in the market include Albemarle Corporation, American Elements, Ganfeng Lithium Co., Ltd., Indium Corporation, Livent Corporation, Lithium Americas Corp., Novonix Limited, Piedmont Lithium Inc., Polyimede Technologies, Inc., Shenzhen Chengxin Lithium Group Co., Ltd., Sichuan Yahua Industrial Group Co., Ltd., Tianqi Lithium Corp., Umicore SA, 6K Inc., and Zpower, Inc.

Premium Insights: Value Chain, Supply Chain Pressure, Pricing Trends, and Market Opportunities

How does the lithium metal value chain work?

The lithium metal value chain is highly specialized, beginning with lithium metal raw material sourcing from brine or hard rock deposits. The lithium that is mined goes through the lithium metal refining process to refine it into either lithium carbonate or lithium hydroxide before converted via electrochemistry into lithium metal.

Shaping of the processed lithium into foil, ingot, and powder form occurs at the final stage for usage in batteries or other industrial purposes. Such complex procedures contribute to higher production costs associated with lithium metal.

Where are the biggest supply-side pressures?

The supply side is constrained due to high concentration of lithium ore in specific geographical locations, hence the emergence of a lithium metal demand-supply mismatch whenever battery demand is high. Battery-grade purity acquisition faces battery-grade purity difficulties.

These constraints, the inability to increase the output of lithium metal facilities, and safety concerns regarding the highly reactive nature of lithium metal have constrained the opportunities for expansion. This is due to the logistics involved due to the high reactivity levels, impacting lithium metal export and import trends around the world.

How are pricing and investment trends shaping the market?

Lithium metal price trends exhibit volatility, affected by feedstock variations, restricted capacities, and increasing battery demands. Lithium metal price volatility is further driven by a limited supplier base and high entry barriers.

Why lithium metal is harder to scale than standard battery materials?

Higher purity requirements, complex processing, and handling challenges make scaling more difficult than conventional lithium compounds.

How recycled lithium may affect long-term supply?

Recycling batteries can help mitigate the supply problem with respect to lithium from a long-term perspective despite its current ineffectiveness.

Which opportunity pockets are underappreciated?

The high quality lithium used in solid-state batteries, local refining, and enhanced processing offer good potential for lithium metal investments.

Key Players

- Albemarle Corporation

- American Elements

- Ganfeng Lithium Co., Ltd.

- Indium Corporation

- Livent Corporation

- Lithium Americas Corp.

- Novonix Limited

- Piedmont Lithium Inc.

- Polyimede Technologies, Inc.

- Shenzhen Chengxin Lithium Group Co., Ltd.

- Sichuan Yahua Industrial Group Co., Ltd.

- Tianqi Lithium Corp.

- Umicore SA

- 6K Inc.

- Zpower, Inc.

Industry Developments

- April 2026: KoBold Metals initiated one of the world’s largest lithium exploration campaigns in the Democratic Republic of Congo, targeting large-scale resource discovery using AI-driven geological analysis. [source: battery-news.de]

- March 2026: POSCO Future M partnered with Kumho Petrochemical and BEI to develop anode-free lithium-metal batteries with 30–50% higher energy density and significantly faster charging. [source: battery-news.de]

Market Segmentation

By Source Outlook (Revenue, USD Billion, 2021-2034)

- Salt Lake brine

- Lithium ores

- Recycled lithium

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Li-ion anode material

- Alloys and metal processing

- Intermediates and specialty chemical

By End-Use Industry Outlook (Revenue, USD Billion, 2021-2034)

- Batteries

- Metal processing

- Pharmaceuticals

- Aerospace & defense

- Electronics / energy storage

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 33.11 Billion |

| Market Size in 2026 | USD 38.99 Billion |

| Revenue Forecast by 2034 | USD 147.61 Billion |

| CAGR | 18.07% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Lithium Metal Market FAQ's

The global market size was valued at USD 33.11 Billion in 2025 and is projected to grow to USD 147.61 Billion by 2034.

Asia Pacific dominated the region in 2025, due to strong battery manufacturing capacity, EV production, and integrated supply chains.

Battery manufacturers account for the largest share due to demand from EVs and energy storage systems.

A few of the key players in the market are Albemarle Corporation, American Elements, Ganfeng Lithium Co., Ltd., Indium Corporation, Livent Corporation, Lithium Americas Corp., Novonix Limited, Piedmont Lithium Inc., Polyimede Technologies, Inc., Shenzhen Chengxin Lithium Group Co., Ltd., Sichuan Yahua Industrial Group Co., Ltd., Tianqi Lithium Corp., Umicore SA, 6K Inc., and Zpower, Inc.

Growth is driven by EV expansion, renewable energy storage demand, and advancements in battery technologies.

Trends include solid-state battery development, recycling expansion, and increasing use in high-performance applications.

In lithium metal batteries, lithium is used as the anode, whereas in lithium-ion batteries, lithium compounds like graphite are used as the anode.

They have higher energy density, greater distance, and better performance than ordinary batteries.

The major applications are in the automobile industry, energy storage, space technology, and electronics.

Download Sample Report of Lithium Metal Market

Please fill out the form to request a customized copy of the research report.