Blood Culture Test Market Trends & Growth Analysis Report, 2026-2034

REPORT DETAILS

REPORT DETAILS

Blood Culture Test Market Summary

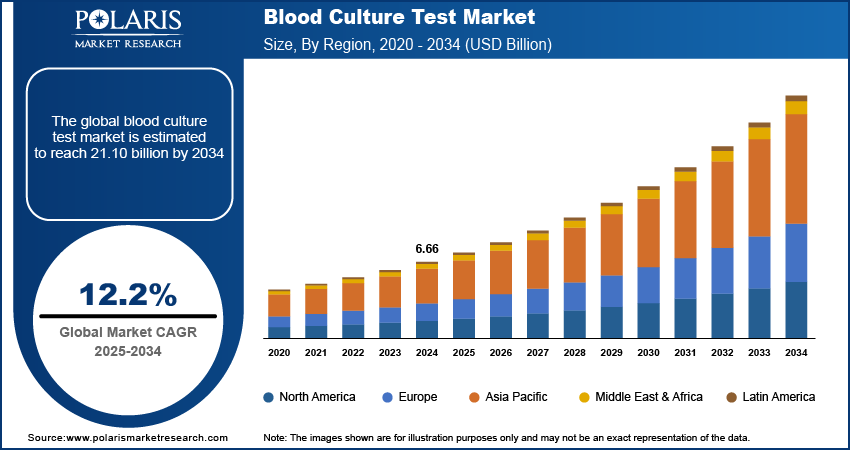

The global blood culture test market size was valued at USD 7.45 billion in 2025. The market is projected to exhibit a CAGR of 12.2% during 2026–2034. The market is driven by the rising prevalence of bloodstream infections, increasing sepsis cases, growing antimicrobial resistance, and an expanding geriatric population. The market is also benefiting from technological advancements in diagnostics and global efforts to enhance infection control through improved healthcare infrastructure and regulatory guidelines.

Market Statistics

Key Takeaways

- North America held the dominant position in the blood culture test market, accounting for 42.39% share in 2025. This is because of the region's technologically advanced healthcare system, high rate of R&D, and high infection prevalence rate.

- Europe is expected to record significant growth at a CAGR of 11.6%. This is attributed to the presence of developed healthcare infrastructure, early detection of infections, and increased cases of sepsis.

- Asia Pacific is projected to grow at a rapid rate of 13.2% CAGR. The growth of the blood culture test market in Asia Pacific is projected to be driven by the rising incidence of infectious diseases, rising healthcare expenditures, and increased diagnostic demand.

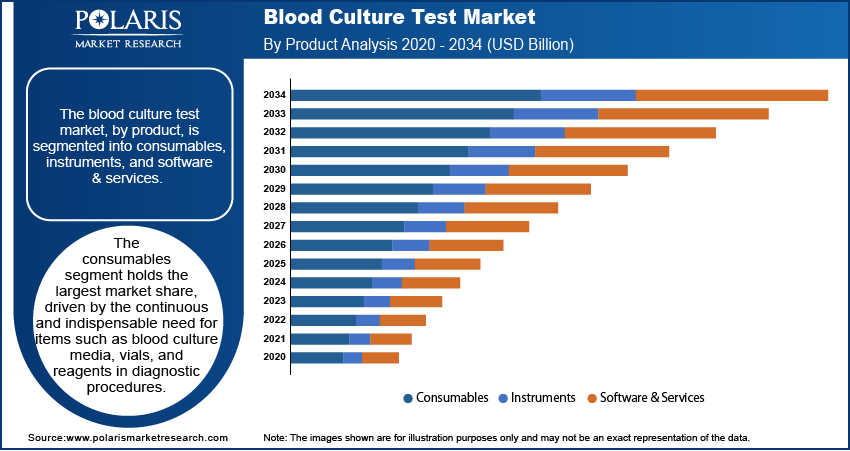

- Consumables accounted for the largest share of 59.6% in 2025. This is because these products are frequently used and disposable, with a constant demand for testing.

- The conventional technique held a market share of 64.5% in 2025. The conventional blood culture test technique is widely used owing to its effectiveness and reliability across hospitals and laboratories.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The rising global incidence of sepsis and bloodstream infections increases the demand for accurate and timely diagnostic solutions such as blood culture tests.

- Growing antibiotic resistance drives the need for precise pathogen identification, fueling the adoption of blood culture testing in antimicrobial stewardship programs.

- Increasing healthcare access in emerging economies expands the patient base for diagnostic tests, including blood culture testing in hospitals and clinics.

- High costs of advanced blood culture systems and limited affordability in low-income regions hinder widespread adoption and market penetration.

AI Impact on Blood Culture Test Market

- Artificial intelligence enables faster detection of infection by interpreting blood samples quickly and effectively.

- It increases the precision of test results by eliminating inaccuracies when detecting microorganisms such as bacteria.

- It ensures that tests are carried out faster through quick interpretation of the results.

- AI makes it easier for laboratories to cope with workload issues through automation

Source: Polaris Market Research Analysis

Blood Culture Test Market Defined

The blood culture test market is a critical segment within the diagnostic industry, focusing on detecting bloodstream infections such as sepsis and bacteremia. Blood culture tests help identify bacterial and fungal pathogens in the blood, aiding in the timely initiation of targeted antimicrobial therapy. The market encompass consumables, instruments, and software solutions used in clinical laboratories, hospitals, and diagnostic centers. Technological advancements, including automated blood culture systems and molecular diagnostic techniques, have enhanced test accuracy and turnaround times, driving adoption across healthcare settings.

Key drivers of the blood culture test market demand include the rising prevalence of infectious diseases, increasing cases of sepsis, and growing demand for rapid and accurate diagnostic solutions. The surge in antibiotic-resistant infections has further intensified the need for effective blood culture tests to guide antimicrobial stewardship programs. Additionally, the expanding geriatric population, which is more susceptible to bloodstream infections, contributes to market growth. Increasing healthcare expenditure, government initiatives for infection control, and the expansion of diagnostic laboratory infrastructure globally are also supporting blood culture test market expansion.

Market Dynamics

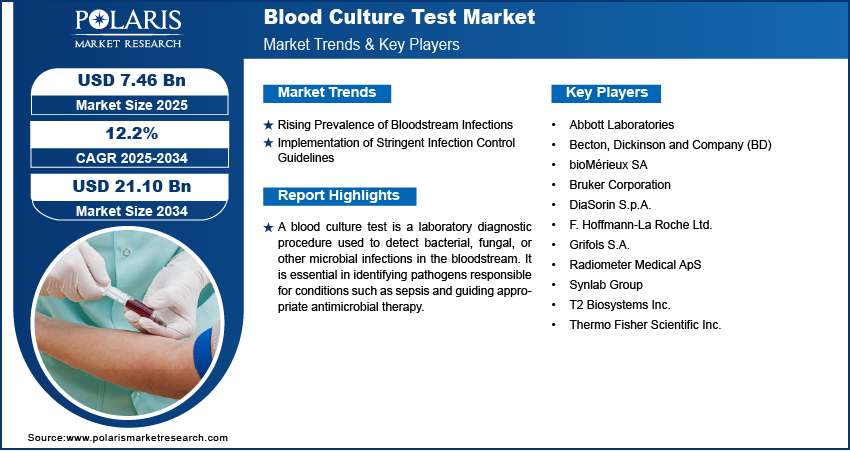

Rising Prevalence of Bloodstream Infections

The increasing incidence of bloodstream infections, including sepsis, has significantly impacted the blood culture test market. Blood culture tests are essential for identifying the causative pathogens, enabling timely and appropriate antimicrobial therapy. According to the Agency for Healthcare Research and Quality (AHRQ), central line-associated bloodstream infections (CLABSIs) result in approximately 28,000 deaths in the US annually. This alarming statistic underscores the critical need for effective diagnostic tools, such as blood culture tests, to detect and manage these infections promptly.

Implementation of Stringent Infection Control Guidelines

The adoption of rigorous infection prevention protocols by healthcare organizations has bolstered the utilization of blood tests. For instance, the World Health Organization (WHO) released new guidelines in May 2024 aimed at reducing bloodstream infections associated with catheter use. These guidelines recommend best practices for the insertion, maintenance, and removal of catheters to minimize infection risks. The emphasis on preventing healthcare-associated infections has led to increased blood culture testing to monitor and control potential outbreaks effectively. Thus, the implementation of stringent infection control guidelines boosts the blood culture test market growth.

Source: Polaris Market Research Analysis

Segment Insights

Market Assessment – By Product

The blood culture test market, by product, is segmented into consumables, instruments, and software & services. Consumables accounted for the largest share of 59.6% in 2025, driven by the continuous and indispensable need for items such as blood culture media, vials, and reagents in diagnostic procedures. The recurrent demand for these products in routine testing and their single-use nature contribute to sustained consumption, ensuring a steady revenue stream for manufacturers. Additionally, the consumables segment benefits from advancements in formulation and quality, enhancing the accuracy and reliability of blood culture tests, which further solidifies its dominant position in the blood culture test market.

| Product Category | Description | Use |

| Consumable | Culture bottles, media, test kits | Collecting and growing microorganisms in blood samples |

| Instruments | Blood culture analyzer, incubator system | Detecting and monitoring microbial growth in blood samples |

| Software/Service | Data management software, reporting services | Assisting in managing test data and improving test accuracy |

Source: Polaris Market Research Analysis

Market Evaluation – By Technique

The blood culture test market, by technique, is segmented into conventional and automated. The conventional technique held a market share of 64.5% in 2025. This dominance is attributed to its extensive utilization across hospitals, pathology laboratories, and clinical settings. The widespread adoption of conventional methods is due to their established reliability and the familiarity of healthcare professionals with these procedures. Additionally, ongoing research and development efforts aim to enhance the efficiency and accuracy of these traditional techniques, further solidifying their prominent position in the market.

Blood Culture Test Technologies

| Technological Method | Explanation of Method | What it Does | Key Benefit |

| Culturing Technology | Cultivation of bacteria from samples in laboratory environment | Finding infections by cultivating microbes | Effective and popular technology |

| Molecular Technology | DNA or RNA molecules are utilized for the detection of pathogens | Finding pathogens through genes within seconds | Speed and precision of detection |

| Proteomic Technology | Examines proteins produced by microbes | Finding microbes through their protein composition | Exact and precise identification of microbes |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Regional Insights

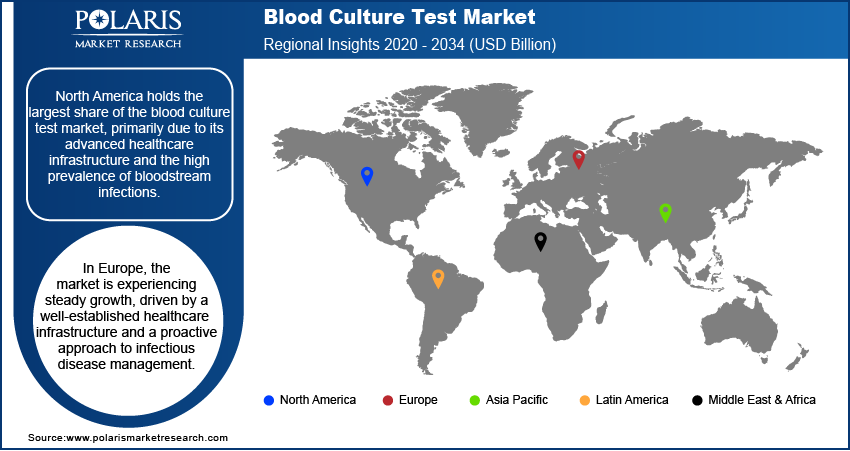

By region, the study provides blood culture test market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. According to the blood culture test market statistics, North America holds the largest market share, primarily due to its advanced healthcare infrastructure and the high prevalence of bloodstream infections. The region benefits from significant investments in research and development, leading to the adoption of innovative diagnostic technologies. Additionally, the presence of key industry players and supportive government initiatives boost the market expansion in this region.

In Europe, the blood culture test market is experiencing steady growth, driven by a well-established healthcare infrastructure and a proactive approach to infectious disease management. Countries such as Germany, France, and the UK are leading contributors, with a strong focus on early diagnosis and treatment of bloodstream infections. The rising prevalence of sepsis and other severe infections has heightened the demand for advanced diagnostic tools, including blood culture tests. Additionally, government initiatives aimed at combating antimicrobial resistance and improving patient outcomes further support market growth in the region.

The Asia Pacific blood culture test market is anticipated to witness significant growth, primarily due to the increasing incidence of infectious diseases and improving healthcare infrastructure. Countries such as China, India, and Japan are at the forefront of this expansion, with rising healthcare expenditures and heightened awareness of early and rare disease detection. The growing burden of sepsis and other bloodstream infections necessitates efficient diagnostic solutions, propelling the adoption of blood culture tests. Moreover, strategic initiatives by key industry players to establish a presence in these emerging markets are expected to drive market growth.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

In the blood culture test market, several key players are actively contributing to advancements in diagnostic technologies. A few notable players in the market are Abbott Laboratories; Becton, Dickinson and Company (BD); bioMérieux SA; Bruker Corporation; DiaSorin S.p.A.; F. Hoffmann-La Roche Ltd.; Grifols S.A.; Radiometer Medical ApS; Synlab Group; T2 Biosystems Inc.; and Thermo Fisher Scientific Inc.

The competitive landscape of the blood culture test market is characterized by continuous innovation and strategic collaborations among these key players. Companies are investing heavily in research and development to introduce automated and rapid diagnostic systems that enhance the accuracy and speed of pathogen detection. For instance, BD's acquisition of specific technologies has expanded its portfolio, enabling the company to offer more integrated blood culture solutions. Similarly, bioMérieux's development of the VITEK REVEAL system exemplifies efforts to provide rapid antimicrobial susceptibility testing directly from positive blood cultures.

Becton, Dickinson and Company (BD) is a prominent global medical technology firm specializing in the development and production of medical supplies, devices, laboratory equipment, and diagnostic products. Serving a diverse clientele that includes healthcare institutions, life science researchers, clinical laboratories, and the pharmaceutical industry, BD is committed to enhancing patient care and advancing healthcare outcomes. The company's extensive portfolio encompasses products essential for blood culture testing, such as advanced diagnostic instruments and consumables.

bioMérieux SA is a leading provider of in vitro diagnostic solutions, dedicated to identifying the sources of diseases and ensuring consumer safety. With a strong focus on infectious disease diagnostics, bioMérieux offers a comprehensive range of products, including automated blood culture systems and reagents designed to detect bloodstream infections. The company's innovations in microbiology and molecular biology have significantly contributed to the efficiency and accuracy of blood culture testing in clinical settings.

List of Key Companies

- Abbott Laboratories

- Becton, Dickinson and Company (BD)

- bioMérieux SA

- Bruker Corporation

- DiaSorin S.p.A.

- F. Hoffmann-La Roche Ltd.

- Grifols S.A.

- Radiometer Medical ApS

- Synlab Group

- T2 Biosystems Inc.

- Thermo Fisher Scientific Inc.

Blood Culture Test Industry Developments

- March 2026: MeMed announced that the U.S. Food and Drug Administration (FDA) granted Breakthrough Device Designation (BDD) to MeMed BV Flex. The company stated that MeMed BV Flex is an AI-powered host-response test. It is designed to distinguish bacterial from viral infections with the use of capillary blood in 15 minutes. (source: me-med.com)

- January 2026: bioMérieux announced the finalization of Accellix, Inc. According to bioMérieux, the acquisition will strengthen its portfolio in rapid microbiology and advanced testing for quality control laboratories. (source: biomerieux.com)

- June 2023: T2 Biosystems announced that its Candida auris test application was submitted to the FDA for Breakthrough Device Designation. The test was added to the T2Candida Panel for rapid, direct-from-blood detection. (Source: biospace.com)

Future Outlook

The market for blood culture testing is projected to experience steady growth, owing to the growing prevalence of sepsis and bloodstream infection cases. The usage of automated and artificial intelligence diagnostic solutions has enhanced the efficiency of testing procedures and improved their accuracy. An expanding healthcare sector, particularly in the Asia Pacific region, is expected to positively impact market growth.

Blood Culture Test Market Segmentation

By Product Outlook (Revenue – USD Billion, 2021–2034)

- Consumables

- Instruments

- Software & Services

By Technique Outlook (Revenue – USD Billion, 2021–2034)

- Conventional

- Automated

By Technology Outlook (Revenue – USD Billion, 2021–2034)

- Culture-Based Technology

- Molecular Technology

- Proteomic Technology

By Application Outlook (Revenue – USD Billion, 2021–2034)

- Bacterial Infections

- Fungal Infections

- Mycobacterial Infections

- Others

By End Use Outlook (Revenue – USD Billion, 2021–2034)

- Hospital Laboratories

- Reference Laboratories

- Others

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest f Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- Suth Korea

- Indnesia

- Australia

- Vietnam

- Rest f Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- Suth Africa

- Rest f Middle East & Africa

- Latin America

- Mexic

- Brazil

- Argentina

- Rest f Latin America

Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 7.45 billion |

| Market Size Value in 2026 | USD 8.33 billion |

| Revenue Forecast by 2034 | USD 20.98 billion |

| CAGR | 12.2% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

How is the report valuable for an organization?

Workflow/Innovation Strategy

The blood culture test market has been segmented into detailed segments of product, technique, technology, application, and end use. Moreover, the study provides the reader with a detailed understanding of the different segments at both the global and regional levels.

Growth/Marketing Strategy

Companies in the blood culture test market focus on expanding their product portfolios through research and development, introducing automated and rapid diagnostic solutions to improve detection efficiency. Strategic partnerships, and mergers and acquisitions are commonly pursued to strengthen market presence and enhance technological capabilities. Geographic expansion into emerging markets is a key strategy, driven by rising healthcare investments and increasing awareness of bloodstream infections. Additionally, players emphasize regulatory approvals and compliance to ensure product adoption in clinical settings. Digital marketing and educational initiatives targeting healthcare professionals further support market penetration and brand recognition.

FAQ's

The size was valued at USD 7.45 billion in 2025 and is projected to grow to USD 20.98 billion by 2034.

The market is projected to register a CAGR of 12.2% during the forecast period.

North America held the dominant position in the blood culture test market, accounting for 42.39% share in 2025.

A few key players in the market include Abbott Laboratories; Becton, Dickinson and Company (BD); bioMérieux SA; Bruker Corporation; DiaSorin S.p.A.; F. Hoffmann-La Roche Ltd.; Grifols S.A.; Radiometer Medical ApS; Synlab Group; T2 Biosystems Inc.; and Thermo Fisher Scientific Inc.

Consumables accounted for the largest share of 59.6% in 2025.

The conventional technique held a market share of 64.5% in 2025.

Download Sample Report of Blood Culture Test Market

Please fill out the form to request a customized copy of the research report.