Organosheet Market Outlook, Growth Drivers, Forecast 2024-2032

REPORT DETAILS

REPORT DETAILS

Market Statistics

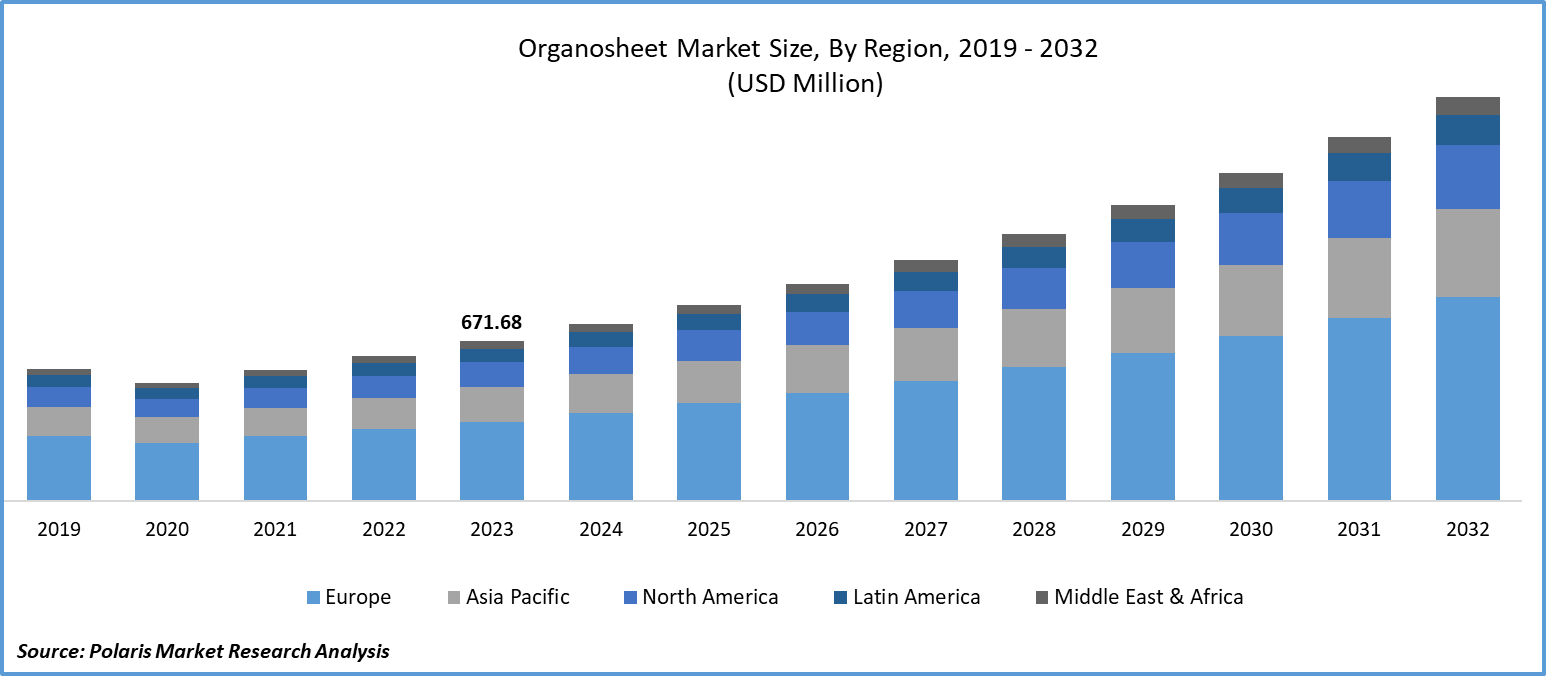

Global organosheet market size was valued at USD 671.68 million in 2023. The market is anticipated to grow from USD 743.14 million in 2024 to USD 1,696.00 million by 2032, exhibiting a CAGR of 10.9% during the forecast period

Market Overview

Organosheets are semi-finished thermoplastic fiber products with thin walls and complete consolidation. They are composed of fabrics that have been crushed and implanted in a thermoplastic plastic matrix. One benefit of the thermoplastic matrix is that hot hot-forming of semi-finished goods is possible. The molding technique was developed for composite materials after beginning in sheet metal processing.

- For instance, in July 2023, Covestro AG and Lanxess AG have announced a strategic partnership to merge their activities in polyamide 6,6. With an estimated combined revenue of approximately USD 5.51 billion (EUR 5 billion), the newly formed entity will become the leading global producer of polyamide 6,6. The acquisition is anticipated to be completed in the latter half of 2024, pending regulatory clearance.

To Understand More About this Research: Download Sample Report

The advantageous characteristics of organosheets make them appropriate for a variety of uses. Their recyclability enables them to comply with modern sustainability requirements. They can be utilized in rapid manufacturing techniques such as thermoforming and over-molding to create sizable, economical parts while preserving excellent visual appeal.

Higher demand for fabric-based organosheet and the aerospace and defense industries are driving manufacturers to develop more advanced technologies into their products, which in turn raises demand for the product. Other major factors driving the organosheet market growth include increased production efficiency due to shorter manufacturing times, rising demand for the product because of its exceptional strength, lightweight nature, and design flexibility, and rising adoption of organosheet in sustainable building systems.

Market Dynamics

Market Drivers

High resilience to fatigue and durability drives the organosheet market growth

Thermoplastic organosheets provide durability thanks to their high resistance to environmental factors and fatigue. Compared to traditional thermoset composite prepregs, thermoplastic organosheets are lighter. This weight advantage stems from their natural properties, including lower density and the capacity to form thinner and lighter structures. This makes them well-suited for use in sports equipment, aerospace, and automotive applications.

A greater emphasis on eco-friendly materials drives the organosheet market growth

Organosheets exhibit recyclability by being melted and reshaped multiple times without losing their properties, thus reducing waste generation. Their lightweight nature contributes to improved fuel efficiency in vehicles and reduces energy consumption during manufacturing and transportation. This lightweight characteristic also aids in lightweight vehicles, thereby reducing greenhouse gas emissions over the vehicle's lifetime. Additionally, organosheets require less material compared to traditional materials like metals, conserving natural resources.

Market Restraints

High expenses for manufacturing and processing

Thermoplastic organosheets reinforced with advanced fibers like carbon or glass may be more costly compared to traditional materials such as thermoset tapes. The increased cost of thermoplastic organosheets is attributed to the utilization of high-performance thermoplastic resins and advanced fiber reinforcements. Additionally, the lower production volume of thermoplastic organosheets compared to traditional materials leads to higher per-unit costs. This cost factor can hinder their extensive adoption, especially in industries with strict budget constraints.

Report Segmentation

The organosheet market report is primarily segmented based on resin type, fiber type, application, and region.

| By Resin Type | By Fiber Type | By Application | By Region |

|

|

|

|

To Understand the Scope of this Report: Request Customization

Organosheet Market Segmental Analysis

By Fiber Type Analysis

- The carbon fiber segment is projected to grow at a CAGR during the organosheet market forecast period. Lightweight carbon fibers embedded in a thermoplastic matrix—typically a high-performance polymer like PEEK, PPS, or PEI—compose carbon fiber organosheet composite materials. They have a special combination of qualities that set them apart from conventional materials and other organosheet kinds, making them extremely sought-after for use in leisure, sports, and automotive applications.

By Application Analysis

- The transportation segment accounted for the fastest-growing CAGR in 2023 and is likely to retain its position throughout the organosheet market forecast period. Organosheets are primarily utilized in aerospace and defense, transportation, sports and leisure, construction, as well as other applications such as industrial, energy, and consumer electronics. In automotive manufacturing, organosheets are favored for their lightweight properties and ease of processing. They are used to substitute metal parts, resulting in weight reduction and enhanced fuel efficiency. Additionally, organosheets are employed in sports equipment like bicycle frames, tennis rackets, and snowboards, where their high strength-to-weight ratio improves performance.

Organosheet Market Regional Insights

The European region dominated the global market with the largest organosheet market share in 2023

The European region dominated the global market with the largest organosheet market share in 2023 and is expected to maintain its dominance over the anticipated period. Strict laws like the EU Green Deal compel automakers to reduce the weight of their vehicles, which is why more and more automakers are using organosheets, which offer great strength-to-weight ratios to construct automotive parts. Organosheet is being used for battery enclosures, interior parts, kayaks, and other uses outside of the automotive industry, including the leisure and sports sector and electric mobility solutions. With its sizable automotive sector, strict environmental regulations, and ambitious recycling goals, Germany leads the pack. Notwithstanding persistent concerns about Brexit, the UK closely trails with comparable environmental goals and a robust electric vehicle industry.

The North American region is expected to be the fastest-growing region, with a healthy CAGR during the organosheet market forecast period. With many US businesses investing in new technologies to enhance product performance, the US leads the world in organosheet innovation. The aerospace and automotive industries are the main drivers of consumer demand, as they are looking for materials that are robust and lightweight to boost efficiency. Organosheet sales are steadily rising in South America, with Brazil leading the way. The increased interest in lightweight and sustainable materials in the building and transportation sectors may be the main driver of the rise.

Competitive Landscape

The Organosheet market is fragmented and is anticipated to witness competition due to several players' presence. Major service providers in the market are constantly upgrading their technologies to stay ahead of the competition and to ensure efficiency, integrity, and safety. These players focus on partnership, product upgrades, and collaboration to gain a competitive edge over their peers and capture a significant market share.

Some of the major players operating in the global market include:

- Avient Corporation

- BUFA

- Ensinger

- Haufler Composites

- Johns Manville

- Kingfa Science & Technology Co. Ltd.

- Kordsa Teknik Tekstil A.S

- Lanxess AG

- Mitsubishi Chemical Group Corporation

- Porcher Industries

- Profol GmbH

- SABIC

- SGL Carbon SE

- Teijin Limited

- Toray Industries Inc.

Recent Developments

In March 2024, Toray Industries, Inc. announced the development of a highly durable reverse osmosis (RO) membrane, designed to ensure the long-term supply of high-quality water. The new membrane retains Toray’s high contaminant removal performance, supporting industrial wastewater recycling and sewage treatment applications.

In February 2024, SGL Carbon SE disclosed that it is evaluating strategic options for its Carbon Fibers (CF) business unit, including the potential full or partial divestment. As part of the initial review phase, the company plans to engage potential buyers by sharing preliminary business information to assess acquisition interest.

In April 2023, Johns Manville showcased their state-of-the-art PA-6 Neomera® organosheets at the esteemed JEC World International Trade Show. These state-of-the-art organosheets stand out for their remarkable mechanical properties, mainly because of the novel liquid impregnation method that guarantees the best possible adherence of glass fibers within the resin matrix.

In April 2023, Valeo displayed its cutting-edge composite solutions at JEC World 2023, making its third straight visit to the leading composites trade event. Valeo is committed to sustainability and innovation, and part of that commitment is lowering its carbon footprint with the goal of becoming carbon neutral by 2050. Using organosheets, a high-performance composite that promises an average 50% reduction in CO2 equivalent and a 12% weight savings, is a crucial component of this approach.

In September 2022, Johns Manville introduced a new range of high-performance, compression-molded thermoplastic composite sheets for the automobile industry called Neomera® PX 3000. These sheets feature good rigidity, strength, and surface polish, making them ideal for lightweight interior and exterior components.

Report Coverage

The Organosheet market report emphasizes key regions across the globe to provide a better understanding of the product to the users. Also, the report provides market insights into recent developments and trends and analyzes the technologies that are gaining traction around the globe. Furthermore, the report covers an in-depth qualitative analysis pertaining to various paradigm shifts associated with the transformation of these solutions.

The report provides a detailed analysis of the market while focusing on various key aspects such as competitive analysis, resin type, fiber type, application, and their futuristic growth opportunities.

Report Scope

| Report Attributes | Details |

| Market size value in 2024 | USD 743.14 million |

| Revenue Forecast in 2032 | USD 1,696.00 million |

| CAGR | 10.9% from 2024 – 2032 |

| Base year | 2023 |

| Historical data | 2019 – 2022 |

| Forecast period | 2024 – 2032 |

| Quantitative units | Revenue in USD million and CAGR from 2024 to 2032 |

| Segments Covered | By Resin Type, By Fiber Type, By Application, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global organosheet market size is expected to reach USD 1,696.00 million by 2032.

Key players in the market are Ensinger, Toray Industries Inc., Johns Manville, Haufler Composites, SGL Carbon SE, Profol GmbH, Lanxess AG

Europe contribute notably towards the global Organosheet Market

Organosheet Market exhibiting a CAGR of 10.9% during the forecast period

The Organosheet Market report covering key segments are resin type, fiber type, application, and region.

Download Sample Report of Organosheet Market

Please fill out the form to request a customized copy of the research report.