Dimethyl Ether Market Share, Opportunity, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

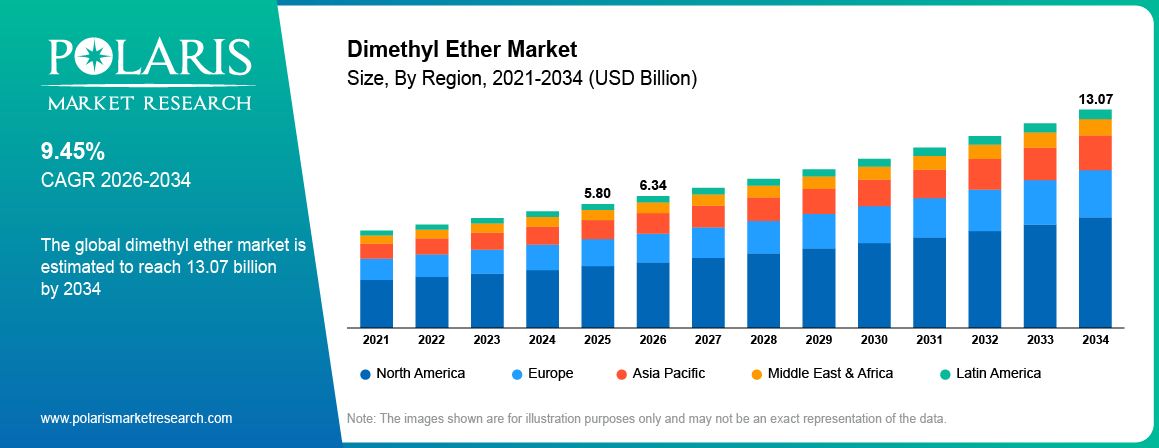

Dimethyl Ether Market Summary

The global dimethyl ether market is estimated around USD 5.80 Billion in 2025,?with consistent growth anticipated during 2026–2034. Expansion is driven by rising demand for clean and low-emission fuels, increasing adoption in LPG blending, and growing use across transportation and industrial heating applications. The market is projected to grow at a CAGR of 9.45% during the forecast period.

Market Statistics

Key Takeaways

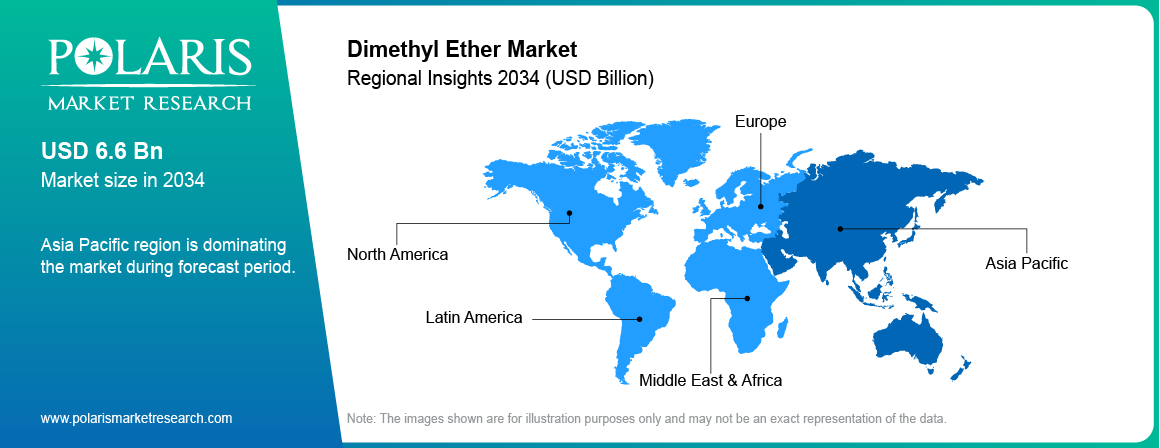

- Asia Pacific emerged dominant in terms of market share, accounting for approximately 43.60% due to existing production capacity and high LPG consumption.

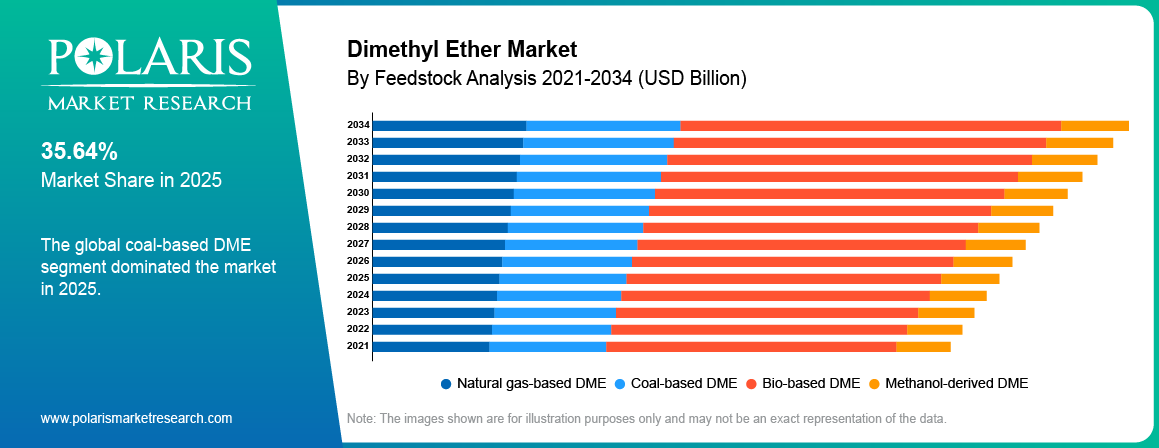

- Coal-based DME dominated the market, holding approximately 38.25% market share due to established production facilities and availability of raw materials.

- Dimethyl ether continues to be an important compound in LPG blending, contributing approximately 35.40% market share owing to compatibility with existing storage and transport systems.

- Energy and fuel sector represents the majority of demand, accounting for approximately 46.15% market share driven by the shift toward low-emission fuels.

- LPG blending registered dominating market share, holding approximately 40.80% due to its widespread use in household and industrial fuel applications.

- Transportation held the leading share, contributing approximately 33.95% market share propelled by increasing demand for cleaner alternatives to diesel.

Industry Dynamics

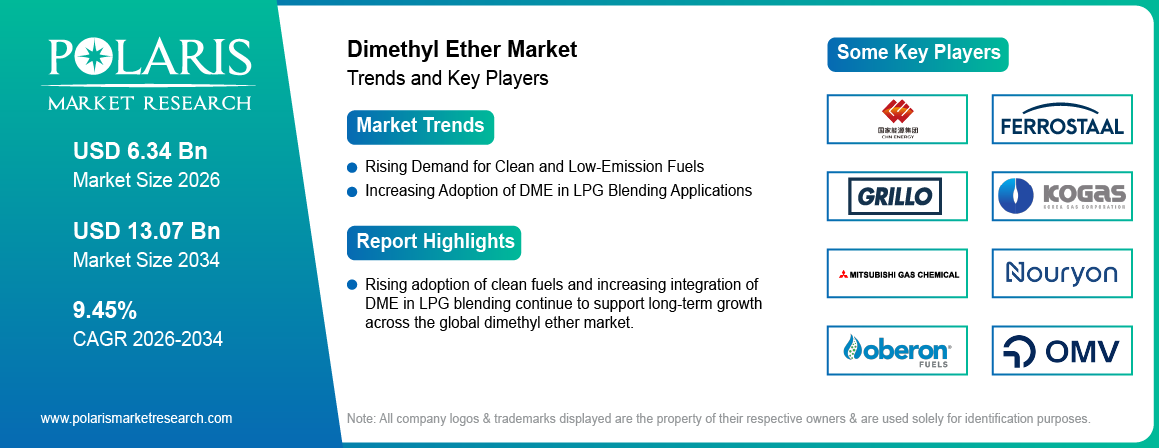

- Growing demand for environmentally-friendly fuels is driving the usage of DME in transportation, cooking, and industrial heating sectors.

- Use of DME in LPG blending is driving demand due to lower infrastructure investment needs.

- The high cost of producing bio-DME has hampered its adoption in price-sensitive regions.

- Advancements in CO₂-to-DME and bio-based production technologies are opening new growth opportunities.

What is included in the Dimethyl Ether market?

The dimethyl ether market reflects steady expansion driven by clean fuel demand and alternative energy adoption. Variations in estimates arise from differences in feedstock coverage and end-use inclusion. Dimethyl ether is a clean fuel, aerosol propellant, and chemical raw material. It is non-toxic, free from sulfur content, and possesses high cetane number, thereby making it ideal for use as a diesel fuel alternative and as a blending agent for liquefied petroleum gas.

Dimethyl ether industry analysis provides positive growth prospects for the future. This fuel finds widespread application in LPG blending, as fuel for residential purposes, aerosol propellants, and as a chemical intermediate. Asia-Pacific region led in terms of its market share owing to the high rate of utilization of LPG, favorable government policy, and substantial production capacity in China.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The growth rate of the DME market is driven by the rise in demand for energy and clean fuels. Its compatibility with existing LPG infrastructure supports faster deployment. Growing application in off grid energy sources and industrial heating boosts the demand. Such trends keep influencing future expansion within the dimethyl ether market.

Drivers & Opportunities

Rising demand for clean and low-emission fuels: Strict regulations on emission levels and targets set for decarbonization, the momentum is growing in favor of fuels with lower carbon emissions. The growing preference for cleaner fuels has led to higher demand for dimethyl ether (DME), owing to its lower emissions in comparison to diesel and LPG. Increasing spending on lower emitting fuels reached USD 13 billion in 2022, according to the International Energy Agency. This expansion is strengthening DME adoption across transport, residential cooking, and industrial heating applications, leading to sustained market growth.

Integration of DME into LPG blending applications: Current LPG systems facilitate direct blending of DME, reducing investments in the construction of storage facilities for the product. The compatibility of DME and LPG fuels is encouraging more use by fuel providers who seek to lower their carbon footprint without making significant improvements in their infrastructure. In February 2026, Fraunhofer ISE created an efficient energy method of producing DME, enhancing its effectiveness in hydrogen transportation and storage.

Restraints & Challenges

High Initial Production Costs for Bio-Based DME: The manufacturing process of bio-DME is complex and involves many stages. Bio-DME plants do not have the necessary infrastructure and equipment. Therefore, DME becomes costly to manufacture, leading to a loss in competitiveness against other petrochemical products like LPG.

Opportunity

Bio-based Dimethyl Ether and CO₂-to-DME Technologies: Research and development in CCU technology has opened doors to alternative methods of producing DME that minimize the environmental impact. CO₂ gas generated by industries are efficiently used to make valuable fuel. Godavari Biorefineries and ICT Mumbai established the world's first single-step CO₂-to-DME plant in November 2025.

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the dimethyl ether market by feedstock, production, and application, and distribution channel to help readers identify the fastest expanding and most attractive demand segments.

By Feedstock

-

Coal-based DME

Coal-based DME accounted for the largest share in dimethyl ether production due to strong availability of coal reserves and established gasification infrastructure in key markets. The coal-based DME production route converts syngas into methanol and further into DME through the methanol to DME process.

-

Bio-based dimethyl ether (renewable DME)

Bio-based dimethyl ether (renewable DME) is the most rapidly growing category due to the transition towards lower-carbon fuel options. The manufacturing process of bio-based dimethyl ether involves biomass, agricultural residues, or renewable methanol as raw materials.

| Feedstock Type | Cost Level | Emissions Profile | Scalability | Key Insight |

| Coal-based DME | Low | High | High | Dominates due to cost advantage and infrastructure |

| Natural gas-based DME | Medium | Moderate | High | Balanced option with cleaner profile than coal |

| Methanol-derived DME | Medium | Depends on source | High | Flexible route via methanol to DME process |

| Bio-based DME | High | Low | Emerging | Future growth driven by sustainability targets |

Source: Polaris Market Research Analysis

By Production

-

Indirect synthesis

Indirect synthesis segment was the largest shareholder in terms of market share owing to the common approach employed in the production of DME. The process comprises two stages including the first stage that entails the synthesis of syngas to methanol, which is later dehydrated to form DME.

-

Direct synthesis

Direct synthesis is projected to grow at a rapid pace due to its energy efficiency. In direct synthesis, syngas is synthesized directly to DME in one step. Direct synthesis saves energy compared to other methods as it only needs one process step, thereby lowering energy expenditure and production costs.

By Application Analysis

-

LPG blending

LPG blending dominated the market due to efficient fuel substitute for LPG in residential and commercial applications. LPG blending with DME ensures high-efficiency burning process as well as reduced particulates that make DME applicable in cooking and heating.

-

Transportation

Transportation fuel is projected to grow rapidly, due to increasing usage of alternate fuel DME in greening transportation. Fuel DME provides high combustion efficiency like diesel but emits less NOx and particles. Its popularity is growing in applications such as heavy trucks, buses, and fleets, where emissions regulations are becoming stricter.

Source: Polaris Market Research Analysis

Regional Analysis

Asia Pacific Dimethyl Ether Market Assessment

Asia Pacific dimethyl ether market led due to strong production capacity and rising demand for clean fuels across China, India, and Japan. China market for Dimethyl Ether sees advantages in the coal to DME route and industrial scale usage, while the Japanese market is centered around blending DME with LPG. India’s Dimethyl Ether market is witnessing growth fueled by supportive policies toward environmentally friendly fuel sources. The Indian government plans to reduce the emission intensity of its GDP by 47% till 2035 and ensure that 60% of the total installed power capacity of India comes from non-fossil fuel sources. Such policies along with the increasing energy needs of the region and change in fuel types in industries are making DME popular in the region.

North America Dimethyl Ether Market Assessment

North America DME market is expected to exhibit moderate growth owing to the increasing number of investments in renewable DME. and clean energy sources. In the US, there is a growing emphasis on low carbon fuel options that benefit from considerable financial backing in energy transition initiatives. The US invested USD 338 billion in 2024 compared to USD 303 billion in 2023 for renewable energy, electric vehicles (EVs), and grid infrastructure. The investment landscape fosters the production of renewable DME from bio-derived and CO₂-based raw materials.

Europe Dimethyl Ether Market Overview

Europe DME demand is increasing due to the emphasis placed on sustainability and the incorporation of renewable energy sources. The regulatory environment that favors low carbon fuels has been instrumental in adopting DME for transportation and heating applications. Nations like Germany and the Netherlands are pursuing policies for clean fuels consistent with their plans to decarbonize. This regulatory push continues to support market growth.

Middle East & Latin America Dimethyl Ether Market Assessment

Middle East and Latin America markets are expanding with energy diversification initiatives and gradual adoption of cleaner fuels. Countries in the Middle East are investing in alternative fuels to reduce reliance on crude oil exports. Latin America is exploring DME for transport and industrial fuel applications. Growing interest in clean energy transitions and infrastructure development is supporting moderate demand growth across these regions.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The market dynamics within the dimethyl ether market show heavy involvement from integrated energy companies, chemicals manufacturers, and new clean fuels ventures interested in commercializing their DME production processes. The competing firms within the dimethyl ether market do so through expanding capacities, employing diverse feedstocks including coal, natural gas, and biomass feedstocks, and developing methanol-to-DME and CO2-to-DME conversion technologies.

Key players operating in the dimethyl ether market include China Energy Investment Corporation (Shenhua), Ferrostaal GmbH, Grillo-Werke AG, Jiutai Energy Group Co., Ltd., JX Nippon Oil & Energy Corporation, Korea Gas Corporation, Mitsubishi Gas Chemical Company, Inc., Nouryon, Oberon Fuels Inc., OMV Aktiengesellschaft, Petra Nova Development LLC, PetroChina Company Limited, Shell plc, TotalEnergies SE, and Zagros Petrochemical Company.

Key Players

- China Energy Investment Corporation (Shenhua)

- Ferrostaal GmbH

- Grillo-Werke AG

- Jiutai Energy Group Co., Ltd.

- JX Nippon Oil & Energy Corporation

- Korea Gas Corporation

- Mitsubishi Gas Chemical Company, Inc.

- Nouryon

- Oberon Fuels Inc.

- OMV Aktiengesellschaft

- Petra Nova Development LLC

- PetroChina Company Limited

- Shell plc

- TotalEnergies SE

- Zagros Petrochemical Company

Industry Developments

- April 2026: Researchers at BITS Pilani developed a technology to convert industrial smoke-like gases into dimethyl ether (DME), enabling direct transformation of emissions into a clean fuel suitable for LPG substitution.[Source: www.indianchemicalnews.com]

- May 2024: Lummus Technology introduced its renewable DME process through catalytic distillation that converts methanol into clean energy for LPG blending and hydrogen carriers. [Source: www.prnewswire.com]

Dimethyl Ether Market Segmentation

By Feedstock Outlook (Revenue, USD Billion, 2021-2034)

- Natural gas-based DME

- Coal-based DME

- Bio-based DME

- Methanol-derived DME

By Production Outlook (Revenue, USD Billion, 2021-2034)

- Indirect Synthesis

- Direct Synthesis

By Application Outlook (Revenue, USD Billion, 2021-2034)

- LPG Blending

- Transportation Fuel

- Aerosol Propellants

- Industrial Applications

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Dimethyl Ether Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 5.80 Billion |

| Market Size in 2026 | USD 6.34 Billion |

| Revenue Forecast by 2034 | USD 13.07 Billion |

| CAGR | 9.45% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Dimethyl Ether Market FAQ's

The global market size was valued at USD 5.80 Billion in 2025 and is projected to grow to USD 13.07 Billion by 2034.

Asia Pacific dominates due to strong production capacity, high LPG consumption, and supportive clean fuel policies.

Energy, residential fuel, and transportation sectors account for the largest share due to widespread fuel applications.

Key companies include China Energy Investment Corporation (Shenhua), Ferrostaal GmbH, Grillo-Werke AG, Jiutai Energy Group Co., Ltd., JX Nippon Oil & Energy Corporation, Korea Gas Corporation, Mitsubishi Gas Chemical Company, Inc., Nouryon, Oberon Fuels Inc., OMV Aktiengesellschaft, Petra Nova Development LLC, PetroChina Company Limited, Shell plc, TotalEnergies SE, and Zagros Petrochemical Company.

Growth is driven by rising clean fuel demand, increasing LPG blending adoption, and expansion of low-emission energy solutions.

The key trends include renewable dimethyl ether, CO?-based dimethyl ether, and application in transport fuel markets.

It enhances combustion efficiency and reduces pollutants emitted without altering LPG facilities and technology.

Download Sample Report of Dimethyl Ether Market

Please fill out the form to request a customized copy of the research report.