Gallium Nitride Semiconductor Devices Market Size, Share Global Analysis Report, 2026-2034

REPORT DETAILS

Gallium Nitride Semiconductor Devices Market Summary

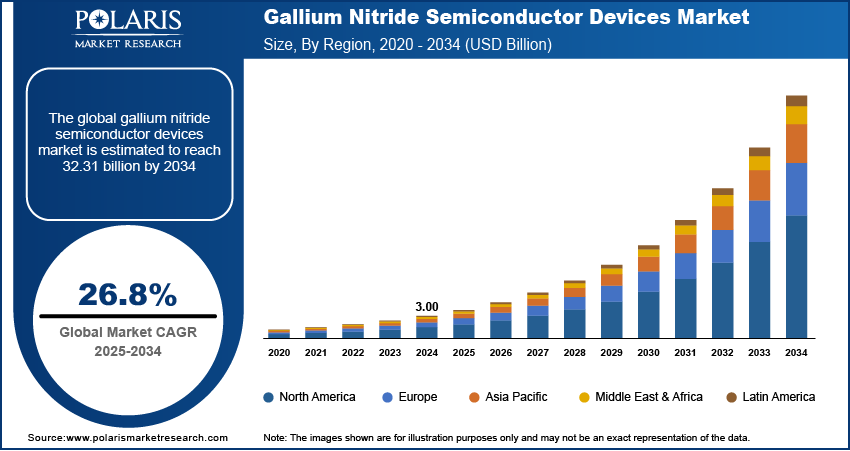

The gallium nitride semiconductor devices market was valued at USD 3.79 billion in 2025 growing at a CAGR of 26.8% from 2026-2034. Rising adoption of GaN devices in 5G communication systems and the expanding EV charging infrastructure are driving market growth.

Market Statistics

Key Takeaways

- Power semiconductors led the market in 2025 by 35.5% of global market due to widespread use in EVs, industrial automation, and energy-efficient power conversion.

- Aerospace & defense is expected to expand at the maximum CAGR of 27.5% from 2026 to 2034, led by increasing deployment of GaN-based communication & radar systems.

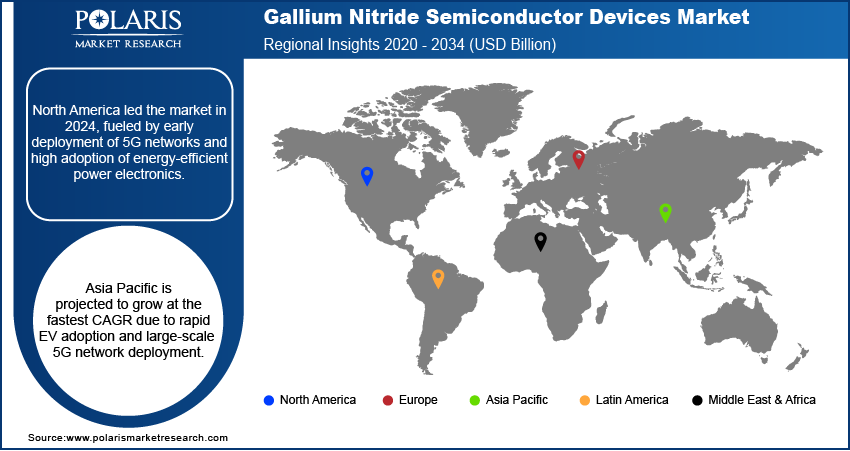

- North America led the market in 2025, with the largest revenue share of 35.75%. Owing to early 5G adoption and robust semiconductor manufacturing presence.

- The U.S. led North America in 2025 with 78.3% market share with advanced semiconductor infrastructure and high adoption of energy-efficient technologies.

- Asia Pacific is expected to register a CAGR of 27.6%, driven by rapid EV adoption and large-scale 5G deployment.

- China led Asia Pacific by holding 39.7% market share due to industrial growth and government incentives toward semiconductor manufacturing and EV infrastructure.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Increasing use of GaN devices in 5G communications systems is driving demand across telecom infrastructure.

- Growth in EV and charging infrastructure is fueling the demand for high-efficiency GaN power devices.

- Huge material and manufacturing costs are restraining large-scale commercialization of GaN semiconductors.

- GaN-on-Silicon and power IC technology advancements are creating new market opportunities.

What are Gallium Nitride Semiconductor Devices?

Gallium nitride (GaN) semiconductor devices are new-generation electronic devices used for high-power, high-frequency, and energy-saving applications in the communication, automotive, and industrial markets. For instance, in July 2025, Renesas released three 650V Gen IV Plus GaN FETs for dense power conversion in AI data centers, industrial systems, and charging, with enhanced efficiency and thermal performance. These devices provide high performance in 5G base stations, RF systems, electric vehicles, and data centers with high switching efficiency and small size.

Growing 5G network deployments, increasing EV infrastructure, and rising usage of energy-efficient power electronics are fueling demand for GaN-based devices globally. Industries are turning towards GaN solutions in order to attain higher signal transmission speed, less energy loss, and enhanced thermal performance.

Source: Polaris Market Research Analysis

Major manufacturers are concentrating on creating GaN-on-Silicon and GaN-on-Diamond technologies to make their products more scalable and cost-effective. Ongoing innovation, coupled with increasing investments in semiconductor manufacturing and renewable energy integration, is driving robust growth opportunities for GaN semiconductor device providers.

Drivers & Opportunity

Adoption of GaN in 5G Communication Systems: Increasing use of GaN devices in 5G communication systems is driving demand in telecom and RF infrastructure. 5G Americas and Omdia released that the number of global 5G connections crossed 2.6 billion in Q2 of 2025, growing 32% year-on-year, and are likely to reach close to 9 billion in 2030, constituting 60% of all wireless connections. GaN components support high-frequency operation with reduced power loss and smaller size. GaN-based RF amplifiers are utilized by network operators for extending support to mmWave and massive MIMO technologies. This is fueling greater deployment of GaN semiconductors in future communication systems.

Expanding Penetration of Electric Vehicles and EV Charging Infrastructure: Wider adoption of electric vehicles and EV charging equipment is driving demand for high-efficiency GaN power devices. According to International Energy Agency (IEA), worldwide electric car sales totaled over 17 million in 2024, up over 25%, with the 3.5 million increases from 2023 exceeding EV sales in 2020. GaN allows for faster switching, increased energy efficiency, and minimized system size in inverters and chargers. Automotive firms are incorporating GaN devices into onboard chargers and powertrains. This is helping to drive the adoption of GaN technology in the electric mobility space.

Source: Polaris Market Research Analysis

Segmental Insights

Component Analysis

Based on component, the segmentation includes transistor, diode, rectifier, power IC, supply and inverter, amplifiers, lighting and laser, switching systems, and other components. The transistor segment led the market during 2025 by 36.6% share due to its efficiency and extensive use in communication systems, RF amplifiers, and power conversion. Robust uptake in the telecom, automotive, and industrial markets continues to keep it leading across the globe.

The power IC segment is anticipated to expand at the highest CAGR in the forecast period based on rising integration in EV chargers, data centers, and renewable energy systems. The growth in demand for power management solutions that are smaller and high in efficiency is driving the use of power ICs in various applications.

Product Analysis

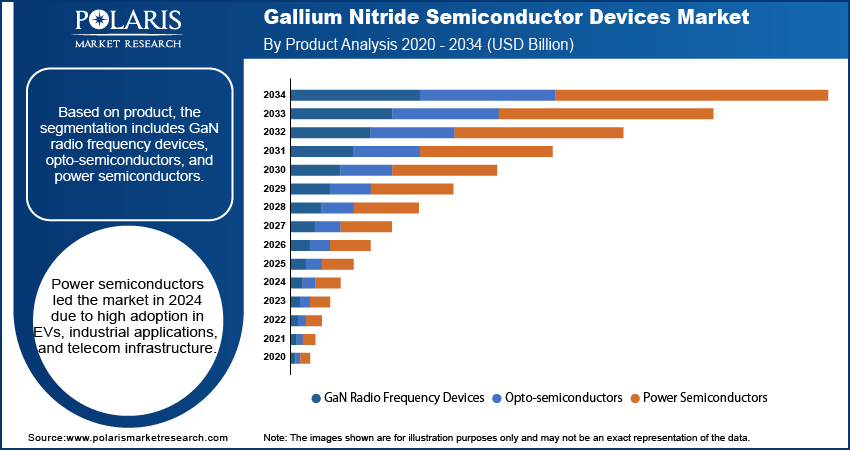

Based on product, the segmentation includes GaN radio frequency devices, opto-semiconductors, and power semiconductors. Power semiconductors led the market in 2025 by 35.5% owing to its energy-efficient power conversion. Universal implementation in EVs, industrial automation, and telecom infrastructure further establishes its market dominance.

GaN RF devices is expanding at the highest growth rate over the forecast period owing to its deployment in 5G base stations, radar systems, and high-frequency wireless networks. Their growing demand for high-frequency, low-loss, and energy-efficient components is boosting their speedy adoption.

Wafer Size Analysis

Based on wafer size, the segmentation includes 2-inch, 4-inch, 6-inch, and 8-inch. The 6-inch wafer is leading segment in 2024 driven by its cost efficiency, manufacturing yield, and compatibility with high-volume GaN device production. 6-inch wafers are favored by manufacturers for mass market applications in power electronics and RF systems. Innoscience launched four 700V SolidGaN power devices with up to 50% better efficiency and high-frequency switching capability for 1–6 kW applications in August 2025.

The 8-inch wafer segment is expected to exhibit the highest growth due to growing requirement for large-scale GaN device manufacturing. Improved efficiency in high-power applications is promoting the adoption of 8-inch wafers in industrial and automotive applications.

Wafer Size Comparison

| Parameter | 2-inch | 4-inch | 6-inch | 8-inch |

| Market Position | Early-stage / niche | Transitional | Dominant | Fastest-growing |

| Cost Efficiency | Low initial cost, high per-unit cost | Moderate | Balanced, optimized | Lowest per-unit at scale |

| Manufacturing Scale | Very limited | Limited | High-volume capable | Large-scale / mass production |

| Yield Efficiency | Low | Moderate | High | Very high |

| Technology Maturity | Mature but outdated for scale | Improving | Widely adopted | Emerging advanced node |

| Key Applications | R&D, prototyping | Small RF, pilot lines | EVs, power electronics, telecom | Automotive, industrial, high-power |

| Business Advantage | Easy entry, low capex | Process stability | Cost-performance balance | Scale + long-term cost reduction |

| Growth Outlook | Declining | Stable | Leading segment | Highest Growth |

| Market Insight | Limited commercial use | Gradual shift to larger wafers | Preferred for mass applications | Driven by scaling manufacturing |

Source: Polaris Market Research Analysis

End User Analysis

Based on end user, the segmentation includes aerospace & defense, automotive, consumer electronics, healthcare, information & communication technology, industrial & power, and other end user. The automotive industry led the market during the year 2025, owing to mass adoption of EVs and incorporation of GaN devices in inverters, onboard chargers, and powertrains. The transition towards energy-efficient and high-performance EVs is also stimulating market growth.

Aerospace & defense is expected to expand at the maximum CAGR of 27.5% over the forecast period as a result of rising deployment of GaN-based electronic warfare systems, satellite communication, and radar. Advanced aerospace and growing defense modernization programs are contributing to the high demand for GaN devices.

Source: Polaris Market Research Analysis

Regional Analysis

North America led the market in 2025, with the largest revenue share of 35.75% due to the early adoption of GaN devices for 5G communication infrastructure to enable high-frequency and energy-saving telecom systems. In October 2025, Alpha and Omega Semiconductor offers SiC and GaN power solutions to enable 800 VDC power architecture for future AI data centers to enhance efficiency and lower cooling and maintenance costs. Furthermore, the availability of leading semiconductor manufacturers spurs innovation and mass deployment.

The U.S. Gallium Nitride Semiconductor Devices Market Insights

The U.S. led North America in 2025 with 78.3% due to early deployment of 5G infrastructure and high demand for RF and power electronics. Moreover, strong presence of semiconductor manufacturers fosters innovation. In addition, government funding for EV and defense projects is supporting growth.

Europe Gallium Nitride Semiconductor Devices Market Insights

Europe holds the substantial market share, fueled by growing penetration of GaN devices in auto and renewable energy segments in Germany and France. For example, in May 2025, Infineon introduced radiation-hardened GaN transistors with CoolGaN technology, qualified for space applications, for high-efficient satellite and deep-space solutions. Moreover, government policies encouraging energy-efficient power electronics are driving adoption.

Asia Pacific Gallium Nitride Semiconductor Devices Market Insights

Asia Pacific is expected to register a CAGR of 27.6%,due to rapid adoption of electric vehicles and expansion of EV charging infrastructure across China and Japan. Moreover, growing deployment of 5G networks in India and South Korea is increasing demand for high-performance GaN devices. In addition, rising industrial automation is contributing to market expansion.

China Gallium Nitride Semiconductor Devices Market Insights

China is driving market growth with rapid expansion of EV infrastructure and increasing industrial automation. Additionally, mass 5G network deployment is driving demand for high-frequency GaN devices in increasingly greater volumes. According to the China Ministry of Industry and Information Technology (MIIT), as of November 2024, China had 4.19 million 5G base stations, 5G utilized in 74 out of 97 priority economic sectors, and more than 15,000 "5G+ industrial internet" projects leading to smarter, greener production.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The gallium nitride (GaN) semiconductor devices market is moderately competitive, with firms improving device performance by leveraging GaN-on-Silicon technology, high-efficient power ICs, and state-of-the-art RF and power electronics solutions. Partnership with telecom operators, automobile OEMs, and industrial integrators also increases market penetration and adoption worldwide.

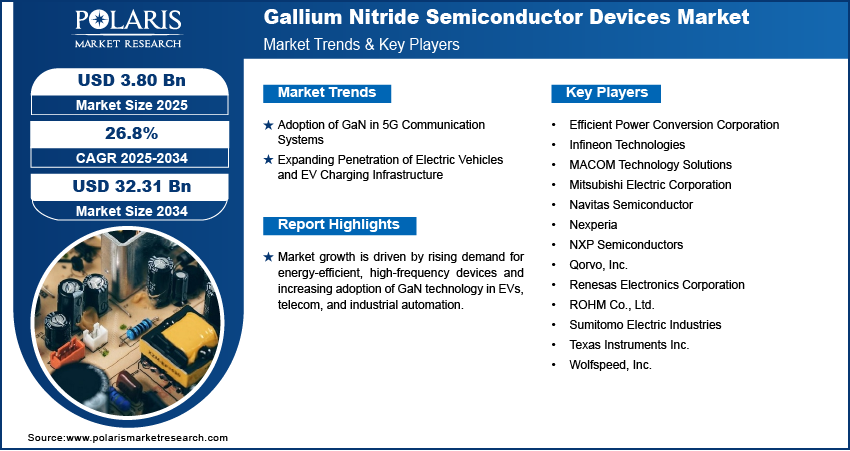

Key players in the market for gallium nitride semiconductor devices are Wolfspeed, Inc., Qorvo, Inc, MACOM Technology Solutions, Infineon Technologies, Sumitomo Electric Industries, Navitas Semiconductor, Efficient Power Conversion Corporation, Nexperia, NXP Semiconductors, ROHM Co., Ltd., Mitsubishi Electric Corporation, Renesas Electronics Corporation, and Texas Instruments Inc.

Key Players

- Efficient Power Conversion Corporation

- Infineon Technologies

- MACOM Technology Solutions

- Mitsubishi Electric Corporation

- Navitas Semiconductor

- Nexperia

- NXP Semiconductors

- Qorvo, Inc.

- Renesas Electronics Corporation

- ROHM Co., Ltd.

- Sumitomo Electric Industries

- Texas Instruments Inc.

- Wolfspeed, Inc.

Industry Development

- March 2026 – Indra Group (GIGaNTE project) started developing GaN-based chips for high-power electronics, radar, and EV uses. The focus is on scaling production and future deployment. Source: indragroup.com

- February 2026 – ROHM Co., Ltd. expanded GaN power device supply by using Taiwan Semiconductor Manufacturing Company technology to develop an integrated production setup. Focus is on AI servers and EV applications. Source: digitimes.com

- October 2025: Imec has initiated a 300mm GaN program aimed at creating advanced, cost-effective power devices and speeding up semiconductor innovation. Source: imec-int.com

Future of GaN Semiconductor Devices Market

The market is expected to grow fast due to rising EV adoption and need for high-efficiency power devices. Expansion of 5G networks is increasing demand for GaN in RF and telecom infrastructure. There is growing use of energy-efficient electronics in consumer and industrial applications. Advancements in GaN-on-silicon technology are supporting reduce costs and improve scalability. Increasing semiconductor manufacturing capacity is also helping larger adoption of GaN devices.

Gallium Nitride Semiconductor Devices Market Segmentation

By Component (Revenue, USD Billion, 2021–2034)

- Transistor

- Diode

- Rectifier

- Power IC

- Supply and Inverter

- Amplifiers

- Lighting and Laser

- Switching Systems

- Other Components

By Product (Revenue, USD Billion, 2021–2034)

- GaN Radio Frequency Devices

- Opto-semiconductors

- Power Semiconductors

By Wafer Size (Revenue, USD Billion, 2021–2034)

- 2-inch

- 4-inch

- 6-inch

- 8-inch

By End User (Revenue, USD Billion, 2021–2034)

- Aerospace & Defense

- Automotive

- Consumer Electronics

- Healthcare

- Information & Communication Technology

- Industrial & Power

- Other End User

By Region (Revenue, USD Billion, 2021–2034)

- North America

- The U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherland

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

- Latin America

- Saudi Arabia

- UAE

- South Africa

- Israel

- Rest of South Africa

Gallium Nitride Semiconductor Devices Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 3.79 Billion |

| Market Size in 2026 | USD 4.80 Billion |

| Revenue Forecast by 2034 | USD 32.13 Billion |

| CAGR | 26.8% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2026-2034 |

| Forecast Period | 2026-2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions and segmentation. |

Source: Polaris Market Research Analysis

Gallium Nitride Semiconductor Devices Market FAQ's

The global market size was valued at USD 3.79 billion in 2025 and is projected to grow to USD 32.13 billion by 2034.

The global market is projected to register a CAGR of 26.8% during the forecast period.

North America led the market in 2025, with the largest revenue share of 35.75% due to early 5G adoption and a strong semiconductor manufacturing base.

A few of the key players in the market are Wolfspeed, Inc., Qorvo, Inc, MACOM Technology Solutions, Infineon Technologies, Sumitomo Electric Industries, Navitas Semiconductor, Efficient Power Conversion Corporation, Nexperia, NXP Semiconductors, ROHM Co., Ltd., Mitsubishi Electric Corporation, Renesas Electronics Corporation, and Texas Instruments Inc.

Power semiconductors led the market in 2025 by 35.5% owing to widespread use in EVs, industrial automation, and energy-efficient power conversion.

Aerospace & defense is expected to expand at the maximum CAGR of 27.5% from 2026 to 2034, driven by rising deployment of GaN-based radar, satellite communication, and electronic warfare systems.

GaN (Gallium Nitride) is a semiconductor material. It functions at higher voltage, frequency, and temperature than silicon. Silicon is cheaper and largely used, but GaN is more efficient and faster.

Higher efficiency, less heat generation, compact size, and better performance in high-frequency operations.

Automotive (EVs), telecom (5G), consumer electronics, industrial equipment, aerospace & defense, and renewable energy systems.

Download Sample Report of Gallium Nitride Semiconductor Devices Market

Please fill out the form to request a customized copy of the research report.