Operating Room Management Software Market Size & Share Global Analysis Report, 2026-2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Operating Room Management Software Market Summery

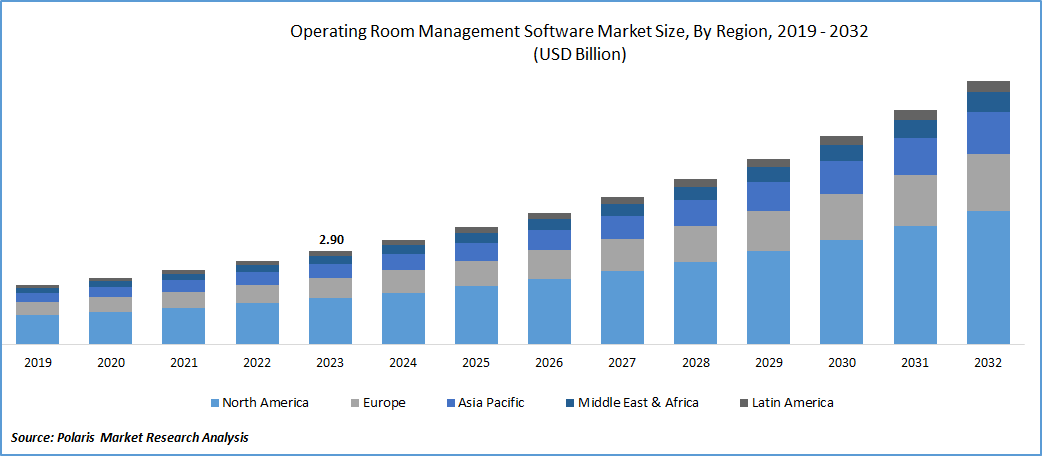

The global operating room management software market was valued at USD 3.65 billion in 2025 and is expected to grow at a CAGR of 12.4% during the forecast period. The growth is driven by rise in the number of surgical procedure wordwide, advancement in the technology, and increase in the adoption of electronic health record.

Market Statistics

Growth is due to increasing adoption of electronic health records (EHRs), a rise in the number of surgical procedures, a heightened focus on cost reduction and efficiency improvements in hospitals and ambulatory surgery centers (ASCs), and advancements in technology associated with managing operating rooms (ORs). As the healthcare sector undergoes substantial digital transformation, these software solutions have become indispensable. They play a crucial role in optimizing surgical scheduling, resource allocation, and the management of patient data, ultimately enhancing efficiency and the quality of patient care.

To Understand More About this Research: Download Sample Report

An increase in the volume of surgical procedures is expected to drive the demand for software, leading to market expansion. The COVID-19 pandemic has profoundly influenced the market, particularly during its initial phases. This decline had adverse effects, as outlined in a study published in the British Journal of Surgery, which reported the postponement or cancellation of 28 million surgeries worldwide in 2020. Many of these delayed surgeries were rescheduled for 2021, creating an increased need to enhance scheduling efficiency. In response to this demand, various technologies have been introduced by companies to address the evolving landscape of surgical procedures.

Industry Dynamics

Growth Drivers

Advancements in technology

Furthermore, advancements in artificial intelligence and data analytics are poised to be key drivers of market growth. The escalating prevalence of chronic diseases on a global scale also plays a significant role in the rising need for efficient operating rooms, primarily due to the nature of severe chronic illnesses often requiring surgical interventions. A notable example is a study published by JAMA Network Open in 2021, which disclosed that over 13 million surgical procedures were conducted across 49 U.S. states from 2019 through 2021. The study reported a 10% decline in surgical procedures by the end of 2020 compared to 2019, largely attributed to the impact of the COVID-19 pandemic.

Key OR Software Trends

| Trend | Description | Key Drivers | Examples from Practice |

| AI/ML case duration prediction | Machine learning models (e.g., XGBoost) forecast surgical durations using historical EHR data, surgeon/procedure specifics, reducing overruns by 10-20%. | Block time under/overutilization; variability in surgeon speeds and case complexity. | XGBoost models outperform traditional regression for surgeon-specific predictions; integrated into scheduling tools. |

| EHR/perioperative integration | Standardized data mapping from AIMS/EHR to central repositories enables semantic interoperability across vendors for research/quality metrics. | Heterogeneous EHRs limit secondary use; need for de-identified limited datasets. | MPOG extracts/transforms data into computable phenotypes (e.g., AKI definitions) from 7 vendors, 10M+ cases. |

| Real-time workflow tracking | Automated capture of case times, staff sign-in/out, vital signs for dashboards monitoring utilization, turnover, delays. | OR downtime (turnover 20-30% of capacity); need for multimodal data protocols. | Consensus on digitizing OR activities, uniform streaming via 5G/AI for efficiency. |

| Clinical decision support (CDS) | Alerts for SCIP metrics (e.g., beta-blockers, antibiotics) via AIMS improve compliance; intraoperative CDS reduces errors. | Procedural adherence gaps; documentation burdens. | AIMS alerts boost SCIP-INF-1/2 documentation; real-time CDS in perioperative tools. |

| Multimodal data management | Integration of video, sensors, wearables into OR systems for AI-driven safety (e.g., checklists, posture monitoring). | Fragmented data silos; regulatory needs for safety analytics. | Electronic WHO checklists, wearables for physiological monitoring in smart ORs. |

| Scheduling optimization | Computational models balance surgeon blocks, turnover, staff via predictive analytics for 15-25% utilization gains. | No-show rates, emergency cases disrupting electives. | AI workflows cut overtime/staff costs; landscape of OR scheduling algorithms. |

Report Segmentation

The market is primarily segmented based on solution, deployment, end use, and region.

| By Solution | By Deployment | By End Use | By Region |

|

|

|

|

To Understand the Scope of this Report: Request Customization

By Solution Analysis

Solution segment accounted for the largest market share in 2025

Data management & communication segment accounted for the largest share. These solutions play a crucial role in facilitating efficient data sharing, seamless communication, and effective collaboration among surgical teams. They establish a centralized storage system for patient information, enabling medical professionals to access critical data in real time. Moreover, these solutions simplify the sharing of patient status updates throughout various perioperative care stages, aid in maintaining schedule adherence, and streamline the exchange of media and case-related information across different operating rooms and hospital departments.

Anesthesia information management segment will grow rapidly. It is primarily driven by the growing emphasis on accurate anesthetic dosing & data management. According to the Anesthesia Patient Safety Foundation, projections indicated that by 2020, approximately 84% of the academic anesthesiology departments in the U.S. would adopt these systems, marking a notable increase from an estimated 75% in 2014. This trend is anticipated to contribute significantly to the substantial expansion of the segment in the foreseeable future.

By Deployment Analysis

Cloud segment held the significant market share in 2025

Cloud segment held the significant market share. Segment’s growth is propelled by the increasing adoption of cloud solutions in clinics aimed at enhancing efficiency and lowering costs. Cloud solutions offer scalability, enabling healthcare organizations to adjust their software usage seamlessly or expand it as needed. This adaptability empowers them to effectively address the growing needs of hospitals and cater to a larger patient population without substantial investments in infrastructure. Furthermore, the cloud affords advantages such as real-time data sharing, secure data handling, flexible storage options, and reliable performance.

On premises segment is expected to gain substantial growth rate. The introduction of new on-premises software offerings equips healthcare organizations with improved offline accessibility, compliance adherence, customization options, and heightened control over their data. This type of software enables organizations to exert more influence over system upgrades, long-term cost management, and seamless integration with their existing systems. These factors contribute to a heightened demand for and increased adoption of on-premises software within the healthcare sector.

By End Use Analysis

Hospitals segment held the significant market share in 2025

Hospitals segment held the significant market share. This dominance is driven by the escalating number of surgical procedures. The American Cancer Society reported that in the U.S. in 2021, there were around 1.9 million new cancer cases and 608,570 cancer-related deaths. Notably, 43% of all cancer diagnoses in males in 2020 were attributed to colorectal, lung, and prostate cancers. Similarly, for women, breast, lung, and colorectal cancers were identified as the three most prevalent types, accounting for an expected 50% of all new cancer diagnoses in female patients.

ASCs segment is expected to gain substantial growth rate. It is attributed to the trend of transitioning from in-patient to out-patient surgical procedures. The Ambulatory Surgery Center Association (ASCA) reported that in 2020, over 5,800 ASCs performed around 30 million procedures. The significant growth of ASCs, particularly in specialized fields like orthopedics, highlights the critical role of customized operating room management software market, positioning it as a key factor driving market growth in the foreseeable future.

Regional Insights

North America dominated the global market in 2025

North America dominated the global market. This supremacy is attributed to the swift adoption of technologically advanced products. The regional growth is fueled by factors such as well-established infrastructure, an increasing embrace of operating room management software, and the presence of major industry players. In the United States, the market is poised for expansion, driven by the innovative strategies implemented by key industry players.

The Asia Pacific will grow with substantial pace. This is primarily due to high prevalence of chronic diseases, a large patient population, and a growing number of hospitals and healthcare facilities with improving infrastructure. Moreover, in August 2021, the government of Delhi announced a USD 19 million project aimed at establishing a cloud-based hospital information management system. This initiative was anticipated to further support the healthcare technology market in the region.

Key Market Players & Competitive Insights

The market is characterized by competitiveness due to the presence of key providers. To secure higher market shares, companies are implementing diverse strategies, including forming partnerships, introducing new products, and expanding regionally.

Some of the major players operating in the global market include:

- BD

- GE Healthcare

- Getinge

- Koninklijke Philips N.V.

- Max Systems Inc.

- Oracle Corporation

- PerfectServe, Inc.

- Picis Clinical Solutions, Inc., a division of N. Harris Computer Corporation.

- Surgical Information Systems

- Veradigm LLC (Allscripts Healthcare Solutions, Inc.)

Recent Developments

- In November 2024, US-based North American Partners in Anesthesia introduced NAPA Managed Services, a comprehensive offering designed to support the essential operating room (OR) operational needs of health systems.

- In February 2024, Veradigm acquired ScienceIO to strengthen its AI-driven data analytics, elevate customer experiences across the healthcare ecosystem, and reinforce its leadership in healthcare data intelligence all with the goal of driving better patient outcomes.

Operating Room Management Software Market Report Scope

| Report Attributes | Details |

| Market size in 2025 | USD 3.65 billion |

| Market size in 2026 | USD 4.09 billion |

| Revenue forecast in 2034 | USD 10.40 billion |

| CAGR | 12.4% from 2026 – 2034 |

| Base year | 2025 |

| Historical data | 2021 – 20224 |

| Forecast period | 2026 – 2034 |

| Quantitative units | Revenue in USD million/billion and CAGR from 2026 to 2034 |

| Segments covered | By Solution, By Deployment, By End Use, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

| Customization | Report customization as per your requirements with respect to countries, region and segmentation. |

FAQ's

BD, GE Healthcare, Getinge, Philips, Max Systems are the key companies in Operating Room Management Software Market.

The global operating room management software market is expected to grow at a CAGR of 12.4% during the forecast period.

Solution, deployment, end use, and region are the key segments covered.

Advancements in technology are the key driving factors in Operating Room Management Software Market.

The global operating room management software market size is expected to reach USD 10.40 billion by 2034

Download Sample Report of operating room management software market

Please fill out the form to request a customized copy of the research report.