Fiber Optics Market Research Report, Share and Forecast, 2026 – 2034

REPORT DETAILS

Fiber Optics Market Summary

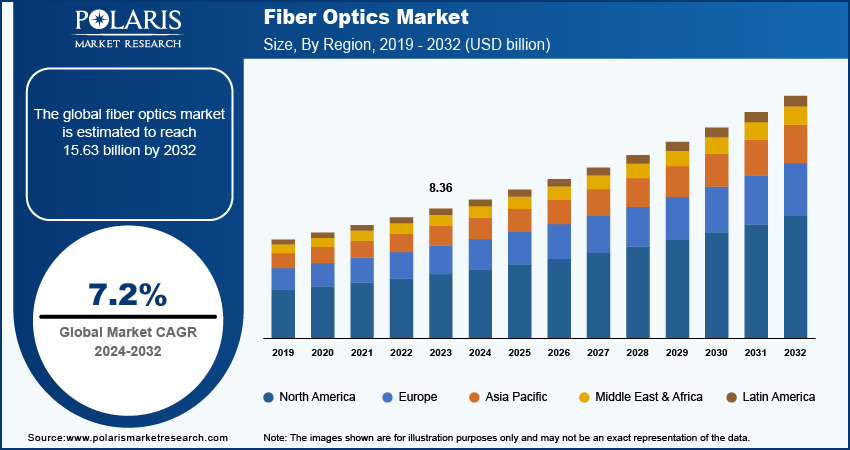

The global fiber optics market size was valued at USD 10.18 billion in 2025 and is expected to register a CAGR of 8.3% from 2026 to 2034. Growth is driven by expanding broadband infrastructure and increasing demand for high-speed data converters. Rising technological investments and the surging penetration of 5G networks also propel the industry expansion.

Market Statistics

Key Takeaways

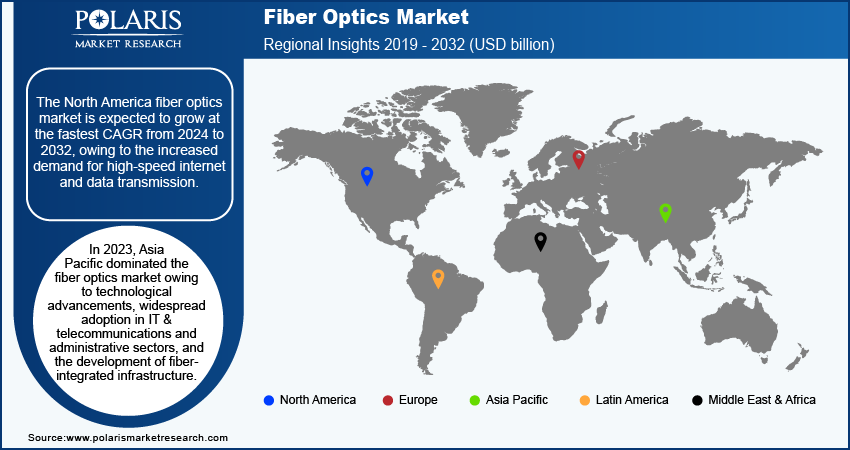

- Asia Pacific fiber optics market led with a 33.55% revenue share in 2025 due to rapid advancements, widespread adoption across information technology, telecommunications, and government sectors, and the development of integrated infrastructure.

- The North America fiber optics market is expected to grow at the highest rate of 9.1% owing to increasing demand for fast internet connectivity services.

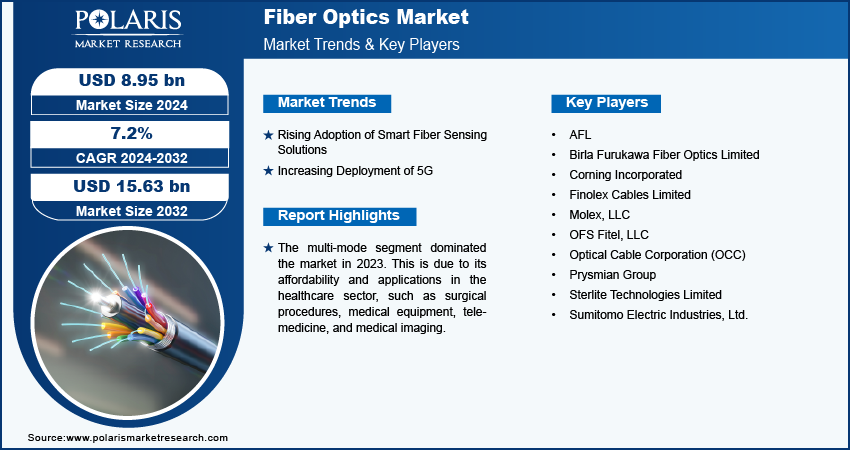

- The multi-mode segment dominated with a 56.3% revenue share in 2025 owing to its low cost and widespread use in short-distance, high-bandwidth environments such as hospitals/

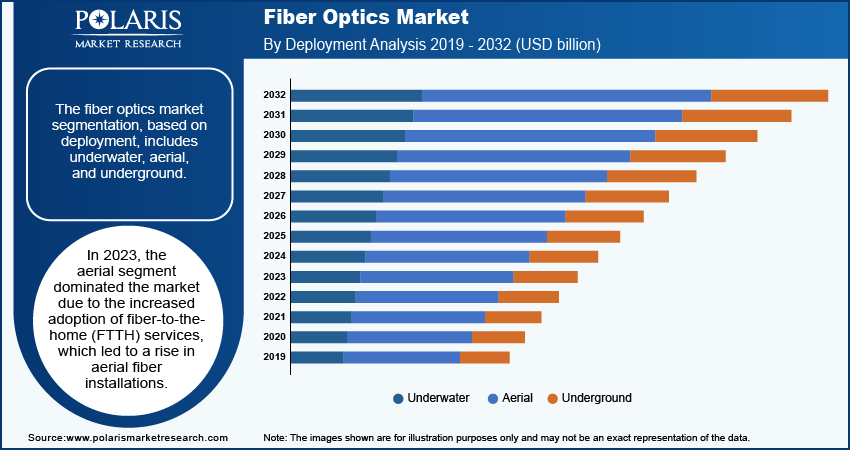

- The aerial segment held 32.1% market share in 2025. Rapid growth at in FTTH fiber deployment continues to support aerial installations.

- The underground segment is projected to witness rapid growth at a 9.1% CAGR. The use of underground fiber optic cable is becoming the preferred choice in densely populated cities.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The rising adoption of smart fiber-sensing solutions is driving market expansion.

- The widespread deployment of 5G in advanced and emerging countries fuels the industry growth.

- The increasing demand for fiber optic cables as a replacement for copper cables is expected to create lucrative opportunities during the forecast period.

- The growing adoption of wireless communication systems hinders market growth.

Source: Polaris Market Research Analysis

The fiber optic market is also known as the fiber optic industry or optical fiber market. The fiber optics industry has several uses for the efficient transmission of data at high speeds through different networks. Fiber optics technology supports various critical applications, which include telecommunication, medical care, industry, and the defense sector. When compared to copper wire networks, fiber optic communication networks provide higher bandwidth and longer transmission distance.

The fiber optics market involves the production and sale of specialized cables and components for high-speed, long-distance data transmission, a crucial component of telecommunications. The market is expanding rapidly, especially due to increased demand for high-speed internet and wire-based broadband connectivity. Additionally, the growing use of the internet and increasing data traffic are driving demand for new fiber cables.

Large companies are also expanding their manufacturing capacity to meet the growing demand for fiber-optic devices. This involves constructing fiber-drawing towers and manufacturing the required glass preforms for fiber optic production. For instance, in February 2024, Finolex Cables invested 580 crore rupees to establish a new manufacturing plant. In response to increased demand for last-mile connectivity driven by the 5G rollout, Finolex Cables expanded its capacity for optical fibre cables from 4 million fiber km to 10 million fiber km.

How Fiber Optics Works?

Fiber optic cables work by changing electrical signals into light pulses using a transmitter like lasers and LEDs. The pulses then travel down the fiber optic cable using total internal reflections. The receiver at the other end detects the pulses and changes them into electrical signals again. This allows for fast and low-loss data transmission compared to copper cables.

Market Dynamics

Rising Adoption of Smart Fiber Sensing Solutions

The fiber optics market is driven by the ever-expanding use of smart fiber-sensing solutions. These technologies are capable of real-time monitoring down the length of an optical fiber. Tools such as DFOS and FBG can detect temperature, strain, pressure, and even vibration with very high precision over long distances.

Smart fiber sensing solutions are therefore applied in the oil and gas industry, civil engineering, and healthcare, among other contexts. Applications include continuous monitoring of infrastructure, pipelines, and patient condition, thereby ensuring safe and efficient operations at a cost-effective price.

In the oil and gas industry, such sensors are used to detect leaks in oil and gas pipes. Otherwise, they can lead to costly failures. An example was seen in March 2024, when Sonatrach, the Algerian oil firm, began implementing an intelligent inspection system for oil pipes using Huawei technology.

The transition from fiber-optic technology to copper cables is currently opening robust growth opportunities across various industries. The displacement of copper cables by fiber optics is facilitated by the distinct advantages fiber optics offers, such as greater bandwidth, reduced signal attenuation, enhanced security, and lower maintenance costs. With the upgrade of their communications infrastructure, fiber optics is emerging as an ideal long-term investment for organizations.

Fiber Optics vs Copper Cable: Key Performance Comparison

| Comparison Metric | Fiber Optics | Copper Cable |

| Bandwidth Capacity | Very high, supports large data volumes | Limited performance drops at high data loads |

| Data Transmission Speed | Extremely fast, suitable for high-speed networks | Slower compared to fiber optics |

| Signal Loss | Minimal signal attenuation over long distances | Higher signal loss, especially over long distances |

| Transmission Distance | Long-distance transmission without repeaters | Shorter distances require signal boosters |

| Security | High security, difficult to tap | More vulnerable to interception |

| Resistance to Interference | Immune to electromagnetic interference | Susceptible to electromagnetic interference |

| Maintenance Requirements | Low maintenance, long operational life | Higher maintenance and frequent upgrades |

| Installation Cost | Higher initial cost | Lower initial cost |

| Long-Term Cost Efficiency | Cost-effective over time | Higher long-term operational costs |

Source: Polaris Market Research Analysis

Increasing Deployment of 5G

The fiber optics market is experiencing significant growth, driven by the widespread deployment of 5G in both advanced and emerging markets. This trend is creating favorable opportunities for fiber optics suppliers in the industry.

The deployment of 5G networks relies on the utilization of optical fibers by organizations and industries, which can transmit large volumes of data at rapid speeds over long distances. Telecommunications companies are installing additional 5G base stations to stay ahead of the competition as 5G services are rolled out commercially.

For instance, in March 2022, the Ministry of Industry and Information Technology (MIIT) announced that China had installed almost 1.425 million 5G base stations. This highlighted how quickly 5G technology expanded in China. These stations require deploying fiber-optic networks and are expected to accommodate network traffic for more than 500 million users across China, thereby driving market revenue.

Real-World Use Cases

- Telecom operators implement fiber optic systems to provide broadband internet (FTTH).

- Data centers utilize fiber optics for their cloud computing and server-to-server communication needs.

- Hospitals leverage fiber optics in performing medical imaging and minimal invasion surgeries.

- Smart cities utilize fiber networks for traffic surveillance and other Internet of Things applications.

- Oil operators use fiber-optic sensors to monitor pipeline integrity problems.

What is Key Restraint in Fiber Optics Market?

High Costs and Implementation Issues Hampering the Market

High installation costs and the complexity of implementing fiber optic networks are major hindrances to the fiber optics market. This is because implementing fiber requires significant investment, especially for underground or long-distance deployments. Furthermore, issues related to infrastructure, governmental policies, or the need for specialized technical experts may also hinder implementation.

Source: Polaris Market Research Analysis

Market Segment Insights

By Cable Type Insights

The segmentation, based on cable type, includes multi-mode and single-mode. The multi-mode segment dominated the fiber optics market in 2025. This is due to its affordability and its applications in the healthcare sector, including surgical procedures, medical equipment, telemedicine, and medical imaging. Also, its versatility helps improve quality, effectiveness, and clarity in medical practices. Multi-mode fiber optics is widely used for critical operations because of its cost-effectiveness and higher bandwidth. Thus, key players in the market are expanding their offerings to meet growing demand across sectors.

For example, OFS launched the LaserWave Dual-Band OM4+ Multi-mode Optical Fiber in January 2024. This new offering, along with their current OM4 and OM5 fibers, raises the bandwidth and performance standards.

The single-mode fiber market is a major one, as it is used extensively for long-distance data transmission, in telecom backbones, and for 5G backhaul. The ability of single-mode fibers to transport light over longer distances with little signal degradation is essential for broadband projects and cross-border connectivity projects. The rising investment in high-speed telecommunications links is another major factor driving the global use of single-mode fibers.

By Deployment Insights

The segmentation, based on deployment, includes underwater, aerial, and underground. In 2025, the aerial segment dominated the market due to increased adoption of fiber-to-the-home (FTTH) services, driving a rise in aerial fiber installations. Aerial fiber optic deployment offers quick installation and lower repair and maintenance costs. Hence, telecommunication companies are deploying aerial fiber networks for their cost-effectiveness, rapid deployment, and flexibility. For instance, in January 2022, Orange S.A. extended its FTTH coverage to around 63% of the 29 million FTTH-eligible premises in France. The expansion was mainly aerial, resulting in a 20% increase in coverage.

The use of underground fiber optic cable is becoming the preferred choice in densely populated cities. This method provides stronger security, a longer lifespan, and resistance to weather conditions. Governments are adopting underground solutions for smart city initiatives and metro development to ensure safe network connectivity.

Submarine fiber optic cables are the backbone of international data connectivity. These enable high-speed data transfer between continents. The escalating need for cloud services and data centers worldwide is driving demand for submarine fiber-optic cable connections.

The use of underground fiber optic cable is becoming the preferred choice in densely populated cities. This method provides stronger security, a longer lifespan, and resistance to weather conditions. Governments are adopting underground solutions for smart city initiatives and metro development to ensure safe network connectivity.

Submarine fiber optic cables are the backbone of international data connectivity. These enable high-speed data transfer between continents. The escalating need for cloud services and data centers globally is driving demand for submarine fiber optic cable connections.

Source: Polaris Market Research Analysis

Regional Insights

By region, it offers market insights for North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The fiber optics market in North America is expected to be the fastest-growing between 2026 and 2034. The rise in 5G backhaul fiber demand, smart city development, and the adoption of IIoT technology across industries have driven fiber-optic infrastructure development in North America.

The fiber optics industry in the US is quite robust, as investment and acquisition deals have been announced between telecom and tech companies. Demand for fiber optics is also increasing in the healthcare and defense sectors.

For instance, in February 2024, Sterlite Technologies signed an agreement with Lumos to build 100% fiber optic internet infrastructure in the United States. Sterlite Technologies will provide specialized, purpose-built optical fiber cable designs to fulfill Lumos' network needs in the mid-Atlantic regions.

In 2025, the Asia Pacific fiber optics market led, bolstered by technological advancements, increased uptake in the IT, telecom, and government sectors, and robust development in fiber optic infrastructure. Also fueling the industry's expansion in the forecast period are evolving government broadband initiatives in Asia Pacific. For instance, in January 2022, the Indian government announced the merger of Bharat Sanchar Nigam Ltd (BSNL) and Bharat Broadband Network Ltd (BBNL) to establish the largest optical fiber cable (OFC) network across 16 states. This merger will grant BSNL full authority over BBNL's extensive 5.67 lakh km optical fiber network.

Several governments also collaborated with industry players to deploy underwater fiber optic cables and enhance their product offerings in the Asia Pacific region. For instance, in January 2024, Alphabet collaborated with the Chilean government to build the first undersea fiber optic cable linking South America and Asia Pacific. The fiber optic cable will have a capacity of 144 terabytes and a 25-year lifespan.

Source: Polaris Market Research Analysis

Key Players & Competitive Insights

Leading players are investing heavily in research and development to expand their product lines, further driving market growth. Fiber optics market participants are also undertaking a variety of strategic activities to expand their global footprint, including new product launches, contractual agreements, mergers and acquisitions, increased investments, and collaborations with other organizations. To expand and survive in a more competitive and rising market climate.

Manufacturing locally to minimize operational costs is one of the key business tactics used by manufacturers to benefit clients and increase the sector. In recent years, the market has offered some technological advancements. Major players include AFL; Birla Furukawa Fiber Optics Limited; Corning Incorporated; Finolex Cables Limited; Molex, LLC; OFS Fitel, LLC; Optical Cable Corporation (OCC); Prysmian Group; Sterlite Technologies Limited; and Sumitomo Electric Industries, Ltd.

Prysmian Group operates as a major player in the energy and telecommunications cable market. Prysmian Group designs, manufactures, and installs various cables and systems. The major product types offered by Prysmian Group include high- and medium-voltage cables, optical fibers, copper cables, submarine cables, and connectivity components. Prysmian operates numerous subsidiaries, including Prysmian Cables & Systems Ltd. and Prysmian Cables y Sistemas de México. In October 2021, Prysmian Group renewed its partnership agreement with Openreach for an additional three years. With the renewed alliance, Prysmian Group will offer its innovation and expertise to assist Openreach in implementing its enhanced Full Fiber broadband in the UK by 2025.

Sumitomo Electric Industries, Ltd. is a global manufacturer specializing in electric wire and optical fiber cables. The firm operates in five principal business areas: automotive, information and communications, energy and environment, electronics, and industrial materials. Its business areas include wiring harnesses, automotive hoses, telecomm cables, optical devices, and power systems. Sumitomo Electric has a global presence in more than 40 countries across the Americas, Africa, Europe, the Middle East, and the Asia Pacific. In November 2021, Sumitomo introduced the ITU-T G. 654. E optical fibers and cables as part of its PureAdvance series. These products include ultra-low-loss optical fibers and cables specifically designed for broadband applications.

Future Outlook for Fiber Optics Market

The market for fiber optics is anticipated to witness robust growth owing to the proliferation of 5G, cloud computing, and artificial intelligence-based data centers. The need for networks that offer high speed and low latency is driving the usage of fiber optics. There would also be a rise in demand from smart cities and Internet of Things (IoT) solutions. Ongoing improvements in cost-efficient manufacturing will support large-scale infrastructure growth worldwide.

List of Key Companies

- AFL

- Birla Furukawa Fiber Optics Limited

- Corning Incorporated

- Finolex Cables Limited

- Molex, LLC

- OFS Fitel, LLC

- Optical Cable Corporation (OCC)

- Prysmian Group

- Sterlite Technologies Limited

- Sumitomo Electric Industries, Ltd.

Fiber Optics Industry Developments

- November 2025: Crown Fiber Optics announced it secured over USD 100 million in multi-year fiber infrastructure contracts. These contracts include new projects in New Mexico and Washington. They also encompass expansions in the Pacific Northwest. (source: globenewswire.com)

- October 2025: Fraunhofer IIS announced the development of SpikeHERO, which aims to design a chip based on artificial intelligence that incorporates both optical and electrical processing techniques in spiking neural networks for fiber-optic networks. The objective is to enhance signal quality and boost data transmission through the integration of brain-inspired SNN technology into fiber infrastructure. (source: iis.fraunhofer.de)

- January 2025: TECNO unveiled the latest Starry Optical Fiber Technology for the first time at this year's innovation festival, CES 2025, a unique technology integrating ultra-thin optical fibers and mini-LEDs into smartphone battery covers for enhancing design and power-saving in new models such as PHANTOM V Flip2 5G. (Source: www.prnewswire.com)

- May 2024: Runaya, a leading manufacturer of optical fiber cable components, outlined plans to increased production. The company stated that the move is aimed at acheiving significant export growth. It will also focus on reaching revenue of Rs 500 crore over the next 3-4 years. (Source: economictimes.indiatimes.com)

- February 2024: HFCL has set up a manufacturing unit in Poland for optical fiber cables with an output capacity of 3.25 million fiber km to meet emerging demand in Europe. (Source: www.prnewswire.com)

Fiber Optics Market Segmentation

By Fiber Type Outlook

- Plastic

- Glass

By Cable Type Outlook

- Multi-mode

- Single-mode

By Deployment Outlook

- Underwater

- Aerial

- Underground

By Application Outlook

- Medical

- Railway

- Oil & Gas

- Telecom

- Military & Aerospace

- BFSI

- Others

By Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Fiber Optics Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 10.18 Billion |

| Market Size in 2026 | USD 10.99 Billion |

| Revenue Forecast by 2034 | USD 20.87 Billion |

| CAGR | 8.3% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

Company Profiles/Industry participants profiling includes company overview, financial information, product/service benchmarking, and recent developments |

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

The fiber optics market comprises the manufacturing, distribution, and implementation of optical fiber cables and associated components for the long-distance transmission of data via light signals. The market includes fiber optic cables, sensing fibers, and implementation solutions, but does not include active components such as routers and switches. In this manner, the market can be clearly distinguished from related markets, such as optical transceivers and networking components.

Fiber Optics Market FAQ's

The global fiber optics market is expected to reach USD 20.87 billion by 2034, growing at a CAGR of 8.3%.

The multi-mode segment leads the market. This is due to its affordability and its applications in the healthcare sector.

The major market uses are telecommunications, data centers, 5G networks, medical equipment, and automation, with telecommunications accounting for the largest share of fiber usage.

The Asia Pacific fiber optics market is growing rapidly owing to massive 5G network investments, smart city projects, government-led broadband initiatives across various nations, and intensified digital transformation in China, India, and Japan.

The difficulty of installation on challenging terrain, the physical fragility of fiber cables, the high cost of deployment, and competition from wireless networks are challenges facing this market.

The aerial segment held the largest share of the market in 2025.

Fiber optics is a technology using specialized cables to transmit data at high speeds via light signals, supporting telecommunications, medical care, defense, and industrial applications with greater bandwidth than copper wires.

Key trends include rising adoption of smart fiber-sensing solutions for real-time infrastructure monitoring, and the widespread global deployment of 5G networks driving increased demand for high-speed optical fiber infrastructure.

Download Sample Report of Fiber Optics Market

Please fill out the form to request a customized copy of the research report.