In-vitro Colorectal Cancer Screening Tests Market Outlook, 2026-2034

REPORT DETAILS

REPORT DETAILS

In-vitro Colorectal Cancer Screening Tests Market Summary

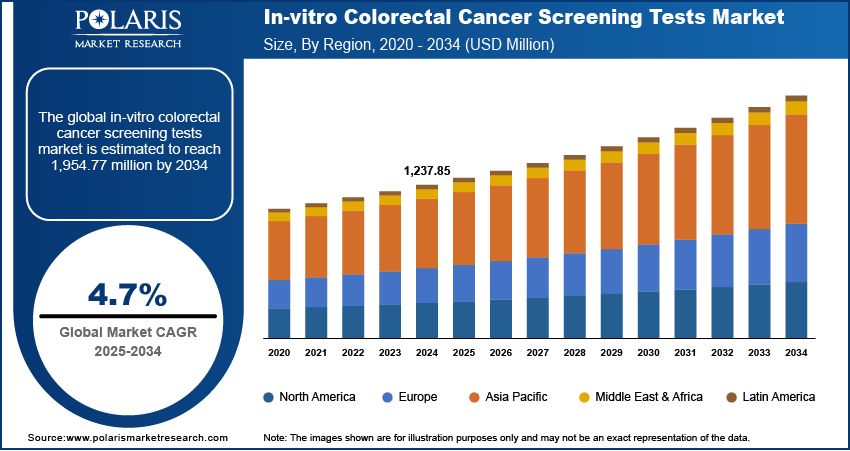

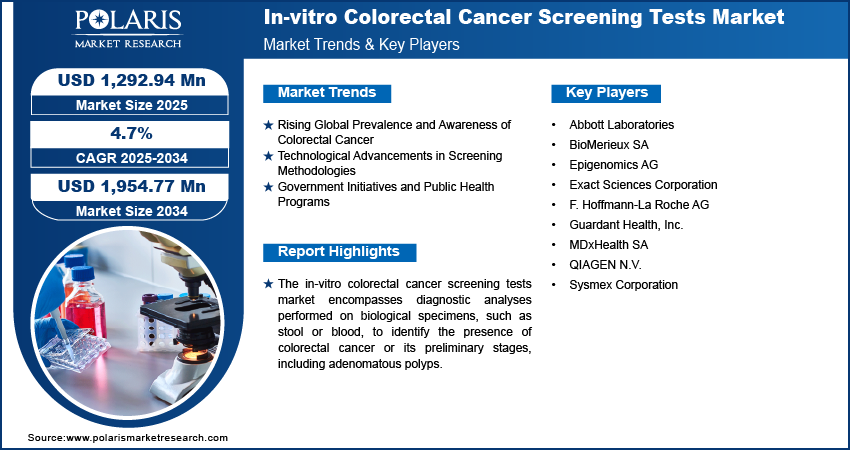

The in-vitro colorectal cancer screening tests market size was valued at USD 1.29 billion in 2025, exhibiting a CAGR of 4.7% during 2026–2034. The market is driven by rising cancer prevalence, aging population, early detection awareness, technological advancements, and strong government-led screening programs promoting non-invasive, accessible diagnostics.

Market Statistics

Key Takeaways

- North America holds the largest market share valued for 40.3% in 2025, due to strong screening programs, a culture of early diagnosis, and favorable reimbursement policies.

- Asia Pacific shows the highest growth rate at a CAGR of 6.8% during the forecast period, driven by aging populations, lifestyle changes, increasing awareness, and expanding healthcare investment.

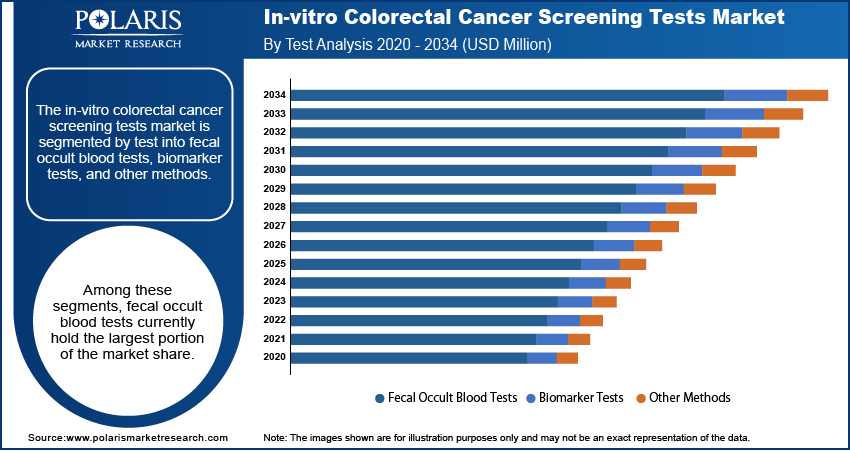

- Fecal occult blood tests dominated the market with a 55.0% share in 2025, due to affordability, ease of use, and their widespread adoption in national screening programs.

- Diagnostic laboratories are seeing the fastest growth at a CAGR of 5.7%, supported by outsourced testing, specialized equipment, and rising demand for advanced biomarker assays.

- Hospitals segment dominated the market accounting for 42.6% share in 2025, due to advanced infrastructure, patient inflow, and reimbursement coverage.

*Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The rising global burden of colorectal cancer is increasing the demand for early detection through efficient and accessible in-vitro screening tests.

- Continuous technological advancements are improving test accuracy, driving the shift from traditional methods to molecular and biomarker-based diagnostics.

- Government-led public health initiatives and national screening programs are significantly boosting test adoption across both developed and emerging markets.

- Growing preference for non-invasive, at-home screening kits is enhancing patient compliance and reshaping screening strategies globally.

- Limited infrastructure and awareness in low-resource settings remain key barriers to widespread implementation of advanced screening technologies.

Source: Polaris Market Research Analysis

What is Colorectal Cancer Screening?

In vitro colorectal cancer screening tests are diagnostic procedures. These procedures are conducted on biological samples such as stool or blood. They are used to identify early signs of colorectal cancer or precancerous conditions like polyps. These tests support early detection. They enable timely medical intervention. The tests help improve patient outcomes through non-invasive or minimally invasive screening approaches.

The in-vitro colorectal cancer screening tests market encompasses diagnostic procedures performed on samples derived from the body, such as stool or blood, to detect the presence of colorectal cancer or its precursors, like adenomas and polyps. These tests including cancer biopsy play a crucial role in the early identification of the disease, which significantly improves treatment outcomes and patient survival rates. The market is driven by a confluence of factors, including the rising global prevalence of colorectal cancer and increasing awareness regarding the importance of early detection. As the global population ages, the incidence of colorectal cancer, which is more common in older adults, is also on the rise, thereby fueling the market demand for effective screening solutions. Furthermore, public health initiatives and government programs promoting regular cancer screenings contribute significantly to the market drive.

Non-Invasive Tests vs Colonoscopy

Non-invasive colorectal cancer screening tests are compared with colonoscopy. This is due to differences in patient experience, accuracy, and cost-effectiveness. Colonoscopy remains the gold standard for diagnosis. However, non-invasive options are improving screening adoption and early detection rates.

| Factor | Non-Invasive Tests (Stool/Blood-based) | Colonoscopy |

| Comfort | High comfort, no sedation or preparation in most cases | Lower comfort due to bowel prep and invasive procedure |

| Accuracy | Moderate to high for early detection, improving with advanced biomarkers | Very high accuracy for detecting and removing polyps |

| Cost | Generally lower cost, suitable for large-scale screening programs | Higher cost due to procedure complexity and clinical setting |

| Accessibility | Easy to distribute and perform at home or clinics | Requires specialized facilities and trained gastroenterologists |

Source: Polaris Market Research Analysis

Several factors underpin the growth of the in-vitro colorectal cancer screening tests market. Technological advancements leading to the development of more sensitive and non-invasive screening methods, such as stool-based DNA tests and blood-based biomarker tests, are key market growth factors. The increasing preference for minimally invasive surgery and diagnostic procedures among both patients and healthcare providers is also boosting market penetration. Moreover, the growing emphasis on preventive healthcare and the availability of at-home testing kits are enhancing patient compliance and accessibility to screening, further driving the market development. Consequently, the market outlook for in-vitro colorectal cancer screening tests remains positive, with continuous innovations expected to shape future market trends.

Market Dynamics:

Rising Global Prevalence and Awareness of Colorectal Cancer

The increasing global incidence of colorectal cancer stands as a significant market drive for in-vitro colorectal cancer screening tests. Colorectal cancer remains a leading cause of cancer-related deaths worldwide, and its prevalence is projected to rise further due to factors such as aging populations and lifestyle changes. Colorectal cancer is the third most common cancer worldwide, with over 1.9 billion new cases diagnosed in 2022. It is also the second leading cause of cancer-related deaths globally, resulting in over 900,000 deaths annually. The global burden of colorectal cancer is projected to increase significantly, with an estimated 3.2 billion new cases and 1.6 billion deaths by 2040

For instance, a research article published on NCBI in 2023 titled "Global patterns and trends in colorectal cancer incidence and mortality" highlighted the substantial increase in colorectal cancer cases in many regions and underscored the critical role of screening in mitigating mortality. The study emphasized that countries with well-established screening programs have demonstrated better control over the disease's impact. The continuous rise in colorectal cancer incidence and the heightened awareness surrounding the importance of multi cancer early detection are undeniably powerful forces propelling the expansion of the in-vitro colorectal cancer screening tests market.

Technological Advancements in Screening Methodologies

Significant technological advancements in in-vitro diagnostic techniques are a crucial market growth factor for the colorectal cancer screening tests market. Innovations in molecular diagnostics and biomarker identification have led to the development of more sensitive, specific, and non-invasive screening assays. Traditional methods like fecal occult blood tests (FOBT) and fecal immunochemical tests (FIT) have been enhanced with the introduction of sophisticated stool-based DNA tests (sDNA) that can detect genetic mutations associated with colorectal cancer and advanced adenomas. Additionally, the emergence of blood-based biomarker tests, although still under development and validation for widespread screening, holds immense potential for convenient and accessible early detection. A study published on PubMed in 2022 titled "Advances in non-invasive colorectal cancer screening: A review of current and emerging technologies" detailed the progress made in developing highly sensitive molecular markers for colorectal cancer detection in stool and blood samples. The research emphasized the improved accuracy and potential for earlier detection offered by these novel technologies compared to traditional methods. The ongoing technological innovation in screening methodologies is a fundamental driver fueling the substantial growth of the in-vitro colorectal cancer screening tests market.

Government Initiatives and Public Health Programs

Government initiatives and public health programs worldwide play a pivotal role in driving the market demand for in-vitro colorectal cancer screening tests. Recognizing the significant public health burden of colorectal cancer, many governments and healthcare organizations have implemented national screening programs and guidelines to encourage early detection. Healthy People 2030 is an initiative by the U.S. Department of Health and Human Services includes objectives to increase the proportion of adults who get screened for colorectal cancer.

Furthermore, research published on PubMed Central (PMC) in 2021 titled "Impact of national colorectal cancer screening programs on incidence and mortality: An international comparison" analyzed the effectiveness of organized screening programs in reducing colorectal cancer incidence and mortality across different countries. The study highlighted that countries with well-established and actively promoted national screening programs have achieved significant improvements in early detection rates and subsequent reductions in advanced-stage diagnoses and deaths. Such governmental support and the implementation of structured screening programs create a consistent and growing demand for in-vitro colorectal cancer screening tests. By lowering the barriers to access and promoting widespread participation, these initiatives are a crucial market drive that significantly contributes to the expansion and sustained growth of the in-vitro colorectal cancer screening tests market.

Challenges in Screening Tests

- False positives and false negatives remain a key limitation. It potentially leads to unnecessary follow-ups or missed diagnoses.

- Limited awareness in developing regions reduces participation in regular colorectal cancer screening programs.

- Access to advanced diagnostic infrastructure is limited, especially in rural and low-resource healthcare settings.

- High costs of certain molecular and blood-based tests restrict large-scale adoption.

- Patient reluctance toward screening and lack of routine preventive health behavior impact screening rates.

Source: Polaris Market Research Analysis

Segment Insights:

Market Assessment – By Test

The in-vitro colorectal cancer screening tests market is segmented by test into fecal occult blood tests, biomarker tests, and other methods. Among these segments, in 2025, fecal occult blood tests currently hold the largest portion of the market capturing 55.0% share. This dominance can be attributed to their long-standing presence, established integration into screening programs, and relative affordability. Fecal occult blood tests, including traditional guaiac-based FOBT and the more sensitive fecal immunochemical tests (FIT), have been widely adopted globally as a primary screening tool for colorectal cancer. Their non-invasive nature and ease of use have contributed significantly to their widespread implementation in population-based screening initiatives.

Conversely, the biomarker tests segment is anticipated to exhibit the highest growth rate at a CAGR of 5.5%, within the in-vitro colorectal cancer screening tests market. This rapid expansion is fueled by the continuous advancements in molecular diagnostics and the increasing identification of novel biomarkers associated with colorectal cancer. Cancer biomarker tests, which include stool-based DNA tests and emerging blood-based assays, offer the potential for enhanced sensitivity and specificity compared to traditional fecal occult blood tests. The ability of these tests to detect precancerous lesions and early-stage cancers with greater accuracy is a significant driver of their projected high growth.

Market Evaluation– By End Use

The in-vitro colorectal cancer screening tests market is segmented by end use into hospitals, clinics, diagnostic laboratories, and others. Currently, tthe hospitals segment accounts for the largest share of the market valued at 42.6% in 2025. This significant market presence is primarily due to the central role that hospitals and clinics play in patient care, including cancer screening and diagnosis. These healthcare facilities are often the first point of contact for individuals seeking medical advice and undergoing routine check-ups, making them key centers for the administration and ordering of colorectal cancer screening tests.

The diagnostic laboratories segment is anticipated to demonstrate the highest growth rate of 5.7%, within the in-vitro colorectal cancer screening tests market. This projected several factors, including the increasing outsourcing of diagnostic testing by hospitals and clinics to specialized laboratories drive rapid growth. Diagnostic laboratories often possess advanced technological capabilities and economies of scale, allowing them to process a large volume of tests efficiently and cost-effectively. The growing trend of centralized testing and the increasing demand for specialized and complex in-vitro colorectal cancer screening tests, such as advanced biomarker assays, further contribute to the expanding role of diagnostic laboratories.

Source: Polaris Market Research Analysis

Regional Footprint

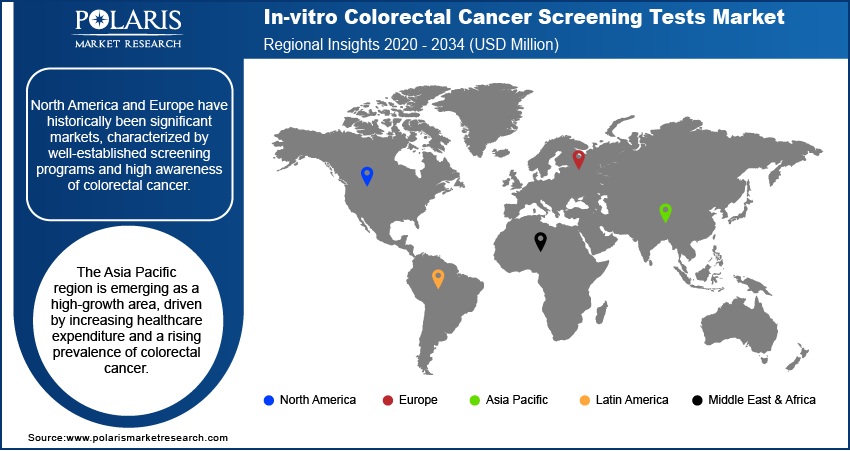

The in-vitro colorectal cancer screening tests market demonstrates varied dynamics across different geographical regions, including North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Each region exhibits unique characteristics influenced by factors such as healthcare infrastructure, government regulations, disease prevalence, awareness levels, and the adoption of advanced screening technologies. North America and Europe have historically been significant markets, characterized by well-established screening programs and high awareness of colorectal cancer. The Asia Pacific region is emerging as a high-growth area, driven by increasing healthcare expenditure and a rising prevalence of colorectal cancer. Latin America and the Middle East & Africa are also witnessing growing adoption of screening tests, albeit at a relatively slower pace compared to more developed regions, presenting considerable future market potential.

In 2025, North America currently held the largest share valued at 40.3% of the in-vitro colorectal cancer screening tests market. This dominance can be attributed to a combination of factors, including a well-developed healthcare infrastructure, the presence of established national screening guidelines, high patient awareness regarding the importance of early cancer detection, and the widespread adoption of advanced screening technologies. Furthermore, the strong presence of major market players and significant healthcare expenditure in the region contribute to its leading market position. The proactive approach towards cancer prevention and early diagnosis, coupled with favorable reimbursement policies for screening tests, further reinforces North America's substantial market share in the global in-vitro colorectal cancer screening tests market.

The Asia Pacific region is projected to exhibit the highest growth rate of 6.8% in the in-vitro colorectal cancer screening tests market over the coming years. This rapid expansion is fueled by a confluence of factors, including a rapidly aging population, rising prevalence of colorectal cancer due to changing lifestyles, increasing healthcare expenditure, and growing government focus on implementing cancer screening programs. Furthermore, improving healthcare access and rising awareness levels across the region are driving greater adoption of screening tests. The increasing penetration of advanced diagnostic technologies and the growing medical tourism sector in some Asia Pacific countries also contribute to the high growth potential of this region in the in-vitro colorectal cancer screening tests market.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

Key participants actively involved in the in-vitro colorectal cancer screening tests industry include Exact Sciences Corporation, F. Hoffmann-La Roche AG, Abbott Laboratories, BioMerieux SA, QIAGEN N.V., Sysmex Corporation, Guardant Health, Inc., Epigenomics AG, and MDxHealth SA. These entities are engaged in the development, manufacturing, and commercialization of various in-vitro tests for colorectal cancer screening, catering to different segments of the market with their diverse product portfolios.

The competitive landscape of the in-vitro colorectal cancer screening tests market is characterized by ongoing innovation and the presence of both established diagnostic companies and emerging players. Competition is driven by factors such as test accuracy, ease of use, cost-effectiveness, and the ability to detect early-stage cancers and precancerous lesions. Companies are focusing on developing more sensitive and specific biomarker-based tests and expanding their market reach through strategic collaborations and partnerships. The increasing emphasis on non-invasive screening methods and the growing demand for early detection are intensifying the competitive dynamics within the market, encouraging continuous advancements and the introduction of novel testing solutions.

Exact Sciences Corporation, located in Madison, Wisconsin, United States, offers the Cologuard test, a non-invasive, multi-target stool DNA test for colorectal cancer screening. This test analyzes both DNA and hemoglobin in stool samples to detect colorectal cancer and precancerous polyps. Their focus on innovative stool-based DNA technology has made them a significant entity in the in-vitro colorectal cancer screening tests market, providing an alternative to traditional colonoscopy and other screening methods.

F. Hoffmann-La Roche AG, headquartered in Basel, Switzerland, provides a range of diagnostic solutions, including fecal immunochemical tests (FIT) under its various business units. These tests are widely used for the detection of hidden blood in stool, a key indicator for colorectal cancer screening. Roche's extensive global presence and comprehensive portfolio of diagnostic products make them a relevant player in the in-vitro colorectal cancer screening tests market, offering established and reliable screening options.

List of Key Companies:

- Abbott Laboratories

- BioMerieux SA

- Epigenomics AG

- Exact Sciences Corporation

- F. Hoffmann-La Roche AG

- Guardant Health, Inc.

- MDxHealth SA

- QIAGEN N.V.

- Sysmex Corporation

Industry Developments

- March 2026: Walgreens and Workflow Services announced a partnership to expand colorectal cancer screening access. Workflow Services will support a new nationwide initiative from Walgreens and Exact Sciences to close critical colorectal cancer screening gaps. (Source: workflowservices.com)

- January 2025: Tempus AI, Inc. introduced xT CDx, its FDA-approved, NGS-based in vitro diagnostic device, in the U.S. Clinicians across the country can now utilize this advanced tool to enhance patient care. (Source: tempusai.com)

- July 2024: the FDA granted approval for Guardant's groundbreaking blood test, Shield, designed for colorectal cancer screening. This milestone marks significant progress in providing a noninvasive and effective approach to early cancer detection. (Source: guardant.com)

What is the Future of the In-Vitro Colorectal Cancer Screening Tests Market?

The market is expected to grow steadily due to the rising global incidence of colorectal cancer. Increasing emphasis on early detection would also boost the industry growth. Advancements in non-invasive diagnostic technologies, such as improved stool DNA and blood-based biomarker tests, will enhance accuracy and patient acceptance. Expansion of government-led screening programs is expected to boost the adoption of in-vitro colorectal cancer screening tests. Rising adoption of at-home testing kits are driving market penetration. Additionally, a growing global shift toward preventive healthcare is projected to support long-term market growth.

Market Segmentation

By Test Outlook (Revenue-USD billion, 2021–2034)

- Fecal Occult Blood Tests

- Biomarker Tests

- Other Methods

By End Use Outlook (Revenue-USD billion, 2021–2034)

- Hospitals

- Clinics

- Diagnostic Laboratories

- Others

By Regional Outlook (Revenue-USD billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Malaysia

- Suth Korea

- Indnesia

- Australia

- Vietnam

- Rest of Asia-Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- Suth Africa

- Rest of Middle East & Africa

- Latin America

- Mexic

- Brazil

- Argentina

- Rest of Latin America

Report Scope:

| Report Attributes | Details |

| Market Size Value in 2025 | USD 1.29 billion |

| Market Size Value in 2026 | USD 1.35 billion |

| Revenue Forecast by 2034 | USD 1.94 billion |

| CAGR | 4.7% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Insights |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

How is the report valuable for an organization?

Workflow/Innovation Strategy: The in-vitro colorectal cancer screening tests market has been segmented into detailed segments of test and end use. Moreover, the study provides the reader with a detailed understanding of the different segments at both the global and regional levels.

Market Entry Strategies: Growth and marketing strategies within the in-vitro colorectal cancer screening tests market are increasingly focused on enhancing patient awareness and accessibility. Companies are investing in direct-to-consumer marketing campaigns to educate individuals about the importance of early screening and the availability of non-invasive testing options. Collaborations with primary care physicians and gastroenterologists are crucial for integrating these tests into routine clinical practice and ensuring seamless referral pathways. Furthermore, strategic partnerships with health insurance providers to improve coverage and reduce out-of-pocket costs are vital for increasing market penetration. Emphasis on the clinical utility and accuracy of advanced biomarker tests, supported by robust clinical data, is also a key marketing message to gain trust and adoption among healthcare professionals and patients. Leveraging digital platforms for education, test ordering, and result delivery is another growing trend to improve convenience and reach a wider population.

FAQ's

The In-vitro colorectal cancer screening tests market size was valued at USD 1.29 Billion in 2025 and is projected to grow to USD 1.94 Billion by 2034.

The market is projected to register a CAGR of 4.7% during the forecast period, 2026-2034.

North America had the largest share of the market accounting for 40.3%.

Key players in the in-vitro colorectal cancer screening tests market include Exact Sciences Corporation, F. Hoffmann-La Roche AG, Abbott Laboratories, BioMerieux SA, QIAGEN N.V., Sysmex Corporation, Guardant Health, Inc., Epigenomics AG, and MDxHealth SA

The hospitals segment accounted for the larger share of the market in 2025 capturing 42.6%.

Download Sample Report of In-vitro Colorectal Cancer Screening Tests Market

Please fill out the form to request a customized copy of the research report.