Flexible Substrates Market Growth Opportunity 2026-2034

REPORT DETAILS

Flexible Substrates Market Summary

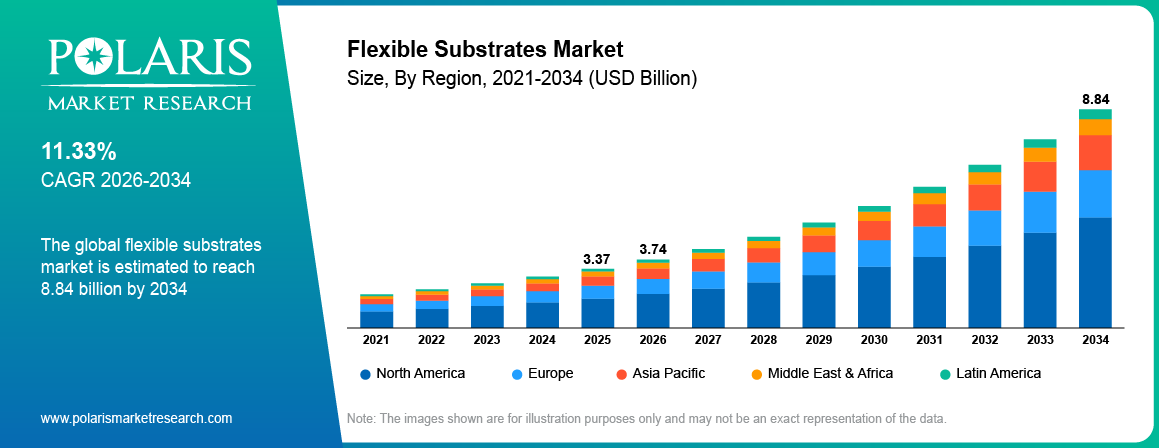

The global flexible substrates market is estimated around USD 3.37 Billion in 2025,with consistent growth anticipated during 2026–2034. This growth is driven by increasing adoption of flexible electronics, foldable displays, wearable medical devices, and advanced semiconductor packaging technologies. The market is projected to grow at a CAGR of 11.33% during the forecast period.

Market Statistics

Key Takeaways

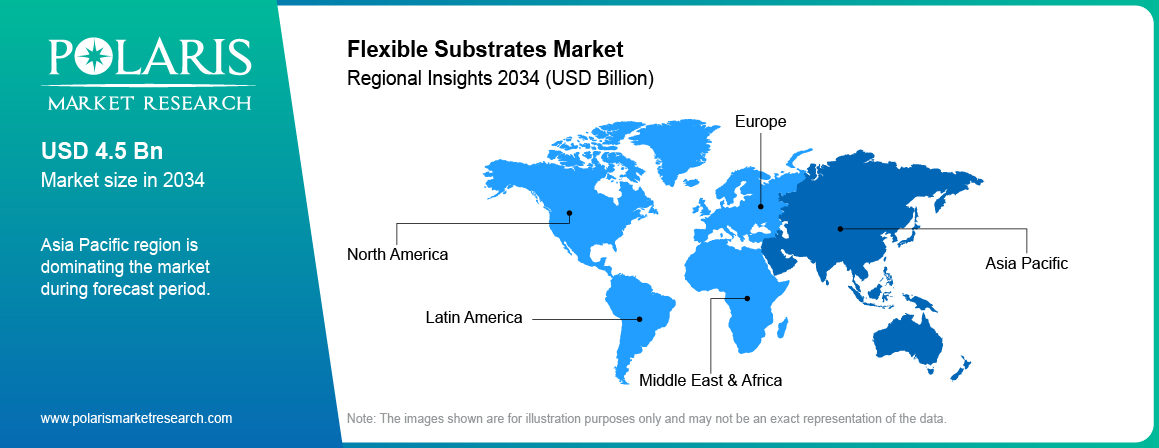

- Asia Pacific dominated the flexible substrates market in 2025, accounting for approximately 47.36% of the total market share due to strong electronics manufacturing activities across China, Japan, and South Korea.

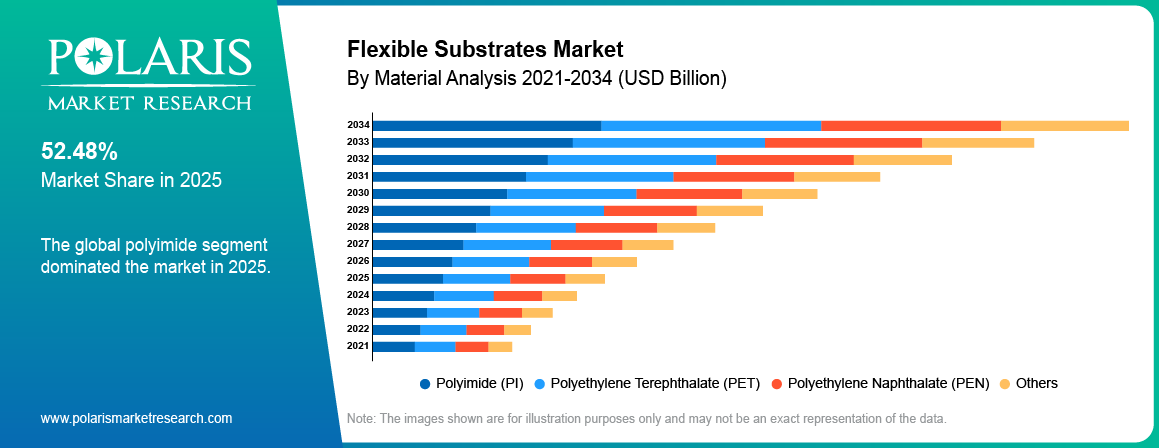

- The polyimide segment dominated the market in 2025, holding nearly 52.48% market share owing to its superior thermal stability, flexibility, and widespread use in OLED displays and semiconductor packaging.

- The flexible displays segment accounted for approximately 44.17% market share in 2025 driven by growing demand for foldable smartphones, wearable displays, and advanced smart display systems.

- Flexible printed circuit boards segment is projected to grow at the fastest CAGR of 12.84% during the forecast period due to increasing adoption in compact electronics, wearable devices, automotive electronics, and next-generation flexible display applications.

- Major companies operating in the market include 3M, DuPont, Kolon Industries, LG Chem, Sumitomo Chemical Co., Ltd., and Toray Industries.

Industry Dynamics

- Rising adoption of foldable electronics and smart wearable devices supports market growth.

- Increasing investments in OLED display manufacturing drive market expansion.

- High manufacturing and coating costs continue to create operational challenges.

- Expansion of printable electronics and smart packaging technologies creates market opportunities.

What is Flexible Substrates?

Flexible substrates are thin and bendable materials used in electronic circuits, displays, sensors, solar cells, and semiconductor devices. These materials are commonly produced using polymers such as polyimide, polyethylene terephthalate, and polyethylene naphthalate. Flexible substrates help electronic devices to maintain conductivity and structural integrity even when subjected to bending.

The value chain involves raw material providers, polymer producers, coating technology providers, makers of flexible electronics, integration of components, distributors, and consumers. Raw material providers supply specialty polymers and films, which are required in substrate manufacturing. Electronics companies utilize such polymers and films in display devices, sensors, health care equipment, and printed electronics.

Source: Polaris Market Research Analysis

Industry growth is attributed to the rise in the commercialization of foldable smartphones, wearable technology, and OLED display technology. Furthermore, automobiles are making use of the flexible electronics in dashboard displays and sensors. Growth in investments in roll-to-roll manufacturing equipment continues to propel industry growth.

Drivers & Opportunities

Rising Demand for Flexible Consumer Electronics: The flexible electronic gadgets are experiencing high demands in mobile phones, smart watches, fitness bands, and augmented reality devices. The Ministry of Electronics and Information Technology reports that there is an increase in production of electronic gadgets in India from USD 21.35 billion in 2014-15 to above USD 127 billion in 2024-25.The consumer electronics industry is increasingly incorporating light and flexible materials in order to enhance convenience. Flexible OLED screens require substrates which withstand bending without affecting durability and conductivity.

Increasing Adoption of OLED Display Technologies: The OLED technology is increasingly applied in premium smartphones, television, laptop, and automobile displays. For instance, LG Display revealed new OLED technologies with greater brightness, energy efficiency, and faster refresh rate in May 2026 during SID Display Week 2026. Consequently, greater investment in OLED manufacturing facilities and display panels continues to meet market demands.

Restraints & Challenges

Manufacturing and Processing Expenses: Flexible substrates require the use of advanced coating processes and equipment as well as cleanrooms to manufacture. The production of defect-free flexible films at large scale increases operational expenditure for manufacturers. High research and development investments also continue to create cost-related challenges for smaller market participants.

Opportunity

Expansion of Printable Electronics Applications: The use of printable electronics technology is offering good chances for flexible substrate suppliers in sectors such as healthcare, smart packaging, and industry. Printable electronics technology helps in making sensors, RFID tags, and wearable products economically and in large numbers. Increasing adoption of conductive inks and roll-to-roll printing systems continues to support future market expansion.

Source: Polaris Market Research Analysis

Segmental Insights

The report provides a comprehensive analysis of the flexible substrates market by material, application, and end use to pinpoint the key revenue generating and growth segments.

By Material

-

Polyimide (PI)

The polyimide segment dominated the market in 2025, holding nearly 52.48% market share owing to its better thermal stability, flexibility, and chemical resistance properties. These materials find extensive application in flexible OLED display panels, semiconductor package, and in aerospace electronics systems. Increasing requirement for electronics with advanced performance attributes drives the segment's growth.

-

Polyethylene Terephthalate (PET)

Polyethylene terephthalate segment is expected to witness the highest CAGR in the forecast period, owing to increasing utilization in printed electronics as well as in flexible sensor applications. These materials feature low-cost fabrication process, optical clarity, and lightweight nature. Increasing usage in disposable and smart packaging segments drives segment growth.

By Application

-

Flexible Displays

The flexible displays segment accounted for approximately 44.17% market share in 2025 owing to increasing demand for foldable smartphones, OLED televisions, and smart display technologies. Electronics manufacturers are heavily investing in bendable display systems to improve product innovation and user experience. Rising production of AMOLED displays continues to support segment demand.

-

Flexible Printed Circuit Boards (FPCBs)

Flexible printed circuit boards segment is projected to grow at the fastest CAGR during the forecast period due to increasing demand for compact and lightweight electronic devices. FPCBs are increasingly used across smartphones, automotive electronics, industrial automation systems, and healthcare devices. Rising miniaturization of electronic components continues to support market growth.

By End Use

-

Consumer Electronics

Consumer electronics segment dominated the market in 2025 due to increasing production of foldable smartphones, tablets, laptops, and wearable devices. Manufacturers are increasingly integrating flexible substrates into next-generation display and sensing technologies. Rising consumer demand for lightweight and compact electronics supports segment dominance.

-

Healthcare

Healthcare segment is projected to grow at the fastest CAGR during the forecast period due to rising adoption of wearable monitoring devices and flexible medical sensors. Flexible substrates are increasingly used in smart patches, diagnostic devices, and biometric monitoring systems. Strong growth is expected due to precision medical technologies and remote patient monitoring devices.

Source: Polaris Market Research Analysis

Regional Analysis

Asia Pacific Flexible Substrates Market Overview

Asia Pacific dominated the flexible substrates market in 2025 due to strong electronics manufacturing activities across China, Japan, South Korea, and Taiwan. Chinese Ministry of Industry and Information Technology, China’s electronic information manufacturing sector recorded strong growth in the first 10 months of 2025, supported by a 10.6% rise in industrial output and a 10.2% increase in integrated circuit production.Regional companies continue investing in semiconductor fabrication, OLED display production, and flexible electronics technologies. Rising government support for advanced electronics manufacturing continues to support regional market growth.

North America Flexible Substrates Market Insights

North America is projected to grow at the fastest CAGR during the forecast period due to increasing semiconductor innovation and rising demand for wearable healthcare devices. The US continues investing in domestic semiconductor manufacturing and advanced electronics technologies. In December 2024, the U.S. Department of Energy joined a USD 285 million CHIPS initiative to advance digital twin technologies for semiconductor manufacturing.

Europe Flexible Substrates Market Insights

Europe had substantial market share in 2025 due to its growing emphasis on sustainable electronics production and innovations in the automobile industry. Eurostat has revealed that the amount of electronic waste recycled in Europe is estimated to be approximately five million metric tons annually, equaling 11 kilograms per household and covering up to 2,000 football fields if piled one meter high.Flexible electronics have been increasingly adopted in countries like Germany, France, and the UK in industrial automation and electric vehicle applications.

Source: Polaris Market Research Analysis

Competitive Landscape & Key Players

The market is moderately fragmented due to the involvement of global material companies and regional electronics suppliers. The main competitive parameters consist of product quality, flex performance, heat resistance, cost, and scalability during production. Companies emphasize their business models based on collaboration, innovation, expansion, and improved supply chain operations.

The leading players involved in the industry include 3M Company, DuPont de Nemours, Inc., FUJIFILM Holdings Corporation, Kolon Industries, Inc., LG Chem Ltd., Mitsubishi Chemical Group Corporation, Nitto Denko Corporation, Samsung SDI Co., Ltd., SKC Co., Ltd., Sumitomo Chemical Co., Ltd., Teijin Limited, Toray Industries, Inc., and others.

Premium Insights

Expansion of Flexible Hybrid Electronics (FHE)

Flexible hybrid electronics (FHE) technology is anticipated to bring changes to the flexible substrates market. FHE technology combines flexible substrate materials along with semiconductor components to produce light weight and energy efficient electronic products. Increasing use of folding electronics, sensor-based devices, and wearable devices contributes toward market growth.

Rising Demand for AI-Enabled Wearable Technologies

AI-based wearable gadgets and smart clothing is expected to drive up the need for advanced flexible conducting materials. The development of biometric sensing technologies in the healthcare wearables market and remote patient monitoring applications is opening up opportunities for manufacturers of flexible substrates. Increasing investments in printable electronics and roll-to-roll manufacturing technologies continue to strengthen future market potential.

Key Players

- 3M Company

- DuPont de Nemours, Inc.

- FUJIFILM Holdings Corporation

- Kolon Industries, Inc.

- LG Chem Ltd.

- Mitsubishi Chemical Group Corporation

- Nitto Denko Corporation

- Samsung SDI Co., Ltd.

- SKC Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Teijin Limited

- Toray Industries, Inc.

Industry Developments

- December 2025: Murata launched the world’s first ultra-low-loss LCP flexible substrate with an inner cavity structure to support high-speed 6G communication and advanced compact electronic devices. [source: www.murata.com]

- August 2024: Researchers from Massachusetts Institute of Technology, University of Utah, and Meta developed a recyclable flexible substrate material for multilayer electronics to reduce e-waste from wearable and disposable devices. [source: mse.utah.edu]

Flexible Substrates Market Segmentation

By Material Outlook (Revenue, USD Billion, 2021-2034)

- Polyimide (PI)

- Polyethylene Terephthalate (PET)

- Polyethylene Naphthalate (PEN)

- Others

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Flexible Displays

- Solar Cells

- Flexible Printed Circuit Boards (FPCBs)

- Sensors

- Others

By End Use Outlook (Revenue, USD Billion, 2021-2034)

- Consumer Electronics

- Healthcare

- Automotive

- Aerospace & Defense

- Industrial

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Flexible Substrates Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 3.37 Billion |

| Market Size in 2026 | USD 3.74 Billion |

| Revenue Forecast by 2034 | USD 8.84 Billion |

| CAGR | 11.33% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Flexible Substrates Market FAQ's

The global market size was valued at USD 3.37 Billion in 2025 and is projected to grow to USD 8.84 Billion by 2034.

Asia Pacific dominated the market in 2025 due to strong electronics manufacturing activities.

Major applications include flexible displays, flexible printed circuit boards, sensors, and solar cells.

A few of the key players in the market are 3M Company, DuPont de Nemours, Inc., FUJIFILM Holdings Corporation, Kolon Industries, Inc., LG Chem Ltd., Mitsubishi Chemical Group Corporation, Nitto Denko Corporation, Samsung SDI Co., Ltd., SKC Co., Ltd., Sumitomo Chemical Co., Ltd., Teijin Limited, Toray Industries, Inc., and others.

Market growth is driven by rising adoption of foldable electronics, OLED displays, and wearable devices.

Polyimide segment dominated the market in 2025 owing to high thermal stability and flexibility.

Increasing adoption of printable electronics, AI-enabled wearables, and smart sensing technologies is expected to support future market expansion.

Download Sample Report of Flexible Substrates Market

Please fill out the form to request a customized copy of the research report.