Copper Mining Market Growth Opportunities, Industry Revenue, 2026-2034

REPORT DETAILS

Copper Mining Market Summary

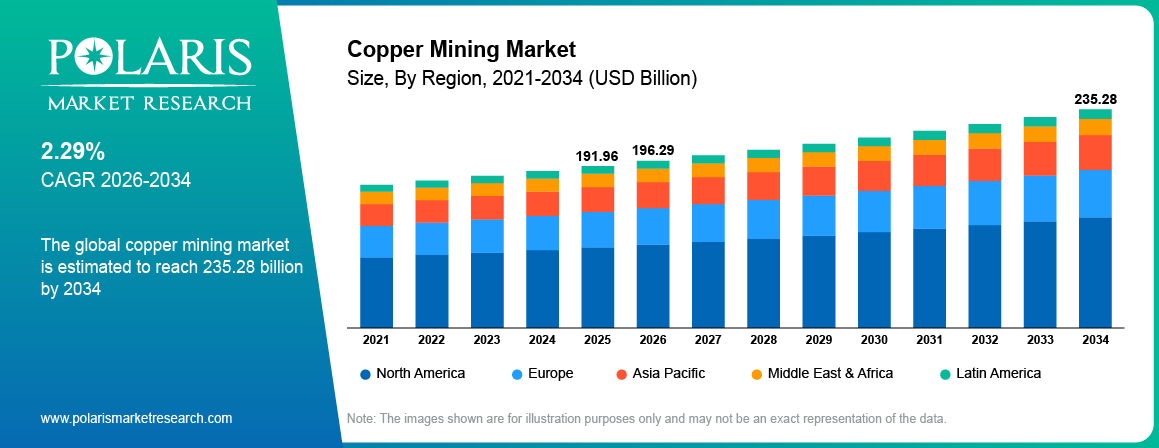

The global copper mining market is estimated around USD 191.96 Billion in 2025, with consistent growth anticipated during 2026–2034. This growth is driven by rising electrification trends and renewable energy expansion that are increasing demand for copper across global markets. The market is projected to grow at a CAGR of 2.29% during the forecast period.

Market Statistics

Key Takeaways

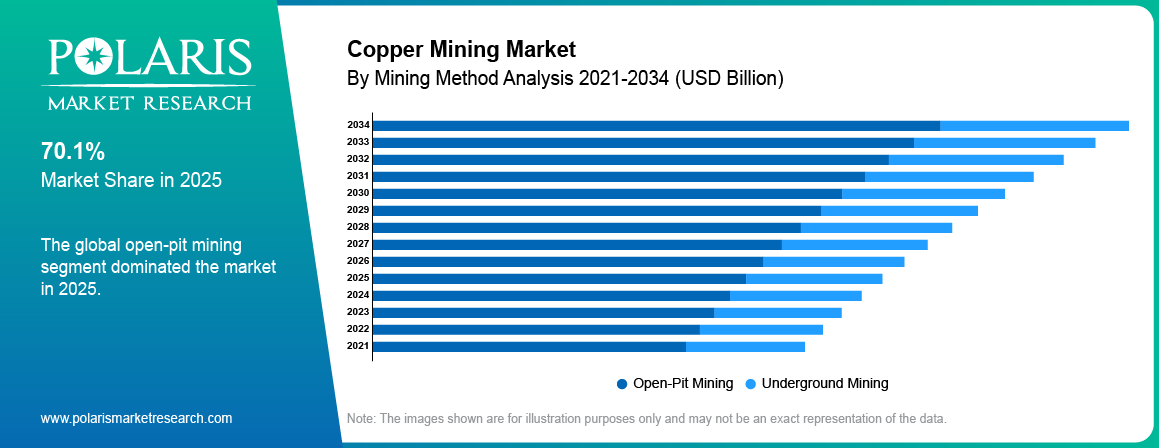

- Open-pit mining sector was dominant in 2025, accounting for nearly 57.40% market share due to cost-effective extraction of ore on a large scale.

- Electrical and electronics sector dominated in 2025, contributing approximately 41.60% market share due to high demand for wiring, motors, and power equipment.

- Underground mining segment is projected to grow at a CAGR of around 8.90% during the forecast period due to increasing demand for deeper mineral extraction and improved underground mining technologies.

- Transportation segment is expected to record the highest growth rate, registering a CAGR of around 10.60% during the forecast period due to increasing demand for efficient mobility solutions and rising adoption of advanced transportation technologies.

- Growing investment in EV production and power infrastructure improves demand visibility and supports scalable growth in the copper mining market.

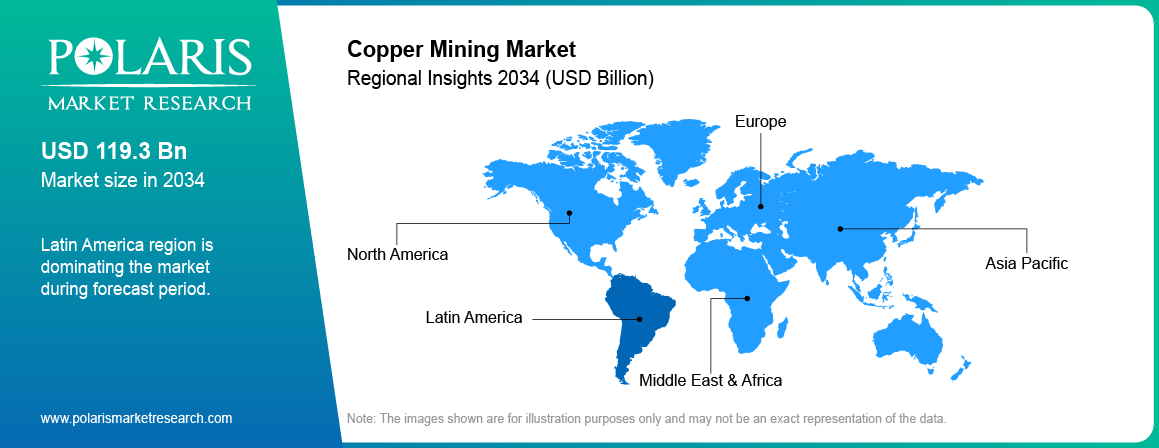

- Latin America dominated the market, accounting for nearly 45.30% market share in 2025 due to large reserves and strong production capacity.

Industry Dynamics

- Rising usage of electric vehicles increases the demand for copper in batteries, motors, and chargers.

- Renewable energy projects have resulted in the increasing usage of copper in power grids and power systems.

- Decreased ore quality and environmental legislation affect market growth in certain areas.

- Recycling integration and digital mining technologies are driving force behind significant market growth for copper mining industry.

What is Copper Mining?

Copper mining is the process through which copper ore is mined, extracted, and processed into copper metal that is applied in electric wiring, building and construction purposes, transportation, electronic devices, and renewable energy facilities. Copper is among the most significant industrial metals due to its conductivity, durability, and recyclability. Copper is used in electric cables, machines, plumbing, transformers, and other industrial purposes. Copper mining is experiencing growth owing to rising electrification and infrastructure development.

The value chain of the copper mining industry involves exploration operations, mine development, mineral excavation, grinding, concentration, smelting, refining, and delivery to consumers and industries. The goal of this industry is to ensure stable ore supply, improved recovery rates, lower production costs, and sustainable mining operations. Demand from electric vehicles, battery systems, grid modernization, and renewable energy projects is encouraging investment in new mines and capacity expansion. Strong copper consumption trends are supporting long-term market growth.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The development of the market started with high demand in the construction and electrical markets where copper are used in wiring and building structures. With the development of the economy and more industrialized and urban environments, demand grew further due to higher consumption of metals in the emerging economies. In the next phase, the market is projected to experience a shortage as the demand expected to exceed the supply due to the growing use of copper in EVs and renewable energies and low mining activities.

Drivers & Opportunities

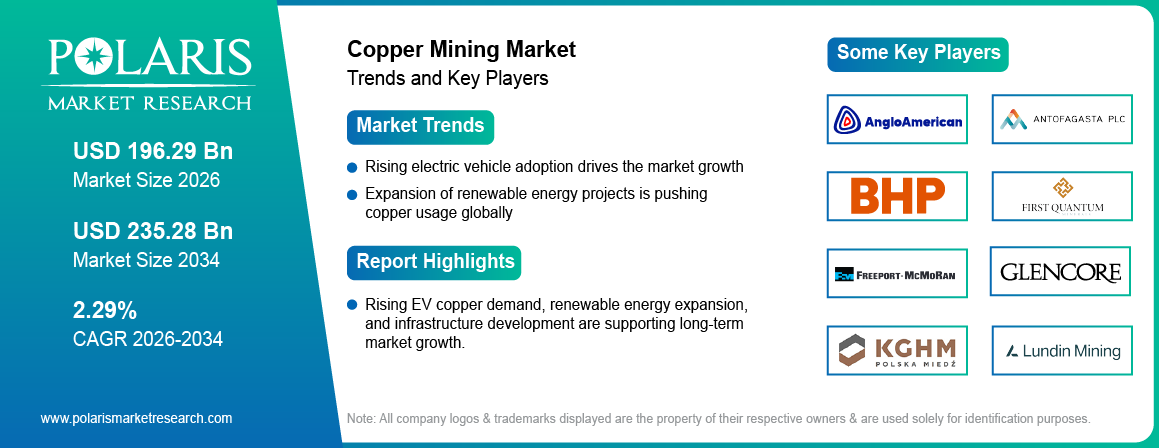

Rising electric vehicle adoption is increasing copper demand across battery and powertrain systems: There are increasing amounts of copper in electric vehicles compared to normal cars due to its batteries, wiring harnesses, inverters, and chargers. According to the International Energy Agency, there are more than 17 million sales of electric vehicles globally in 2024, representing over 20% of the market, while the increase of 3.5 million from the previous year was greater than the total number of electric cars sold globally in 2020.[Source: www.iea.org] Higher production of electric vehicles in China, Europe, and the US is causing rising trends of copper usage.

Expansion of renewable energy projects is supporting higher copper usage globally: The wind farms, solar farms, battery energy storage systems, and grids that carry all this energy are reliant on large amounts of copper as a means of generating electricity. According to International Energy Agency, the global renewable electricity generation capacity is expected to reach 4,600 GW during the period of 2025 to 2030. It is expected to be double compared to the previous five years from 2019 to 2024.[Source: www.iea.org] The government is investing more in renewable energy, which has led to high demand for copper mining.

Restraints & Challenges

Declining ore grades are increasing production costs and operational pressure: Many older copper mines have lower ore grades, resulting in less recovery of metal from each ton of ore that is mined. Mining firms require more money to mine deeper, process the ores, and handle the larger amounts of ore mined.

Environmental regulations are slowing mine approvals and expansions: Copper mining projects face strict rules related to water usage, emissions, land impact, and waste disposal. As per U.S. Environmental Protection Agency, if copper concentrations exceed 1.3 ppm in more than 10% of sampled customer taps, water systems must take additional corrosion control actions.[Source:www.epa.gov] Delays in permits and compliance costs are affecting project timelines in several producing regions. This creates pressure on future supply availability.

Opportunity

Recycling integration presents strong growth opportunities for copper supply security: Recycled copper consumes less energy than newly mined one, and helps realize the concept of the circular economy. In April 2026, Amermin and Ulterra Drilling Technologies extended their recycling cooperation agreement for the extraction of copper and other critical minerals from waste flows worldwide to ensure the sustainable copper supplies. More manufacturers and smelters now utilize scrap copper, thus reducing their reliance on newly mined copper as it generates additional revenues at all stages.

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the copper mining market mining method and application to help readers identify the fastest expanding and most attractive demand segments.

By Mining Method

-

Open-Pit Mining

Open-pit mining sector was dominant in 2025, accounting for nearly 57.40% market share due to cost-efficiency and capability to extract ore from relatively shallow deposits in large quantities. Major copper producing countries prefer this method for large-scale operations and stable output. Rising production needs are supporting growth of this segment.

-

Underground Mining

Underground mining segment is projected to grow at a CAGR of around 8.90% during the forecast period due to depletion of near-surface reserves and rising development of deeper ore bodies. For instance, in January 2026, Hindustan Copper Ltd., began underground mining in Jharkhand to boost the production of copper ore domestically. Mining firms are adopting state-of-the-art machinery and automation to ensure higher efficiency. There is an increasing emphasis on high-grade ores, aiding the growth of this category.

By Application

-

Electrical & Electronics

Electrical and electronics sector dominated in 2025, contributing approximately 41.60% market share due to the extensive use of copper in electrical wiring, circuit boards, motors, and power generation equipment. Copper is highly crucial for its conductivity and reliability, and hence continues to be a key material in electrical and electronic applications.

-

Transportation

Transportation segment is expected to record the highest growth rate, registering a CAGR of around 10.60% during the forecast period owing to an increase in the production of electric vehicles and investments in charging facilities. Increasing use of copper is expected within the electric vehicle components such as batteries, motors, and cables.

Source: Polaris Market Research Analysis

Regional Analysis

Latin America Market Assessment

Latin America dominated the market, accounting for nearly 45.30% market share in 2025, owing to high reserves of copper and existing infrastructure for mining purposes. Chile was seen as an important market in the region after Peru, as both countries have good mining capacities and export network facilities. According to National Institute of Statistics Chile, the copper production in Chile increased from 500.982 thousand tonnes in December 2021 to 540.221 thousand tonnes in December 2025.[Source: tradingeconomics.com] Growth is likely due to the development of mining projects and the demand for copper.

Asia Pacific Copper Mining Market Insights

Asia Pacific is projected to register the fastest CAGR during the forecast period, fueled by strong copper consumption in China and India. China’s Ministry of Industry and Information Technology shows that China expects to expand its copper ore reserves by between 5% and 10% by 2027.[Source: english.scio.gov.cn] This is part of a collaborative policy document from 11 different government departments that seeks to improve the recovery process of copper ore recycling. China continues to be the biggest market for copper ore due to its industrial sector, energy sector, and EV industry.

North America Copper Mining Market Overview

North America region had a substantial market share, owing to the availability of modern mining technology and production capabilities. In addition, the US and Canada are among the important regions where the market focuses on the adoption of automation, efficiency, and sustainable mining processes. For example, in April 2026, Mariana Minerals & Sandvik entered into a partnership for deploying autonomous mining operations in a US copper mine. Investments in the development of metal supply chains are fueling the growth of the market.

Europe Market Insights

Europe has significant market share owing to the high demand for industrial copper usage in the automobile, energy, and electronics industries. According to statistics provided by Eurostat, the amount of renewable energy sources in terms of final gross energy consumption in the EU increased from 9.6% in 2004 to 16.7% in 2013 and 24.6% in 2023, whereas the goal is to reach 42.5% in 2030.[Source: ec.europa.eu] Moreover, Europe relies on imports to provide its raw materials demands.

Source: Polaris Market Research Analysis

Competitive Landscape & Key Players

The copper mining industry is moderately concentrated, and its competition involves mining corporations from all over the world, regional miners, and integrated metal processors. The essential elements of success in the industry include the quality of mineral deposits, size of production, cost-effectiveness, and reliable production capacity. Investment in mining facilities, sustainable business activities, and innovative technology extraction techniques are among the key growth drivers.

Among the major companies operating in this industry are BHP Group, Rio Tinto Group, Freeport-McMoRan Inc., Glencore, Anglo American plc, Southern Copper Corporation, Antofagasta plc, First Quantum Minerals, KGHM Polska Miedź S.A., Teck Resources Limited, Vale S.A., Lundin Mining Corporation, and others.

Strategic Initiatives

- Expansion of existing mining operations to increase output capacity.

- Mergers and acquisitions to strengthen reserves and market position.

- Investment in digital mining technologies to enhance productivity.

- Emphasis on ESG compliance as well as sustainability efforts.

Premium Insights

The demand-supply gap for copper mines is predicted to be significant over the next ten years. Due to the rise in demand resulting from electrification, renewable energy sources, and the use of electric vehicles, demand will outstrip supply, leading to a potential shortage of copper by 2030.

Demand from electric vehicles is likely to contribute significantly to growing consumption as electric vehicles consume higher quantities of metals. The trend is putting increasing pressure on global copper supplies.

Recycling is essential in meeting future supply deficits. Recycling is becoming significant as companies try to stabilize their supplies, reduce energy, and minimize reliance on production from mining operations.

Key Players

- Anglo American plc

- Antofagasta plc

- BHP Group

- First Quantum Minerals

- Freeport-McMoRan Inc.

- Glencore

- KGHM Polska Miedź S.A.

- Lundin Mining Corporation

- Rio Tinto Group

- Southern Copper Corporation

- Teck Resources Limited

- Vale S.A.

Industry Developments

- April 2026: The Ivanhoe Mines successfully achieved the milestones required for the expansion of the Platreef project, thus enabling greater production of copper in the future. [source: www.ivanhoemines.com]

- April 2026: ABB received an order for the Eva Copper Mine Project in Australia, which involved supplying state-of-the-art grinding technology for improved copper production. [source: new.abb.com]

Copper Mining Market Segmentation

By Mining Method Outlook (Revenue, USD Billion, 2021-2034)

- Open-Pit Mining

- Underground Mining

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Electrical & Electronics

- Construction

- Transportation

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Copper Mining Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 191.96 Billion |

| Market Size in 2026 | USD 196.29 Billion |

| Revenue Forecast by 2034 | USD 235.28 Billion |

| CAGR | 2.29% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Copper Mining Market FAQ's

The global market size was valued at USD 191.96 Billion in 2025 and is projected to grow to USD 235.28 Billion by 2034.

Latin America dominated the market, accounting for nearly 45.30% market share in 2025 due to large copper reserves, strong production capacity, and established mining infrastructure.

Major applications include electrical wiring, electronics, construction materials, transportation equipment, and renewable energy systems.

A few of the key players in the market are BHP Group, Rio Tinto Group, Freeport-McMoRan Inc., Glencore, Anglo American plc, Southern Copper Corporation, Antofagasta plc, First Quantum Minerals, KGHM Polska Mied? S.A., Teck Resources Limited, Vale S.A., Lundin Mining Corporation, and others.

Key drivers include rising EV adoption, renewable energy expansion, grid modernization, and growing infrastructure investment.

Major demand comes from electrical & electronics, construction, transportation, industrial equipment, and energy sectors.

The market outlook remains positive due to electrification trends, clean energy investment, and rising recycling integration.

Download Sample Report of Copper Mining Market

Please fill out the form to request a customized copy of the research report.