C-Beauty Products Market Size & Trends, Forecast 2026-2034

REPORT DETAILS

C-Beauty Products Market Summary

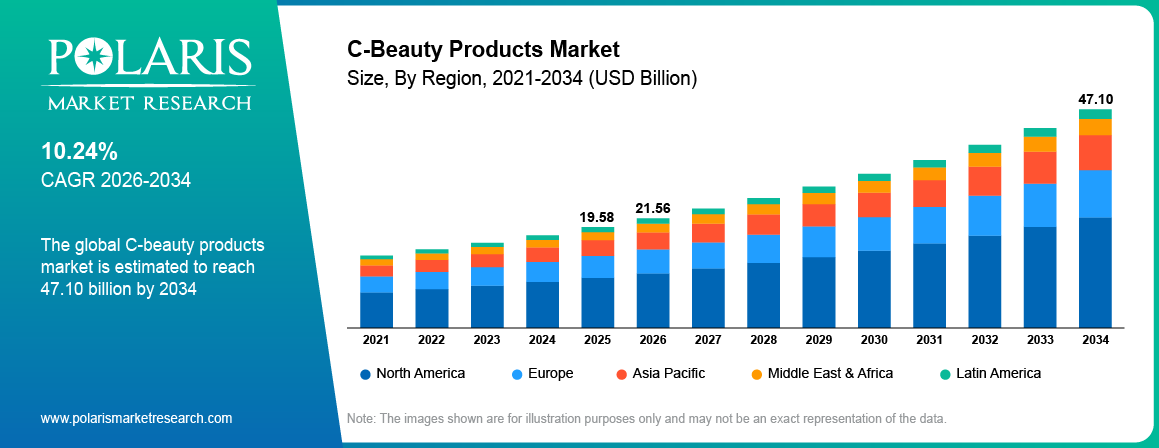

The global C-beauty products market is estimated around USD 19.58 Billion in 2025,?with consistent growth anticipated during 2026–2034. Growth is driven by digital commerce expansion and rising middle-class spending that are increasing demand for C-beauty products across globe. The industry is projected to grow at a CAGR of 10.24% during the forecast period.

Market Statistics

Key Takeaways

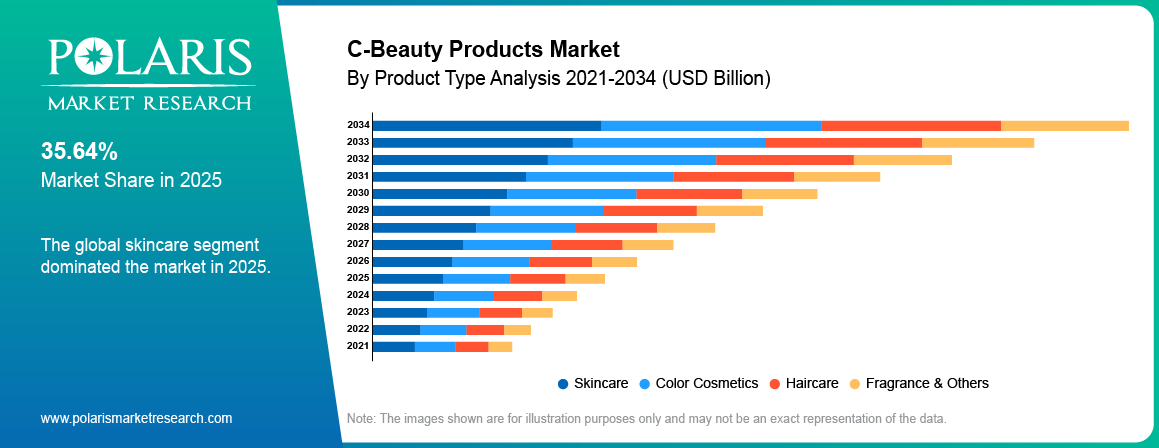

- Skincare category took the lead in 2025, accounting for nearly 36.50% market share due to the high demand for regular use and premium products.

- Online retail category was dominant in 2025, contributing approximately 39.80% market share owing to the fast-growing popularity of online sales and social commerce.

- Color cosmetics category is expected to grow at a CAGR of around 9.70% due to rising consumer demand for trendy cosmetic products.

- Companies are focusing on expanding portfolios across skincare, makeup, and personal care categories.

- Increasing AI-based innovations and launches of clean beauty products increase the attractiveness of C-beauty products.

- China held the largest share, accounting for nearly 42.60% share in 2025 due to strong domestic demand and digital commerce leadership.

Industry Dynamics

- Growing prevalence of digital business models will accelerate sales of such companies.

- Growth in the purchasing power of the middle class will boost the demand for affordable premium beauty goods.

- Stringent regulatory frameworks are increasing compliance pressure for manufacturers.

- AI-powered skincare and clean beauty trends are creating new growth opportunities.

What is C-beauty products?

C-beauty refers to beauty and personal care products created, branded, and sold by Chinese companies across skincare, makeup, haircare, and personal wellness categories. Such brands emphasize localization in terms of customer tastes, modern packaging, swift product launches, and high levels of social media engagement. Domestic cosmetic brands have started gaining popularity domestically and internationally, owing to their cost-effective nature and innovation-based on trends. Personalized cosmetics have been increasingly favored in recent times.

The supply chain of the C-beauty products market includes ingredient sourcing, product formulation, packaging, manufacturing, digital marketing, e-commerce distribution, and retail sales. The industry aims to deliver fast product development, competitive pricing, and strong consumer reach through online channels. Platforms such as Douyin, Tmall, JD.com, and Xiaohongshu are helping domestic brands China expand visibility and sales. Rapid growth in the skincare sector in China has been driving the development of new brands and product range extension.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The development began with the launch of mass-market personal care goods and subsequently proceeded towards luxury skincare and cosmetics. The rising demand was attributed to the growing preference for locally branded products among Chinese consumers. The industry is evolving towards premium, clean beauty, and international markets. Firms are emphasizing innovation, social media engagement, and overseas sales as key drivers of digital beauty success.

Drivers & Opportunities

Digital commerce dominance is accelerating sales growth of C-beauty brands: China boasts one of the most advanced digital retail systems for cosmetics. As per the National Bureau of Statistics of China, China’s total online retail sales of commodities and services grew by 9.2% year-on-year during January and February 2026.[Source: english.www.gov.cn]Digital commerce, social media marketing, and m-commerce are making the discovery and purchase process easier and better. Through platforms like Douyin, Tmall, and Xiaohongshu, brands are launching their products faster and attracting more young customers.

Rising middle-class consumption is increasing demand for premium affordable products: Growing disposable incomes have positively influenced the spending behavior of consumers who prefer purchasing more skincare, cosmetics, and personal care items. As per estimates by Mastercard, the largest middle-class growth is estimated to witness in Asia Pacific region, with projected to hit 3.2 billion people out of 5 billion middle-class consumers in the world by 2035.[Source: www.mastercard.com]The C-beauty industry is positively affected due to its quality products available at cheaper prices. Urban consumers like to use beauty products with innovative packaging designs under the brand name.

Restraints & Challenges

Stringent regulatory structures are putting immense pressure on manufacturers: The regulation for cosmetics in China is very strict when it concerns the safety of ingredients, labelling, testing, and registering of cosmetics. Manufacturers have been facing high costs in introducing a new product due to lengthy regulatory approval processes. Small firms may feel the strain from the shifting regulations as it may affect the product’s expansion.

Perceived quality concerns in international markets are limiting overseas growth: Chinese cosmetics continue to be viewed with suspicion by some consumers abroad. They present a challenge for companies positioning themselves as luxury brands. Companies need stronger branding, certifications, and product transparency to improve global acceptance. The issue may restrain export growth.

Opportunity

AI-powered skincare and clean beauty trends are creating new growth opportunities: Companies from the beauty industry are now using AI-powered technology that offers skin diagnostics and personalized recommendations for customers. For example, in January 2025, Datasea introduced its 5G AI solution and acoustic technology in northern Chinese beauty stores, which facilitated the development of intelligent retail and innovations in the cosmetics industry. The increasing need for sustainability in packaging, natural ingredients, and clean beauty products is also forming new product categories.

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the C-beauty products product type, price tier, and distribution channel to help readers identify the fastest expanding and most attractive demand segments.

By Product Type

-

Skincare

Skincare category took the lead in 2025, accounting for nearly 36.50% market share, led by high demand for products that provide anti-aging benefits, hydrating effects, skin whitening, and overall skin repair. The skincare segment continue to grow, as consumers invest more in functional skin care products whose formulas were ingredient-based.

-

Color Cosmetics

Color cosmetics category is expected to grow at a CAGR of around 9.70%, owing to the high influence of Gen Z consumers and quick changes in beauty trends. The demand for lip care products, foundations, and eye makeup was steadily growing. Fast product innovation is supporting expansion of this segment.

By Price Tier

-

Mass

Mass segment held the largest share in 2025 due to high customer demand for cost-effective beauty products with modern packaging. The domestic brands are gaining popularity through their value-based pricing approach. The high repurchase rate has contributed to their dominance in the segment.

-

Premium

Premium segment is expected to witness the highest CAGR during the forecast period owing to rising disposable income among the middle-class population and a shift towards effective beauty products. Customers are exhibiting an inclination towards advanced skincare products, luxurious makeup items, and clean labels.

By Distribution Channel

-

Online

Online retail category was dominant in 2025, contributing approximately 39.80% market share owing to wide acceptance of e-commerce, live selling, and e-commerce platforms. According to the International Trade Administration, global B2C e-commerce revenue is expected to achieve USD 5.5 trillion in 2027 growing at a CAGR of 14.4%, providing ample growth prospects for sales through the online channel of C-beauty products..[Source: www.trade.gov] Convenience and variety make the online channel the choice of consumers.

-

Offline

Offline segment is projected to grow at the fastest CAGR during the forecast period due to expansion of beauty specialty stores, experiential retail formats, and department store counters. Consumer demand for in-store trials and consultations is rising. Retail network expansion is supporting growth of this segment.

Source: Polaris Market Research Analysis

Regional Analysis

China Market Assessment

China held the largest market share, accounting for nearly 42.60% share in 2025 driven by strong domestic demand, advanced manufacturing capacity, and rapid digital commerce adoption. As per Yatsen Holding Limited, the share of Chinese beauty brands within the domestic market has climbed from 43% in 2015 to 57% in the previous year, rising gradually from 50% in 2022..[Source: news.cgtn.com] In addition, consumers tend to favor domestically made beauty brands as they cater to trends while keeping their products priced reasonably.

Asia-Pacific (Ex-China) C-Beauty Products Insights

Asia-Pacific excluding China region is expected to be the fastest-growing at the highest CAGR over the forecasted period owing to rising consumer awareness about beauty products, demands for affordable products, and greater access to online shopping platforms. For instance, in July 2025, Joocyee established its international store for the first time in Singapore, enhancing the growth of C-beauty in Southeast Asia. The nations like Indonesia, Vietnam, and Thailand are expected to be future growth hubs for the Chinese cosmetics firms.

North America & Europe C-Beauty Products Overview

North America and Europe have seen consistent growth in the popularity of C-beauty owing to the rising trend of incorporating Asian skincare practices into their beauty routines. In November 2025, an investment by L’Oreal in one of the skincare products from China highlights the increasing international interest in C-beauty brands. E-commerce sites are contributing significantly to providing access to Chinese brands to new consumers using the DTC business model.

Source: Polaris Market Research Analysis

Competitive Landscape & Key Players

C-beauty industry demonstrates moderate fragmentation owing to rivalry from indigenous brands, new companies targeting digital media channels, and foreign cosmetic brands within China. The key success elements within this industry include innovation, branding, pricing, and online engagement. Product innovation, influencer collaborations, and fast-paced product rollouts are critical aspects that need to be considered to obtain an advantage. Expansion is realized through diversification in premium and clean beauty products and cross-border b2c e-commerce.

Some firms in this industry include Perfect Diary, Florasis, Proya Cosmetics, Winona, Judydoll, Carslan Cosmetics, Chando, Pechoin, Herborist, Marie Dalgar, Inoherb, Biohyalux, and others.

Company Benchmarking Table

| Company | Strengths | Weaknesses | Strategy Focus |

| Perfect Diary | Strong online reach, fast launches | Margin pressure, high ad spend | Influencer marketing, premium growth |

| Florasis | Premium image, strong branding | Limited global reach | Cultural branding, export expansion |

| Proya | Strong R&D, trusted skincare | Lower Gen Z appeal | Product innovation, channel growth |

| Winona | Sensitive skin expertise, strong trust | Niche focus | Clinical skincare, premium expansion |

| Perfect Diary | Strong online reach, fast launches | Margin pressure, high ad spend | Influencer marketing, premium growth |

Source: Polaris Market Research Analysis

Premium Insights

- ROI Potential: C-beauty brands have the potential for ROI thanks to quick production times, inexpensive digital advertising, and easy scalability through online sales. The ability to adapt quickly to trends in the beauty industry contributes to faster revenues.

- Entry Barriers: There exist moderate barriers to entry in the manufacturing process in the industry; however, intense competition and product branding are also barriers. Trust and visibility on the internet are also barriers to entry.

- M&A Opportunities: International businesses have considered M&A within Chinese beauty brands in order to secure positions in China and the younger generation.

Strategic Insights for Investors

- Invest in OEM/ODM cosmetic brands to secure stable supply agreements and margins.

- Consider new age brands that have good scalability online.

- Consider investing in clean cosmetics and derma skincare companies.

- Allocate resources to cosmetic products that enter Southeast Asia via cross-border commerce.

Trends & Future Outlook

- AI-powered skincare diagnosis and virtual consultations are becoming popular.

- Personalized beauty products are increasing consumer engagement.

- Eco-friendly packaging and clean ingredients are influencing product launches.

- The cross-border market is helping C-beauty brands go global.

Key Players

- Biohyalux

- Carslan Cosmetics

- Chando

- Florasis

- Herborist

- Inoherb

- Judydoll

- Marie Dalgar

- Pechoin

- Perfect Diary

- Proya Cosmetics

- Winona

Industry Developments

- December 2025: Flower Knows was the debut product line from Ulta Beauty and became the first C-beauty brand in America. [source: www.beautyindependent.com]

- May 2024: Florasis expanded its global presence by opening at Samaritaine Paris, which is a huge leap towards the expansion of the C-beauty industry in Europe. [source: florasis.com]

C-Beauty Products Market Segmentation

By Product Type Outlook (Revenue, USD Billion, 2021-2034)

- Skincare

- Moisturizers

- Cleansers

- Face Masks

- Serums & Essences

- Toners

- Color Cosmetics

- Lipstick & Lip Tint

- Foundations & BB/CC Creams

- Eye Makeup (Eyeliners, Eyeshadows, Mascaras)

- Blushers & Highlighters

- Haircare

- Shampoo & Conditioner

- Hair Masks & Oils

- Scalp Treatments

- Fragrance & Others

By Price Tier Outlook (Revenue, USD Billion, 2021-2034)

- Mass

- Mid-Range

- Premium

By Distribution Channel Outlook (Revenue, USD Billion, 2021-2034)

- Online

- Offline

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

C-Beauty Products Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 19.58 Billion |

| Market Size in 2026 | USD 21.56 Billion |

| Revenue Forecast by 2034 | USD 47.10 Billion |

| CAGR | 10.24% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

C-Beauty Products Market FAQ's

The global market size was valued at USD 19.58 Billion in 2025 and is projected to grow to USD 47.10 Billion by 2034.

China held the largest market share, accounting for nearly 42.60% share in 2025 due to strong domestic demand, advanced manufacturing capacity, and high digital commerce adoption.

Major applications include skincare, color cosmetics, haircare, fragrance, and personal wellness products.

A few of the key players in the market are Perfect Diary, Florasis, Proya Cosmetics, Winona, Judydoll, Carslan Cosmetics, Chando, Pechoin, Herborist, Marie Dalgar, Inoherb, Biohyalux, and others.

Key drivers include rising online beauty sales, growing middle-class spending, premiumization trends, and strong social media influence.

Major demand comes from personal care, cosmetics retail, e-commerce, wellness, and beauty services sectors.

There are good market prospects because of beauty innovations such as AI technologies, clean beauty products, and cross-border expansion.

Download Sample Report of C-Beauty Products Market

Please fill out the form to request a customized copy of the research report.