Automated Cell Culture Market Trends Analysis Report, 2026-2034

REPORT DETAILS

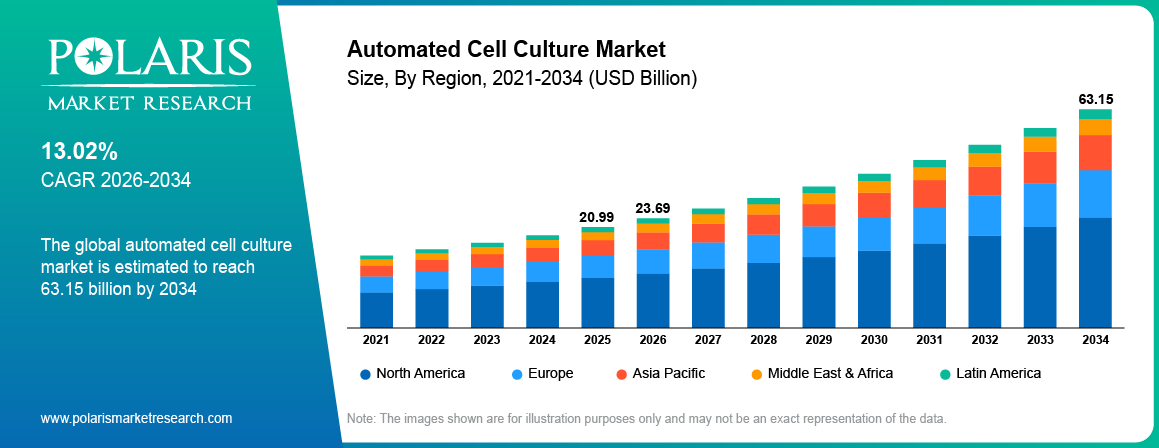

Automated Cell Culture Market Summary

The global automated cell culture market is estimated around USD 20.99 Billion in 2025,with consistent growth anticipated during 2026–2034. This growth is driven by increasing demand for biologics, rising adoption of automation in laboratory workflows, and expanding research in cell therapy and regenerative medicine. The market is projected to grow at a CAGR of 13.02% during the forecast period.

Market Statistics

Key Takeaways

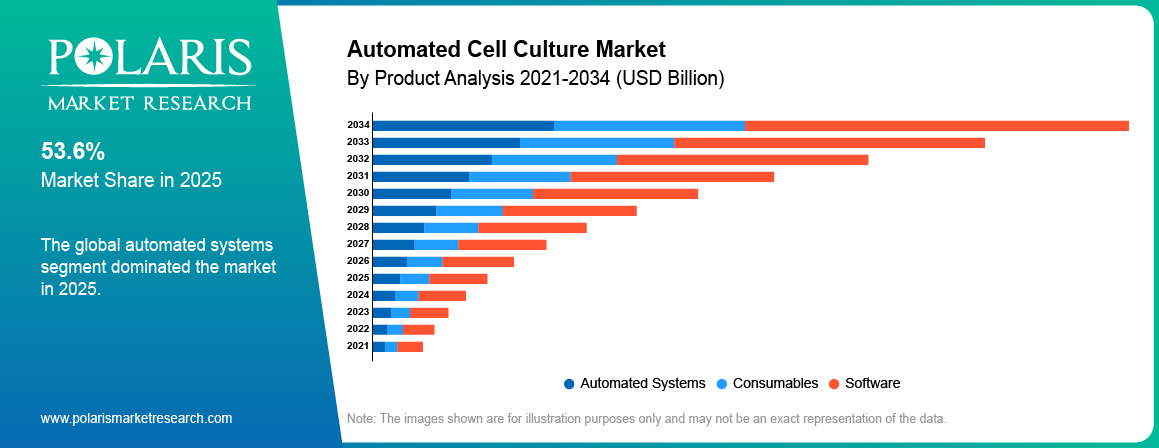

- Automated systems segment dominated in 2025, accounting for nearly 29.20% market share due to strong adoption in research and biomanufacturing environments.

- Biopharma segment led in 2025, contributing approximately 43.50% market share owing to increasing use of automation in biologics development and production processes.

- Consumables segment is projected to grow at a CAGR of around 11.10% due to recurring demand in routine cell culture operations.

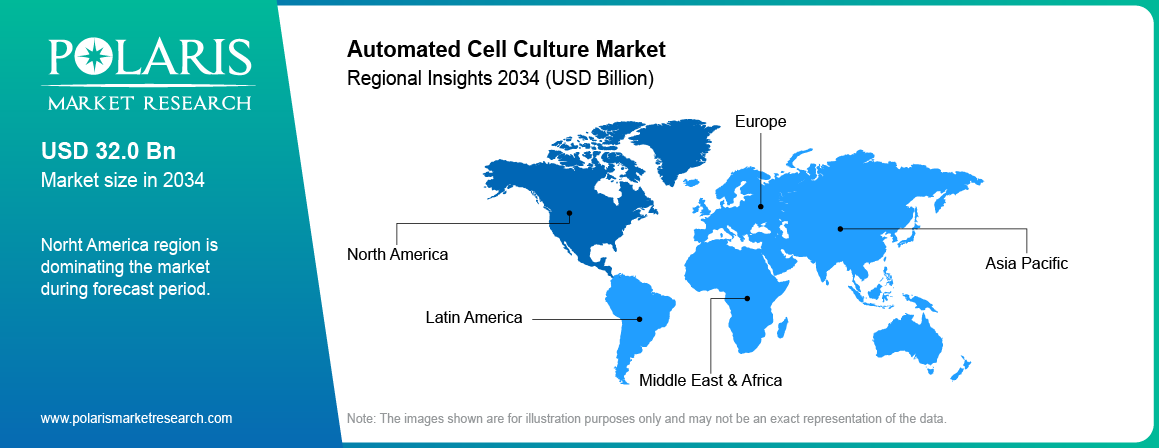

- North America dominated the market with nearly 48.30% share in 2025 due to strong presence of biopharmaceutical companies and advanced research infrastructure.

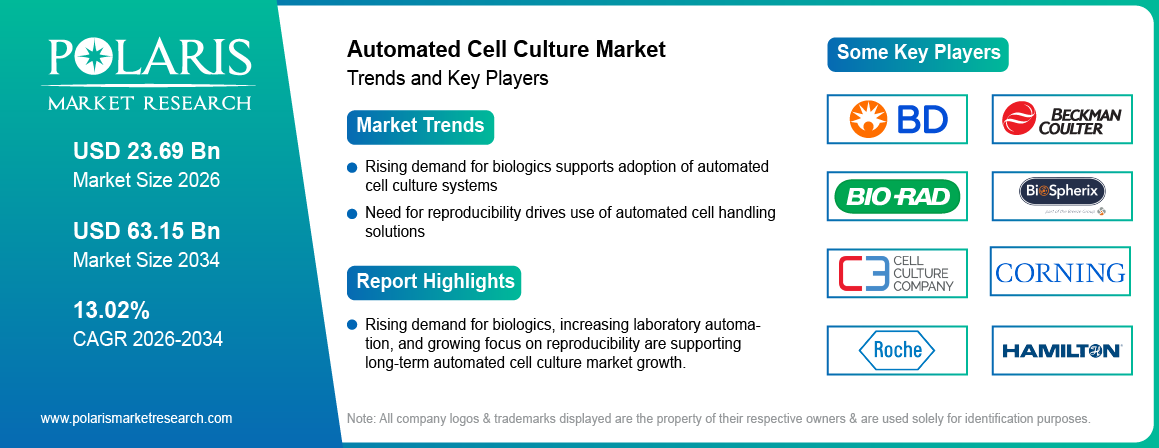

- Key players operating in the market include Becton, Dickinson and Company, Beckman Coulter, Inc., Bio-Rad Laboratories, Inc., Biospherix Ltd., Cell Culture Company, LLC, Corning Incorporated, F. Hoffmann-La Roche Ltd., Hamilton Company, Hitachi High-Tech Corporation, Lonza Group Ltd., Merck KGaA, Miltenyi Biotec B.V. & Co. KG, PromoCell GmbH, Sartorius AG, Tecan Trading AG, and others.

Industry Dynamics

- Rising demand for biologics increases adoption of automated cell culture systems.

- The requirement for reproducibility ensures the need for adopting automation and AI-powered cell manipulation tools.

- Heavy investments make the solution unaffordable for small labs.

- AI-based integration into automation offers promising growth potential.

What are Automated Cell Culture?

The cell culture automation involves an advanced process involving the use of robots, artificial intelligence, and digital surveillance technology that allows easy manipulation of the whole process of cellular growth, development, and study with minimal human intervention. The concept involves using specialized equipment to provide higher efficiency and consistency in cell manipulation processes. The technology has become popular in the fields of biopharmaceutical automation, research institutes, and other industries.

Demand for automated cell culture systems is increasing owing to the changing trends towards precision medicine and the development of cell therapies. Expansion of regenerative medicine research has created strong demand for scalable and reproducible cell culture processes. Automated platforms are used to support stem cell research, tissue engineering, and advanced therapeutic development, which is strengthening adoption across research and clinical pipelines.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

Biopharmaceutical firms are adopting biopharmaceutical automation solutions to boost productivity while lowering the incidence of errors in cell handling protocols. The problems that emerge when it comes to the manufacturing of biological drugs and conducting clinical tests have played a significant role in creating demand for automation. Advances in robotics and software and real-time monitoring are contributing toward improved system performance. Quality assurance and process standardization and cost optimization are some of the factors likely to fuel market growth in the coming years.

Drivers & Opportunities

Rising Biologics Demand Strengthens Automation Drivers in Cell Culture: Increasing focus on biologics creation are boosting the need for effective cell cultures. According to the American Medical Society, global consumption of biologics is expected to reach USD 569.7 billion by 2027, at an annual growth rate of 9.2%.[Source: web.cas.org] Efficiency and consistency in the laboratory setting are becoming increasingly important owing to the developments in this area. The automation of cell culture procedures and the use of robotic cell culture systems help achieve this by minimizing human intervention and providing better control of the process.

Need for Reproducibility Drives Adoption of Automated Cell Handling Solutions: Reproducibility and reliability of results are crucial for any research and bioprocess development process. These inconsistencies occur as humans participate in these operations, thereby influencing the consistency of outcomes obtained and quality of the products manufactured. Automated incubation of cells and intelligent cell cultures allow for a higher level of consistency and control over experimental parameters, thereby increasing the need for cell-handling automation.

Restraints & Challenges

High Capital Cost Limits Adoption of Automation Systems: Automation in cell culture processes is highly capital-intensive, which is one of the major barriers to adoption. Automation in cell cultures are expensive as robots, software, and even changes in the facility are needed. This makes small labs and scientific organizations find it difficult to implement automation due to budget constraint.

Opportunity

AI-driven Automation Creates new Opportunities for Process Optimization: The inclusion of AI in facilitating the evolution of the cell culture process workflow are creating opportunities in the field of cell culture. In January 2026, Automata made a strategic alliance with Cellvoyant to develop an AI-based closed-cell culture process workflow system using the predictive analytics method alongside lab automation tools.[Source:www.automata.tech] It helps in process monitoring and optimization, enhancing efficiency and accuracy.

Source: Polaris Market Research Analysis

Segmental Analysis

The report offers an extensive study of the automated cell culture market on the basis of product, application and end user to determine key revenue generating segments along with growth opportunities.

By Product

-

Automated Systems

Automated systems segment dominated in 2025, accounting for nearly 29.20% market share owing to growing usage of modern cell culture systems for laboratory studies and manufacturing processes. They are capable of enhancing operational efficiencies, avoiding errors and facilitating high throughput processing, thus ensuring wide adoption.

-

Consumables

Consumables segment is projected to grow at a CAGR of around 11.10% driven by recurring demand in routine cell culture processes. Consumables including media, reagents, and cell culture containers are crucial for the ongoing operations, ensuring constant earnings generation.

By Application

-

Drug Discovery

Drug discovery application accounted for the largest share in 2025 owing to growing adoption of drug discovery automation in preliminary research and screening phases. Automation ensures that more samples are processed efficiently and accurately by conducting faster screenings while also ensuring shorter development times. For example, in April 2026, OpenAI revealed its artificial intelligence model GPT-Rosalind, designed for the industry, to speed up early-stage drug discovery processes.[Source: openai.com]

-

Stem Cell Research

Stem Cell Research is expected to witness the highest growth during the forecast period due to the increasing need for regenerative medicines and novel treatments. The use of automation in the system allows better control of growth parameters of cells.

By End-User

-

Biopharma

Biopharma segment led in 2025, contributing approximately 43.50% market share owing to the growing use of automation in cell culture processes used in the development and production of biological products. Automation is preferred due to efficiency and quality control needs.

-

CROs

CROs segment is expected to register the highest growth rate during the forecast period due to the rising trend of outsourcing research and development functions. CROs use automation techniques to deal with intricate processes efficiently.

Source: Polaris Market Research Analysis

Regional Analysis

North America Automated Cell Culture Market Assessment

North America dominated the market with nearly 48.30% share in 2025, supported by a strong presence of biopharmaceutical companies and advanced research infrastructure. The area exhibits high deployment of automation technology for drug discovery and cellular research. In December 2025, Emory University introduced, CellXpress.ai Automated robotic and AI Imaging cell cultivation technology in the US for high throughput organoid research.[Source: news.emory.edu] Increasing use of AI-driven monitoring and continuous cell analysis supports efficiency and scalability in research workflows, strengthening market demand.

Europe Automated Cell Culture Market Overview

Europe was the second leading market in automated cell culture, propelled by regulatory structures that help facilitate the use of bioprocessing. The region is focusing on developing the biotech sector through legislation and policies. In December 2025, the European Commission introduced the Biotech Act to develop Europe's biotech industry with special emphasis on healthcare. [Source:health.ec.europa.eu]The introduction of the Biotech Act is in line with the life sciences strategy of 2024–2029, encouraging adoption of automated systems in research and production environments.

Asia Pacific Automated Cell Culture Market Insights

Asia-Pacific projected to witness highest CAGR during the forecast period due to rising investments in biotechnology infrastructure in China, India, and South Korea. Different measures implemented by various governments in the regions towards research and biomanufacturing capacity building have played a significant role in driving innovation within their territories. The government of India initiated the project “Bio-RIDE” with a budget allocation of USD 1.1 billion from 2021 to 2026 for biomanufacturing and biofoundry capabilities. [Source: www.ibef.org] Expansion in research laboratories and adoption of automation solutions continue to boost the need for automated cell culturing devices in the region.

Rest of the World Automated Cell Culture Market Outlook

The rest of the world (RoW) region witnessing moderate growth, fueled by the growing application of automation solutions in Latin America and the Middle East. Automation systems are getting introduced in the laboratories and health care institutes in the RoW area in order to improve the efficiencies associated with cell culturing procedures.

Source: Polaris Market Research Analysis

Competitive Landscape & Key Players

The field of automated cell cultures is marked by a concentrated market structure with firms involved in life sciences and lab automation competing among themselves in delivering advanced solutions to the market. The competitive nature of the market is attributed to issues such as the ability to integrate systems, speed of operation, usability, and adherence to laboratory standards. Demand from biopharmaceutical manufacturing and research institutions continues to shape vendor positioning.

The key players in the market include Thermo Fisher Scientific, Sartorius AG, Danaher Corporation, Becton, Dickinson and Company, Beckman Coulter, Inc., Bio-Rad Laboratories, Inc., Biospherix Ltd., Cell Culture Company, LLC, Corning Incorporated, F. Hoffmann-La Roche Ltd., Hamilton Company, Hitachi High-Tech Corporation, Lonza Group Ltd., Merck KGaA, Miltenyi Biotec B.V. & Co. KG, PromoCell GmbH, and Tecan Trading AG.

Premium Insights

Regulatory Framework

The regulation governing the automated cell culture sector centers on process standardization, contamination management, and data integrity. Authorities such as the U.S. Food and Drug Administration and European Medicines Agency define guidelines for automated systems used in bioprocessing and cell-based production. Companies required to adhere to the GMP guidelines and make sure that the process is traceable, reproducible, and validated within automated procedures.

Key Risks Associated with Automated Cell Culture Market

High entry costs and system complexity are some of the threats that the sector encounters. Integrating automated systems in current lab settings present operational difficulties. Technical issues with the systems or any other software-related problems lead to contamination and decrease in productivity. Inadequate personnel to operate automated systems further affect growth within smaller laboratories.

Strategic Insights

Future trends in the field includes AI predictive systems to optimize cell growth without manual operations. Autonomous labs are projected to gain popularity as there is a requirement to minimize human interference in the operation of the lab. Digital twin technology is used to simulate the lab environment for real-time analysis. Future trends in the automation sector include AI labs and scalable automation platforms.

Key Players

- Becton, Dickinson and Company

- Beckman Coulter, Inc.

- Bio-Rad Laboratories, Inc.

- Biospherix Ltd.

- Cell Culture Company, LLC

- Corning Incorporated

- F. Hoffmann-La Roche Ltd.

- Hamilton Company

- Hitachi High-Tech Corporation

- Lonza Group Ltd.

- Merck KGaA

- Miltenyi Biotec B.V. & Co. KG

- PromoCell GmbH

- Sartorius AG

- Tecan Trading AG

Industry Developments

- May 2024: Sinfonia Technology Co., Ltd. provided its CellQualia Intelligent Cell Processing System in Japan for automating cell cultures in order to provide quality regenerative medicine manufacturing. [source: www.sinfo-t.com]

- January 2024: Thermo Fisher Scientific launched the CTS Cellmation software platform for use in the United States, combining various tools to provide automation in the processes involved in cell therapy. [source: thermofisher.com]

Automated Cell Culture Market Segmentation

By Product Outlook (Revenue, USD Billion, 2021-2034)

- Automated Systems

- Consumables

- Software

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Drug Discovery

- Stem Cell Research

- Biopharmaceutical Production

By End-User Outlook (Revenue, USD Billion, 2021-2034)

- Biopharmaceutical Companies

- CROs & CDMOs

- Academic & Research Institutes

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Automated Cell Culture Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 20.99 Billion |

| Market Size in 2026 | USD 23.69 Billion |

| Revenue Forecast by 2034 | USD 63.15 Billion |

| CAGR | 13.02% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Automated Cell Culture Market FAQ's

The global market size was valued at USD 20.99 Billion in 2025 and is projected to grow to USD 63.15 Billion by 2034.

North America dominated the market with nearly 48.30% share in 2025 due to strong biopharmaceutical presence and advanced research infrastructure.

Major applications include drug discovery, stem cell research, biologics production, and tissue engineering.

Key players include Becton, Dickinson and Company, Beckman Coulter, Inc., Bio-Rad Laboratories, Inc., Biospherix Ltd., Cell Culture Company, LLC, Corning Incorporated, F. Hoffmann-La Roche Ltd., Hamilton Company, Hitachi High-Tech Corporation, Lonza Group Ltd., Merck KGaA, Miltenyi Biotec B.V. & Co. KG, PromoCell GmbH, Sartorius AG, and Tecan Trading AG.

Growth is driven by increasing biologics production, rising demand for automation in laboratories, and expansion of regenerative medicine research.

High capital cost and infrastructure requirements limit adoption among smaller research facilities.

Demand drivers include biopharmaceutical firms, contract research organizations, and academic research institutions.

The market outlook remains strong due to increasing integration of AI and automation in laboratory workflows.

AI improves process optimization, enhances monitoring capabilities, and increases efficiency in cell culture workflows.

Download Sample Report of Automated Cell Culture Market

Please fill out the form to request a customized copy of the research report.