Compound Semiconductor Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Compound Semiconductor Market Summary

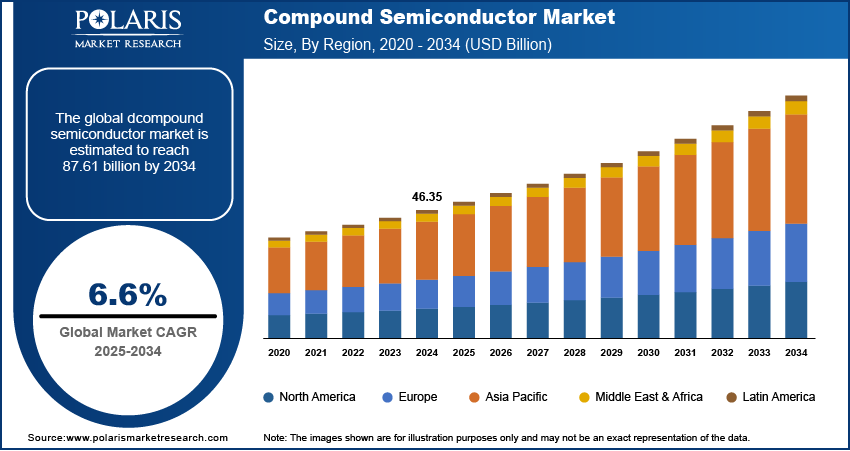

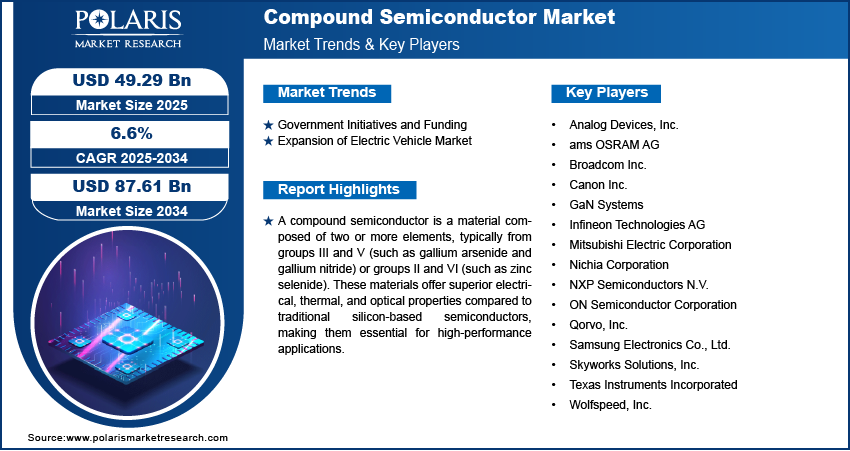

The compound semiconductor market size was valued at USD 49.20 billion in 2025. The market is projected to grow from USD 52.27 billion in 2026 to USD 87.45 billion by 2034, exhibiting a CAGR of 6.6% during 2026–2034.

Market Statistics

Key Insights

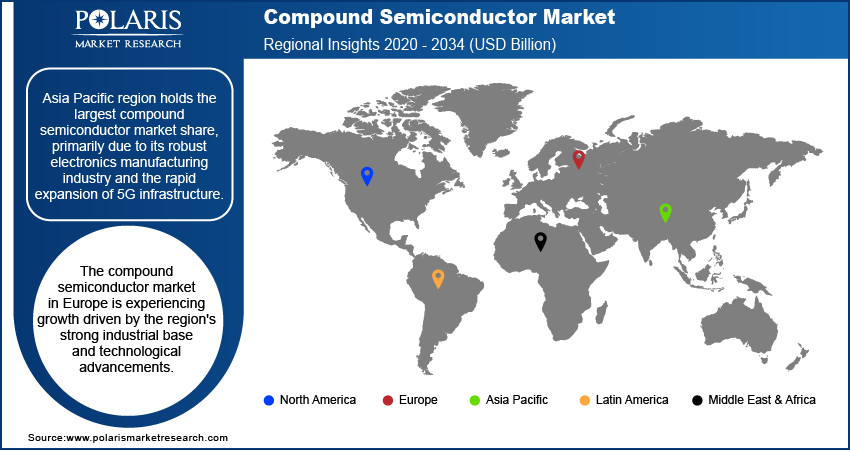

- Asia Pacific dominated the compound semiconductor market in 2025, accounting for 48.0% of total revenue, driven by strong electronics manufacturing and rapid 5G deployment.

- Europe is expected to register the fastest growth during 2026–2034 at a CAGR of 7.1%, supported by increasing investments in EVs, renewable energy, and semiconductor innovation.

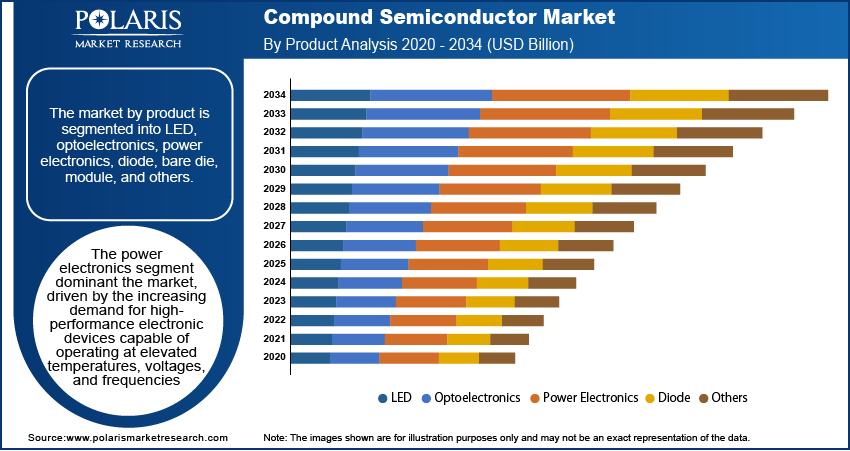

- The Power Electronics segment in 2025 held revenue share of 19.2%, owing to rising adoption of GaN and SiC devices in EVs and industrial applications.

- The Telecommunication segment held the largest market share of 22.4% in 2025, fueled by expanding 5G networks and growing demand for high-frequency RF components.

- The Power Electronics segment is projected to witness the fastest CAGR of 7.1% during 2026–2034, driven by increasing demand for energy-efficient power management solutions.

- Germany accounted for 25.6% of the European compound semiconductor market in 2025, supported by its strong automotive, industrial, and semiconductor manufacturing ecosystem.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations

Industry Dynamics

- Government funding and semiconductor support programs are driving compound semiconductor manufacturing and research activities globally.

- Growing electric vehicle adoption is increasing demand for silicon carbide semiconductors in automotive power electronics applications.

- Rising deployment of 5G networks is boosting demand for compound semiconductors in communication infrastructure equipment.

- High production costs and complex manufacturing processes are restricting compound semiconductor market growth to some extent.

AI Impact Compound Semiconductor Market

- AI infrastructure expansion is increasing demand for compound semiconductors in data centers and HPC systems.

- AI workloads need high-speed processors and energy-efficient computing hardware, supporting compound semiconductor usage.

- Growth in AI servers is increasing demand for GaN and SiC power semiconductor devices.

- Increasing AI computing deployments are supporting development of advanced compound semiconductor technologies

What are Compound Semiconductors?

Compound semiconductors are materials made by combining two or more elements from groups III-V or II-VI, such as GaN, GaAs, and SiC. They offer better electrical, thermal, and optical performance than silicon and are widely used in high-speed, high-power, and high-frequency applications across telecommunications, automotive, aerospace, and optoelectronics industries.

The compound semiconductor market is experiencing significant growth due to its wide-ranging applications in telecommunications, consumer electronics, automotive, and industrial sectors. These semiconductors, composed of elements from two or more different groups in the periodic table, offer superior electronic and optical properties compared to traditional silicon-based semiconductors. Key materials such as gallium arsenide (GaAs), gallium nitride (GaN), and silicon carbide (SiC) enable high-speed performance, energy efficiency, and enhanced thermal stability. The market is driven by the increasing demand for high-performance electronic devices, the expansion of 5G infrastructure, and the growing adoption of electric vehicles (EVs), which rely on compound semiconductors for efficient power management and fast charging capabilities. Additionally, advancements in optoelectronics, including laser diodes and photodetectors, are further accelerating market expansion.

Technological advancements and rising investments in semiconductor manufacturing is driving the growth of the market. The increasing preference for GaN and SiC in power electronics, due to their higher efficiency and durability, is influencing compound semiconductor market development. Moreover, the rapid expansion of data centers and high-frequency communication networks is driving the adoption of compound semiconductors in radio frequency (RF) and microwave applications. The ongoing research and development efforts aimed at improving manufacturing efficiency and reducing costs are expected to fuel the market growth during the forecast period.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Compound Semiconductors vs Silicon Semiconductors

| Parameter | Compound Semiconductors | Silicon Semiconductors |

| Material Type | Made from two or more elements (GaN, GaAs, SiC) | Made from silicon only |

| Efficiency | Higher power efficiency | Lower compared to compound semiconductors |

| Heat Resistance | Operates at higher temperatures | Lower thermal tolerance |

| Frequency Handling | Suitable for high-frequency applications | Limited at very high frequencies |

| Power Performance | Supports high-power operation | Better suited for moderate power levels |

| Switching Speed | Faster switching speeds | Slower switching speeds |

| Cost | Higher manufacturing cost | Lower manufacturing cost |

| Telecom Applications | Widely used in 5G, RF, and satellite systems | Limited use in high-frequency telecom |

| Automotive Applications | Preferred for EV power electronics and charging systems | Used in conventional automotive electronics |

| Optoelectronics | Commonly used in LEDs, lasers, and photonics | Less suitable for optoelectronic devices |

| High-Performance Computing | Supports energy-efficient AI and HPC systems | Used in general-purpose computing devices |

Source: Polaris Market Research Analysis

Market Dynamics

Government Initiatives and Funding

Government policies and financial support play a pivotal role in propelling the compound semiconductor market growth. In the US, the CHIPS and Science Act of 2022 allocated USD 52.7 billion to bolster domestic semiconductor manufacturing and research, aiming to improve supply chain resilience and technological leadership. This substantial investment underscores the government's commitment to advancing semiconductor technologies, including compound semiconductors. These initiatives reflect a global trend of governmental support for fostering innovation and expansion, thereby driving the market.

Expansion of Electric Vehicle Market

The automotive industry's shift towards electric vehicles (EVs) has created a substantial demand for compound semiconductors, particularly silicon carbide (SiC) devices. SiC semiconductors offer higher efficiency and durability in power electronics, which are essential for EV performance. The global push for sustainable transportation solutions has accelerated the adoption of EVs, thereby increasing the need for advanced semiconductor components. This trend highlights the symbiotic relationship between the growing EV market and the compound semiconductor industry.

Source: Polaris Market Research Analysis

Segment Insights

Market Assessment by Product

The compound semiconductor market segmentation, based on product, includes LED, optoelectronics, power electronics, diode, bare die, module, and others. The Power Electronics segment in 2025 held revenue share of 19.2%, driven by the increasing demand for high-performance electronic devices capable of operating at elevated temperatures, voltages, and frequencies. This segment's expansion is due to the rising adoption of electric vehicles (EVs), renewable energy systems, and advanced industrial applications. Compound semiconductors, such as gallium nitride (GaN) and silicon carbide (SiC), are pivotal in enhancing the efficiency and reliability of power electronic components, thereby driving the segmental growth in the market.

Market Evaluation by Application

The compound semiconductor market is segmented by application into general lighting, telecommunication, military/ defense & aerospace, automotive, power supply, datacom, consumer display, commercial, consumer devices, and others. The Telecommunication segment held the largest market share of 22.4% in 2025, driven by the escalating demand for high-speed data transmission and the global rollout of 5G networks. Compound semiconductors, such as gallium nitride semiconductor (GaN) and gallium arsenide (GaAs), are integral to the development of high-frequency, high-efficiency components essential for modern telecommunication infrastructure. These materials facilitate the creation of advanced radio frequency (RF) devices, including power amplifiers and switches, which are crucial for enhancing network capacity and reliability. The increasing reliance on wireless communication platforms, coupled with the necessity for higher bandwidths to support increasing mobile data usage, underscores the segment's prominence. The continuous evolution of telecommunication technologies, such as the transition to 5G, further amplifies the demand for compound semiconductors, solidifying the segment's substantial market share.

Source: Polaris Market Research Analysis

Regional Insights

By region, the study provides compound semiconductor market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific dominated the compound semiconductor market in 2025, accounting for 48.0% of total revenue, primarily due to its robust electronics manufacturing industry and the rapid expansion of 5G infrastructure. China's aggressive deployment of 5G networks, exemplified by the construction of approximately 3.22 million 5G base stations by October 2023, has significantly boosted the demand for compound semiconductors essential for high-speed data transmission and network efficiency. Additionally, the region's cost-effective manufacturing capabilities and the anticipated growth of the electronics sector contribute to its substantial market share.

The compound semiconductor market in Europe is expected to register the fastest growth during 2026–2034 at a CAGR of 7.1% driven by the region's strong industrial base and technological advancements. Germany accounted for 25.6% of the European compound semiconductor market in 2025, owing to its robust semiconductor manufacturing sector and extensive network of technology firms. The country's significant investments in research and development, particularly in the automotive and industrial sectors, have fostered innovation in high-tech industries. Germany's focus on electric vehicle production and renewable energy systems has further increased the demand for compound semiconductor products. Additionally, the United Kingdom is emerging as a notable player in the compound semiconductor industry. The UK government has recognized the strategic importance of semiconductors, with industry leaders advocating for substantial investment funds to establish a semiconductor "super cluster" and a National Semiconductor Institute, aiming to drive growth and job creation in the sector.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

The compound semiconductor market comprises several prominent companies actively contributing to its growth and innovation. Key players include Nichia Corporation, Samsung Electronics Co., Ltd., ams OSRAM AG, Qorvo, Inc., Skyworks Solutions, Inc., Wolfspeed, Inc., GaN Systems, Canon Inc., Infineon Technologies AG, Mitsubishi Electric Corporation, ON Semiconductor Corporation, NXP Semiconductors N.V., Broadcom Inc., Texas Instruments Incorporated, and Analog Devices, Inc.

These companies engage in continuous research and development to enhance the performance and efficiency of compound semiconductors, catering to diverse applications such as telecommunications, automotive, consumer electronics, and industrial sectors. For instance, Wolfspeed, Inc. specializes in silicon carbide (SiC) and gallium nitride (GaN) technologies, which are pivotal in electric vehicles and renewable energy systems. Similarly, Skyworks Solutions, Inc. focuses on advanced RF and mobile communication solutions, leveraging GaAs and GaN technologies to meet the increasing demand for high-performance RF components in consumer electronics and telecommunications.

Strategic collaborations and partnerships are common among these key players to strengthen their market positions and expand their technological capabilities. For example, Qorvo, Inc. established a strong presence in the telecommunications and defense sectors through its extensive portfolio of GaN-based RF amplifiers and integrated circuits. Additionally, companies such as Infineon Technologies AG and Mitsubishi Electric Corporation are investing in expanding their manufacturing capabilities to meet the growing demand for compound semiconductors across various industries. This dynamic and competitive landscape fosters continuous innovation, driving the evolution of the compound semiconductor market.

Wolfspeed, Inc. is a semiconductor company specializing in silicon carbide (SiC) and gallium nitride (GaN) technologies, which are essential for applications in electric vehicles, renewable energy, and telecommunications. The company has been expanding its manufacturing capabilities, including the development of a new facility in Chatham County, North Carolina, aimed at increasing SiC crystal production for electric vehicles.

Skyworks Solutions, Inc. focuses on analog and mixed-signal semiconductors, providing solutions for wireless communications, automotive, and industrial applications. The company offers products such as amplifiers, filters, and modulators, which are integral to wireless connectivity and communication systems.

List of Key Companies

- Analog Devices, Inc.

- ams OSRAM AG

- Broadcom Inc.

- Canon Inc.

- GaN Systems

- Infineon Technologies AG

- Mitsubishi Electric Corporation

- Nichia Corporation

- NXP Semiconductors N.V.

- ON Semiconductor Corporation

- Qorvo, Inc.

- Samsung Electronics Co., Ltd.

- Skyworks Solutions, Inc.

- Texas Instruments Incorporated

- Wolfspeed, Inc.

Compound Semiconductor Industry Developments

- May 2026: Integra Technologies launched the IGN1030S10000 GaN/SiC transistor, the industry's first single-device 10 kW L-Band transistor for high-power RF applications. (Source: compoundsemiconductor.net)

- February 2026: Navitas Semiconductor launched its 5th-generation GeneSiC TAP technology, featuring 1200V SiC MOSFETs for AI data centers, energy infrastructure, and industrial applications. (Source: navitassemi.com)

- January 2026: Wolfspeed achieved a 300mm SiC wafer technology breakthrough, supporting AI infrastructure, AR/VR devices, and advanced power electronics applications. (Source: wolfspeed.com)

- In August 2025, Rocket Lab increased its U.S. investments to enhance semiconductor production capacity and strengthen supply-chain resilience for space-grade solar cells and electro-optical sensors, backed by a $23.9 million award from the Trump Administration. (Source: rocketlabcorp.com)

- In May 2025, Malaysian chipmaker SMD Semiconductor launched a new R&D Innovation Hub in Wales, focused on partnering with UK organizations to develop next-generation semiconductor designs and accelerate collaborative technology advancement. (Source: smdsemiconductor.com)

Future Outlook

The compound semiconductor market is expected to grow steadily in the coming years. Expansion of 5G and upcoming 6G networks will support demand. Rising electric vehicle adoption will increase the use of SiC devices. Growing demand for energy-efficient electronics will further drive market growth. Advances in GaN and SiC technologies will expand applications across communication, mobility, AI, and computing systems.

Compound Semiconductor Market Segmentation

By Product Outlook (Revenue-USD Billion, 2021–2034)

- LED

- Optoelectronics

- Power Electronics

- Diode

- Bare Die

- Module

- Others

By Application Outlook (Revenue-USD Billion, 2021–2034)

- General Lighting

- Telecommunication

- Military/ Defense & Aerospace

- Automotive

- Power Supply

- Datacom

- Consumer Display

- Commercial

- Consumer Devices

- Others

By Type Outlook (Revenue-USD Billion, 2021–2034)

- GaN

- GaAs

- SiC

- INP

- SIGE

- GAP

- Others

By Regional Outlook (Revenue-USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest f Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- Suth Korea

- Indnesia

- Australia

- Vietnam

- Rest f Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- Suth Africa

- Rest f Middle East & Africa

- Latin America

- Mexic

- Brazil

- Argentina

- Rest f Latin America

Compound Semiconductor Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 49.20 billion |

| Market Size Value in 2026 | USD 52.27 billion |

| Revenue Forecast by 2034 | USD 87.45 billion |

| CAGR | 6.6% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

How is Report Valuable for Organization?

Workflow/Innovation Strategy: The compound semiconductor market has been segmented into detailed segments of product, application, and type. Moreover, the study provides the reader with a detailed understanding of the different segments at both the global and regional levels.

Growth/Marketing Strategy: Companies in the compound semiconductor market focus on expanding manufacturing capabilities, forming strategic partnerships, and investing in research and development to enhance product efficiency. Market players are strengthening their presence through mergers, acquisitions, and collaborations with end-user industries such as automotive, telecommunications, and consumer electronics. Additionally, businesses are leveraging government incentives and funding programs, such as the US CHIPS and Science Act, to boost domestic production. Marketing efforts emphasize the advantages of compound semiconductors in high-performance applications, including 5G networks, electric vehicles, and renewable energy systems. Expanding global distribution networks and targeting emerging economies further support market growth.

Compound Semiconductor Market FAQ's

The global Compound Semiconductor Market was valued at USD 49.20 billion in 2025 and is expected to reach USD 87.45 billion by 2034 from 2026 to 2034

The market is projected to register a CAGR of 6.6% during the forecast period, 2026-2034.

Asia Pacific dominated the compound semiconductor market in 2025, accounting for 48.0% of total revenue.

Key players include Nichia Corporation, Samsung Electronics Co., Ltd., ams OSRAM AG, Qorvo, Inc., Skyworks Solutions, Inc., Wolfspeed, Inc., GaN Systems, Canon Inc., Infineon Technologies AG, Mitsubishi Electric Corporation, ON Semiconductor Corporation, NXP Semiconductors N.V., Broadcom Inc., Texas Instruments Incorporated, and Analog Devices, Inc.

The Power Electronics segment in 2025 held revenue share of 19.2%.

A compound semiconductor is a type of semiconductor material made from two or more different elements, typically from groups III and V or groups II and VI of the periodic table.

A semiconductor material made from two or more different elements, typically from periodic table groups III–V or II–VI, offering superior electronic and optical properties over traditional silicon.

Key trends include rising 5G infrastructure expansion, growing electric vehicle adoption driving SiC and GaN demand, advancements in optoelectronics, and increasing government investments boosting semiconductor manufacturing globally.

Download Sample Report of Compound Semiconductor Market

Please fill out the form to request a customized copy of the research report.