Electronic Design Automation Market Size, Share & Growth Analysis Report, 2026-2034

REPORT DETAILS

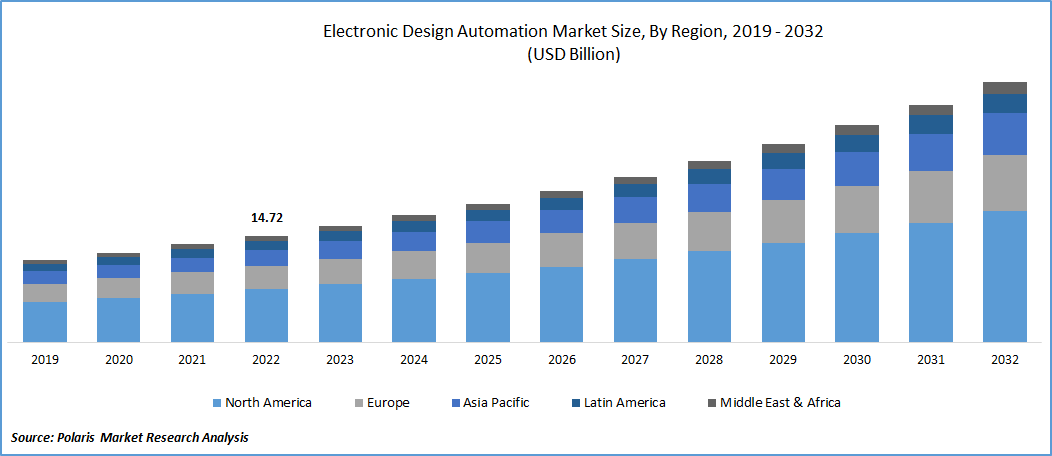

Electronic Design Automation Market Summary

The electronic design automation market was valued at USD 19.15 billion in 2025. The market is projected to account for a CAGR of 9.4%between 2026 and 2034. The market is primarily driven by increased demand for advanced chips for artificial intelligence accelerators, automotive electronics, and new communication systems. With decreasing node sizes in semiconductors, chip designs have become more complex, leading to an increased requirement for advanced EDA solutions.

Market Statistics

Key Takeaways

- North America dominated the global electronic design automation market with over 49.80% revenue share in 2025. This is due to the introduction of favorable government initiatives in the region.

- Asia Pacific is projected to register the highest CAGR of 10.2% during the projection period. The strong semiconductor ecosystem in countries like China and Taiwan is driving regional market growth.

- The cloud-based segment led the electronic design automation market with a 67.1% revenue share in 2025. It is because cloud-based EDA tools provide remote access to design software, resources, and computing capabilities.

- The semiconductor IP segment is projected to account for a CAGR of 9.8% during the forecast period. Semiconductor IP allows designers to avoid re-creating complex components.

The differences in the market-size estimates among research firms are mainly due to differences in scope, including the inclusion of IP licensing revenues and service components. They are also due to the differences in the methods used to forecast the semiconductor demand cycles.

Industry Dynamics

- This shift towards chiplet design software and 3D IC integration is creating the need for enhanced EDA tools to deal with these complex designs involving multiple chips and various technologies in a single system.

- Advances in technology in the field of EDA tools, like simulation, synthesis, and verification, are also one of the key EDA market drivers.

- Cloud-based EDA tools are creating fresh opportunities as they can access computing and collaboration.

- Licensing costs and the complexity of EDA tools may pose a challenge to the market, especially for SMEs and start-ups. Security risks of data in cloud computing are also a challenge.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

AI Impact on Electronic Design Automation Market

- AI in EDA is enhancing efficiency in design processes by reducing manual intervention and hastening development cycles.

- It facilitates greater accuracy in designs as errors are detected at earlier stages.

- AI allows firms to analyze various design possibilities, hence yielding better results.

- It enables faster time-to-market for firms in the semiconductor industry by improving overall design processes.

Electronic design automation (EDA) encompasses a set of software tools. These tools aid in the design, testing, and manufacturing of electronic and semiconductor devices. They are useful in the design of complex electronic devices, achieving high accuracy and efficiency. Some of the electronic devices designed using EDA are integrated circuits, printed circuit boards, and system-on-chip designs.

The EDA process flow often involves front-end design, verification, physical design, and sign-off. There has been an increase in chip complexity, especially at deeper nodes like 5nm and 3nm. This has made EDA tools critical for achieving performance and manufacturability.

The increase in the demand for semiconductors and the growth of the semiconductor industry itself create the need for advances in electronic design automation. The complexity of designing semiconductors has increased over the years. This has been addressed by the advances in EDA technology. The vendors of EDA technology invest heavily in R&D to launch products that meet the rising demands of the semiconductor industry.

The automotive industry is a major consumer of semiconductor chips. With the growing use of electronic components and advanced technologies in automobiles, such as ADAS, infotainment, and electric vehicle components, demand for semiconductor chips in the automotive sector is rising. To support this, EDA tools play a major role in the design and validation of automotive systems.

The rapid development of artificial intelligence, high-performance computing, and 5G technology is fueling the need for advanced semiconductor design. This is resulting in a higher adoption rate for EDA tools in the global market.

Market Dynamics

Growth Drivers

As integrated circuits become more advanced, the process of designing them is getting more complex. The demands for better performance, power consumption, and more features in smaller chips have added to this complexity. In this regard, EDA tools can help reduce this complexity, making it easier for designers to work more efficiently and reduce errors.

At the same time, there is an increased demand for high-end electronic devices in various industries. EDA tools can help meet this increasing demand while maintaining quality and performance.

The semiconductor industry is constantly evolving with new technologies and design methods. EDA tool vendors are also improving their tools to meet emerging trends such as IoT, AI, and 5G technologies. Improved simulation, verification, and design capabilities are making these tools even better and easier to use.

At the same time, the automotive and aerospace industries are becoming increasingly complex. The development of technologies such as cars, autonomous driving, and avionics is creating a requirement for better design and testing. This has led to the increased use of EDA tools in the industry.

Technology Trends

Some electronic design automation market technology trends include the use of AI in EDA, which helps speed up the design process while ensuring accuracy. Also, cloud-based EDA tools are gaining popularity, as remote teams can easily use them. Another technology trend is the use of chiplets in chip design. Here, chips are divided into smaller sections for better performance. Packaging technologies such as 2.5D and 3D are being used to improve performance while reducing the space required.

Source: Polaris Market Research Analysis

Market Segmentation

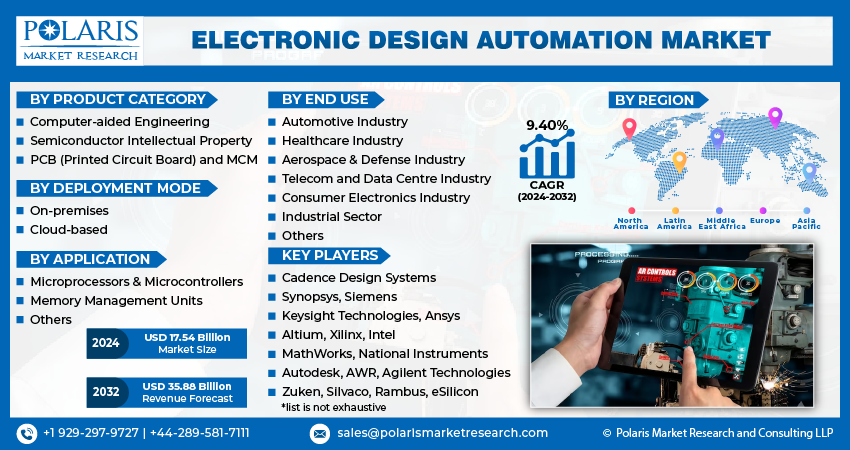

By Product Category Insights

Based on product category, the electronic design automation market is segmented into computer-aided engineering (CAE), semiconductor intellectual property (IP), printed circuit board (PCB) and multi-chip module (MCM), and services. The semiconductor IP segment is projected to witness the fastest growth with a 9.8% CAGR during the forecast period. With the growing complexity of semiconductor design, the requirement for pre-designed and pre-verified IP blocks is increasing. Semiconductor IP refers to the set of ready-to-use components like processor IPs, memory IPs, interface IPs, and application-specific IPs, which can be integrated into a custom chip design. The availability of a variety of IP blocks facilitates the design process by reducing the costs and time required to develop a chip.

Designers can avoid re-creating complex components through the use of Semiconductor IP. This not only saves designers’ time but also significantly cuts down on the overall cost of development. Designers can instead focus on integrating and optimizing the components, thus increasing overall design efficiency. The cost and time advantages offered by Semiconductor IP have been a major reason for its increased adoption, thus propelling its market growth.

By Deployment Mode Insights

Based on deployment mode, the market is segmented into on-premises and cloud-based. The cloud-based segment led the electronic design automation market with a 67.1% revenue share in 2025. These tools provide remote access to design software, resources, and computing capabilities over the internet from anywhere in the world. With such tools, the design team can collaborate efficiently without regard to their geographical location. Also, it is possible to scale up or scale down the required resources depending on the specific needs of the projects. Cloud-based EDA tools usually use a pay-as-you-go model. With such tools, it is not necessary to spend heavily on the infrastructure required for implementing EDA tools. The SMEs or start-ups with limited budgets prefer such tools. All these factors contribute to the segment’s leading market position.

By Application Insights

By application, the electronic design automation market segmentation is done into microprocessors & microcontrollers, memory management units, and others. The microprocessors & microcontrollers segment is projected to account for a larger revenue share in the coming years. The demand for high-performance microprocessors and microcontrollers is on the rise in different industry segments. These industries include consumer electronics, automotive, telecommunication, and industrial automation. These high-performance microprocessors and microcontrollers are used in a range of applications, including smartphones, laptops, IoT devices, and automotive electronics. The complexity in designing these high-performance microprocessors and microcontrollers is high. They require advanced EDA tools to design and verify their functionality.

By End User Insights

Based on end user, the electronic design automation market is segmented into automotive, healthcare, aerospace & defense, telecom and data center, consumer electronics, industrial sector, and others. The automotive segment is projected to witness the fastest growth during the projection period. The automotive industry has undergone a rapid transformation by adopting cutting-edge technologies such as electrification, autonomous driving, connectivity, and driver assistance. These technologies have increased the complexity of automotive designs, such as the development of complex electronic control units, in-vehicle networks, sensors, and communication systems.

EDA tools play an important role in the design, simulation, and verification of complex systems. The recent increase in the number of electric vehicles has brought new challenges in the design process. EDA tools help design power electronics, battery management systems, motor control systems, and other components for electric vehicles. Optimizing power efficiency, range, and charging infrastructure requires advanced EDA tools to meet the specific needs of electric vehicle design.

Source: Polaris Market Research Analysis

Regional Analysis

North America led the global electronic design automation market with over 49.80% revenue share in 2025. Government initiatives are opening new avenues for the market. The enforcement of the CHIPS and Science Act is boosting the growth of the EDA market in North America. Many companies have recently announced further investments in American semiconductor manufacturing due to the enactment of the CHIPS and Science Act of 2022. These investments in semiconductor manufacturing are driving demand for EDA tools and solutions. They are creating a conducive business environment for EDA companies operating in the region.

The Asia Pacific EDA market is projected to witness the highest CAGR of 10.2% during the forecast period. Countries like Taiwan, South Korea, and Japan have a strong semiconductor ecosystem. This is boosting growth in these regions. These countries are investing heavily in R&D, leading to the development of more advanced chips. As chip design complexity increases, the need for advanced EDA tools is growing. In China, the semiconductor industry's growth is boosting the EDA tools market. As the industry advances and designs more advanced chips, EDA tools for chip design, verification, and testing become necessary. This growth in China is fueling the overall development of the EDA tools market.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

The global electronic design automation market is dominated by a few key players, alongside specific vendors and semiconductor firms. Competition and cooperation in the EDA sector are affected by continuous innovations in chip design, the increasing complexity of integrated circuits, and the rising demand for high-end electronics.

A few of the key electronic design automation market players include Cadence Design Systems, Synopsys, Siemens (Siemens EDA), Keysight Technologies, Ansys, Altium, Zuken, Silvaco, Aldec, Dassault Systèmes, EMA Design Automation, Verific Design Automation, Sonnet Software, Sigasi, EDA Direct, Intel, AMD (including Xilinx), Microchip Technology, Infineon Technologies, onsemi (On Semiconductor), Lattice Semiconductor, Rambus, Cirrus Logic, Imagination Technologies, and eASIC Corporation.

Cadence Design Systems is a global market leader in electronic design solutions. It helps organizations in developing innovative products. Its products are diverse and help engineers design and improve electronics. Cadence is recognized for innovation and has a significant presence in the global semiconductor and electronics industry.

Synopsys provides software and services that make the design of electronic circuits easier and faster. Its products help engineers develop efficient, high-performance electronic chips for a range of products, including smartphones and cars. Synopsys is recognized for innovation and helps organizations keep pace with the evolving electronics industry.

List of Key Companies

- Aldec

- Altium

- AMD (including Xilinx)

- Ansys

- Cadence Design Systems

- Cirrus Logic

- Dassault Systèmes

- eASIC Corporation

- EDA Direct

- EMA Design Automation

- Imagination Technologies

- Infineon Technologies

- Intel

- Keysight Technologies

- Lattice Semiconductor

- Microchip Technology

- onsemi (On Semiconductor)

- Rambus

- Siemens (Siemens EDA)

- Sigasi

- Silvaco

- Sonnet Software

- Synopsys

- Verific Design Automation

- Zuken

Buyer Landscape

The main EDA buyers are fabless companies, IDMs, foundries, OEMs, and research institutions. These companies make use of EDA tools for designing and testing electronic products. Semiconductor companies and IDMs are mainly focused on developing new chips, while foundries and OEMs use the tools for production and quality control. Research institutions make use of EDA software for learning and innovation. These users have varying requirements, and hence EDA solutions are tailored to their needs and the size of their operations.

Recent Developments

- June 2025: Siemens Digital Industries Software introduced two new EDA tools: Innovator 3D IC and Calibre 3D Stress. These tools help develop 2.5D and 3D ICs by overcoming challenges in simulation, design, and long-term reliability.

- February 2025: Intel launched a dedicated website for its 18A process technology. The website features Ribbon FET transistors and PowerVia.

- December 2024: Samsung Semiconductor India Research has launched the "Chip Design for High School" program. This program will enable students in grades 6-12 to learn the basics of chip design.

- November 2024: Keysight Technologies introduced an EDA software suite. The company stated that the software suite uses AI and machine learning. It will help users increase productivity and simplify the design of RF devices.

- June 2024: Siemens Digital Industries Software and Intel Foundry collaborated to create a new EDA certification. The collaboration also focuses on enabling breakthroughs for embedded multi-die interconnect bridge technology.

Market Segmentation

By Product Category Outlook (Revenue, USD Billion, 2021–2034)

- Computer-aided Engineering (CAE)

- Semiconductor Intellectual Property (IP)

- PCB (Printed Circuit Board) and MCM (Multi-chip Module)

- Services

By Deployment Mode Outlook (Revenue, USD Billion, 2021–2034)

- On-premises

- Cloud-base

By Workflow Stage Outlook (Revenue, USD Billion, 2021–2034)

- Front-end design tools

- Verification tools

- Physical design tools

- Sign-off tools

- Packaging & system-level tools

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Microprocessors & Microcontrollers

- Memory Management Units

- Others

By End User Outlook (Revenue, USD Billion, 2021–2034)

- Automotive

- Healthcare

- Aerospace & Defense

- Telecom and Data Center

- Consumer Electronics

- Industrial Sector

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Electronic Design Automation Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 19.15 billion |

| Market Size in 2026 | USD 20.93 billion |

| Revenue Forecast by 2034 | USD 43.07 billion |

| CAGR | 9.4% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Electronic Design Automation Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Electronic Design Automation Market FAQ's

The market for electronic design automation stood at USD 19.15 billion in 2025. It is projected to reach USD 43.07 billion by 2034.

The market is projected to account for a CAGR of 9.4% between 2026 and 2034.

Electronic design automation refers to the software tools used for designing semiconductor chips and electronic systems.

The market for EDA is driven by growing demand from 5G and the semiconductor industry. The market is also benefiting from the growth of automotive electronics.

North America led the market in 2025. Government initiatives are opening new avenues for the market in the region.

EDA tools are used for chip design and verification.

The different types of EDA tools are simulation, verification, and PCB design.

Semiconductor IP (Intellectual Property) is a pre-designed, reusable building block for microchips.

A few of the leading market companies include Cadence Design Systems, Synopsys, Siemens (Siemens EDA), Keysight Technologies, Ansys, Altium, Zuken, Silvaco, Aldec, Dassault Systèmes, EMA Design Automation, Verific Design Automation, Sonnet Software, Sigasi, EDA Direct, Intel, AMD (including Xilinx), Microchip Technology, Infineon Technologies, onsemi (On Semiconductor), Lattice Semiconductor, Rambus, Cirrus Logic, Imagination Technologies, and eASIC Corporation.

Download Sample Report of Electronic Design Automation Market

Please fill out the form to request a customized copy of the research report.