Graphene Market Trends, Growth, Industry Share Forecast 2026-2034

REPORT DETAILS

Graphene Market Summary

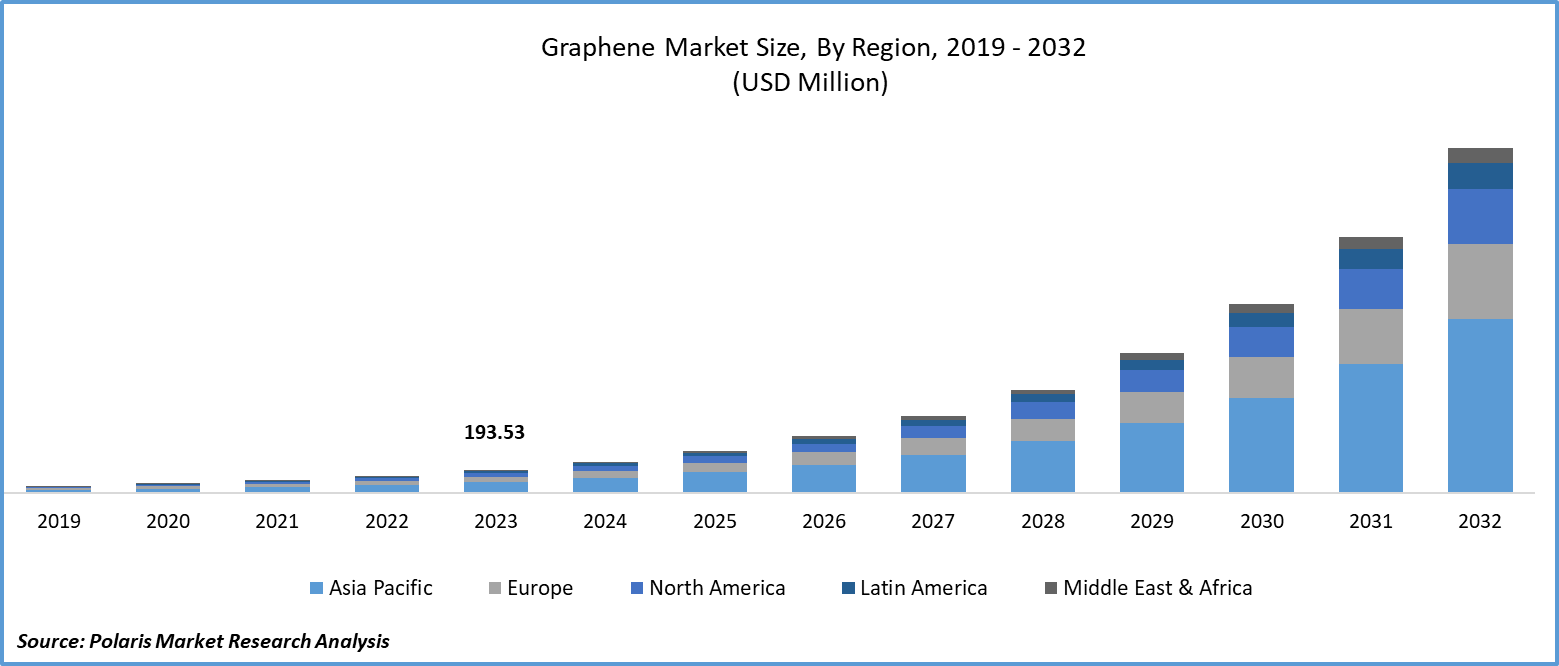

The global graphene market was valued at USD 1,177.63 million in 2025. The graphene market CAGR is expected to be 39.2% during 2025 to 2034. The graphene market is experiencinga remarkable growth because graphene is being used in a number of applications such as electronics, energy, and composites. Graphene is widely researched and developed for various applications; however, graphene commercialization varies across fields. A short validation period is required for uses such as conductive additives, coatings, and polymers. High-spec electronics like semiconductors require a longer period for validation.

Market Statistics

Key Takeaways

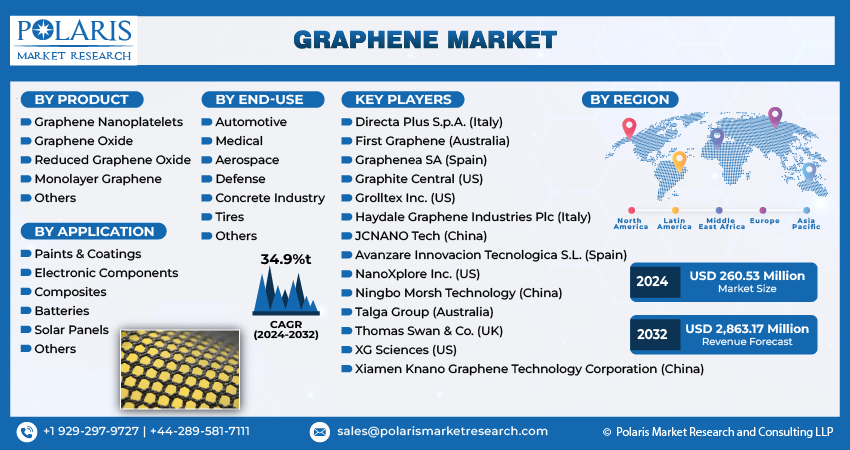

- Asia Pacific dominated the overall market with 32.0% revenue share in 2025, driven by the intense activity of graphene suppliers and consumers, as well as the massive growth in production by industries such as automotive, defense, and aerospace.

- North America is poised for considerable growth witnessing a CAGR of 37.6%, as demand for graphene in the aerospace and automotive industries continues to increase.

- The graphene oxide segment captured 18.0% market share in 2025, primarily due to its widespread use with various polymers and materials to enhance properties such as conductivity, tensile strength, and elasticity.

- The electronic components segment accounted for the highest revenue share accounting for 15.0% due to the accelerating adoption of graphene in electronics production, owing to its high permeability, conductivity, and thinness.

- The medical segment is forecasted to expand with a CAGR of 36.9% during the forecast period due to the development of graphene as a central material for treating major diseases, including cancer.

- Buyer scrutiny is increasing around standardized graphene characterization. This has made traceable QC and ISO graphene testing a competitive advantage for suppliers.

What is Graphene?

Graphene is a single layer of carbon atoms that are arranged in a hexagonal style. It is very thin, strong, and a good conductor of heat and electricity. It has properties including high strength, flexibility, and low weight. It is used in batteries, electronics, coatings, automotive components, and energy storage, as industries look for better performance materials.

Different Forms of Graphene

| Graphene Material Forms | Definition | Cost and Scalability | End-Use Fit |

| Graphene Oxide (GO) | Oxygen-functionalized graphene with high dispersibility in liquids | Low to moderate cost. Highly scalable | Coatings, composites, membranes, sensors |

| Reduced Graphene Oxide (rGO) | Partially restored graphene structure derived from GO | Moderate cost. Scalable with variable quality | Energy storage, conductive inks, electronics |

| Graphene Nanoplatelets (GNP) | Stacked graphene layers with high surface area | Cost-effective. Mass-production friendly | Polymer reinforcement, thermal management |

| CVD-Grown Graphene Films | High-purity graphene grown using chemical vapor deposition | High cost. Limited scalability | Electronics, semiconductors, transparent conductors |

Source: Polaris Market Research Analysis

Industry Dynamics

- Graphene demand is rising in automotive and transport. It is used in batteries, tires, braking systems, and engine parts due to its lightweight and conductivity.

- Vehicle production is increasing globally. This supports higher use of graphene across mobility and transportation applications.

- Material science advancements are creating new use cases. Companies are investing in R&D to reduce cost and improve production.

- Graphene competes with carbon black and nanotubes. It is used when smaller quantity gives better performance or multiple benefits together.

- Lack of proper standards and regulations creates issues. Quality varies, and fake graphene in the market affects buyer trust.

The price of graphene varies greatly depending on the synthesis method, the amount of oxygen content in the case of GO/rGO, the surface area, size distribution, and number of defects. Graphene production cost also depends on the form in which the material is delivered: powder, dispersion, or graphene masterbatch. For many end users, the total cost of adoption depends less on “price per kg” and more on dispersion stability and batch-to-batch reproducibility.

The increasing applications of graphene materials, due to their beneficial properties such as mechanical robustness, flexibility, and higher conductivity, are among the major graphene market drivers. Also, graphene-based materials possess diverse eco-friendly advantages over existing materials. For instance, it helps reduce vehicle weight, carbon emissions, and plastic use. It can also improve fuel efficiency, which, along with other graphene performance benefits, leads to an increasing use of these materials worldwide. For example, in October 2023, Gerdau Graphene launched a new graphene-enriched packaging for Gerdau’s nail product range. This new graphene packing is estimated to decrease plastic use by 25% or above 72 tons per year. In procurement terms, adoption is strongest where graphene delivers a clear KPI improvement without the need for a full material system redesign.

Graphene has the potential to revolutionize the semiconductor and electronics industry because it can be used to develop efficient and faster electronic devices such as integrated circuits, transistors, and displays. Thus, with the constantly increasing demand for consumer electronics, including smartphones and tablets worldwide, the need for graphene to create high-mobility electronics is growing substantially. For instance, according to the International Telecommunication Union, 73 percent of the world’s population aged 10 and above own a mobile phone in 2022, and mobile phone ownership is continuously rising globally. Commercial momentum is currently more visible in electronics adjacent areas. These include conductive inks, EMI shielding coatings, thermal interface enhancement, and sensor platforms. On the other hand, semiconductor-grade graphene is a longer-cycle opportunity due to integration constraints.

The graphene market report details key market dynamics that help industry players to align their business strategy with current and future trends. It highlights technological advancements and breakthroughs along with the respective impact on the market presence. Additionally, a comprehensive regional analysis of the industry on local, national, and global levels has been provided.

What is the Impact of Regulatory Landscape on the Graphene Market?

Regulations on graphene are fragmented but rapidly maturing. In the European Union (EU), graphene falls under REACH/CLP nano rules and requires robust substance characterization. The US treats nanoscale graphene under TSCA. The EPA issued targeted controls (SNURs) for certain nanoplatelets. Also, OSHA/NIOSH provides occupational guidance, but no universal exposure limits yet. China is imposing strict norms on export controls on upstream graphite and developing domestic graphene standards. Market players are focusing on prioritizing standardized characterization, TSCA/REACH readiness, health/safety controls, and supply-chain risk mitigation.

Source: Polaris Market Research Analysis

Graphene Compliance Requirements

To overcome friction in regulation and in purchases, suppliers and demanders are increasingly standardizing:

- Form and flake size distribution of material identity files

- Exposure controls, ventilation, and personal protective equipment

- Lifecycle considerations, such as waste handling assumptions and wastewater control

- Graphene documentation readiness for graphene quality for REACH and/or TSCA customer audits

| Area | Regulatory Status & Key Rules | Responsible Agencies/Standards Bodies | Practical Implications for Industry |

| International Standards & Characterization | ISO/TC 229 (Nanotechnologies) has graphene-specific guidance.

ISO/TS 21356-1:2021 (structural characterization of graphene from powders/dispersions) and other ongoing ISO activities harmonize definitions and measurements | ISO/TC 229, national standards bodies, such as BSI, NPL leadership) | The use of ISO measurement standards reduces disputes over material identity/quality, supports product claims, and eases procurement and regulatory submissions (REACH/TSCA). Implement standardized characterization in QC and technical files. |

| Occupational Health & Safety | Scientific evidence and guidance (NIOSH, OSHA, EU studies) indicate potential respiratory and environmental hazards for some graphene forms.

There is no universally accepted OEL for graphene yet, but NIOSH banding/controls and precautionary engineering controls are recommended.

Recent studies (2024–2025) push for tailored testing and banding. | NIOSH (US), OSHA (US), ECHA/EU scientific bodies, and national public health institutes. | Employers must adopt nano-specific risk assessments, exposure monitoring, PPE, ventilation, and worker training. Regulatory bodies may set limits in the coming years. |

| Environmental/Waste Management | Disposal, emissions, and wastewater are regulated under existing chemical/waste frameworks, but guidance specific to graphene is limited and often science-driven

Lifecycle/environmental testing (OECD/TG applicability studies) is ongoing. | National environmental agencies (EPA, EU member states), OECD guidance | Manufacturers are required to include environmental fate and ecotoxicity testing for regulatory dossiers.

They must treat graphene-contaminated waste as hazardous until proven otherwise. |

| Medical/Consumer Applications | Use of graphene in drug/medical devices must adhere to medical device or pharmaceutical regulations (CE marking/MDR in EU; FDA device/drug rules in the US).

Safety and biocompatibility data are essential. | EMA/FDA/other national regulators, notified bodies in EU. | Clinical/biocompatibility testing and conservative regulatory strategy are required for biomedical uses; regulatory pathways can be lengthy and data-intensive. |

| Trade Controls & Strategic Materials | A few jurisdictions (notably China) have adjusted export controls on graphite/graphite-derived materials.

National security/strategic-material rules may influence cross-border shipments. | Customs, trade ministries, export control agencies | Supply chain planning and alternative sourcing are important

Compliance teams must track export control lists and licensing requirements. |

Source: Polaris Market Research Analysis

Growth Factors

Growing Demand for Graphene from Automotive & Transportation Industry to Drive Graphene Market Growth

The lightweight, higher strength, and conductivity of graphene make this nanomaterial very useful for applications in different components of automobiles, like batteries, tires, anti-braking systems, and engine components. Therefore, with the rise in the production of automobiles and the growth of the transportation industry, the demand for graphene also rises. For instance, as per a May 2023 report by the European Automobile Manufacturers Association, approximately 85.4 million motor vehicles were produced globally in 2022, registering a substantial 5.7% rise from 2021.

However, automotive adoption is affected by qualification timelines and supply assurance. Customers generally expect graphene dispersion stability, mechanical/electrical qualifications across temperature and aging conditions, and scalable graphene supply contracts for graphene before it transitions from pilot lines to high-volume platforms.

Advancements in Material Science and Investments in R&D Boost the Market Growth

Rising advancements in material science led to the creation of new potential applications for the graphene market across different verticals and an increasing number of companies and research institutes focusing on R&D to make it cost-efficient and improve the production process, further boosting the market’s growth. For instance, in October 2022, Researchers from the laboratory of Nai-Chang Yeh performed new studies on graphene and said that graphene can significantly improve electrical circuits required for flexible and wearable electronics.

In some applications, graphene competes with established alternatives. These include carbon black, carbon nanotubes, and other conductive additives. Graphene is preferred when it can offer better results using a smaller amount of material. It is also used when it offers multiple benefits at once.

Restraining Factors

Lack of Industrialization and Regulatory Uncertainty Hampering the Market Growth

As graphene is currently in its initial stages and lacks globally accepted industry standards for production or characterization, companies are producing different types of graphene that result in the creation of fake graphene. Also, the regulatory framework for graphene is underdeveloped and still evolving, meaning the graphene regulatory uncertainty creates a hurdle for graphene market growth.

Graphene Quality Verification Parameters

Buyers increasingly ensure fake graphene verification by requesting:

- ISO graphene characterization: Identity confirmation for powders/dispersions

- Batch-to-batch COA consistency: Surface area, particle/flake distribution, and oxygen content where applicable

- Dispersion performance data in relevant matrices: Epoxy, elastomers, and battery slurry

- Application-specific benchmarks: Conductivity at loading %, mechanical uplift, aging behavior

Source: Polaris Market Research Analysis

Segmental Insights

By Product Insights

-

Graphene oxide segment accounted for the largest share in 2025

The graphene oxide segment accounted for 18.0% share in the graphene market. Segment’s dominance is attributed to its widespread use with different types of polymers and materials in order to enhance their properties like conductivity, tensile strength, and elasticity. Additionally, graphene oxide is highly fluorescent, which makes it suitable for use in disease detection, biosensing, antibacterial materials, and drug carriers.

The graphene nanoplates segment will grow rapidly with a CAGR of 37.1% on account of its exceptional properties, including high surface area, electrical conductivity, thermal conductivity, and greater mechanical strength. Also, rising demand for lightweight composite constituents in the aerospace and automotive industries further escalates demand for graphene nanoplates. The main issues for graphene are controlling its levels of oxidation and ensuring a graphene oxide dispersion in the end product each time. This is particularly challenging for the industrial production scale for the polymer and coating materials because graphene manufacturing consistency is required here.

By Application Insights

-

The electronic components segment held a significant share in 2025

The electronic components segment held 15.0% share in 2025. This dominance is attributable to the surging demand for graphene in the electronics industry to manufacture several components, as it provides high permeability, graphene conductivity, and thinness. In addition, growing R&D to develop graphene semiconductors to increase energy efficiency and electron mobility in semiconductors drives the segment’s growth.

Its use within the industry is apparent with regard to conductive coatings, flexible electronics graphene substrates, graphene sensors, heat transfer improvements, and graphene EMI shielding. In these applications, the combination of thin materials, conductivity, and multifunctionality creates immediate engineering value.

By End-Use Insights

-

The medical segment is expected to expand fastest with a CAGR of 36.9% during the forecast period

The medical segment will grow at the highest growth rate in the market forecast period. Segment’s growth is attributed to the emergence of graphene as an innovative and crucial material in the medical field because of its potential to treat severe diseases, including cancer. Also, graphene-based materials are being studied or researched globally for graphene drug delivery applications due to their high surface area, which, in turn, bodes well for the segment’s growth. For instance, in November 2023, the Indian Institute of Technology Guwahati announced that it had discovered the use of modified graphene oxide in graphene biomedical applications, as it offers low cytotoxicity and a large surface area.

Medical commercialization will still need quite a lot of testing data for graphene biocompatibility, toxic testing, and graphene clinical validation, which can be a lengthy procedure. So short-term growth can be noticed mostly in research-grade products and medical applications, rather than clinical-scale applications.

Real-World Examples

| Industry | Application Area | What Graphene Does | Example |

| Electronics | Conductive inks, sensors | Improves conductivity and thinness | Used in flexible circuits and wearable electronics |

| Batteries | Lithium-ion batteries | Enhances conductivity and energy flow | Improves electrode performance and charging speed |

| Coatings | Anti-corrosion coatings | Increases durability and protection | Used in industrial and marine coatings |

| Automotive | Tires, composites, parts | Reduces weight and improves strength | Used in tires and lightweight vehicle components |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Regional Insights

Asia Pacific region dominated the global market in 2025

The Asia Pacific region dominated the global market. The Asia Pacific graphene market dominance is accelerated by the robust presence of graphene manufacturers and consumers, coupled with the exponential rise in production volumes across various sectors such as automotive, defense, and aerospace. Also, the rising number of favorable policies by government authorities, academic research, and funding promotes the development of new graphene applications and improvements in the production process, fostering the region’s growth. For instance, in August 2023, the Ministry of Electronics & Information Technology, India, announced the launch of the ‘Graphene Aurora program’ in order to bolster graphene engineering.

Asia Pacific sees strong demand for graphene. The high Asia Pacific graphene demand is because the region has mature manufacturing sectors, such as electronics, automotive components, and high-performance materials, that require widespread adoption of graphene. In addition, there are government-backed R&D initiatives that enable quicker commercialization of products that involve testing phases and manufacturing.

As the production of graphene depends on graphite, companies are monitoring the regulations and conditions of the graphene supply chain. In order to prevent shortages, especially for volume applications, companies are now resorting to alternative suppliers.

The North America region is projected to gain a substantial growth rate owing to a rapid increase in demand for graphene from the automobile and aerospace industries. Additionally, the rising number of collaborations among product manufacturers and research institutions to focus on research & development activities and increase end-use applications of graphene is likely to bode well for the region’s growth.

Source: Polaris Market Research Analysis

Key Market Players & Competitive Insights

-

Improvements in product quality and automation driving the market competition

The market for graphene is highly fragmented and is witnessing significant graphene market competition from various regional and global players. Key graphene market companies are highly focused on adopting several growth strategies to increase their foothold in the market. Also, companies are competing on factors such as improving the purity of graphene, graphene production automation, cost-efficiency, improving supply chain & distribution networks, and developing customized solutions. For instance, in November 2023, EnyGy announced its plan to launch a graphene-based super-capacitor in 2024, which will provide higher energy storage capabilities across a wide range of applications.

The graphene route-to-market significantly affects how quickly consumers can begin using it. When marketed by suppliers through a dispersion or graphene masterbatch formulation by a formulator, consumers can immediately evaluate and begin utilizing graphene. However, selling it in powdered formulation may require consumers to develop a dispersion method, which can be more expensive.

Some of the major players operating in the global market include:

- Avanzare Innovacion Tecnologica S.L. (Spain)

- Directa Plus S.p.A. (Italy)

- First Graphene (Australia)

- Graphenea SA (Spain)

- Graphite Central (US)

- Grolltex Inc. (US)

- Haydale Graphene Industries Plc (Italy)

- JCNANO Tech (China)

- NanoXplore Inc. (US)

- Ningbo Morsh Technology (China)

- Talga Group (Australia)

- Thomas Swan & Co. (UK)

- XG Sciences (US)

- Xiamen Knano Graphene Technology Corporation (China)

Graphene Industry Developments

- April 2026: Graphene Manufacturing Group (GMG) improved its graphene aluminium-ion battery. Energy density increased to around double levels. The company is aiming very fast charging, close to 6 minutes. Customer testing is planned in 2026, while commercial production is expected in 2027. Source: (graphenemg.com)

- December 2025: Graphene Square completed a mass-production facility in Korea. The move helps large-scale graphene output and improves supply for commercial uses. (Source: graphene-info.com)

- In April 2025, HydroGraph Clean Power partnered with an industrial gas supplier to establish a graphene production facility in Texas, securing access to high-purity acetylene feedstock. (Source: hydrograph.com)

- In March 2025, NEI Corporation launched new graphene dispersions. The new dispersions have been developed in collaboration with HydroGraph. They aim at improving electrode slurry in flexible high-performance batteries. This solution provides a green alternative for battery production instead of traditional conductive carbons. (Source: neicorporation.com)

- In January 2025, Perpetuus Advanced Materials launched proprietary nano-engineered graphene masterbatch compounds for commercial, passenger, and industrial tires. (Source: perpetuusam.com)

These developments and graphene innovations demonstrate that graphene research and development have moved from being a new material to an established one. The focus is currently on developing graphene-based products that are proven and user-friendly for mass production. This is especially the case with energy storage and conductive materials, among others, where mass production is feasible.

Graphene Market Segmentation

By Product Outlook (Revenue – USD Million, 2021–2034)

- Graphene Nanoplatelets

- Graphene Oxide

- Reduced Graphene Oxide

- Monolayer Graphene

- Others

By Application Outlook (Revenue – USD Million, 2021–2034)

- Paints & Coatings

- Electronic Components

- Composites

- Batteries

- Solar Panels

- Others

By End-Use Outlook (Revenue – USD Million, 2021–2034)

- Automotive

- Medical

- Aerospace

- Defense

- Concrete Industry

- Tires

- Others

By Regional Outlook (Revenue – USD Million, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indnesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Graphene Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 1,177.63 million |

| Market Size in 2026 | USD 1,635.02 million |

| Revenue Forecast by 2034 | USD 23,107.63 million |

| CAGR | 39.2% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD million, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Graphene Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Graphene Market FAQ's

The graphene market stood at USD 1,177.63 million in 2025. It is projected to account for a CAGR of 39.2% between 2025 and 2034.

Water miscibility is high for graphene oxide, while it is poorly conductive. The reduced graphene oxide is more conductive than graphene oxide, but it is difficult to mix.

Large-scale production of graphene is challenging. Quality is limited to the manufacturer, and additional processing is required before it can be utilized.

Customers review test reports, evaluate performance parameters, and consult dependable suppliers to ensure that it can do what is stated.

Today, solutions from the graphene market are used in batteries, coatings, inks, plastics, sensors, and semiconductors.

There are several methods for preparing graphene, ranging from chemical methods to thin-film methods. Different preparation methods will influence the price, quality, and functionality of the resulting graphene.

Graphene is used in batteries, electronics, coatings, composites, and sensors. It supports improve conductivity, strength, and overall material performance.

Graphene offers high strength and lightweight structure. It also provides excellent electrical and thermal conductivity.

Download Sample Report of Graphene Market

Please fill out the form to request a customized copy of the research report.