Global Ferrosilicon Market Trends, Share & Research Report, 2026-2034

REPORT DETAILS

Ferrosilicon Market Summary

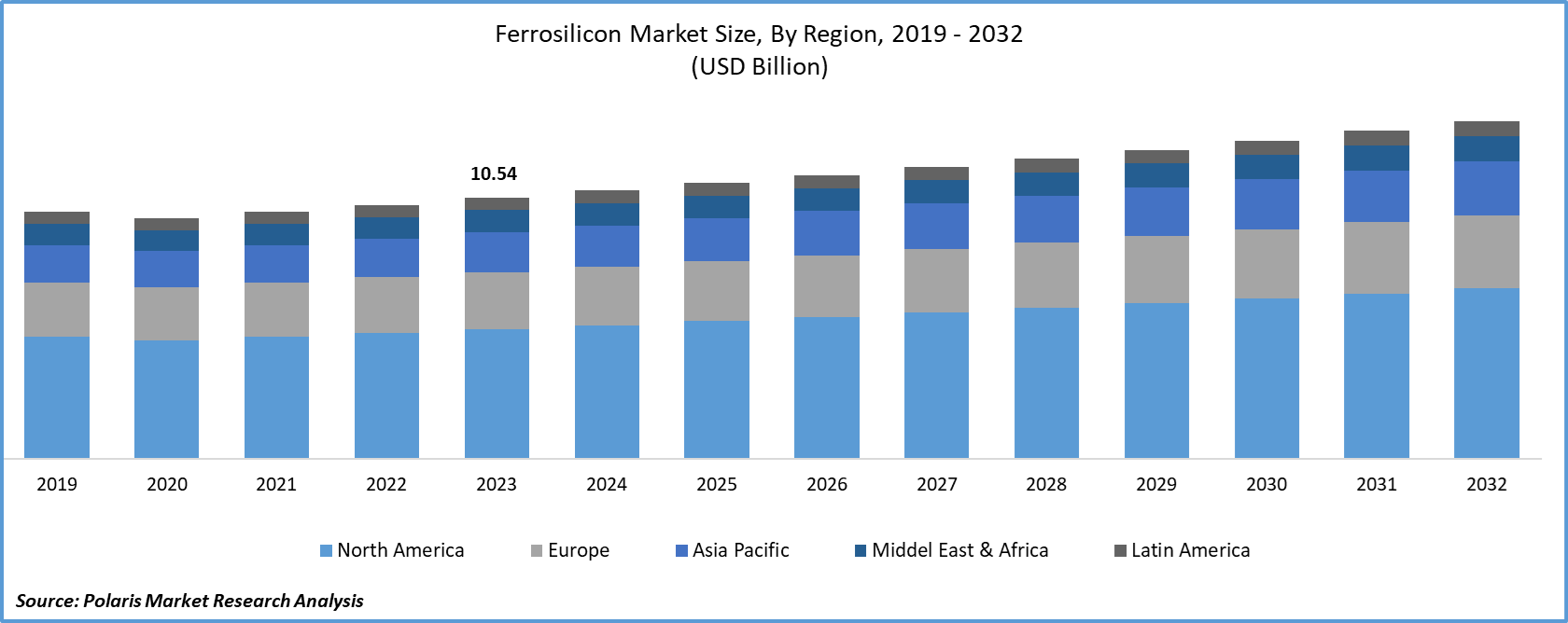

Global ferrosilicon market size was valued at USD 11.05 billion in 2025 and is projected to exhibit a compound annual growth rate (CAGR) of 2.9% during the forecast period (2026 - 2034). Increase in production capacity, growth in steel production, and growing automotive sales is fueling the growth.

Market Statistics

Key Takeaways

-

North America led with a 22.36% revenue share in 2025. This is due to the presence of a well-established steel industry in the region.

- Asia Pacific is projected to grow at a 3.1% CAGR. Rapid industrialization in emerging economies such as China and India contributes to the regional market growth.

- The deoxidizer segment led with a 72.15% revenue share in 2025. Deoxidizers are widely used to remove oxygen from molten steel and improve the quality of the final steel product.

- The cast iron segment is projected to witness significant growth at a 3.4% CAGR. This is due to the rising demand for high-quality cast iron across various sectors.

- The atomized ferrosilicon segment dominated with a 68.43% revenue share in 2025. This is because atomized ferrosilicon is highly favored in the steel and foundry industries.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The rising production capacity of ferrosilicon across countries is contributing to the market demand.

- The growing global demand for steel across sectors such as construction and automotive is fueling market development.

- Increased demand for customized alloy compositions to create lightweight components is expected to present market opportunities.

- High energy costs and intensity associated with ferrosilicon may hinder market growth

Ferrosilicon (FeSi) is an iron-silicon alloy used in the steelmaking process for deoxidation and as an alloying agent. The growth in infrastructural developments globally drives the ferrosilicon market growth. Also, the rise in population has resulted in heightened investment in residential and commercial infrastructures. For instance, in May 2024, the United States spent around USD 120.76 billion on commercial construction, according to the U.S. Census Bureau. The increasing spending on infrastructural projects is creating the need for efficient steel solutions. Thus, ferrosilicon, an essential alloying agent and deoxidizer in steel production becomes critical to meet this growing demand. Consequently, the emphasis on modernization and expansion of infrastructure ensures demand for ferrosilicon, resulting in its market growth.

Source: Polaris Market Research Analysis

Furthermore, the ferrosilicon market is driven by the growing automobile production that demands high-quality steel for vehicle production. For instance, according to the International Organization of Motor Vehicle Manufacturers, in 2022, the total number of vehicles manufactured in the Asia Pacific region was 55,115,837 units. The production of modern automobiles requires advanced steel grades infused with ferrosilicon for various components, including the chassis, body panels, and engine parts, to ensure safety, performance, and fuel efficiency. Additionally, the growing consumer interest in electric vehicles, which rely on lighter and stronger materials, is increasing the need for specialized steel made with ferrosilicon. As a result, the rising demand for ferrosilicon-based steel from automobile manufacturers is fueling the market expansion.

Core Uses of Ferrosilicon in Metallurgy

Ferroalloys: Ferrosilicon belongs to the group of ferroalloys, which are essential for enhancing the characteristics of metals in the process of steel making. Ferroalloys have become indispensable in contemporary metallurgy.

Steel Deoxidation: One of the key roles of ferrosilicon is that it deoxygenates molten steel, thus improving the quality of the end product.

Alloying Process: The alloy can be added in the process of steel making to enhance its strength and resistance to corrosion. Various types of alloys are employed depending on end application requirements.

Foundry Applications: In foundries, ferrosilicon is utilized for inoculating cast iron and thus improving its structure and workability

Market Trends

Increased Production Capacity of Ferrosilicon is Fueling the Market Growth

Market CAGR for ferrosilicon is driven by the increased production capacity of ferrosilicon across countries. Manufacturers and governments are investing in expanding production facilities and adopting advanced technologies. For instance, in May 2024, Kanat Sharlapayev, the Minister of Industry and Construction in Kazakhstan, announced plans for the construction of an international plant dedicated to the production of ferrosilicon, with a projected annual production capacity of 160,000 tonnes. This expansion in production capacity ensures a stable supply of ferrosilicon, i.e., crucial for the steel manufacturing sector. Furthermore, enhanced production capabilities lead to economies of scale, reducing production costs and making ferrosilicon more accessible and affordable for end-users. Thus, the production of ferrosilicon in larger quantities at low cost drives the growth of the ferrosilicon market outlook.

Growth in Steel Production Worldwide

Steel production is dependent on ferrosilicon, which is used as a deoxidizer and alloying agent to improve the quality, strength, and durability of steel. The global demand for steel is driven by several industries, including construction, automotive, oil and gas, and industrial machinery. Thus, steel-producing companies, including China Baowu Group, ArcelorMittal, Ansteel Group, Nippon Steel Corporation, and Tata Steel Group, are increasing the production of crude steel to meet the growing demand from the aforementioned industries. For instance, according to the World Steel Association, global crude steel production totaled 1,892.2 million tonnes in 2023, an increase of 0.1% from the 2022 production of 1,890.2 million tonnes. The surge in steel production necessitates an increased supply of ferrosilicon to meet the stringent quality and performance standards. Thus, the growing steel production to meet the industrial demand directly boosts the ferrosilicon market size.

Source: Polaris Market Research Analysis

Atomized vs Milled Ferrosilicon

| Type | Form | Benefits | Application |

| Atomized Ferrosilicon | Spherical particles/ granular form | Good flow characteristics | Dense medium separation, metallurgy |

| Milled Ferrosilicon | Powdered material form | Simple to blend and reacts well | Welding, chemistry and alloy manufacture |

Source: Polaris Market Research Analysis

Segment Insights

Ferrosilicon Application Insights

The global ferrosilicon market segmentation, based on application, includes deoxidizers, inoculants, and others. In 2025, the deoxidizer segment held the largest market share in the global market as it is widely used to remove oxygen from molten steel and improve the quality of the final steel product. Furthermore, there is a heightened use of ferrosilicon for the deoxidization of iron and steel. For instance, according to Anyang Xinlongsen Metallurgical Material Co. Ltd., more than 90% of the annual ferrosilicon production is used for deoxidation purposes globally. Thus, the increased utilization of ferrosilicon in steel and iron production for the deoxidization process is contributing to the dominance of the deoxidizer segment in the global ferrosilicon market.

Ferrosilicon End-Use Insights

The global ferrosilicon market segmentation, based on end-use, includes carbon & other alloy steel, cast iron, electric steel, stainless steel, and others. The cast iron segment of the ferrosilicon (FeSi) market is expected to grow significantly over the forecast period due to the increasing demand for high-quality cast iron in various industries, including automotive, construction, mining, and defense.

Furthermore, the increasing production of cast iron is expected to drive the demand for ferrosilicon. For instance, in 2019, China smelted 809.37 million tons of cast iron, which is 5.33% more than the preceding year. This rising production of cast iron underscores the growing demand for ferrosilicon to prevent the formation of carbide in iron, which results in the significant growth of the cast iron segment of the ferrosilicon market.

Source: Polaris Market Research Analysis

Regional Insights

By region, the study provides the ferrosilicon market insights into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The North America ferrosilicon market held the highest revenue share due to the presence of a well-established steel industry. For instance, according to the World Steel Association, North America produced 93.6 million tonnes of steel in 2023. The region's advanced production capabilities and technological innovations in steel manufacturing enhance the use of ferrosilicon as a deoxidizer and alloying agent. In addition, the presence of major steel producers, such as United States Steel Corporation, Kloeckner Metals Corporation, Nucor Corporation, Steel Dynamics, and Cleveland-Cliffs Inc., is bolstering the production of high-quality steel. Thus, the increased consumption of ferrosilicon by steel manufacturers contributed to the dominance of North America in the global market.

Further, the major countries studied in the market report are the US, Canada, German, France, the UK, Italy, Spain, China, Japan, India, Australia, South Korea, and Brazil.

Asia Pacific ferrosilicon market is expected to grow with a significant CAGR over the forecast period in the global market due to rapid industrialization in countries such as China and India. The countries are investing heavily in infrastructure projects, including commercial buildings and manufacturing facilities, which require large quantities of steel. For instance, according to a report by the Boston University Global Development Policy (GDP) Center, from 2013 to 2021, China allocated a total of USD 331 billion in funds to various countries as a part of its Belt and Road Initiative to construct pipelines, roads, and railroads across the world. Thus, the significant investments by countries such as China, India, and Japan in infrastructure projects across various nations are expected to bolster the Asia Pacific ferrosilicon market.

Japan's ferrosilicon market is expected to grow significantly during the forecast period due to its growing consumption of steel for several applications, including construction, shipbuilding, automobiles, industrial machinery, and electrical machinery. For instance, according to the Nippon Steel Corporation, Japan's total consumption of ordinary steel products was 43,670 metric tonnes in 2021. The heightened consumption of steel in the country underscores the rising demand for ferrosilicon, consequently driving the growth of the ferrosilicon market in the country.

Source: Polaris Market Research Analysis

Key Market Players & Competitive Insights

Leading market players are investing heavily in research and development in order to expand their offerings, which will help the ferrosilicon market grow even more. Market participants are also undertaking a variety of strategic activities to expand their global footprint, with important market developments including innovative product launches, international collaborations, higher investments, and mergers and acquisitions between organizations. To expand and survive in a more competitive and rising market climate, the ferrosilicon industry must offer cost-effective solutions.

The ferrosilicon market faces competition from major global players, fueled by rising demand from the steel and cast iron industries. The major players dominate the market with their extensive production capacities and advanced technologies. Competition is further heightened by fluctuating raw material prices, stringent environmental regulations, and the necessity for technological advancements to improve efficiency and reduce emissions. Major players in the ferrosilicon market, including Anyang Jinfang Metallurgy Co., Ltd., Anyang Yuneng Metallurgy Refractory Co., Ltd., DMS Powders, Elkem ASA, Eurasian Resources Group, Ferroglobe, FINNFJORD AS, OM Holdings Ltd., RFA International, and SINOGU INDUSTRY CO., LTD.

Elkem ASA is a global provider of advanced material solutions, operating across three segments, including Silicon Products, Silicones, and Carbon Solutions. The company's offerings include a wide range of silicone polymers, such as silicone compounds, oils, greases, emulsions, and resins. In addition, Elkem provides a variety of silicon-based materials, including silicon powder/micronized silicon, ferrosilicon, silica fume/micro-silica, and grain refiners. In June 2022, Elkem ASA acquired KeyVest Belgium S.A, a distributor specializing in ferrosilicon nitride, boron carbide, fused silica, and aluminum powder. The acquisition aimed to broaden Elkem ASA's product portfolio and establish a foundation for further expansion.

OM Holdings Limited is a global company involved in the mining, smelting, trading, and marketing of manganese ores and ferroalloys. The company's operations are divided into the Mining, Smelting, and Marketing and Trading segments. It possesses and manages the Bootu Creek manganese ore mine situated in Australia's Northern Territory. In addition to this, the company is engaged in the production and trading of ferrosilicon, silicon metal, manganese sinter ore, and manganese alloys. In October 2021, OM Holdings Limited reported an increase in production volumes for ferrosilicon, manganese alloys, and manganese sinter ore at its ferroalloy smelter unit in Samalaju Industrial Park, Malaysia.

Key Companies:

- Anyang Jinfang Metallurgy Co., Ltd.

- Anyang Yuneng Metallurgy Refractory Co., Ltd.

- DMS Powders

- Elkem ASA

- Eurasian Resources Group

- Ferroglobe

- FINNFJORD AS

- OM Holdings Ltd.

- RFA International

- SINOGU INDUSTRY CO., LTD

Future of Ferrosilicon Market

The ferrosilicon industry is forecast to gain momentum driven by increasing demand for steel, growing infrastructure investment, and rising automobile manufacturing. The rising need for higher-quality steel across industries will further boost consumption. Rising demand for electric vehicle components, casting operations, and sophisticated engineering will drive market growth. Upgrading manufacturing plants and expanding manufacturing capacity in developing nations is expected to present new opportunities.

Industry Developments

- December 2024: Nyato Dukam, Industries Minister of Arunachal Pradesh, India, inaugurated a state-of-the-art ferrosilicon production facility at the Industrial Growth Centre in Niglok, East Siang district. The initiative aims to strengthen domestic ferrosilicon output while driving regional economic development and generating new employment opportunities. (Source: timesofindia.indiatimes.com)

Market Segmentation

Ferrosilicon Type Outlook

- Atomized Ferrosilicon

- Milled Ferrosilicon

Ferrosilicon Application Outlook

- Deoxidizer

- Inoculants

- Others

Ferrosilicon, End-Use Outlook

- Carbon & Other Alloy Steel

- Cast Iron

- Electric Steel

- Stainless Steel

- Others

Ferrosilicon Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Report Scope

| Report Attributes | Details |

| Market size value in 2025 | USD 11.05 billion |

| Market size value in 2026 | USD 11.36 billion |

| Revenue Forecast in 2034 | USD 14.24 billion |

| CAGR | 2.9% from 2026 – 2034 |

| Base Year | 2025 |

| Historical Data | 2021 – 2024 |

| Forecast Period | 2026 – 2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Ferrosilicon Market FAQ's

The global ferrosilicon market size was valued at USD 11.05 billion in 2025 and is projected to grow to USD 14.24 billion by 2034.

The global market is projected to grow at a CAGR of 2.9% during the forecast period, 2026-2034.

North America had the largest share of the global market.

The key players in the market are Anyang Jinfang Metallurgy Co.,Ltd, Anyang Yuneng Metallurgy Refractory Co., Ltd., DMS Powders, Elkem ASA, Eurasian Resources Group, Ferroglobe, FINNFJORD AS, OM Holdings Ltd., RFA International, and SINOGU INDUSTRY CO., LTD.

The deoxidizer category held the highest share of the market in 2025.

The cast iron segment had the highest CAGR in the global market.

Ferrosilicon is an alloy of iron and silicon mainly used in steelmaking and foundry applications.

This material is used for deoxidizing, alloying, inoculating cast iron, refining magnesium, and manufacturing welding materials.

Ferrosilicon is usually made in electric arc furnaces through silica and iron sources under high temperatures.

There are different types of ferrosilicon depending on the silicon content and industrial applications.

Download Sample Report of Ferrosilicon Market

Please fill out the form to request a customized copy of the research report.