Industrial Coatings Market Demand, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

REPORT DETAILS

Industrial Coatings Market Overview

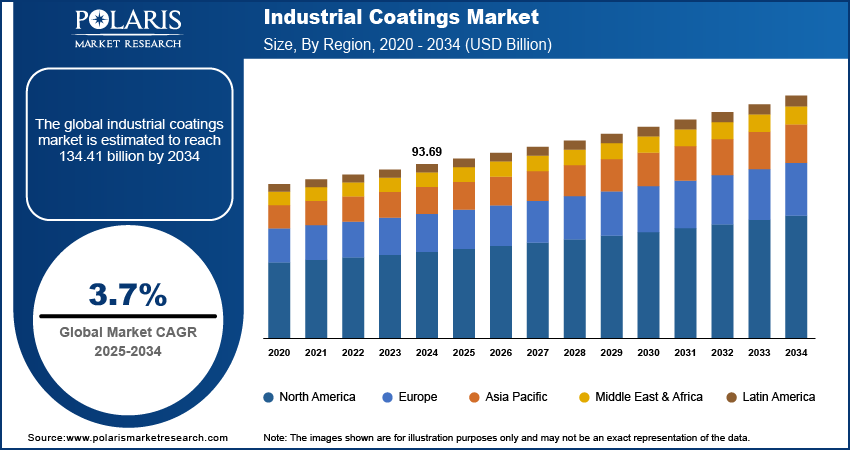

The industrial coatings market size was valued at USD 95.75 billion in 2025, exhibiting a CAGR of 3.5% during 2026–2034. It is driven by growing demand for both protective and functional industrial coatings across the manufacturing, infrastructure, automotive, marine, and energy sectors.

Market Statistics

Key Takeaways

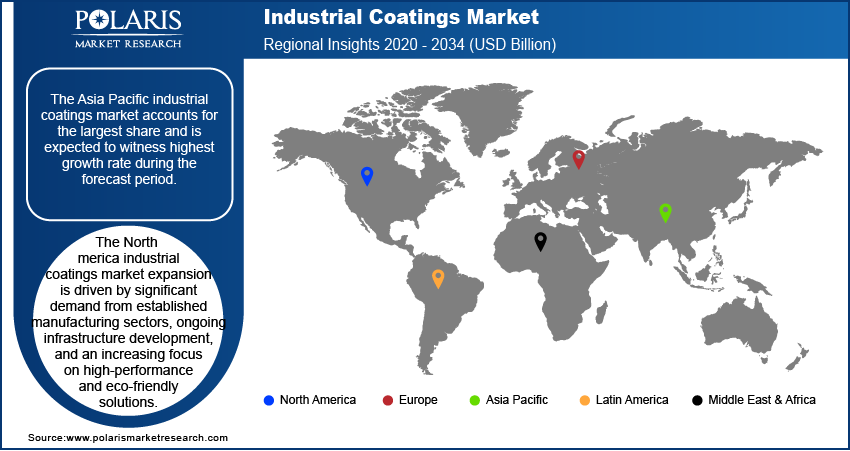

- By region, the Asia Pacific industrial coatings market led globally in 2024 with 43.40% share in 2025 . This is a direct result of the region's industrial growth.

- The North America industrial coatings market is expected to register CAGR of 3.86%, driven by significant demand from established manufacturing sectors, ongoing infrastructure development.

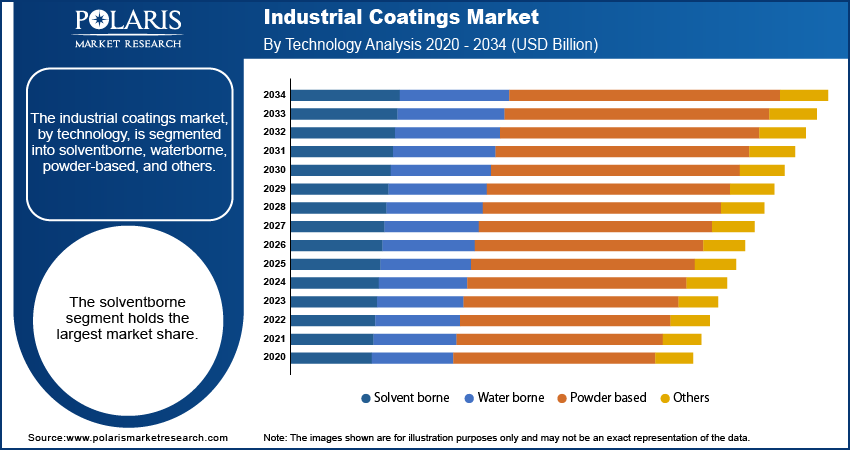

- By technology, solventborne industrial coatings held the largest share of 46.3% in 2025. This was due to their strong durability, chemical resistance, and reliable performance in high-moisture conditions.

- By resin type, epoxy industrial coatings accounted for the largest market share of 31.10% in 2025, owing to their high adhesion strength and corrosion-resistant properties.

- By end use, the general industry segment had the highest adoption of the product in 2025 and led with 46.52% share. This was followed by consumer products, which gradually increased in popularity.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The rising number of infrastructure projects, especially in emerging countries, is a key driver.

- There is a global shift in the approach to governing the emissions of Volatile Organic Compounds (VOCs).

- The general, automotive, and aerospace industries are rapidly growing, which in turn provides demand for coatings.

What are Industrial Coatings?

Industrial coatings are protective and functional coating materials. They are applied to metal, concrete, plastic, wood, and other industrial surfaces. These coatings help improve corrosion resistance, chemical protection, abrasion resistance, thermal stability, durability, and overall surface performance. They are widely used across manufacturing, automotive, marine, aerospace, infrastructure, oil & gas, and energy industries. The coatings are adopted to extend equipment lifespan and reduce maintenance costs. They also help enhance operational efficiency in demanding industrial environments.

Industrial Coatings vs Paints

| Parameter | Industrial Coatings | Conventional Paints |

| Primary Purpose | Designed for surface protection, durability, and functional performance in harsh industrial environments | Primarily used for decoration, aesthetics, and basic surface protection |

| Performance Characteristics | Offers high corrosion resistance, chemical protection, abrasion resistance, thermal stability, and weather resistance | Provides moderate protection with a greater focus on color, finish, and appearance |

| Application Areas | Used in manufacturing plants, automotive, marine, aerospace, oil & gas, infrastructure, and heavy machinery | Commonly applied in residential, commercial, and light-duty applications |

| Substrate Compatibility | Engineered for metal, concrete, composites, plastics, pipelines, tanks, and industrial equipment | Mainly applied on walls, wood, and general-purpose surfaces |

| Durability | Long service life with resistance to extreme industrial conditions and mechanical stress | Lower durability under aggressive environmental or chemical exposure |

| Regulatory & Performance Standards | Must comply with industrial safety, environmental, corrosion, and performance standards | Generally follows decorative and consumer safety standards |

| Maintenance Requirements | Lower maintenance frequency due to superior protective performance | Requires more frequent repainting and maintenance in demanding environments |

| Cost Structure | Higher upfront cost but lower lifecycle cost due to extended asset protection | Lower initial cost but potentially higher long-term maintenance expenses |

| Application Methods | Often applied using specialized spraying, powder coating, curing, and multi-layer coating systems | Usually applied using brushes, rollers, or conventional spray painting methods |

| End-User Industries | Automotive, aerospace, marine, industrial manufacturing, energy, mining, and infrastructure sectors | Residential construction, commercial buildings, and consumer applications |

The industrial coatings market is mature and continues to grow at a healthy rate. It is driven by growing demand for both protective and functional industrial coatings across the manufacturing, infrastructure, automotive, marine, and energy sectors. These coatings are used on metal, concrete, plastic, and composite surfaces for protection and performance. They also provide enhanced resistance to corrosion and chemicals and aid in retaining thermal stability. These factors are driving the growing importance of industrial coatings in extending the lifespan of items and, consequently, reducing overall costs.

The industrial coatings market comprises protective and functional coatings applied to industrial substrates. The purpose is to enhance functionality. The coatings have protective properties against corrosion, chemicals, abrasion, and high and low temperatures. Demand for corrosion protection coatings and high-performance industrial coatings is closely linked to the growth of industrial production and the need to meet regulatory requirements. Therefore, industrial coating is becoming an important input critical to the reliability of the manufacturing operation and is no longer a matter of an optional or discretionary outlay.

Another significant factor driving demand for industrial coatings, or hard coatings, is the robust growth in key end-use industries, including automotive, aerospace, construction, marine, and oil & gas. These coatings not only enhance the appeal but also protect vehicles from environmental damage, extending their lifespan in the automotive sector. In construction, they protect steel and concrete from corrosion and wear, thereby creating long-lasting, safe structures. The increasing demand for high-performance coatings and advances in formulation technology continue to drive market growth.

Market Dynamics

Stringent Environmental Regulations

Stringent government regulations on environmental issues are driving the industrial coatings market. Governments are working towards lowering VOC emissions from coatings to control air pollution and related human health concerns. For instance, the EU’s VOC Emissions Directive regulates VOC content in paints and varnishes intended for architectural and vehicle uses. Analytical research indicates that such regulations have increased the use of water- and powder-coatings across various industry segments. These coatings emit much lower VOC levels than solvent-based coatings.

The shift toward low-VOC industrial coatings, waterborne industrial coatings, and powder coatings is accelerating across industries. Manufacturers are aligning with sustainability rules and ESG goals. These coatings have lower environmental impacts without compromising performance. Currently, these coatings are used in car refinishing, maintenance, and construction.

Expansion of Infrastructure Development

Modern governments are spending abundantly on roads, construction, and utility services. Many such projects involve large metal and concrete structures that require high-quality protective coatings. The Global Infrastructure Hub reports that the world will require $94 trillion in infrastructure investment by 2040. According to NCBI, long-lasting coatings lower maintenance costs. The growing number of infrastructure projects, especially in emerging markets, has driven demand for industrial paints.

Growing Automotive Production and Demand

The role of coatings cannot be overstated, especially in the automotive industry. The coating solutions enhance the aesthetics and durability of vehicles. The coating protects the vehicles against scratches, corrosion, UV exposure, and other environmental adversities. Global car and light-vehicle production returned in 2022, according to the Bureau of Transportation Statistics. Global car manufacturing in 2023 was approximately 90 million units, indicating strong demand for vehicle coatings applied to OEM and refinishing applications. Furthermore, the rising trend of vehicle customization and the increasing focus on exterior finishes are also boosting the demand for a variety of specialized industrial coatings in the automotive sector. Therefore, growing automotive production and global vehicle demand are significant drivers.

Segmental Insights

Market Assessment By Technology

Based on industrial coatings by technology, the market is segmented into solventborne, waterborne, powder-based, and other advanced coating technologies. The solventborne coatings segment holds the largest share of 46.3%. These coatings are also known for their good performance and higher durability. These are resistant to environmental conditions such as temperature and humidity during the curing process. These are applied in factories related to general manufacturing, oil and gas, marine, and automotive.

The waterborne coatings market is also projected to expand at a faster rate. The main reasons for this growth are increased awareness of environmental protection and stringent regulation of VOC levels in most markets. Waterborne coatings are in high demand for their environmentally friendly properties, low VOC content, low odor, and long durability. The automotive refinish industry drives this demand due to environmental regulations and a desire for high-quality finishes.

Market Evaluation By Resin

The segmentation, by resin, includes epoxy, acrylic, alkyd, polyester, polyurethane, fluoropolymer, and others. The epoxy resin segment accounts for the largest share of 31.10% . Epoxy coating offers many benefits, including excellent adhesion, chemical resistance, and mechanical properties. Hence, they can be applied to a variety of industrial applications, including metal coating and floor protection. The widespread application of epoxy coatings across industry and related fields is a major factor driving its current market share.

The polyurethane resin market is anticipated to register the fastest growth. This is owing to the increasing demand for paints that possess flexibility, abrasion resistance, and durability. Polyurethane paints are widely used in the automotive, aircraft, and wood industries. Improvements in polyurethane technology are also driving increased use of polyurethane resins across various industrial applications.

Market Evaluation By End Use

The segmentation, by end use, includes general industry, automotive, aerospace, power generation, oil and gas, mining, and others. The general industry sector has the largest market share of 46.52%. It covers many application areas in the manufacturing industry, such as equipment manufacturing, metal fabrication, and infrastructure. Industrial coating has numerous applications across general industries, where it is used to protect and enhance equipment and infrastructure. The large number of application areas makes this market sector the largest.

The automotive segment is growing at the fastest rate. This is due to the growing demand for high-performance coatings worldwide. These coatings possess advanced properties and can withstand natural degradation. The advancement of technology and the attention to vehicle longevity and beauty are factors behind the rapid expansion within the market.

Regional Analysis

By region, the study provides insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The market can be divided into various regions, such as North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. All these regions have their own set of trends, depending upon industrialization, government policies, and major industries. Asia Pacific and North America have the largest markets; however, other markets are growing rapidly as industrialization increases.

Asia Pacific industrial coatings market size is the largest with 43.40% revenue share and fastest-growing. This is due to the rapid growth of industries such as automotive, construction, and manufacturing in countries like China and India. The Infrastructure development in China and the growth of manufacturing facilities are driving demand for coatings. Increased income and manufacturing also drive demand for coatings. The adoption of advanced coating technologies in India and increased public awareness of them have driven demand for coatings.

Which Country Dominated the Asia Pacific Industrial Coatings Market in 2025?

China industrial coatings market is supported by large infrastructure projects, strict environmental regulations, and the growing use of sustainable coating technologies. Industrialization and infrastructure development in transportation, energy, and manufacturing are driving market demand. Strict environmental regulations drive the use of low-VOC, eco-friendly coatings. Economic conditions remain favorable, thereby enhancing industry growth. Also, the need for sustainable solutions increases the growth of this industry. Below is an overview of the competitive approach of major firms:

| Company | Strategic Focus | Key Initiatives |

| Akzo Nobel N.V. | Shift toward B2B performance coatings |

|

| PPG Industries, Inc. | Expansion through manufacturing and distribution network optimization |

|

| RPM International Inc. | Focus on protective coatings for industrial applications |

|

| Jotun | Focus on marine and protective coatings |

|

| Sherwin-Williams | Expansion of product portfolio and regional presence |

|

Companies are focusing on innovation, sustainability, and strategic partnerships. They are expanding their presence in emerging markets. They help maintain competitiveness in the industrial coatings sector.

The North America industrial coatings market is expected to register CAGR of 3.86%, driven by significant demand from established manufacturing sectors, ongoing infrastructure development, and an increasing focus on high-performance and eco-friendly solutions. The construction industry is expanding rapidly due to urbanization and infrastructure development, thereby boosting demand for industrial coatings to protect and enhance buildings. The US market is expanding significantly due to a large automotive and aircraft manufacturing sector. Water protection coating is utilized in these sectors. Environmental regulations in the US include control of VOC emissions. By this regulation, water-soluble and UV coatings are favored. Additionally, significant reconstruction activities and continuous infrastructure development are creating substantial opportunities for high-performance protective coatings.

Key Players and Competitive Insights

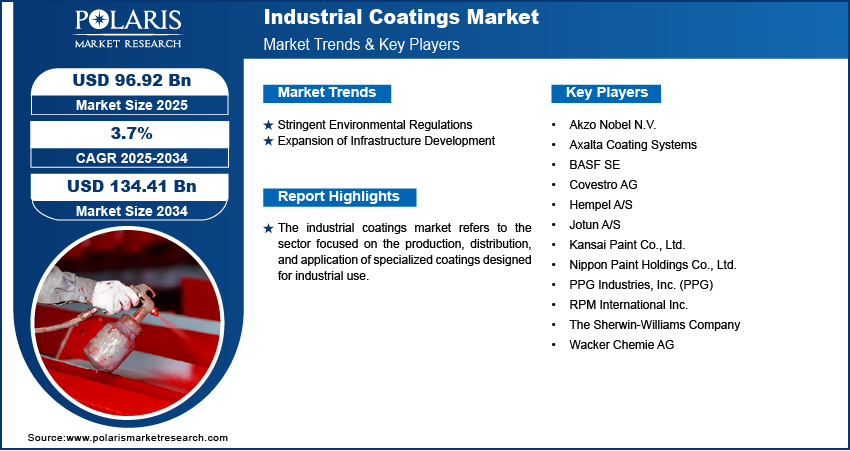

A few of the major players in the industrial coatings market include PPG Industries, Inc. (PPG); The Sherwin-Williams Company; Akzo Nobel N.V.; RPM International Inc.; Axalta Coating Systems; BASF SE; Kansai Paint Co., Ltd.; Nippon Paint Holdings Co., Ltd.; Hempel A/S; Jotun A/S; Wacker Chemie AG; and Covestro AG. These companies offer a wide range of industrial coating solutions catering to diverse end-use industries and applications.

The industrial coatings market competitive landscape is characterized by several competitors across international and regional markets. Innovation, technology, quality, price, and consumer satisfaction are the critical factors driving competition in the industrial coatings market. A lot of interest has been generated in the development of environmentally friendly and advanced coatings. Partnerships, acquisitions, and expansion are also being pursued to boost market share and meet consumer demand.

PPG Industries, Inc. (PPG) has its headquarters in Pittsburgh, USA. The company provides coatings for industry – liquids, powders, and electrocoating – with a focus on the automotive, aerospace, industrial equipment, and packaging markets. At PPG, the answer to meeting the needs of different industries is innovation and sustainability.

AkzoNobel N.V., based in Amsterdam, the Netherlands, provides protective industrial coatings. Its main products include protective, marine, and coil coatings. The company is a major player focused on advanced, green coatings. Target industries comprise, among others, Oil & Gas, Infrastructure, and Transport.

List of Key Companies in Industrial Coatings Market

- Akzo Nobel N.V.

- Axalta Coating Systems

- BASF SE

- Covestro AG

- Hempel A/S

- Jotun A/S

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc. (PPG)

- RPM International Inc.

- The Sherwin-Williams Company

- Wacker Chemie AG

Industrial Coatings Industry Developments

February 2026: Henkel announced that it had agreed to acquire the Dutch-based Stahl Group. It had signed the deal with a purchase price of 2.1 billion euros. It is majority-owned by the Wendel SE, a French Private Equity firm. Stahl offers high-performance specialty coatings for flexible materials. It serves leading brands across fashion & lifestyle, automotive, and packaging markets around the world. (Source: henkel.com)

In November 2025: PPG introduced the ENVIROCRON Extreme Protection Edge Plus, a powder coating designed for use by various industries such as heavy-duty equipment, HVAC, and electrical. (Source: ppg.com)

What is the Future of the Industrial Coatings Market?

The market is expected to witness strong growth in the coming years. The expansion would be driven expanding automotive, aerospace, marine, and industrial manufacturing activities worldwide. Also, rapid infrastructure development will propel the growth. Rising regulatory emphasis on environmental sustainability will accelerate demand for low-VOC, waterborne, powder, and bio-based coating solutions. There are growing technological advancements in smart coatings, nano-coatings, and self-healing protective materials. These innovations enhance coating performance, durability, and operational efficiency. In addition, AI-enabled coating manufacturing systems and automated quality monitoring technologies are improving production precision and reducing material waste. Growing industrial focus on corrosion protection, lifecycle cost reduction, and long-term asset durability supports market expansion

Industrial Coatings Market Segmentation

By Technology Outlook (Revenue – USD Billion, 2021–2034)

- Solventborne

- Waterborne

- Powder Based

- Others

By Resin Outlook (Revenue – USD Billion, 2021–2034)

- Epoxy

- Acrylic

- Alkyd

- Polyester

- Polyurethane

- Fluoropolymer

- Others

By End Use Outlook (Revenue – USD Billion, 2021–2034)

- General Industry

- Automotive

- Aerospace

- Power Generation

- Oil and Gas

- Mining

- Others

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indnesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Industrial Coatings Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 95.75 billion |

| Market Size in 2026 | USD 98.91 billion |

| Revenue Forecast by 2034 | USD 130.50 billion |

| CAGR | 3.5% |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Industrial Coatings Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

How is the Report Valuable for an Organization?

Workflow/Innovation Strategy: The industrial coatings industry has been bifurcated on the basis of technology, resin type, and end-use applications. In addition, the report provides the reader with a clear insight into the various segments, both globally and regionally.

Market Entry Strategies: A prominent growth strategy is continuous product innovation. The core business involves high-performance, sustainable, and specialty coatings. Collaboration with industries could accelerate market expansion and focus on high-growth geographies. Marketing emphasizes product performance, economic value, and environmental sustainability. The delivery of customized solutions, along with technical support, fosters long-lasting relationships with customers. Online marketing and trade shows are other ways to improve market visibility.

FAQ's

The global industrial coatings market was valued at USD 95.75 billion in 2025 and is projected to grow at a CAGR of 3.5% from 2026 to 2034, reaching USD 130.50 billion in 2034. The market is driven by increased infrastructure spending and industrialization, which are driving demand for industrial coatings.

Solvent-borne industrial coatings currently have the largest market share in 2024 due to their superior durability, chemical resistance, and performance in extreme conditions. Nevertheless, the waterborne coatings market is anticipated to grow most rapidly due to increased VOC regulations.

The general industry sector is the major market segment with the widest application. The coatings applied to machines, metal fabrication, industrial equipment, and infrastructure fall under it. The automobile, aerospace, oil & gas, and power sectors are major end-use markets with high growth rates.

The Asia Pacific market dominates the industrial coatings market globally and accounted for the largest market share of 43.40% in 2025. The market is fueled by swift industrialization, growing manufacturing, and infrastructure development, specifically in China and India.

There is an increasing demand for environmentally friendly coatings in the industrial sector due to stringent regulations on VOC emissions. To meet these requirements, there is an increasing trend toward low-VOC, waterborne, and powder coatings.

Following are a few of the trends: ? Increasing Demand for Sustainable Coatings: Driven by stricter environmental regulations and growing consumer awareness, there's a significant shift toward eco-friendly coatings with low or zero VOC content, such as waterborne, powder-based, and UV-cured coatings. ? Advancements in Coating Technologies: Continuous innovation in materials science is leading to the development of high-performance coatings with enhanced properties such as self-healing capabilities, anticorrosion, antimicrobial, and improved durability. Nanotechnology is also playing a crucial role in enhancing coating performance. ? Focus on Energy Efficiency: Coatings that contribute to energy savings, such as heat-reflective coatings for buildings and coatings that improve the efficiency of solar panels and electric vehicle batteries, are gaining traction.

Industrial coatings are specialized protective or functional layers applied to surfaces in various industrial sectors. Unlike decorative paints and coatings, their primary purpose is to enhance the performance, durability, and longevity of the underlying materials. These coatings are engineered to withstand harsh conditions such as corrosion, abrasion, chemical exposure, extreme temperatures, and UV radiation, thereby safeguarding industrial assets and reducing maintenance costs. They are applied to a wide range of substrates, including metals, concrete, wood, and plastics, across diverse end-use industries such as automotive, aerospace, construction, oil & gas, and general manufacturing.

Download Sample Report of industrial coatings market

Please fill out the form to request a customized copy of the research report.