Flexible Endoscopes Market Size, Share & Forecast Report 2026-2034

REPORT DETAILS

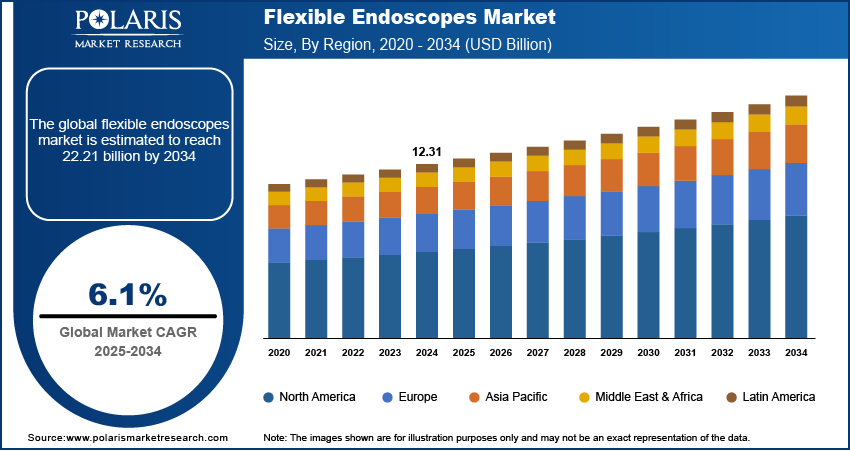

Flexible Endoscopes Market Summary

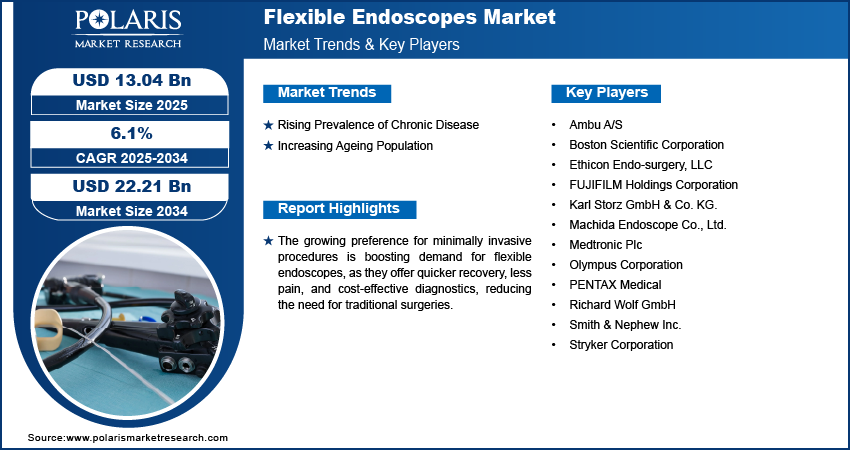

The global flexible endoscopes market size was valued at USD 13.04 billion in 2025. The market is projected to grow at a CAGR of 6.10% from 2026 to 2034. The growth is driven by the rising prevalence of chronic disease and an aging population. The market is also benefiting from the shift toward minimally invasive surgeries.

Market Statistics

Key Takeaways

- North America led with a 40.2% market share in 2025. This is owing to the presence of advanced healthcare infrastructure and high adoption of minimally invasive procedures in the region.

- Asia Pacific is expected to witness significant growth at a 6.9% CAGR. This is due to increasing healthcare investments and the rising prevalence of chronic diseases.

- The gastrointestinal endoscopes segment held the largest market share of 46.8% in 2025. These endoscopes are widely used for diagnosing and treating gastrointestinal tract conditions.

- The ureteroscopes segment is expected to witness significant growth at a 7.3% CAGR. This is owing to increasing cases of urinary tract disorders and the growing adoption of minimally invasive urological procedures.

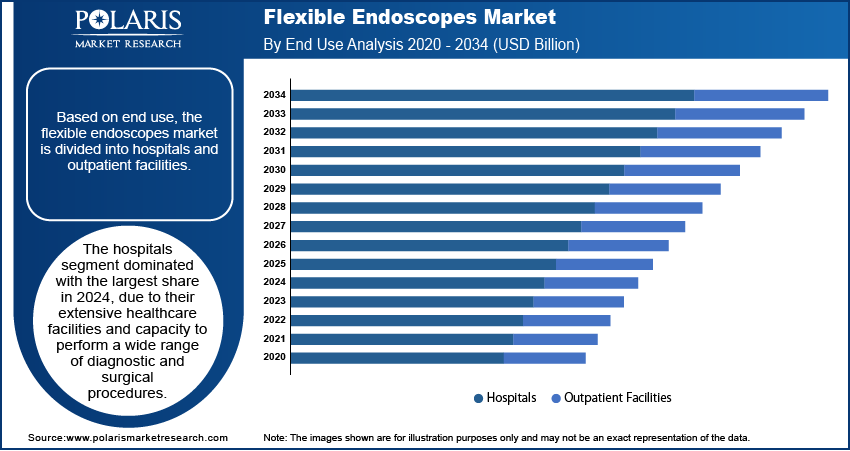

- The hospitals segment dominated with the largest share of 69.1% in 2025. The segment’s dominance is attributed to its extensive healthcare facilities and capacity to perform a wide range of diagnostic and surgical procedures.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The rising prevalence of chronic diseases has resulted in increased demand for flexible endoscopes for diagnosing and monitoring these conditions.

- The growing global aging population is another factor contributing to the development of the market.

- The shift towards single-use disposable scopes to prevent cross-contamination is expected to create several market opportunities.

- High capital investments needed for advanced imaging systems may present market challenges.

AI Impact on Flexible Endoscopes Market

- AI increases the efficiency of flexible endoscopy through effective image processing and accurate disease diagnosis.

- AI helps medical practitioners detect irregularities such as polyps, lesions, and even cancer in early stages.

- AI makes work faster because it carries out some processes, including automatically taking pictures.

- AI ensures good health outcomes for patients through accurate detection and treatment.

Flexible endoscopes are thin, bendable medical instruments equipped with a light and camera, used to visually examine the inside of the body’s hollow organs and cavities. They allow doctors to diagnose and sometimes treat conditions without making large incisions.

Patients and healthcare providers are increasingly preferring minimally invasive procedures due to quicker recovery times, less pain, and lower complication risks. Flexible endoscopes enable these less invasive examinations and treatments by allowing access to internal organs through natural body openings. This reduces the need for traditional surgeries, encouraging hospitals to invest in flexible endoscopy equipment. The demand for flexible endoscopes is growing as the healthcare industry shifts toward patient-friendly, cost-effective solutions.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Technological improvements have made flexible endoscopes smaller, more flexible, and equipped with better imaging capabilities such as high-definition and 3D visuals. These advances make procedures more accurate and safer, encouraging more doctors to use flexible endoscopes. Innovations such as better sterilization methods and disposable endoscopes further reduce infection risks, making these devices more appealing to hospitals. The demand for flexible endoscopes is growing as technology continues to evolve, thereby driving the industry growth.

Flexible vs Rigid Endoscopes

| Factor | Flexible Endoscope | Rigid Endoscope |

| Flexibility | Extremely flexible | Rigid construction |

| Maneuverability | Ability to move through curvatures | Convenient for straight path navigation |

| Patient Comfort | Higher patient comfort | May lead to discomfort |

| Application | Gastroenterology, pulmonary, urological, and ENT surgery | Surgery in orthopedics, laparoscopy, etc. |

| Internal Navigation | Has access to hard-to-reach internal sites | Unable to reach deep and internal sites in curved anatomy |

| Purpose | Used mainly for diagnosis and minimally invasive procedures | Used during surgical procedures |

Industry Dynamics

Rising Prevalence of Chronic Disease

Chronic diseases such as gastrointestinal disorders, respiratory illnesses, and urological conditions are becoming more common worldwide. According to the National Institute of Diabetes, Digestive and Kidney Disease, 60 to 70 million people are affected by all kinds of digestive diseases annually. Flexible endoscopes are used in diagnosing and monitoring these conditions by allowing doctors to observe internal parts of the body without surgery. Hospitals and clinics perform more endoscopy procedures as more people suffer from these illnesses, driving demand for flexible endoscopes.

Increasing Aging Population

The global population is aging, and older adults are more likely to suffer from diseases that require endoscopic examination, such as colon cancer and chronic digestive issues. According to Eurostat, as of 2024, 21.6% of Europe's population is aged 65 years and above. The growing elderly population increases the need for regular screening and minimally invasive diagnostic procedures. Flexible endoscopes offer a safer, less painful option for these patients compared to traditional surgery. Therefore, the demand for flexible endoscopes rises as healthcare systems prepare to meet the needs of aging populations and improve their quality of life.

Single-Use and Disposable Endoscope Trends

Disposable and single-use flexible endoscopes are increasingly favored in hospitals, clinics, and ambulatory facilities as health care professionals are making efforts to ensure their patients' safety through minimizing possible infections. Contrary to reusable endoscopes, disposable endoscopes are only used once and then discarded. This helps eliminate the necessity of cleaning and sterilizing the instrument before another use, thus minimizing cross-contamination and nosocomial infections. Moreover, disposable endoscopes can simplify the work of health care institutions and guarantee the availability of a new endoscope for each procedure performed. It is expected that due to high prioritizing of infection control practices and search for efficiency, demand for single-use endoscopes will be further increased.

Source: Polaris Market Research Analysis

Segmental Insights

By Product Analysis

The gastrointestinal endoscopes segment holds the largest share of 46.8% in 20245 as they are widely used to diagnose and treat digestive tract conditions such as ulcers, polyps, and cancers. These endoscopes allow doctors to observe esophagus, stomach, and intestines with ease, helping in early detection and minimally invasive treatment. The high prevalence of gastrointestinal diseases globally and growing awareness about routine screening procedures boost the gastrointestinal endoscopes segment growth.

The ureteroscopes segment is expected to witness significant growth of CAGR 7.3% during the forecast period, due to increasing cases of urinary tract disorders, especially kidney stones and strictures. These flexible endoscopes are designed specifically to navigate the urinary tract, allowing doctors to diagnose and treat problems with minimal discomfort. The rising incidence of kidney stones and other urological conditions, along with advances in ureteroscopy technology, has boosted their adoption. Additionally, the growing focus on minimally invasive urological procedures is driving the segment growth.

By End Use Analysis

The hospitals segment dominated with the largest share of 69.1% in 2025 due to their extensive healthcare facilities and capacity to perform a wide range of diagnostic and surgical procedures. They handle the highest patient volumes and have specialized departments for gastroenterology, pulmonology, and urology that extensively use flexible endoscopes. Hospitals invest heavily in advanced medical technologies to provide comprehensive care, which keeps the demand for flexible endoscopes consistently high. Their capability to offer emergency and complex procedures is further driving the segmental growth.

The outpatient facilities segment is expected to witness significant growth as more endoscopic procedures shift to these settings for cost-efficiency and convenience. These centers offer diagnostic and minor treatment services without requiring overnight hospital stays, appealing to patients and providers alike. Improvements in flexible endoscope technology allow safe and effective procedures in outpatient clinics, encouraging their increased use. The rising trend of ambulatory care services and preference for less invasive, quicker procedures outside hospitals are driving the growing adoption of flexible endoscopes in outpatient facilities.

Source: Polaris Market Research Analysis

Regional Analysis

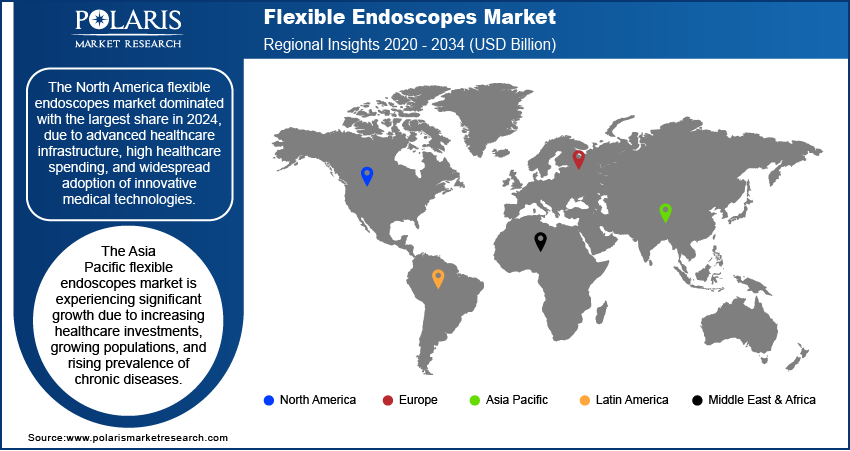

The North America flexible endoscopes market dominated with the largest share of 40.2% due to advanced healthcare infrastructure, high healthcare spending, and widespread adoption of innovative medical technologies. The region has a large patient base with chronic diseases such as cancer and gastrointestinal disorders that require endoscopic procedures. Strong government support for healthcare and growing awareness about preventive screenings drive demand. Additionally, the presence of key players and ongoing research and development activities contribute to the market growth. North America’s well-established healthcare system and preference for minimally invasive procedures further drive the industry growth in the region.

The Asia Pacific flexible endoscopes market is expected to witness significant growth of CAGR 6.9% during the forecast period, due to increasing healthcare investments, growing populations, and rising prevalence of chronic diseases. Improving healthcare infrastructure in countries such as China, Japan, and South Korea is boosting access to advanced medical devices. Additionally, rising health awareness and expanding health insurance coverage encourage more people to undergo diagnostic procedures. The region further benefits from a large patient pool requiring gastrointestinal and urological examinations, thereby driving the market growth.

The India flexible endoscopes market is growing due to expanding healthcare infrastructure and increasing government initiatives to improve medical services. The rising prevalence of lifestyle-related diseases such as diabetes and gastrointestinal disorders is driving demand for diagnostic tools such as flexible endoscopes. Growing awareness among patients and doctors about early disease detection and minimally invasive procedures supports growth in demand. Additionally, private hospitals and outpatient clinics are increasingly investing in advanced endoscopy equipment. India’s large population and improving access to healthcare facilities are further boosting the market growth.

Source: Polaris Market Research Analysis

The Europe flexible endoscopes market is expected to grow significantly during the forecast period due to well-developed healthcare systems and high adoption of advanced medical technologies. Countries such as Germany, France, and the UK are investing significantly in healthcare, supporting widespread use of endoscopic procedures for diagnosis and treatment. The aging population in Europe is driving the demand for routine screenings and minimally invasive interventions. Strict regulatory standards ensure high-quality medical devices, fostering innovation in the region. Europe’s focus on improving patient outcomes and increasing healthcare awareness is further fueling the growth of the industry.

Key Players and Competitive Analysis

The flexible endoscope market is highly competitive, dominated by established medical technology leaders such as Olympus Corporation, Karl Storz GmbH & Co. KG, and FUJIFILM Holdings Corporation, known for their innovative imaging technologies and broad product portfolios. Key players such as Medtronic Plc, Boston Scientific Corporation, and Smith & Nephew Inc. compete by expanding endoscopic capabilities and improving ergonomics. Emerging firms such as Machida Endoscope Co., Ltd. and Ambu A/S focus on single-use and disposable endoscopes to address infection control concerns. Companies such as PENTAX Medical; Ethicon Endo-surgery, LLC; Richard Wolf GmbH; and Stryker Corporation further intensify competition through advanced features, clinical support, and strategic partnerships to capture market share globally.

Key Players

- Ambu A/S

- Boston Scientific Corporation

- Ethicon Endo-surgery, LLC

- FUJIFILM Holdings Corporation

- Karl Storz GmbH & Co. KG.

- Machida Endoscope Co., Ltd.

- Medtronic Plc

- Olympus Corporation

- PENTAX Medical

- Richard Wolf GmbH

- Smith & Nephew Inc.

- Stryker Corporation

Industry Developments

May 2026: FUJIFILM Healthcare Americas Corporation announced that its ELUXEO 8000 Endoscopic Imaging System, coupled with its EG-840TP ultra slim therapeutic gastroscope, received the “Best New Endoscopy Technology Solution” award in the 10th annual MedTech Breakthrough Awards program. (source: fujifilm.com).

Flexible Endoscopes Market Segmentation

By Product Outlook (Revenue, USD Billion, 2021–2034)

- Bronchoscopes

- Laparoscopes

- Laryngoscopes

- Otoscopes

- Ureteroscopes

- Cystoscopes

- Nasopharyngoscopes

- Rhinoscopes

- Arthroscopes

- Neuroendoscopes

- Hysteroscopes

- Gynecology Endoscopes

- Gastrointestinal Endoscopes

- Colonoscope

- Gastroscope (Upper GI Endoscope)

- Duodenoscope

- Enteroscope

- Sigmoidoscope

By End Use Outlook (Revenue, USD Billion, 2021–2034)

- Hospitals

- Outpatient Facilities

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Flexible Endoscopes Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 13.04 Billion |

| Market Size Value in 2026 | USD 13.87 Billion |

| Revenue Forecast by 2034 | USD 22.21 Billion |

| CAGR | 6.1% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Flexible Endoscopes Market FAQ's

The global market size was valued at USD 13.04 billion in 2025 and is projected to grow to USD 22.21 billion by 2034.

The global market is projected to register a CAGR of 6.1% during the forecast period.

North America dominated the market with 40.2% share in 2025.

A few of the key players in the market are Ambu A/S; Boston Scientific Corporation; Ethicon Endo-surgery, LLC; FUJIFILM Holdings Corporation; Karl Storz GmbH & Co. KG.; Machida Endoscope Co., Ltd.; Medtronic Plc; Olympus Corporation; PENTAX Medical; Richard Wolf GmbH; Smith & Nephew Inc.; and Stryker Corporation.

The gastrointestinal endoscope segment dominated the market with 46.8% share in 2025.

The outpatient facilities segment is expected to witness the significant growth during the forecast period.

Download Sample Report of Flexible Endoscopes Market

Please fill out the form to request a customized copy of the research report.