Polyolefins Market Research Report, Size, Share & Forecast by 2026 - 2034

REPORT DETAILS

Polyolefins Market Overview

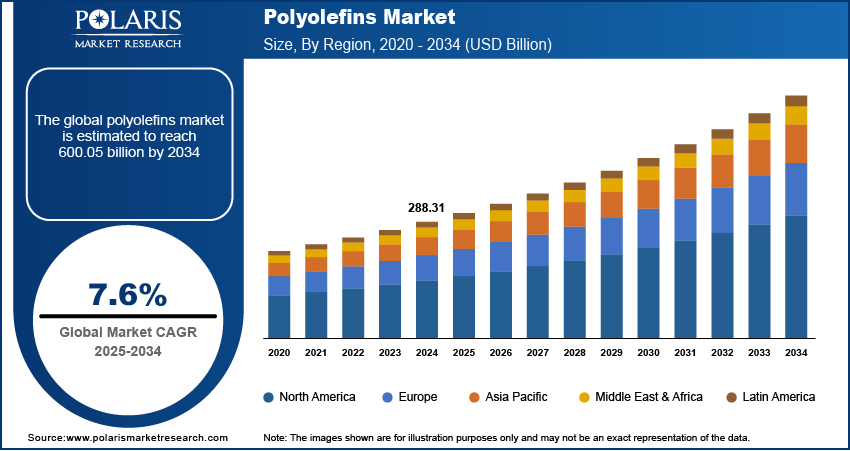

The global polyolefins market size was valued at USD 308.64 billion in 2025, growing at a CAGR of 7.5% from 2026 to 2034. The market demand is primarily driven by the booming solar power industry and the implementation of favorable policies and regulations related to waste disposal.

Market Statistics

Key Takeaways

- Asia Pacific held the largest share of 49.81% in 2025, driven by fast industrial growth and growing end-use industries.

- North America is projected to grow at a CAGR of 8.2%, owing to higher demand from the packaging and pharmaceutical industries.

- The United States dominated the NA market with around 73% share, by its strong packaging industry and advanced manufacturing base

- The polyethylene segment led the market in 2025 with around 50.65% share. Mainly because it was strong, flexible, and can handle impacts, which made it a popular choice for both packaging and industrial uses.

- The film & sheet segment accounted for 25.51% share in 2025. This was because packaging, agriculture, and construction all wanted it owing to its light, strong, and cheap.

*Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

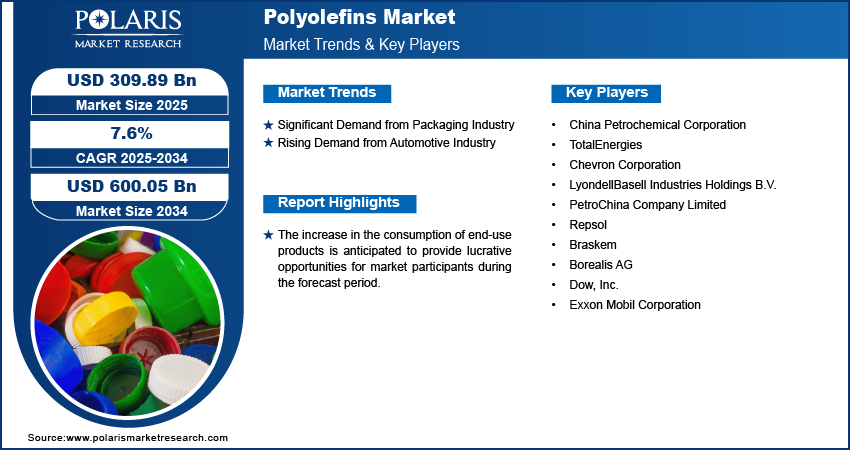

- The significant demand for polyolefins for the production of packaging products such as bags, films, and containers contributes to the market growth.

- The rising adoption of polyolefins in the automotive industry, owing to their desirable characteristics, contributes to market expansion.

- The increasing consumption of end-use products is projected to provide several market opportunities in the coming years.

- Fluctuating raw material costs may present challenges to market growth.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Polyolefins Market Definition

Polyolefins are a group of thermoplastics made from polymers of olefins, such as propylene and ethylene. They are among the most widely used synthetic polymers for manufacturing a variety of end-use products. Polyolefins are favored for a wide range of applications due to their favorable properties, such as lightweight and high chemical resistance, along with their lost cost of production.

Several factors, including the development of the solar power industry and rising demand from the packaging sector in major economies, are driving the polyolefins market development. The implementation of favorable policies and regulations related to packaging and waste disposal is further encouraging the use of high-quality and innovative polyolefins for labeling and packaging products, thereby supporting market growth.

Leading market participants are constantly upgrading their product portfolios to meet the growing demand from various application sectors, such as film and sheet production and injection molding, which is anticipated to support polyolefins market expansion in the coming years. The increase in the consumption of end-use products, such as flexible packaging and bio-based products, is anticipated to provide lucrative market opportunities during the forecast period.

Polyethylene vs Polypropylene

| Factor | Polyethylene (PE) | Polypropylene (PP) |

| Structure and Flexibility | Soft and extremely flexible material | Harder and stronger material |

| Resistance to Heat | Less resistant to heat | More resistant to heat and temperature variations |

| Strength | Reasonable strength and ideal for light applications | Greater strength and enhanced durability |

| Usage | Films for wrapping, plastic bags, bottles, and boxes | Used in automotive parts, reusable containers, medical equipment |

| Price | Typically cheaper and extensively used for bulk packaging | More expensive because of improved properties |

| Main Advantage | Best moisture barrier and flexibility | Extremely strong and heat resistant |

Source: Polaris Market Research Analysis

Market Dynamics

Significant Demand from Packaging Industry

Polyolefins, composed of polypropylene and polyethylene, are widely used for producing different packaging products such as containers, films, and bags due to their durability, lightweight, and cost-effectiveness. With the growth of e-commerce, there has been a surge in the need for packaging materials that are flexible and strong, making polyolefins an ideal choice. The increase in demand for innovative packaging materials such as polyolefins from the packaging industry drives the polyolefins market growth.

Rising Demand from Automotive Industry

Polyolefins are gaining popularity in the automotive industry owing to their favorable properties. They are lighter than other materials such as metal and rubber, which helps manufacturers reduce vehicle weight and improve fuel efficiency. Also, polyolefins are cost-effective to manufacture and can improve the comfort and safety of a vehicle. They are used in several vehicle parts, including the engine section, bodywork, and exterior and interior components. The rising applications of polyolefins in the automotive sector are a major polyolefins market revenue contributor.

Technological Advancements in Polyolefin Production

Advances in polyolefin manufacturing technologies have resulted in improvements in efficiency and sustainability in the polyolefin industry. Metallocene catalysis technology allows better control of polymer structure, producing higher-strength, high-transparency, and flexible polyethylene and polypropylene. New blending techniques are helping produce specialized material grades for applications such as packaging, automotive, and industrial. Bio-based polyolefins have minimized environmental impacts in recent times. Moreover, advances in automation and digitization have resulted in increased efficiency in production processes

Source: Polaris Market Research Analysis

Sustainable and Recyclable Polyolefin Materials

Recyclable and sustainable polyolefins are gaining importance as various industrial sectors work to minimize plastic waste and improve environmental performance. There is a move towards producing recyclable polyethylene and polypropylene grades that will have long-lasting usability without any major quality degradation. Bio-based polyolefin materials manufactured from renewable sources are also being produced as alternatives to traditional fossil polyolefin materials. The recycling of used polyolefins via improved mechanical and chemical processes will also contribute significantly towards the reuse of such plastic materials. These trends are playing an important role in shaping the future prospects of the polyolefin industry.

Segment Insights

Market Outlook by Feedstock Insights

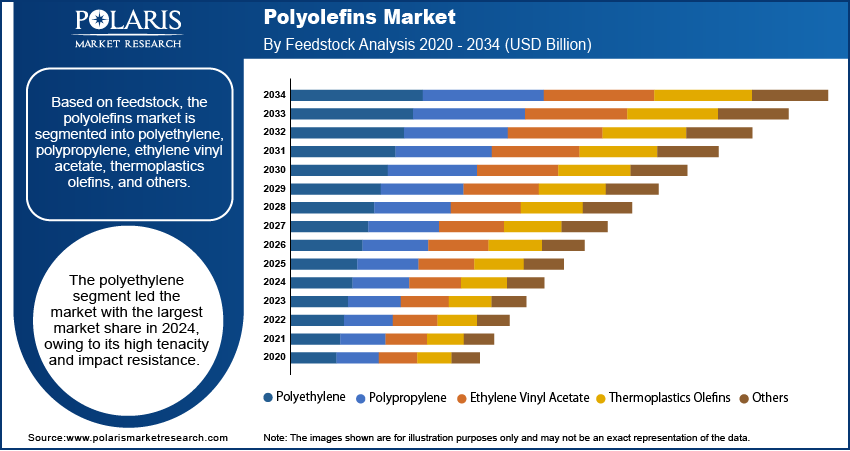

The polyolefins market, based on feedstock, is segmented into polyethylene, polypropylene, ethylene vinyl acetate, thermoplastics olefins, and others. The polyethylene segment led the market with the largest market share of 50.65% in 2025. Its high tenacity and impact resistance contribute to its strong market appeal. Products made from polyethylene have gained popularity, particularly among the middle-class population, driven by urbanization, rising disposable incomes, and significant advancements in material science. The segment’s robust growth is further supported by the strategic efforts of many market players and their well-established networks.

The polypropylene segment accounted for a significant market revenue share of 31.0% in 2025. Polypropylene has high tensile strength, making it strong enough to handle heavy loads. Also, it is resistant to fatigue, has excellent chemical resistance, and can withstand extreme temperatures and freezing. The ability to mold polyolefins into various shapes means it can easily produced in a living hinge, which is a thin piece of material that can be bent without breaking. Thus, the durability and versatility of polypropylene contribute to its high share in the market.

Market Assessment by Application Insights

The polyolefins market, based on application, is segmented into films and sheets, injection molding, blow molding, extrusion coating, fiber, and others. The films and sheets segment accounted for the largest polyolefins market share of 28.1% in 2025. Films and sheets made using polyolefins provide improved clarity and performance for the consumer goods industry. Also, they have stronger puncture resistance and are more durable than films and sheets made from other materials. Thus, the various benefits of polyolefin films and sheets contribute to their dominance in the market.

The injection molding segment is projected to witness significant growth from 2026 to 2034, owing to its ability to produce custom polyolefin materials. The rising demand for polyolefin injection molding from various end-use sectors such as automotive, healthcare, and packaging is also contributing to the robust growth of the segment. Growing awareness about the benefits of polyolefin injection molding among manufacturers is expected to further drive the segment’s growth in the global market.

Source: Polaris Market Research Analysis

Regional Analysis

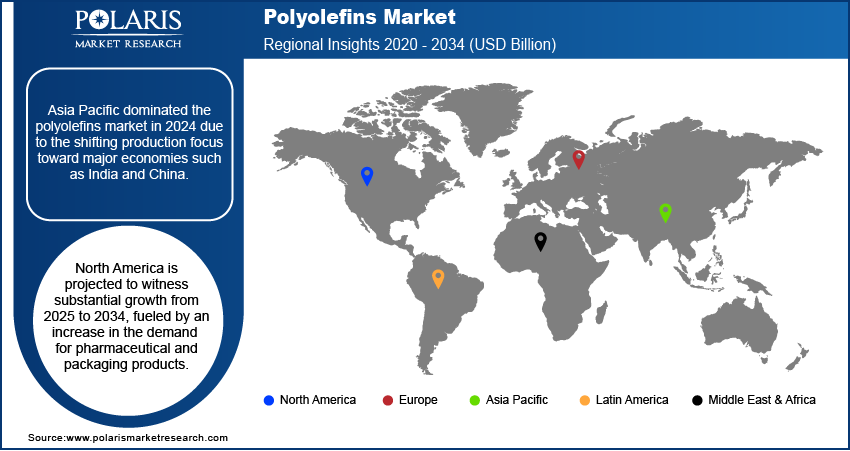

By region, the market report offers polyolefins market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific dominated the market with a revenue share of 49.81% in 2025. The region is known for its easily accessible land and the availability of skilled labor at low costs. The shifting production focus toward major economies such as India and China drives regional market dominance. Further, the presence of rapidly growing industries, such as electronics and telecommunications, provides significant potential for polyolefin manufacturers in the region.

The polyolefins market in North America is projected to witness substantial growth from 2026 to 2034. The US plays a significant role by holding the largest share of the regional market. The North America polyolefins market is distinguished by an increase in the demand for pharmaceutical and packaging products, which is expected to drive the requirement for polyolefins in the region during the forecast period.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

The polyolefins market is characterized by intense competition, driven by factors such as innovative product offerings, technological advancements, mergers and acquisitions, and other strategic partnerships. The key players in the market strive to differentiate themselves in terms of pricing, quality, offering, and customer service. Also, they make significant investments in R&D initiatives to introduce advanced polyolefins to cater to diverse consumer needs.

Several market participants are prioritizing the development of sustainable and eco-friendly polyolefins that comply with stringent government regulations. The polyolefins market research report offers a market assessment of all the leading players, including China Petrochemical Corporation; TotalEnergies; Chevron Corporation; LyondellBasell Industries Holdings B.V.; PetroChina Company Limited; Repsol; Braskem; Borealis AG; Dow, Inc.; and Exxon Mobil Corporation.

List of Key Companies

- China Petrochemical Corporation

- TotalEnergies

- Chevron Corporation

- LyondellBasell Industries Holdings B.V.

- PetroChina Company Limited

- Repsol

- Braskem

- Borealis AG

- Dow, Inc.

- Exxon Mobil Corporation

Polyolefins Industry Developments

March 2026: OMV Aktiengesellschaft (OMV) and XRG announced the successful formation of Borouge Group International AG. According to OMV, the strategic move will create a world-scale polyolefins leader with differentiated technology. (source: omv.com)

October 2025: GCR launched CICLICNXT, a fresh range of post-consumer recycled (PCR) polyolefins. These are engineered to offer performance comparable to virgin materials, but at an industrial scale. This advancement simplifies the adoption of sustainable plastics in significant applications, including packaging, construction, and consumer goods. (Source: recyclingtoday.com)

December 2025: Borealis and Borouge launched Recleo, a global brand for mechanically recycled polyolefins. It combines materials from both consumers and businesses into one portfolio. This program makes it easier to find eco-friendly plastics and helps the goals of the circular economy. (Source: borealisgroup.com)

Polyolefins Market Segmentation

By Feedstock Outlook

- Polyethylene

- Polypropylene

- Ethylene Vinyl Acetate

- Thermoplastics Olefins

- Others

By Application Outlook

- Films and Sheets

- Injection Molding

- Blow Molding

- Extrusion Coating

- Fiber

- Others

By Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Polyolefins Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 308.64 billion |

| Market Size Value in 2026 | USD 330.67 billion |

| Revenue Forecast by 2034 | USD 591.72 billion |

| CAGR | 7.5% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Polyolefins Market FAQ's

The market was valued at USD 308.64 billion in 2025 and is projected to grow to USD 591.72 billion by 2034.

The market is projected to register a CAGR of 7.5% from 2026 to 2034.

Asia Pacific accounted for the largest region-wise market share of 49.81% in 2025.

A few of the key players in the market are China Petrochemical Corporation; TotalEnergies; Chevron Corporation; LyondellBasell Industries Holdings B.V.; PetroChina Company Limited; Repsol; Braskem; Borealis AG; Dow, Inc.; and Exxon Mobil Corporation.

The polyethylene segment accounted for the largest market share of 50.65% in 2025.

The films and sheets segment accounted for the largest polyolefins market share of 25.51% in 2025.

Download Sample Report of Polyolefins Market

Please fill out the form to request a customized copy of the research report.