Integrated Delivery Network Market Size, & Growth Analysis Report, 2026-2034

REPORT DETAILS

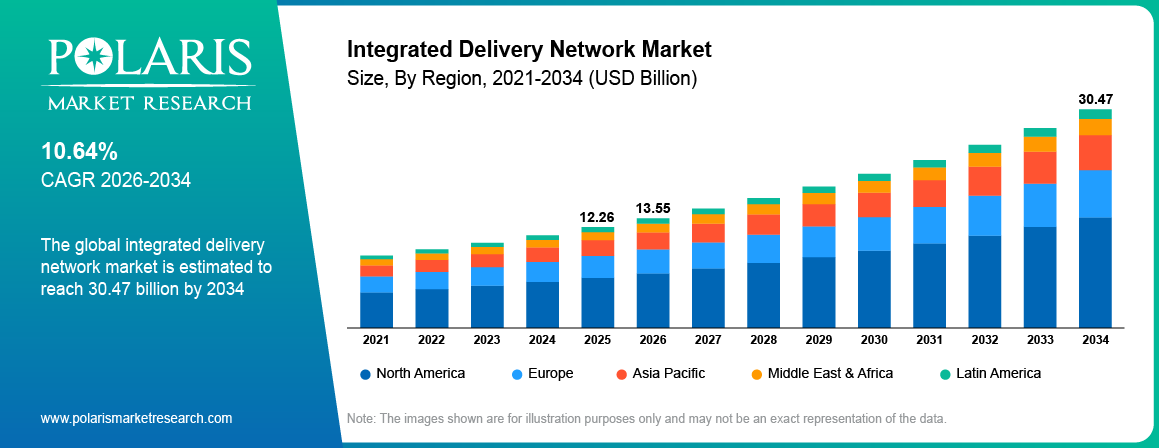

Integrated Delivery Network Market Summary

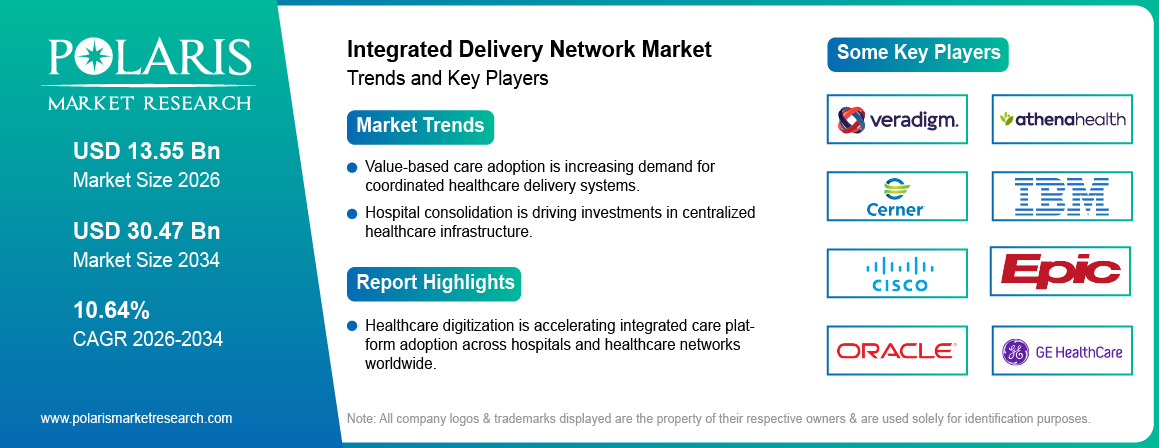

The global integrated delivery network market is estimated around USD 12.26 Billion in 2025,with consistent growth anticipated during 2026–2034. This growth is driven by healthcare digitization, hospital consolidation, and value-based care adoption are driving demand for centralized systems that improve care coordination and operational efficiency. The market is projected to grow at a CAGR of 10.64% during the forecast period.

Market Statistics

Key Takeaways

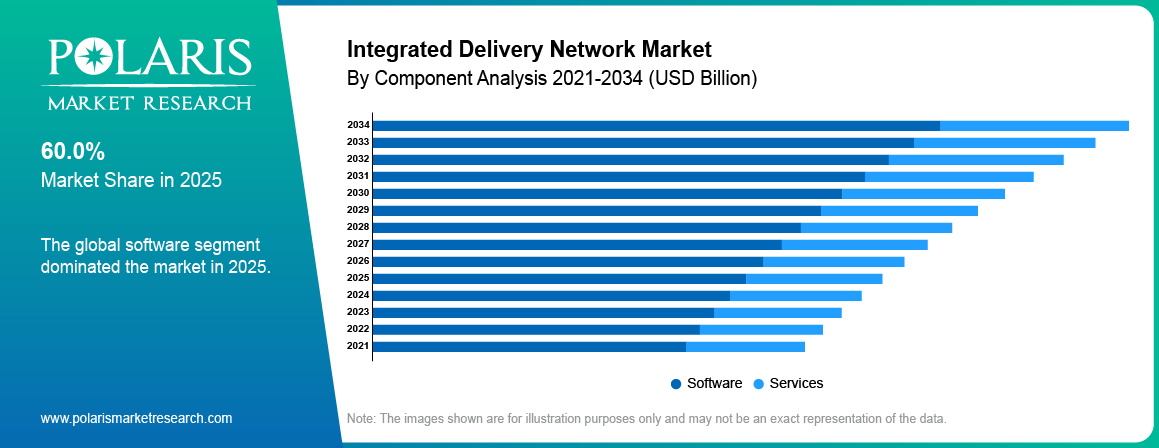

- The software segment dominated the market in 2025 with 48.9% share due to rising adoption of healthcare interoperability platforms.

- Population health management dominated the application segment with 29.0% share in 2025 due to growing focus on preventive care.

- Hospitals dominated the end use segment in 2025 with 47.0% share due to large-scale healthcare infrastructure investments.

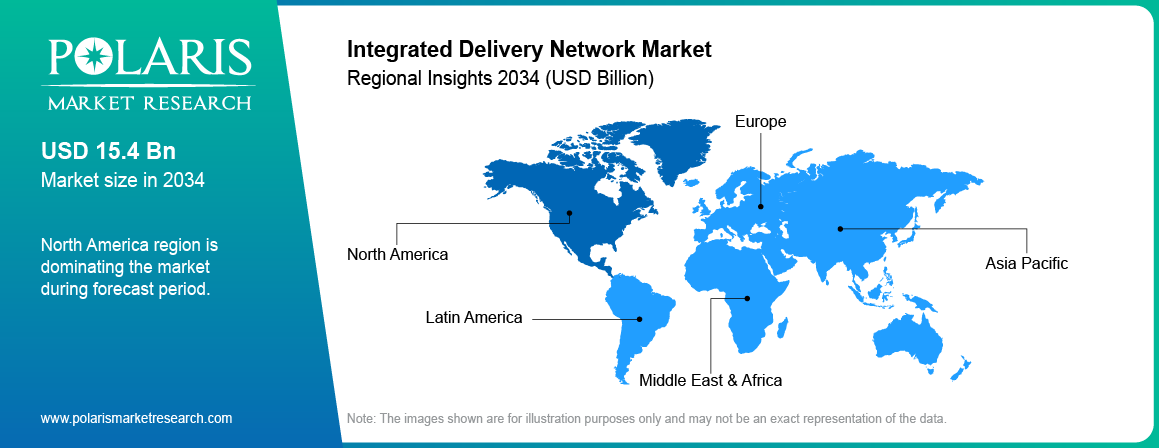

- North America dominated the global market in 2025 with 48.9% share.

- Asia Pacific is projected to grow at the fastest CAGR of 18.5% during the forecast period.

- Major companies operating in the market include Veradigm Inc., Athenahealth, Cerner Corporation, Cisco Systems, Epic Systems Corporation, and others.

Industry Dynamics

- Rising healthcare digitization is increasing adoption of integrated healthcare systems.

- Hospital consolidation trends are supporting market expansion.

- Legacy infrastructure creates interoperability challenges.

- AI-powered care coordination platforms are creating growth opportunities.

What is Integrated Delivery Network?

Integrated delivery networks are connected healthcare organizations that provide coordinated medical services across hospitals, physician groups, outpatient centers, pharmacies, and digital health platforms. They help healthcare service providers become more efficient, effective, and profitable.

The value chain comprises software companies for healthcare, cloud computing technology companies, hospitals, insurance companies, diagnostic centers, pharmaceuticals, and consumers. Technology companies provide interoperability services, data analysis services, and workflow management services to healthcare service providers.

Source: Polaris Market Research Analysis

Growth in the industry has been fueled by increasing use of centralization in healthcare processes. The trend towards health information technologies and data analysis tools has improved the efficiency of healthcare service providers.

Drivers & Opportunities

Rising Adoption of Value-Based Care Is Increasing Market Demand: The healthcare industry is shifting from the fee-for-service model to the value-based care model. In February 2026, Optum rolled out a new value-based care model that uses artificial intelligence to improve care coordination, reduce expenses, and prevent any gap in the delivery of care services. Such transformation requires coordination between healthcare facilities, healthcare providers, and insurance companies. Integrated delivery networks are utilized by providers to reduce readmission rates and manage their risks.

Growing Hospital Consolidation Is Supporting Market Growth: Healthcare companies are becoming very proactive in their efforts to enter into mergers and acquisitions to create strong service networks. Large hospitals need a good centralized structure as they run through various institutions. The merger and acquisition process leads to effective resource management, patient information flow, and process visibility within healthcare organizations. According to the World Health Organization, hospital expenditures account for 40% of total health care expenditures, while outpatient care and pharmacies account for 31% and 29%, respectively.

Restraints & Challenges

Legacy Infrastructure Is Limiting Market Growth: Many organizations in the healthcare industry employs the outdated systems, posing difficulties with interconnectivity. Data silos, high costs involved with moving data, and cybersecurity issues are some of the major hurdles. Smaller healthcare organizations tend to postpone investments due to their financial limitations.

Opportunity

AI-Powered Healthcare Coordination Is Creating Growth Opportunities: The use of artificial intelligence leads to many opportunities for firms. AI has been adopted by many healthcare organizations for better staffing and workflow optimization. In April 2026, Viz.ai and National Rural Health Association initiated a partnership to develop AI-based detection and care coordination programs for rural hospitals. As AI-enabled care coordination platforms are expected to improve long-term operational efficiency.

Source: Polaris Market Research Analysis

Segmental Insights

The report provides a comprehensive analysis of the integrated delivery network market by component, application, and end use to pinpoint the key revenue generating and growth segments.

By Component

-

Software

The software segment dominated the market in 2025 with 60.0% share due to rising adoption of interoperability platforms, EHR systems, and analytics solutions. Healthcare companies are adopting centralized software systems to ensure efficiency in their operations. The software systems assist healthcare companies in enhancing the availability of patient information and reducing delays within administrative processes.

-

Services

Services segment is expected to grow at the highest CAGR of 9.7% during the forecast period owing to the increasing requirement for implementation, consulting, cloud migration, and managed services. Healthcare companies require assistance in adopting new technologies and integrating them into the digital infrastructure.

By Application

-

Population Health Management

The population health management segment is dominating the market with 29.0% share in 2025 owing to an increasing emphasis on preventive healthcare. Providers are using analytics platforms to improve long-term patient outcomes. Rising cases of chronic diseases are increasing demand for coordinated patient monitoring systems.

-

Revenue Cycle Management

The revenue cycle management segment is projected to grow at the fastest CAGR of 9.5% during the forecast period due to rising demand for billing automation and financial optimization tools. Healthcare organizations are now implementing automation in their payment processes to minimize claim errors and optimize cash flow management.

By End Use

-

Hospitals

The hospitals segment led the market during 2025 with 47.0% share due to increased funding for enterprise healthcare systems and system improvements. Hospital chains have been installing integrated solutions to enhance patient coordination between different locations.

-

Ambulatory Care Centers

The ambulatory care centers segment is projected to grow at the fastest CAGR of 11.2% during the forecast period due to rising outpatient care demand and remote monitoring adoption. Expanding same-day treatment services are increasing demand for connected healthcare platforms.

Source: Polaris Market Research Analysis

Regional Analysis

North America Integrated Delivery Network Market Overview

North America dominated the market in 2025 with 48.9% share due to advanced healthcare IT infrastructure and high healthcare spending. The US remains the largest contributor due to strong hospital consolidation activity and rising investment in AI-enabled healthcare systems. Increasing adoption of value-based healthcare services is driving regional market growth. In March 2025, Beckman Coulter received FDA clearance for its DxC 500i analyzer to help integrated delivery networks streamline lab operations and improve testing efficiency.

Asia Pacific Integrated Delivery Network Market Insights

Asia Pacific is projected to grow at the fastest CAGR of 13.0% during the forecast period due to rising healthcare expenditure and rapid digital transformation. According to China’s National Bureau of Statistics, healthcare and medical services spending reached approximately USD 357 billion in 2025 (RMB 2,573 billion), up from around USD 354 billion in 2024 (RMB 2,547 billion). China, India, Japan, and South Korea are expanding healthcare infrastructure investments. Growing private hospital expansion is creating additional demand for integrated healthcare systems.

Europe Market Insights

Europe has a significant market share of 28.0% share in 2025 due to the rise in healthcare modernization projects. Germany, France, and the UK are allocating funds for centralized healthcare systems. Digital health services backed by government funding are gaining acceptance in healthcare networks. According to a press release by the European Commission in March 2026, 23% of digital health vendors in the EU are currently focusing on AI/ML technology and AI diagnostics are expected to touch 80% by 2029.

Latin America and Middle East & Africa

Latin America and Middle East and Africa regions are witnessing consistent growth with 9.5% as a result of improvements in their health care infrastructure and rising investments in healthcare by the public and private sector. Brazil, Mexico, Saudi Arabia, and UAE are playing significant roles owing to increasing adoption of digital health systems and smart hospitals in these regions

Source: Polaris Market Research Analysis

Competitive Landscape & Key Players

The market is moderately fragmented owing to the existence of healthcare IT solution providers, enterprise software vendors, and cloud infrastructure providers. The main aspects of competition include price, interoperability, innovation, and quality of services. Companies are focusing on acquisitions, AI integration, cloud expansion, and strategic partnerships to strengthen market position.

Among the major companies operating in this industry are Veradigm Inc., Athenahealth, Cerner Corporation, Cisco Systems, Epic Systems Corporation, GE HealthCare, IBM Corporation, McKesson Corporation, Microsoft Corporation, Oracle Corporation, Optum Inc., Siemens Healthineers., and others.

Premium Insights

The next phase of growth in the integrated delivery network market is expected to be supported by increasing investments in connected healthcare infrastructure and intelligent care coordination platforms. Healthcare providers are focusing on centralized ecosystems that improve patient outcomes, reduce operational costs, and strengthen financial performance across multi-location networks.

Key future growth areas include:

- AI-powered clinical workflow automation

- Population health analytics expansion

- Virtual care integration

- Real-time interoperability platforms

- Predictive patient management systems

- Cloud-based healthcare infrastructure modernization

Healthcare businesses that develop fully integrated digital ecosystems featuring high levels of interconnectivity, automation, and consumer involvement can look forward to greater efficiency and competitiveness in the future.

Key Players

- Veradigm Inc.

- Athenahealth

- Cerner Corporation

- Cisco Systems

- Epic Systems Corporation

- GE HealthCare

- IBM Corporation

- McKesson Corporation

- Microsoft Corporation

- Oracle Corporation

- Optum Inc.

- Siemens Healthineers

Industry Developments

- January 2025: Arrive Health partnered with Amazon Web Services and a leading integrated delivery network to launch a generative AI solution that speeds medication access. [source: arrivehealth.com]

Integrated Delivery Network Market Segmentation

By Component Outlook (Revenue, USD Billion, 2021-2034)

- Software

- Services

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Population Health Management

- Revenue Cycle Management

- Care Coordination

- Clinical Data Management

By End Use Outlook (Revenue, USD Billion, 2021-2034)

- Hospitals

- Ambulatory Care Centers

- Diagnostic Centers

- Specialty Clinics

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Integrated Delivery Network Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 12.26 Billion |

| Market Size in 2026 | USD 13.55 Billion |

| Revenue Forecast by 2034 | USD 30.47 Billion |

| CAGR | 10.64% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The global market size was valued at USD 12.26 Billion in 2025 and is projected to grow to USD 30.47 Billion by 2034.

North America dominated the market in 2025 with 48.9% share due to strong healthcare IT infrastructure and high spending on digital healthcare systems.

The software segment dominated the market with 60.0% share in 2025 due to rising demand for interoperability platforms, EHR systems, and analytics tools.

A few of the key players in the market are Veradigm Inc., Athenahealth, Cerner Corporation, Cisco Systems, Epic Systems Corporation, GE HealthCare, IBM Corporation, McKesson Corporation, Microsoft Corporation, Oracle Corporation, Optum Inc., Siemens Healthineers, and others.

Growth is driven by healthcare digitization, hospital consolidation, and value-based care adoption across global healthcare systems.

The hospitals sector occupied 47.0% share of the market in 2025 owing to increasing investments in infrastructure and integrated health care delivery systems.

Integration of AI and predictive analysis is anticipated to lead to future growth prospects.

Download Sample Report of Integrated Delivery Network Market

Please fill out the form to request a customized copy of the research report.