Photoacoustic Imaging Market Demand, Growth, Industry Trends, 2026-2034

REPORT DETAILS

Photoacoustic Imaging Market Summary

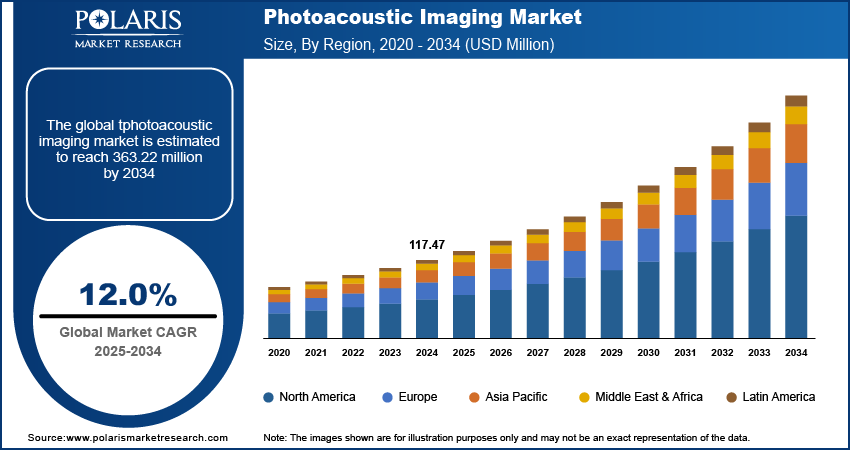

The global photoacoustic imaging market size was valued at USD 131.04 million in 2025. The market is projected to grow at a CAGR of 12.0% from 2026 to 2034. The rising adoption of photoacoustic imaging in brain imaging and skin cancer detection and the shift towards radiation-free imaging techniques are the key factors fueling market growth.

Market Statistics

Key Takeaways

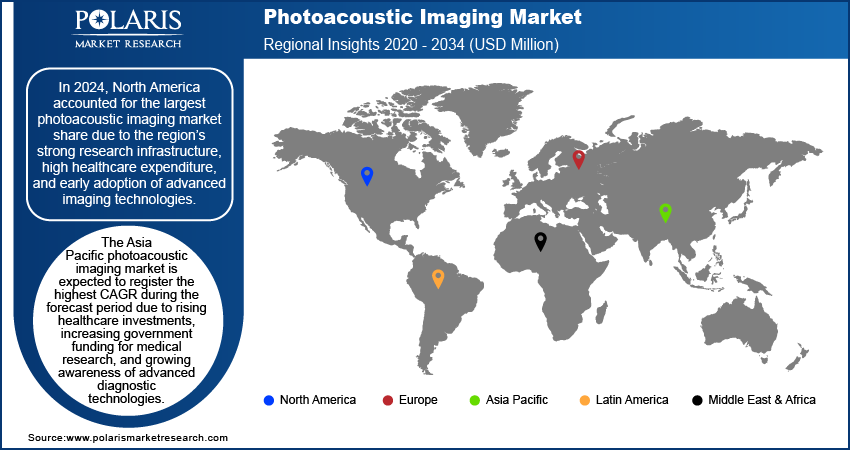

- North America accounted for the largest market share of 39.5% in 2025. This is owing to the region’s high healthcare expenditure and strong research infrastructure.

- Asia Pacific is projected to register the highest CAGR of 12.5%. This is primarily driven by the region’s rising healthcare investments and increased government funding for medical research.

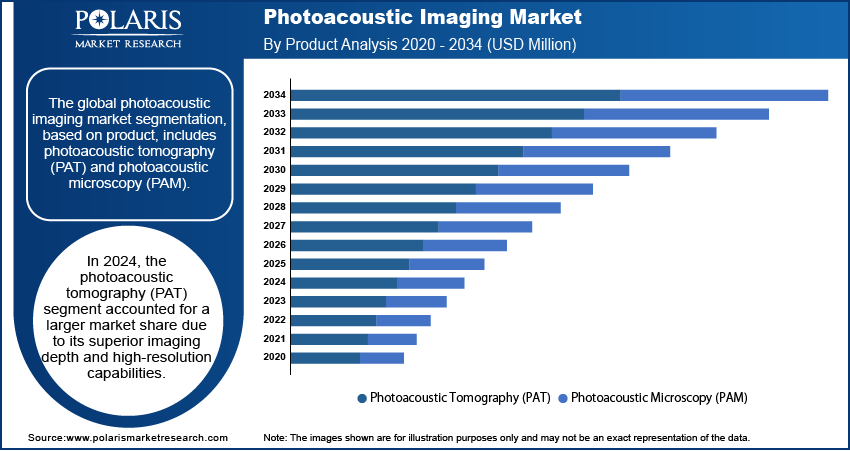

- The photoacoustic tomography (PAT) segment accounted for the largest market share of 64.3% in 2025. This is due to its excellent imaging depth and high-resolution capabilities.

- The oncology segment accounted for the largest market share of 44.3% in 2025. The rising prevalence of cancer contributes to increased demand for photoacoustic imaging in oncology.

- The cardiology segment is anticipated to register the highest CAGR of 12.6%. The growing incidence of cardiovascular diseases (CVDs) and the need for advanced imaging technologies contribute to the segment’s growth.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations

The rising adoption of photoacoustic imaging in brain imaging and skin cancer detection and the shift towards radiation-free imaging techniques are the key factors fueling market growth.

Industry Dynamics

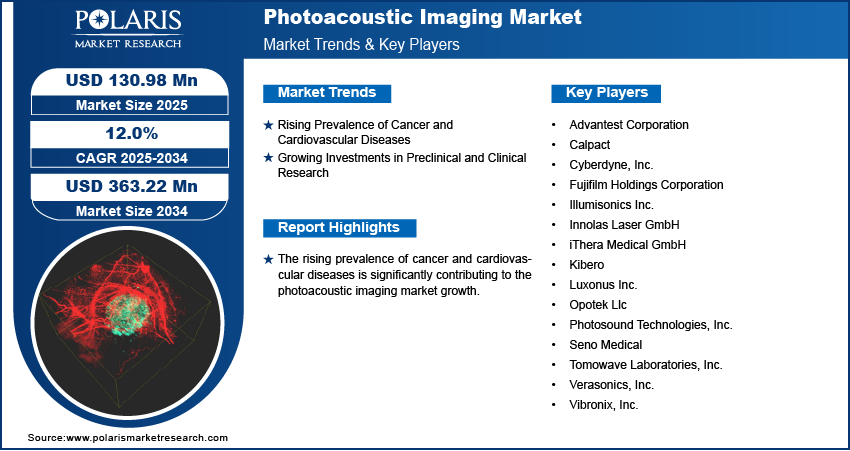

- The rising prevalence of cancer and cardiovascular diseases is fueling the demand for high-resolution imaging solutions and boosting market growth.

- Increased investment in biomedical research and drug development has led to increased need for advanced imaging techniques in therapy monitoring and disease modeling, fueling market expansion.

- The trend of personalized medicine is expected to create several market opportunities in the coming years.

- Shortage of skilled professionals may hinder market growth.

AI Impact on Photoacoustic Imaging Market

- AI-powered algorithms enhance image reconstruction. They produce clearer, high-resolution outputs from complex photoacoustic signals.

- Machine learning enables faster data interpretation, supporting early and more accurate detection of tumors, vascular diseases, and tissue abnormalities.

- AI reduces operator dependency by automating image analysis, making photoacoustic imaging more accessible in clinical settings.

- Continuous integration of AI with hybrid imaging platforms is driving innovation. It is expanding applications in oncology, cardiology, and neurology diagnostics.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Photoacoustic imaging (PAI) is an advanced biomedical imaging method that operates non-invasively. PAI functions by generating ultrasonic waves through pulsed laser irradiation of tissue, followed by reconstructing an image derived from the absorption pattern of light energy within the tissue. The ability of photoacoustic imaging to provide detailed vascular and molecular insights is boosting its adoption in brain imaging and skin cancer detection, thereby fueling photoacoustic imaging market expansion. Advancements in laser technology, increasing biomedical research, and rising demand for noninvasive imaging solutions are key factors shaping the market dynamics.

The rising shift toward safer, radiation-free imaging techniques for real-time visualization is accelerating photoacoustic imaging market demand. Furthermore, increasing Food and Drug Administration and Conformite Europeenne (CE) approvals for clinical photoacoustic imaging devices are driving market demand.

Photoacoustic Imaging vs Traditional Ultrasound & MRI

| Criteria of Comparison | Photoacoustic Imaging | Traditional Ultrasound | MRI |

| Technology | Combination of ultrasound waves and laser light. | Use of sound waves in imaging the body tissues and organs. | Use of magnetic field and radio wave imaging technologies. |

| Imaging Quality | Provision of high-quality imaging of blood vessels and tissue activities. | High quality but not detailed images for visualizing structures and shapes. | Extremely high quality imaging of soft tissues and organs. |

| Functional Imaging | Visualization of biological functions like blood flow and oxygen saturation. | Typically used to visualize anatomical shapes and structures. | Some functional images but mostly anatomical and structural imaging. |

| Speed of Imaging | Quick imaging and ability to perform imaging in real time. | Fast imaging procedures and ability to do in real time. | Typically takes much longer to perform scanning. |

| Cost and Equipment Requirements | Less costly compared to MRI, special equipment required. | Lower cost technology; widely used in healthcare organizations. | Expensive equipment needed for this technology. |

| Common Uses | For cancer diagnosis, imaging of vasculature, research purposes and more accurate diagnoses. | Main uses include pregnancy scans, heart disease and general imaging applications. | Common applications include brain, spinal cord and other joints imaging. |

Market Dynamics

Rising Prevalence of Cancer and Cardiovascular Diseases

The rising prevalence of cancer and cardiovascular diseases is significantly contributing to the photoacoustic imaging market growth. According to the New York State Behavioral Risk Factor Surveillance System, in New York State, 1.3 million adults (i.e., about 8.2% of people) have cardiovascular disease. As the demand for noninvasive, high-resolution imaging solutions increases for disease detection, the adoption of photoacoustic imaging technology is accelerating. This modality enables precise tumor detection, vascular imaging, and functional tissue characterization, enhancing diagnostic accuracy and early disease intervention. The growing need for real-time, high-contrast imaging is driving investments in research and development. Moreover, with increasing advancements in laser-based imaging and multimodal integration, the market forecast indicates sustained growth. Increasing clinical applications and supportive regulatory approvals are further strengthening the photoacoustic imaging market demand in modern medical diagnostics.

Growing Investments in Preclinical and Clinical Research

Increased funding for biomedical research and drug development is driving demand for advanced imaging techniques in disease modeling and therapy monitoring. For instance, the National Institutes of Health invested nearly USD 48 billion annually in medical research to improve life and reduce illness and disability. Moreover, the ability of photoacoustic imaging to provide high-resolution, real-time visualization of biological tissues is accelerating market expansion across pharmaceutical and research institutions. The photoacoustic imaging market statistics indicate a rising adoption of this technology for studying tumor microenvironments, vascular abnormalities, and treatment responses. The demand for photoacoustic imaging is expected to increase as researchers integrate photoacoustic imaging into precision medicine applications. Rising focus on technological advancements and increasing regulatory approvals for clinical adoption are generating investments in preclinical and clinical research. Thus, growing investments in preclinical and clinical research are expected to create the photoacoustic imaging market opportunities in the coming years.

Emerging Innovations in Optoacoustic Imaging

Various technologies will influence the optoacoustic imaging industry in the coming years. The latest advancements that include portable scanners, wearable imaging devices, multi-spectral imaging machines, artificial intelligence diagnostic software, and real-time three-dimensional imaging technology will play a significant role in making imaging more efficient and effective. Such advanced technologies will enable healthcare practitioners to obtain precise, reliable, and accurate diagnostic data from patients more quickly. Also, the expanding scope of application of such technologies across different branches of medicine, including oncology, cardiology, and dermatology, will drive industry development. Therefore, with continuous advancement in this area, optoacoustic imaging technology will eventually leave research labs and find its place in regular clinical procedures.

Source: Polaris Market Research Analysis

Segment Insights

Assessment by Product Outlook

The global photoacoustic imaging market segmentation, based on product, includes photoacoustic tomography (PAT) and photoacoustic microscopy (PAM). The photoacoustic tomography (PAT) segment accounted for the largest market share of 64.3% in 2025 due to its superior imaging depth and high-resolution capabilities, making it indispensable in clinical and preclinical applications. The increasing adoption of PAT in oncology, neurology, and vascular imaging is driving market expansion, as it enables noninvasive visualization of deep tissue structures with functional and molecular contrast. PAT’s integration with ultrasound further enhances its diagnostic potential. The growing emphasis on precision medicine and the rising need for real-time, high-contrast imaging solutions are key factors contributing to photoacoustic tomography dominant market value.

The photoacoustic microscopy (PAM) segment is expected to witness a higher CAGR during the forecast period due to its ability to deliver ultra-high resolution at the cellular and subcellular levels. The rising demand for detailed vascular and microcirculatory imaging, particularly in dermatology, ophthalmology, and neurovascular research, is fueling market growth. The increasing utilization of PAM in drug discovery and histopathological studies is further expanding the demand for PAM. Moreover, continuous advancements in laser technology and miniaturization of imaging systems are enhancing PAM’s accessibility and usability, strengthening its market forecast as a critical tool in biomedical research and diagnostics.

Evaluation by Application Outlook

The global photoacoustic imaging market segmentation, based on application, includes oncology, cardiology, angiology, histology, and interventional radiology. The oncology segment accounted for the largest market share of 44.3% in 2025 due to the rising prevalence of cancer and the urgent need for early, noninvasive tumor detection. Photoacoustic imaging provides superior soft tissue contrast and functional imaging capabilities, enabling real-time monitoring of tumor angiogenesis, hypoxia, and therapy response. The growing investments in cancer research, coupled with the increasing adoption of precision oncology solutions, are driving market expansion. The growing adoption of personalized treatment strategies is creating demand for advanced imaging modalities and enhancing its market value in oncology applications.

The cardiology segment is anticipated to register the highest CAGR of 12.6% over the forecast period due to the increasing incidence of cardiovascular diseases (CVDs) and the need for advanced imaging technologies to assess vascular health. Photoacoustic imaging enables high-resolution visualization of atherosclerotic plaques, microvascular changes, and myocardial tissue oxygenation, driving market demand for early diagnosis. Advancements in multimodal imaging integration, such as PAT-ultrasound hybrids, are enhancing diagnostic accuracy and expanding market opportunities. The rising focus on preventive cardiology and the growing adoption of non-ionizing imaging modalities are key factors accelerating the photoacoustic imaging market expansion for the cardiology segment.

Source: Polaris Market Research Analysis

Regional Analysis

By region, the study provides photoacoustic imaging market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America accounted for the largest market share of 39.5% in 2025 due to the region’s strong research infrastructure, high healthcare expenditure, and early adoption of advanced imaging technologies. The increasing prevalence of cancer and cardiovascular diseases, coupled with growing investments in biomedical research, is driving market expansion. Leading academic institutions and research centers in the US and Canada are actively integrating photoacoustic imaging for clinical and preclinical applications, further contributing to market growth. Additionally, the presence of key industry players and favorable regulatory frameworks supporting medical imaging innovation strengthen North America’s dominant position in the global market.

Asia Pacific is projected to register the highest CAGR of 12.5% over the forecast period due to rising healthcare investments, increasing government funding for medical research, and growing awareness of advanced diagnostic technologies. For instance, according to the World Health Organization, over 2.3 million people are diagnosed with cancer in Southeast Asia annually, with approximately 1.4 million deaths by cancer in the region. The region’s expanding biotechnology and pharmaceutical sectors, particularly in China, Japan, and India, are accelerating demand for noninvasive, high-resolution imaging solutions. Additionally, the rising burden of cancer and cardiovascular diseases, coupled with an increasing focus on early disease detection and personalized medicine, is driving market growth. Collaborations between research institutes and industry players, along with technological advancements, are further boosting the Asia Pacific market expansion.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The photoacoustic imaging market is characterized by intense competition, with key players focusing on strategic partnerships, collaborations, and mergers and acquisitions to strengthen their market position. Leading companies are investing in technological advancements to enhance imaging resolution, expand clinical applications, and integrate artificial intelligence for improved diagnostics. Academic and industry collaborations are driving innovation, particularly in preclinical and clinical research. Market participants are also expanding their geographic presence through joint ventures and distribution agreements to capitalize on growing demand in emerging economies. Furthermore, increased funding for biomedical research and precision medicine is prompting companies to develop next-generation imaging platforms, supporting the market’s growth trajectory and competitive intensity.

Fujifilm Corporation is involved in creating, selling, and distributing image, information, and document solutions. The company has established 280 regional management companies at major locations in the US, Europe, China, and Southeast Asia. It was founded in 1934 and is headquartered in Minato-ku, Tokyo. The three divisions through which the company functions are imaging solutions, information solutions, and document solutions. The Imaging solutions business unit deals with electronic imaging, photofinishing equipment, lab services, film processing, color films, color paper, and chemicals. The information solutions cover visual arts, recording media, and medical and life sciences systems. The document solutions division offers printers, office supplies, document creation, and outsourcing services. Fujifilm Corporation is actively engaged in the photoacoustic imaging market, leveraging its expertise in advanced imaging technologies to develop high-resolution, noninvasive diagnostic services for oncology and cardiovascular applications. The company focuses on technological innovation and strategic collaborations to enhance the adoption of photoacoustic imaging in clinical and research settings.

Advantest Corporation, is a major manufacturer of automatic test equipment (ATE) for the semiconductor industry. The company initially began as Takeda Riken Industry Co., Ltd., focusing on electronic measuring instruments before entering the semiconductor testing business in 1972. The company operates through three primary business segments: Semiconductor and Component Test Systems, Mechatronics Systems, and Services, Support, and Others. The semiconductor and component test systems segment includes various test solutions such as SoC test systems, memory test systems, and burn-in test systems. Advantest's global footprint is extensive, with operations in 18 countries and subsidiaries strategically located across North America, Europe, and Asia. Advantest Corporation is a key player in the photoacoustic imaging market, specializing in high-precision diagnostic and analytical imaging solutions.

List of Key Companies

- Advantest Corporation

- Calpact

- Cyberdyne, Inc.

- Fujifilm Holdings Corporation

- Illumisonics Inc.

- Innolas Laser GmbH

- iThera Medical GmbH

- Kibero

- Luxonus Inc.

- Opotek Llc

- Photosound Technologies, Inc.

- Seno Medical

- Tomowave Laboratories, Inc.

- Verasonics, Inc.

- Vibronix, Inc.

Industry Developments

- January 2026: Seno Medical received European Union Medical Device Regulation (EU MDR) CE Mark certification for its next-generation Imagio Breast Imaging System (Model 9100). The company stated that the regulatory milestone will enable it to market the technology to clinicians across the E.U. (source: senomedical.com)

- January 2026: Researchers at the Keck School of Medicine of USC and Caltech unveiled a 3D dual-imaging system called RUS-PAT. The technology combines photoacoustic imaging and ultrasound to simultaneously capture images of both blood vessels and tissues. (source: keck.usc.edu)

- November 2024: Seno Medical received an innovative technology contract from Vizient for its Imagio Breast Imaging System, which combines opto-acoustic and ultrasound imaging to enhance breast cancer diagnostics. (Source: radiologybusiness.com)

Market Segmentation

By Product Outlook (Revenue – USD Million, 2021–2034)

- Photoacoustic Tomography (PAT)

- Photoacoustic Microscopy (PAM)

By Imaging Type Outlook (Revenue – USD Million, 2021–2034)

- Pre-Clinical

- Clinical

By Application Outlook (Revenue – USD Million, 2021–2034)

- Oncology

- Cardiology

- Angiology

- Histology

- Interventional Radiology

By Regional Outlook (Revenue – USD Million, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 131.04 Million |

| Market Size Value in 2026 | USD 146.29 Million |

| Revenue Forecast in 2034 | USD 363.37 Million |

| CAGR | 12.0% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Million, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

photoacoustic imaging market FAQ's

The global market size was valued at USD 131.04 million in 2025 and is projected to grow to USD 363.37 million by 2034.

The global market is projected to register a CAGR of 12.0% during the forecast period.

North America accounted for the largest market share of 39.5% in 2025 due to the region’s strong research infrastructure, high healthcare expenditure, and early adoption of advanced imaging technologies.

A few of the key players in the market are Advantest Corporation; Calpact; Cyberdyne, Inc.; Fujifilm Holdings Corporation; Illumisonics Inc.; Innolas Laser GmbH; iThera Medical GmbH; Kibero; Luxonus Inc.; Opotek LLC; Photosound Technologies, Inc.; Seno Medical; Tomowave Laboratories, Inc.; Verasonics, Inc.; and Vibronix, Inc.

The photoacoustic tomography (PAT) segment accounted for the largest market share of 64.3% in 2025 due to its superior imaging depth and high-resolution capabilities.

The oncology segment accounted for the largest market share of 44.3% in 2025 due to the rising prevalence of cancer and the urgent need for early, noninvasive tumor detection.

Download Sample Report of photoacoustic imaging market

Please fill out the form to request a customized copy of the research report.