Europe Epoxy Resins Market Growth Opportunities, Industry Revenue, 2025-2034

REPORT DETAILS

Market Statistics

Overview

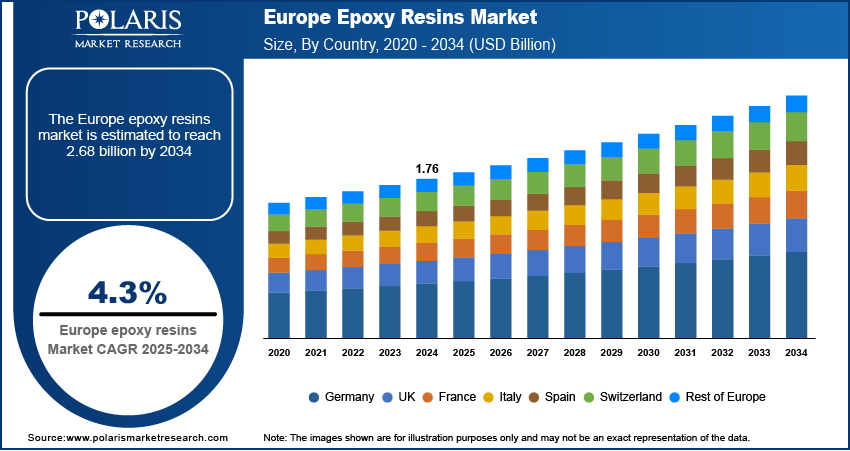

The Europe epoxy resins market size was valued at USD 1.76 billion in 2024, growing at a CAGR of 4.3% from 2025–2034. Key factors driving demand is strong presence of chemical giants and R&D centers, and green building initiatives and regulations.

Key Insights

- The DGBEA segment is expected to grow at a CAGR of 5.4% over the forecast period, supported by its versatility and superior mechanical and thermal properties, which align well with the stringent performance requirements of Europe’s automotive, aerospace, and electronics sectors.

- The construction segment captured a notable 7.1% revenue share in 2024, fueled by increasing use of epoxy resins in flooring, adhesives, sealants, and protective coatings across commercial and residential infrastructure projects.

- Germany accounted for 35.0% of the global epoxy resin market revenue in 2024, owing to its strong presence in the automotive and industrial manufacturing industries, which rely heavily on advanced resin technologies.

- France held an 11.33% share of the European epoxy resin market in 2024, driven by significant investments in infrastructure upgrades and the ongoing expansion of public transportation networks across major cities.

Industry Dynamics

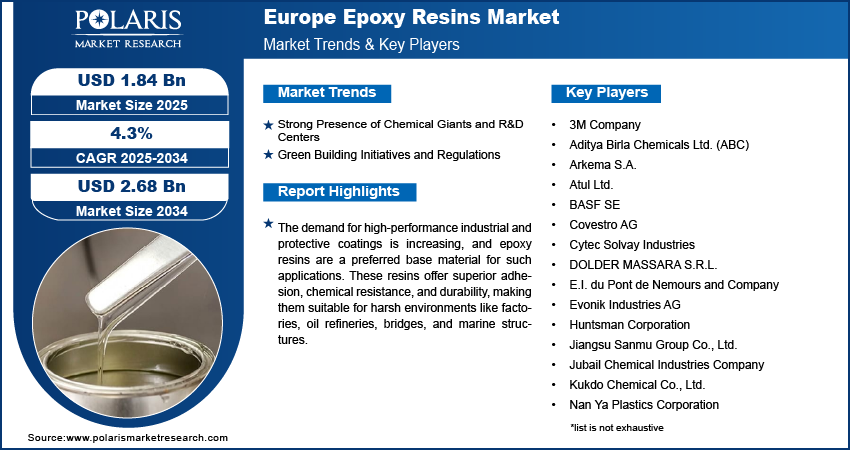

- Strong presence of chemical giants and R&D centers are driving the demand for epoxy resins.

- Green building initiatives and regulations is driving the Europe epoxy resins market

- The demand for high-performance industrial and protective coatings is increasing, and epoxy resins are a preferred base material for such applications.

- Fluctuating raw material prices and the growing popularity of alternative resins limits the growth.

Market Statistics

- 2024 Market Size: USD 1.76 Billion

- 2034 Projected Market Size: USD 2.68 Billion

- CAGR (2025-2034): 4.3%

- Germany: Largest Market Share

AI Impact on the Industry

- AI accelerates epoxy resin formulation by analyzing chemical properties, curing behaviors, and performance metrics to design resins with enhanced strength, flexibility, and thermal resistance.

- Integration of AI enables predictive modeling to optimize resin compositions and curing processes, reducing trial-and-error in R&D and shortening time-to-market.

- AI-powered market intelligence tools track industry trends, customer demands, and competitive landscapes, helping manufacturers align product offerings with evolving market needs.

- AI-driven automation improves supply chain and production workflows, enhancing quality control, minimizing defects, and reducing operational costs across epoxy resin manufacturing plants.

Epoxy resin is a type of thermosetting polymer known for its strong adhesive properties, chemical resistance, and durability. It is formed through the reaction of epoxide compounds with hardeners, creating a rigid, high-performance material. Commonly used in coatings, electronics, construction, and composites, epoxy resin provides excellent mechanical strength and environmental protection.

Europe’s electronics and electrical equipment industry, especially in countries like Germany and the UK, relies on epoxy resins for insulation, encapsulation, and circuit board protection. The shift toward electric vehicles, smart grids, and 5G infrastructure increases the need for reliable electrical components with high heat and chemical resistance. Epoxy resins are preferred due to their strong dielectric properties and ability to withstand harsh conditions. The EU’s drive for digital transformation and energy-efficient electronics directly contributes to rising epoxy resin applications in this sector, fueling the expansion.

Source: Polaris Market Research Analysis

Europe is one of the most mature and fastest-growing wind energy markets globally. Countries like Germany, the UK, and Spain are investing heavily in both onshore and offshore wind farms. Epoxy resins are crucial in manufacturing wind turbine blades due to their excellent mechanical strength, resistance to fatigue, and lightweight properties. The demand for epoxy-based composites used in wind turbines is expected to grow as the EU intensifies its renewable energy targets to achieve climate neutrality by 2050, thereby fueling the growth in the region.

Drivers & Opportunities

Strong Presence of Chemical Giants and R&D Centers: Europe is home to major chemical companies such as BASF, Covestro, and Solvay, which actively invest in epoxy resin innovation. These firms have well-established R&D hubs that continuously develop advanced resin formulations tailored for regional industries. Supportive regulatory frameworks, strong intellectual property protection, and access to skilled labor foster innovation. Furthermore, collaborations between chemical companies and universities in Germany, Switzerland, and the Netherlands accelerate the commercialization of new, sustainable epoxy technologies, including bio-based variants. This robust ecosystem fuels the growth of the industry.

Green Building Initiatives and Regulations: The European Union is a global leader in sustainability and green construction. Epoxy resins are heavily used in flooring, coatings, and adhesives in the construction sector due to their durability and chemical resistance. There is a growing push for eco-friendly construction materials with regulations like the Energy Performance of Buildings Directive (EPBD). Epoxy resins that offer low VOC emissions and improved insulation performance are increasingly in demand. The rise in infrastructure renovation projects and smart buildings across Western Europe is further contributing to growth for epoxy-based construction solutions, thereby fueling the growth.

Source: Polaris Market Research Analysis

Segmental Insights

Type Analysis

Based on type, the segmentation includes DGBEA, DGBEF, novolac, aliphatic, glycidylamine, and hardener. DGBEA segment is projected to grow at a CAGR of 5.4% over the forecast period driven by its versatility and excellent mechanical and thermal properties, making it highly suitable for Europe’s demanding industries like automotive, aerospace, and electronics. European manufacturers prefer DGBEA for its reliability in producing durable composites and coatings that comply with strict EU environmental and safety regulations. The ongoing demand for lightweight, high-performance materials in these sectors further supports the rising consumption of DGBEA-based epoxy resins.

DGBEF segment is expected to witness a significant share over the forecast period due to its superior chemical resistance and lower viscosity compared to other epoxy types. These properties make DGBEF highly attractive for specialized industrial applications such as coatings, adhesives, and electrical encapsulation. Europe’s stringent environmental norms and focus on sustainability further favor the use of DGBEF because it enables formulations with reduced volatile organic compounds (VOCs). The growing demand in the automotive and construction sectors for durable and eco-friendly materials is driving the adoption of DGBEF epoxy resins.

Application Analysis

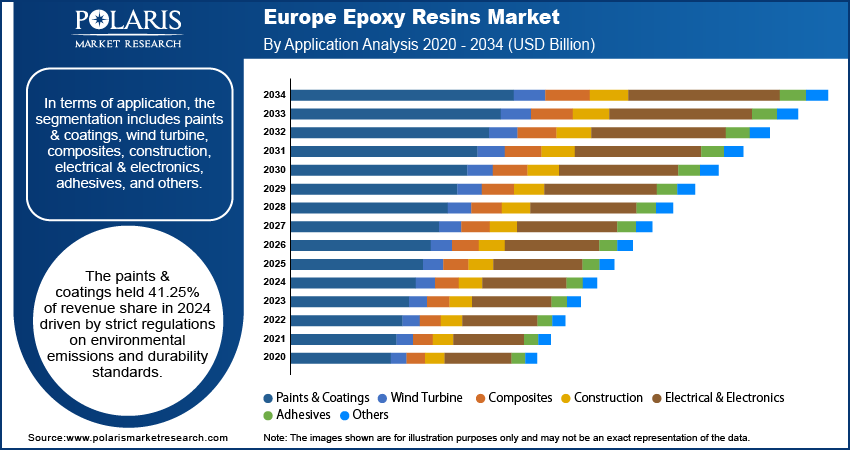

In terms of application, the segmentation includes paints & coatings, wind turbine, composites, construction, electrical & electronics, adhesives, and others. The paints & coatings held 41.25% of revenue share in 2024 driven by strict regulations on environmental emissions and durability standards. Epoxy resins are widely used in industrial coatings, flooring, and protective layers due to their excellent adhesion, chemical resistance, and corrosion protection. The surge in infrastructure upgrades, renewable energy installations, and industrial automation has increased the need for high-performance coatings. Additionally, the growing emphasis on sustainable and low-VOC formulations aligns with Europe’s green initiatives, further boosting epoxy resin usage in the coatings industry.

The construction segment held significant revenue share in 2024, holding 7.1% driven by rising demand for flooring, adhesives, sealants, and protective coatings. Epoxy resins are favored for their strong bonding, durability, and resistance to moisture and chemicals with increasing renovation and infrastructure development projects across countries like Germany, France, and the UK. European building regulations emphasize energy efficiency and environmental safety, encouraging the use of epoxy resin-based materials that improve thermal insulation and reduce maintenance costs. Moreover, the growing trend toward sustainable construction and smart buildings propel epoxy resin adoption in this sector.

Source: Polaris Market Research Analysis

Country Analysis

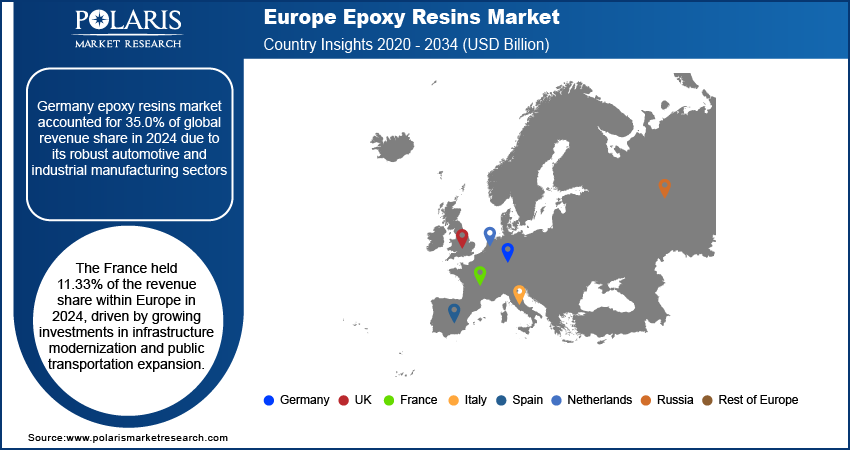

Germany epoxy resins market accounted for 35.0% of global revenue share in 2024 due to its robust automotive and industrial manufacturing sectors. The country’s strong focus on high-quality engineering and innovation drives demand for epoxy resins in automotive components, machinery, and electrical insulation. Additionally, Germany’s commitment to sustainable construction and renewable energy projects boosts epoxy resin use in coatings and flooring applications. Strict environmental regulations further push manufacturers to adopt low-VOC, durable epoxy formulations, further boosting growth.

France Epoxy Resins Market Insight

The France held 11.33% of the revenue share within Europe in 2024, driven by growing investments in infrastructure modernization and public transportation expansion. The rising need for durable coatings, adhesives, and sealants in construction and aerospace sectors drives demand. France’s increasing adoption of eco-friendly building materials and stringent safety standards encourage the use of advanced epoxy resins with superior chemical resistance and longevity. Moreover, the country’s focus on green technologies and energy-efficient buildings supports epoxy resin applications in sustainable construction, thereby driving the growth.

UK Epoxy Resins Market

The market in UK is expected to register a CAGR of 3.4% during the forecast period by its expanding aerospace, automotive, and construction industries. Post-Brexit infrastructure development projects and government investments in renewable energy systems are drives the growth. Epoxy resins’ role in protective coatings, adhesives, and composite materials aligns with the UK’s drive for high-performance and environmentally friendly solutions. Additionally, growing demand for rapid curing and durable resins in flooring and industrial applications accelerates growth in the country.

Netherlands Epoxy Resins Market Overview

The demand for epoxy resin in Netherlands is rising due to its strong maritime, construction, and electronics sectors. Increasing infrastructure projects, especially in flood control and urban development, require high-performance epoxy coatings and sealants resistant to harsh environments. The country’s commitment to sustainability encourages the use of low-VOC and eco-friendly epoxy formulations. Furthermore, rapid industrialization and growth in renewable energy installations drive epoxy resin use in protective and insulating materials, thereby driving the growth.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis

The Europe epoxy resin market features a competitive landscape with key global and regional players striving for technological innovation and market expansion. Major companies such as BASF SE, Arkema S.A., Evonik Industries AG, and Covestro AG lead the market with strong manufacturing capabilities and advanced R&D infrastructure. These firms focus on sustainable product development, low-VOC formulations, and high-performance epoxy systems tailored for Europe's stringent environmental regulations and growing demand in automotive, construction, and wind energy sectors. Additionally, companies like Solvay SA, Sika AG, and Atul Ltd. are enhancing their footprint through collaborations, acquisitions, and product diversification. European players benefit from proximity to major end-use industries, skilled labor, and a strong regulatory framework promoting green chemistry. Competition is also intensifying with Asian manufacturers like Nan Ya Plastics and Kukdo Chemical expanding their presence in Europe. Overall, the market is marked by innovation, sustainability efforts, and strategic partnerships across the value chain.

Key Players

- 3M Company

- Aditya Birla Chemicals Ltd. (ABC)

- Arkema S.A.

- Atul Ltd.

- BASF SE

- Covestro AG

- Cytec Solvay Industries

- DOLDER MASSARA S.R.L.

- E.I. du Pont de Nemours and Company

- Evonik Industries AG

- Huntsman Corporation

- Jiangsu Sanmu Group Co., Ltd.

- Jubail Chemical Industries Company

- Kukdo Chemical Co., Ltd.

- Momentive Performance Material (MPM) Holding LLC

- Nan Ya Plastics Corporation

- Olin Corporation

- Sika AG

- Sinopec Bailing Petrochemical Company, Ltd.

- SIR INDUSTRIALE S.p.A

- Solvay SA

Industry Developments

In March 2025, BASF and Sika launched a new epoxy hardener, Baxxodur EC 151, designed for flooring coatings. The product delivered high gloss, fast curing, low VOC emissions, and enhanced durability, supporting sustainability and performance in industrial and commercial flooring applications.

In April 2024, Westlake Corporation launched a new series of epoxy products engineered to minimize yellowing. This initiative reflects the company’s focus on delivering high-performance materials that satisfy the rising requirements of sectors such as electronics, automotive, and construction. By tackling yellowing issues, Westlake seeks to improve both the durability and visual quality of epoxy resins, ensuring compliance with increasingly strict industry standards.

In October 2023, Robnor ResinLab, a prominent epoxy formulator, introduced PX806C, its newest bio-based epoxy resin. This development demonstrates the company’s dedication to sustainability, assisting customers in creating eco-conscious products while fostering a more environmentally responsible supply chain.

Europe Epoxy Resins Market Segmentation

By Type Outlook (Volume, Kilo Tons, Revenue, USD Billion, 2021–2034)

- DGBEA

- DGBEF

- Novolac

- Aliphatic

- Glycidylamine

- Hardener

By Application Outlook (Volume, Kilo Tons, Revenue, USD Billion, 2021–2034)

- Paints & Coatings

- Wind Turbine

- Composites

- Construction

- Electrical & Electronics

- Adhesives

- Others

By Country Outlook (Volume, Kilo Tons, Revenue, USD Billion, 2021–2034)

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

Europe Epoxy Resins Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 1.76 Billion |

| Market Size in 2025 | USD 1.84 Billion |

| Revenue Forecast by 2034 | USD 2.68 Billion |

| CAGR | 4.3% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2021–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Volume in Kilo Tons, Revenue in USD Billion and CAGR from 2025 to 2034 |

| Report Coverage | Volume Forecast, Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Country Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, and segmentation. |

Source: Polaris Market Research Analysis

Europe Epoxy Resins Market FAQ's

The market size was valued at USD 1.76 billion in 2024 and is projected to grow to USD 2.68 billion by 2034.

The market is projected to register a CAGR of 4.3% during the forecast period.

Germany dominated the market in 2024

A few of the key players in the market are 3M Company; Aditya Birla Chemicals Ltd. (ABC); Arkema S.A.; Atul Ltd.; BASF SE; Covestro AG; Cytec Solvay Industries; DOLDER MASSARA S.R.L.; E.I. du Pont de Nemours and Company; Evonik Industries AG; Huntsman Corporation; Jiangsu Sanmu Group Co., Ltd.; Jubail Chemical Industries Company; Kukdo Chemical Co., Ltd.; Momentive Performance Material (MPM) Holding LLC; Nan Ya Plastics Corporation; Olin Corporation; Sika AG; Sinopec Bailing Petrochemical Company, Ltd.; SIR INDUSTRIALE S.p.A; Solvay SA.

The DGBEA segment dominated the market revenue share in 2024.

The construction segment is projected to witness the fastest growth during the forecast period.

Download Sample Report of Europe Epoxy Resins Market

Please fill out the form to request a customized copy of the research report.