Ophthalmic Drug Market Size, Share Global Analysis Report, 2026-2034

REPORT DETAILS

Ophthalmic Drug Market Overview

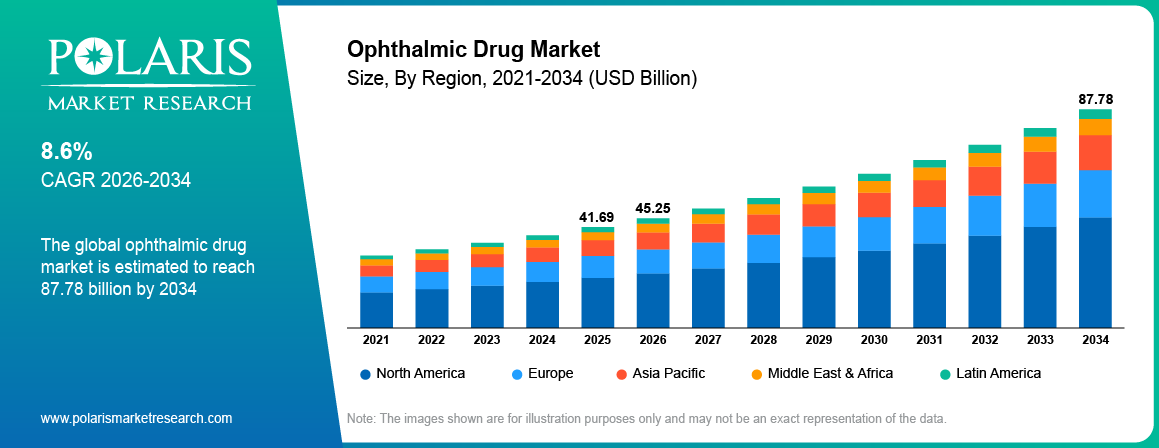

The global ophthalmic drug market was valued at USD 41.69 billion in 2025 and is expected to grow at a CAGR of 8.6% during the forecast period. The growth is driven by rising prevalence of eye disorder, rising elderly population and focus on fast track product approvals.

Market Statistics

Industry Dynamics

- The increased in research and development activities is fueling the industry growth.

- Rising prevalence of ophthalmic disease is driving the growth.

- The advancement in technology is boosting the industry growth.

- Stringent regulatory requirements and lengthy approval processes for new ophthalmic drugs limits the growth.

Impact of AI on Industry

- Speeds up the identification of potential ophthalmic drug candidates by analyzing large biomedical datasets.

- Improves patient selection, monitoring, and outcome prediction, improving the efficiency and success rate of clinical trials for eye-related drugs.

- Reduce R&D cost by streamlining preclinical and clinical phases.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Ophthalmic Drugs Market Defined

The ophthalmic drugs market involves medicines intended for the diagnosis, treatment, and management of different eye disorders like glaucoma, dry eye disease, retinal diseases, infections, allergic reactions, and eye inflammations. Such medications come in the form of eye drops, gels, ointments, injections, and implants. They assist in maintaining proper eye health, managing disease development, and preventing vision impairment.

The surge in research and development activities directed towards the creation and introduction of innovative ophthalmic drugs, in combination with various strategic initiatives envisioned by key industry players, is driving the growth. Furthermore, the unaddressed requirements within the realm of ophthalmology are likely to fuel the expansion of the ophthalmic drug market. As per a report by the World Health Organization in October 2021, an estimated 2.2 billion individuals grapple with vision impairments, encompassing both nearsightedness and farsightedness. Notably, around half of these cases, accounting for at least 1 billion instances, can be prevented through suitable treatment. Age-related factors predominantly underpin the leading causes of blindness and vision impairments. This heightened prevalence places a considerable financial burden on governments, with myopia alone estimated to cost as much as USD 244 billion in terms of vision impairment. Consequently, due to the rising incidence of eye-related disorders, the ophthalmic drug market is poised to encounter promising growth opportunities.

Ophthalmic drugs are pertained to the eye or adjoining tissue. Drugs for ocular management surface in several configurations involving solutions, ointments, suspensions, and gels and can be utilized to distribute an active pharmaceutical ingredient (API) to the exterior of the eye, within the eye, near to eye, or they can be utilized with an ophthalmic device. There is an aggregate of ophthalmic preparations obtainable over the counter for extensive sales, with the majority offering a cure for dry eye or redness.

Source: Polaris Market Research Analysis

Prescription vs OTC Ophthalmic Drugs

| Factor | Prescription Ophthalmic Medications | Over-the-Counter Ophthalmic Medications |

| Use | Treatment of serious or chronic eye diseases | Treatment of minor symptoms |

| Consultation Required | With physician | Doesn’t require consultation |

| Formulation | Strong formulation | Formulations meant to provide temporary relief |

| Diseases treated | Glaucoma, retinal disease, eye infections | Dry eyes, conjunctivitis, allergic reactions |

| Price | High | Low |

| Side effects | High risk if not used appropriately | Low risk if not used appropriately |

Source: Polaris Market Research Analysis

Industry Dynamics

Growth Drivers

What are the Factors Driving the Industry Growth?

The industry is driven by combination of various factor. Major factor driving the growth is rising prevalence of eye disorder. Eye disorder such as glaucoma, age-related macular degeneration (AMD), diabetic retinopathy, and dry eye syndrome is rising globally. This rise in the prevalence is driving the demand for the ophthalmic drugs. Moreover, the number of elderly populations is rising worldwide. This rise in the elderly population is further fueling the prevalence of eye disease, consequently driving the demand for the ophthalmic drugs. Moreover, the government focus on fast-track approvals for novel drugs are rising, due to which players with drugs are entering the industry. This in turn is driving the expansion of the industry.

Regulatory Approvals and Clinical Trials

Approval processes and clinical testing are critical to drug development for ocular therapy, as they ensure that all medications meet safety and effectiveness standards and comply with specific quality requirements to reach the market successfully. Clinical testing is a mandatory step that is necessary for all pharmaceutical companies producing drugs and aimed at proving the effectiveness of such medicines in treating eye conditions and minimizing adverse reactions. The manufacturing process, formulation, label information, and efficacy in treating the disease should be approved prior to marketing a product. Despite the additional costs and development period caused by the approval process, it guarantees the safety and efficacy of ocular drugs.

Report Segmentation

The market is primarily segmented based on disease, drug class, route of administration, dosage form, product type, and region.

| By Drug Class | By Disease | By Route of Administration | By Product Type | By Dosage Form | By Region |

|

|

|

|

|

|

Source: Polaris Market Research Analysis

To Understand the Scope of this Report: Request Customization

Which Segment By Drug Class Witness Significant Growth?

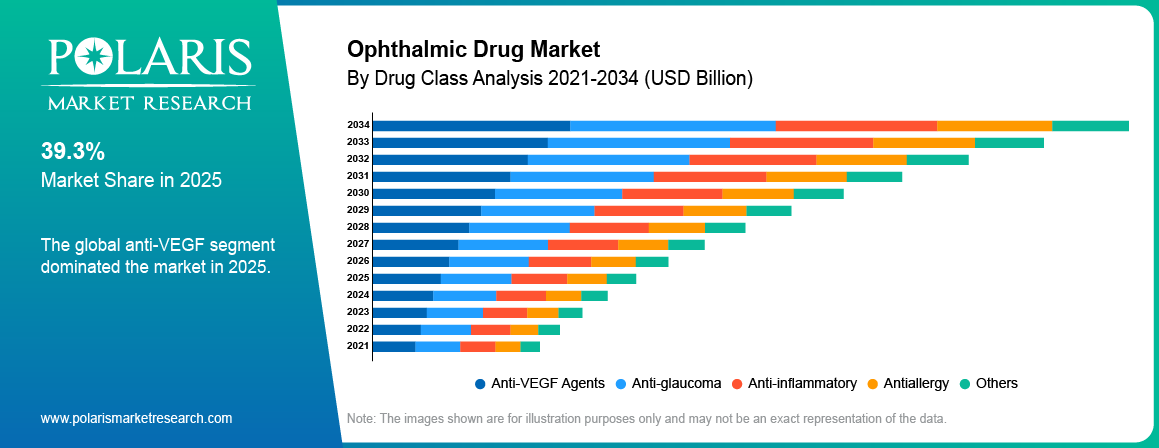

The Anti-VEGF segment is held 39.3% share in 2025. The increasing prevalence of retinal disorders such as diabetic retinopathy, age-related macular degeneration, and others, coupled with a rising rate of diagnosis for these conditions in the population, is driving the growing demand for anti-VEGF therapy in various regions. For instance, according to the CDC, approximately 20.0 million Americans were affected by age-related macular degeneration, and the global figure is projected to reach 288 million by 2040, consequently driving the segment demand in the forecast period. Furthermore, the increasing number of product approvals and launches is contributing to the segment's global growth. For instance, In January 2022, Genentech, Inc., a subsidiary of F. Hoffmann-La Roche Ltd., obtained approval from the U.S. FDA for Vabysmo, a treatment for wet, or neovascular, age-related macular degeneration and diabetic macular edema, targeting vascular endothelial growth factor.

Why Semisolid Segment Dominated in 2025?

The Semisolid segment accounted for a share of 19.0% in 2025 primarily due to the increasing approvals and product launches, encompassing ointments, suspensions, gels, and others. The expanded utilization of ointments, especially in addressing inflammatory conditions, infections, and dry eye, is contributing to their growing popularity, given their enhanced efficacy. Additionally, the segment's growth is further driven by the heightened focus of key industry players on obtaining approvals and introducing a wider range of products. For instance, In November 2021, I-MED Pharma Inc. introduced I-DEFENCE, a nighttime ointment for dry eye, to the U.S. market

Source: Polaris Market Research Analysis

Regional Insights

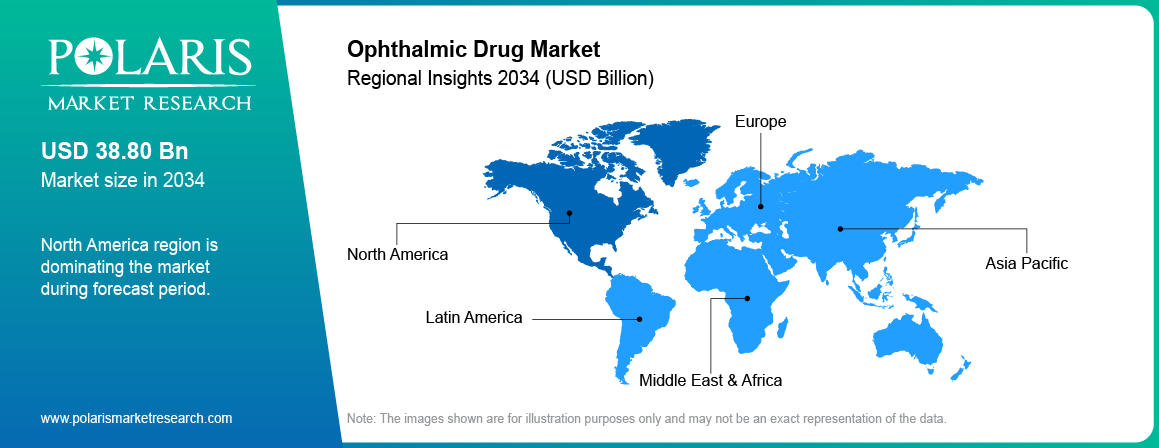

How North America Captured Largest Market Share in 2025?

North America dominated with largest share of 38.0% in 2025 due to a higher prevalence of eye diseases and an increasing awareness of these conditions. Additionally, the ongoing research and development efforts of key industry players are expected to drive regional growth further. Furthermore, North America benefits from the presence of major players such as Pfizer Inc., Alcon, and Bausch and Lomb, which drives the product accessibility, thereby driving the growth.

What are the Reasons for Asia Pacific's Significant Growth?

Asia Pacific is expected to witness significant growth at a CAGR of 13.8% during the forecast period due to several factors, including a substantial patient population, a high prevalence of eye diseases, and the emergence of local companies. Although the Asia Pacific region boasts the largest patient base, the treatment rate is comparatively lower in this area, which creates an opportunity for global players as well as local businesses. Furthermore, the implementation of various strategic initiatives by market players is anticipated to contribute to regional growth.

Source: Polaris Market Research Analysis

Key Market Players & Competitive Insights

The market is characterized by intense competition, with established players relying on advanced technology, high-quality products, and a strong brand image to drive revenue growth. These companies employ various strategies such as research and development, mergers and acquisitions, and technological innovations to expand their product portfolios and maintain a competitive edge in the market.

Some of the major players operating in the global market include:

- Alcon

- Allergan (AbbVie Inc)

- Bausch Health Companies Inc.

- Bayer AG

- Coherus Biosciences, Inc.

- Genentech, Inc. (F. Hoffmann-La Roche Ltd)

- Merck & Co., Inc

- Nicox

- Novartis AG

- Pfizer Inc.

- Regeneron Pharmaceuticals Inc

Recent Developments

- May 2026: Biogen announced the completion of the acquisition of Apellis Pharmaceuticals, Inc. According to Biogen, the strategic move adds two best-in-class commercialized products, SYFOVRE and EMPAVELI. (source: biogen.com)

- January 2026: LENZ Therapeutics, Inc. announced an exclusive commercialization partnership with Lunatus Marketing & Consulting FZCO. According to LENZ Therapeutics, the partnership focuses on expanding the international reach of its presbyopia treatment, VIZZ, in the Middle East. (source: lenz-tx.com)

- July 2025: Alcon launched TRYPTYR (acoltremon ophthalmic solution) 0.003% in the U.S. as a first-in-class treatment for Dry Eye Disease, offering rapid natural tear production and expanding options for over 30 million Americans suffering from dry eye symptoms. (Source: alcon.com)

- July 2025: Lupin launched its generic Loteprednol Etabonate Ophthalmic Suspension, 0.5% in the U.S., a bioequivalent to Bausch & Lomb’s Lotemax, expanding treatment options for steroid-responsive eye inflammation and targeting a USD 55 million annual market. (Source: lupin.com)

Ophthalmic Drug Market Report Scope

| Report Attributes | Details |

| Market size value in 2025 | USD 41.69 billion |

| Market size value in 2026 | USD 45.25 billion |

| Revenue forecast in 2034 | USD 87.78 billion |

| CAGR | 8.6% from 2026 – 2034 |

| Base year | 2025 |

| Historical data | 2021 – 2024 |

| Forecast period | 2026 – 2034 |

| Quantitative units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Segments Covered | By Disease, By Drug Class, By Route of Administration, By Dosage Form, By Product Type, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

| Customization | Report customization as per your requirements with respect to countries, region and segmentation. |

Source: Polaris Market Research Analysis

ophthalmic drug market FAQ's

• The market size was valued at USD 41.69 Billion in 2025 and is projected to grow to USD 87.78 Billion by 2034.

• The market is projected to register a CAGR of 8.6% during the forecast period.

• A few of the key players in the market are Alcon, Allergan (AbbVie Inc), Bausch Health Companies Inc., Bayer AG, Coherus Biosciences, Inc., Genentech, Inc. (F. Hoffmann-La Roche Ltd), Merck & Co., Inc., Nicox, Novartis AG, Pfizer Inc., and Regeneron Pharmaceuticals Inc.

• The semisolid segment accounted for a share of 19.0% in 2025.

• The Anti-VEGF segment held 39.3% share in 2025

• The market size was valued at USD 38.47 Billion in 2024 and is projected to grow to USD 87.37 Billion by 2034.

• The market is projected to register a CAGR of 8.6% during the forecast period.

• A few of the key players in the market are Alcon, Allergan (AbbVie Inc), Bausch Health Companies Inc., Bayer AG, Coherus Biosciences, Inc., Genentech, Inc. (F. Hoffmann-La Roche Ltd), Merck & Co., Inc., Nicox, Novartis AG, Pfizer Inc., and Regeneron Pharmaceuticals Inc.

• The semi solid segment accounted for the largest market share in 2024.

• The Anti-VEGF is expected to record significant growth.

Download Sample Report of ophthalmic drug market

Please fill out the form to request a customized copy of the research report.