Polypropylene Market Size, Demand, Global Analysis Report, 2026-2034

REPORT DETAILS

What is Polypropylene Market Size?

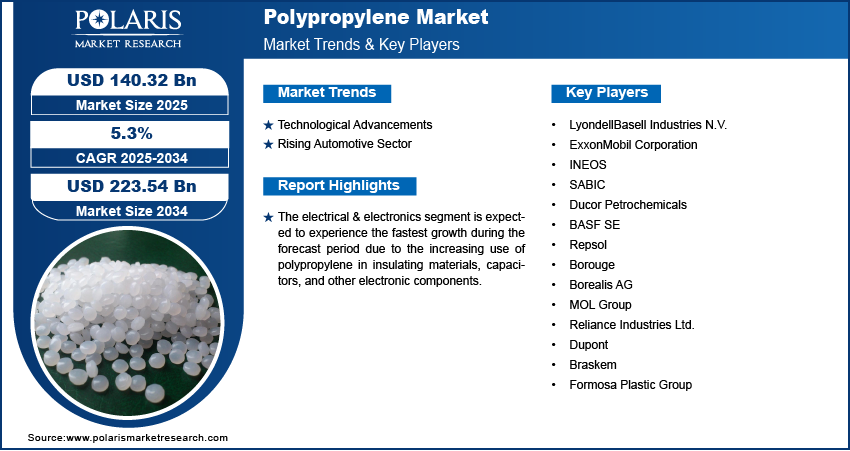

The global polypropylene (PP) market size was valued at USD 137.14 billion in 2025, growing at a CAGR of 6.22% from 2026–2034. The wide usage of polypropylene in several end use applications, such as medical, electronics, and automobiles, is propelling the industry growth. As per our polypropylene industry analysis, the rising demand for lightweight materials across packaging sector is expected to drive the adoption of polypropylene in the coming years.

Market Statistics

Key Takeaways

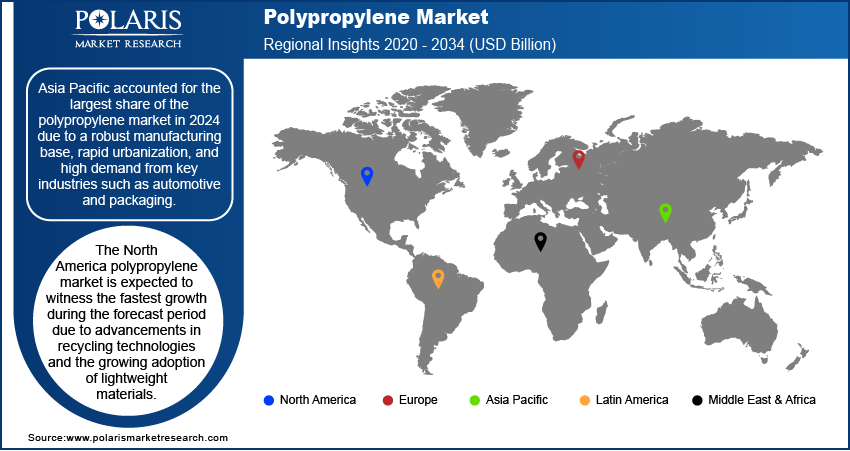

- The Asia Pacific polypropylene market held the largest revenue share of 36.40% in 2025. The region’s strong manufacturing growth; elevated demand from several critical industries such as automotive, packaging, and construction; and notable funding in infrastructure advancements fueled the regional market dominance.

- The North America polypropylene industry is anticipated to witness significant growth rate of CAGR 5.9% during the forecast period. Growing demand from the automotive and packaging industries and rising acquisition of lightweight and eco-friendly materials will drive the growth

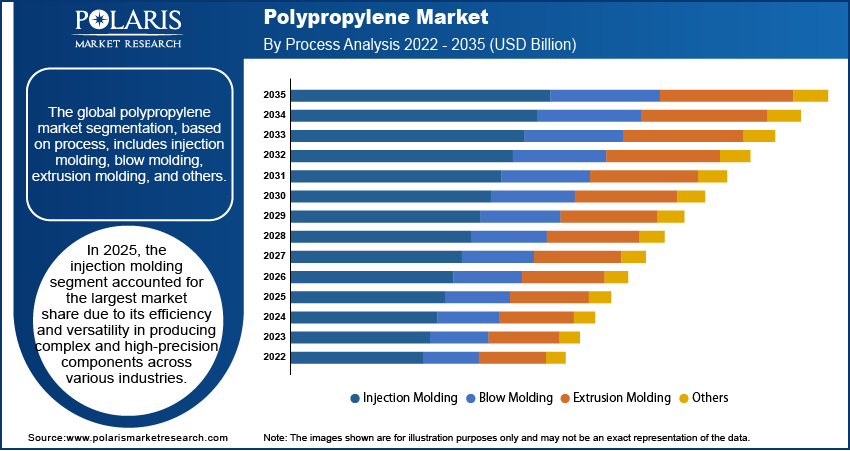

- Based on our polypropylene market segment, by process type, the injection molding segment dominated the market share by holding ~45.8% of the total revenue in 2025.

- The electrical & electronics segment, by end user, is anticipated to experience the fastest growth rate of CAGR 7.1% during the forecast period. The growing usage of polypropylene in insulating substances, ultracapacitors, and other electronic components will boost segment growth.

Industry Dynamics

- One of the noteworthy polypropylene industry trends is the rising acquisition of bio-based polymers and recyclable polypropylene. Rising shift toward green and environmentally friendly solutions will drive the PP demand.

- The automotive sector increasingly prefers lightweight components to enhance fuel efficiency and decrease carbon emissions. Therefore, the PP demand is rising across the sector to meet sustainability goals.

- The growing demand for lightweight plastic packaging in the electronics and consumer goods industries is expected to boost the PP adoption.

- The uncertainty in supply and cost of crude oil, due to fluctuating political scenarios in the Middle East and in other oil-generating nations, hinders the market growth.

Source: Polaris Market Research Analysis Market.png)

To Understand More About this Research:Download Sample Report

What is Polypropylene?

Polypropylene is a thermoplastic polymer belonging to the polyolefin family. It is known for its balanced combination of lightweight structure and chemical resistance. It exhibits a relatively high melting point along with low density. These features support its use in varied operating conditions. The material does not absorb moisture and shows strong resistance to corrosion, allowing it to perform reliably in chemically aggressive environments. Because of these properties, polypropylene is used across sectors such as medical, construction, electronics, packaging, automotive, and consumer goods.

Types of Polypropylene

Polypropylene is mainly available in two types: homopolymer and copolymer. Each type is designed for different performance needs.

- Homopolymer polypropylene is the most widely used type. It provides high strength, stiffness, and good chemical resistance. This material is commonly used in applications including packaging, textiles, and medical components where rigidity is important.

- Copolymer polypropylene is produced by combining propylene with small amounts of other monomers, typically ethylene. This improves impact resistance and increases flexibility. It is further divided into random and block copolymers and is widely used in automotive parts, containers, and products that require durability under stress.

Key Application Areas of Polypropylene

| Application | Use Cases | Benefits |

| Packaging | Food containers, bottles, films, pouches, caps, and rigid packaging | Moisture resistance and lightweight |

| Automotive | Bumpers, interior trims, battery cases, dashboards, and under-the-hood components | Durability and chemical resistance |

| Textiles (Non-woven & Woven) | Carpets, ropes, upholstery, bags, and geotextiles | High tensile strength and low cost |

| Consumer Goods | Appliances, household items, furniture, toys, and storage containers | Versatility and moldability |

| Medical Applications | Syringes, medical vials, disposable items, and laboratory equipment | Sterilization compatibility |

| Electronics | Insulation, capacitors, housings, and cable jackets | Excellent dielectric properties |

| Construction | Pipes, sheets, insulation panels, and fittings | Corrosion resistance and durability |

| Industrial Applications | Tanks, sheets, liners, fibers, and machine parts | Chemical resistance and mechanical performance |

Source: Polaris Market Research Analysis

What is Driving Global Polypropylene Demand?

According our polypropylene industry analysis, the increasing preference for effective plastic packaging propels the demand for polypropylene. Its lightweight and low density make it an efficient material for handling and transportation. Its high tensile strength enables it to withstand heavy loads without failure. Further, its impact resistance and high melting point make it suitable for high-temperature applications. All these benefits are contributing to its widespread adoption. Furthermore, techniques such as injection molding, extrusion, and blow molding are used to ease PP processing. Such processes underscore its versatility across industries, including automotive, electronics, construction, packaging, and consumer goods.

Polypropylene Vs. Other Plastics

Industrial buyers consider PP as the most balanced material due to its benefits such as cost efficiency, processability, recyclability, heat resistance, and design versatility. PE is a dominating material in films and flexible packaging. PVC is mainly used in construction. PS is increasingly used for low-cost rigid packaging. According to our polypropylene demand analysis, PP has experienced significant demand in B2B applications due to its multifunctionality.

| Attribute | Polypropylene (PP) | Polyethylene (PE: HDPE/LDPE) | Polyvinyl Chloride (PVC) | Polystyrene (PS) |

| Material Cost | Low cost; excellent value per kg due to its low density | Cheapest material for films and bags | Moderate cost. Additives increase cost. | Low cost, moderate but limited usability |

| Density/Lightweighting | Lowest density: more parts per kg | Low density, but slightly higher than PP | Heaviest density | Moderate density. Heavier than PP/PE |

| Heat Resistance | High (~160–170°C). Hot-fill and auto parts | Low–moderate (110–135°C). Softens early | Moderate but limited by chlorine content | Low. Softens & deforms easily |

| Chemical Resistance | Excellent vs acids, bases, and oils | Excellent overall | Good vs acids | Poor; dissolves in various solvents |

| Recyclability/Circularity | Strong. PP monomaterial recycling is expanding globally | Strong. PE has large recycling streams | Weak. Additives complicate recycling | Weak. Brittle and low-value recyclate |

| Regulatory & Food-Grade Compliance | Very strong. Widely approved for food/medical | Strong for food contact | Moderate. Concerns due to chlorine and additives | Weak. Styrene monomer concerns |

| Equipment Compatibility | Noncorrosive and low wear on tooling | Noncorrosive and easier on equipment | Corrosive (HCl release).Needs special tooling | Noncorrosive |

| Industry Applications | Packaging, automotive (mostly EVs), FMCG, appliances, medical, and nonwovens | Films, bags, containers, and pipes (HDPE) | Construction, pipes, wire/cable, and medical | Disposable packaging, insulation, and rigid boxes |

| Key Benefits | Low cost, high performance, and excellent processability | Very cheap and highly versatile for films | Rigid and durable for construction | Good clarity, but brittle and limited |

Source: Polaris Market Research Analysis

Polypropylene Market Dynamics

Drivers

Growing Automotive Sector

The automotive sector increasingly uses polypropylene as lightweight properties of the polymer help improve fuel efficiency and reduce carbon emissions. It aligns with industry trends toward sustainability. According to the Alliance for Automotive Innovation, the automotive ecosystem contributes over USD 1 trillion to the U.S. economy each year, representing around 4.9% of GDP. The increasing adoption of electric vehicles has boosted the expansion of the sector. In EVs, polypropylene is used in battery housings and interiors. Hence, the expanding automotive sector drives the polypropylene market demand.

Increasing Adoption in Packaging Industry

The packaging industry increasingly uses polypropylene due to its excellent balance of performance, sustainability, and cost. High clarity, durability, and moisture resistance propel its preference across FMCG and food and beverage packaging. In addition, its high compatibility with advanced processing methods such as thermoforming, injection molding, and film extrusion boosts the PP adoption. Regulatory pressures for sustainable practices are driving the bio-based polypropylene market growth. PP is suitable for rigid containers, caps and closures, flexible films, food-grade packaging, and e-commerce protective solutions. It is a strategic material for FMCG, food & beverage, healthcare, and industrial packaging sectors.

Opportunity

Rising Demand for Sustainable and Eco-Friendly Materials

The rising adoption of bio-based polymers and recyclable polypropylene will create lucrative opportunities for PP players. Industries move toward sustainable and eco-friendly solutions. In September 2024, Braskem America launched a Bio-Circular Polypropylene (PP). It is designed to meet the sustainability challenges faced by the restaurant and snack food sectors. This material leverages renewable feedstocks and incorporates advanced recycling processes. It reduces the carbon footprint associated with traditional polypropylene production. This shift, aligned with global environmental regulations and corporate sustainability goals, boosts the polypropylene sustainability trends. Therefore, technological advancements and increasing demand for sustainable materials propel the the polypropylene recycling market.

Challenges

Inconsistency in Feedstock Pricing and Supply and Plastic Bans

Volatility in polypropylene feedstock pricing is driven by fluctuations in refinery output. Also, global supply chain disruptions due to trade tariffs, primarily across Europe & Asia, and freight inflation restrain the supply of polypropylene. Furthermore, governments in many countries are increasingly imposing regulations on the use of single-use plastics. Such a regulatory landscape prompts industry players to shift toward recycling and alternative PP solutions. Thus, supply chain vulnerabilities and sustainability initiatives can impact the polypropylene price trends.

Source: Polaris Market Research Analysis

Segment Insights

By Polymer Type

Based on polymer type, the market is segmented into homopolymer and copolymer. The homopolymer segment accounted for a larger polypropylene market share of ~78% in 2025. The growth of the homopolymer polypropylene market is attributed to its widespread use in packaging. Polypropylene produced by using a single monomer type is known as a homopolymer. Homopolymer is widely used across a few end users, such as medical, automotive, electrical, building and construction, and packaging. The copolymers segment is expected to witness significant growth during the forecast period. Copolymers are produced by using more than one monomer type. Random copolymers and block copolymers are two types of copolymers. Rapid urbanization, penetration of e-commerce, and growing preference for recyclable materials across consumer goods and industrial applications boost the copolymer polypropylene market demand.

Comparison Between PP-H, Random PP-C, and Impact PP-C

| Attribute | Homopolymer (PP-H) (Largest Shareholder) | Copolymer PP-C | |

| Random Copolymer PP-C (R-PP) | Impact Copolymer PP-C (I-PP) | ||

| Composition | 100% Propylene | Propylene + small percentage of ethylene (randomly distributed) | Propylene + high percentage of ethylene (block structure) |

| Stiffness / Rigidity | High | Medium | Low–Medium |

| Transparency | Opaque | Highest clarity and good optical properties | Opaque |

| Melting Point | 160–165°C | 140–150°C | 150–160°C |

| Flexibility | Low | Medium | High |

| Stress Crack Resistance | Moderate | Good | Very Good |

| Processing Characteristics | Fast cycle times and easy molding | Easy flow and good for thin walls | Requires slightly higher processing control |

| Cost | Lowest | Medium | Medium to high |

| Typical Applications | Rigid packaging, pipes, closures, and industrial components | Transparent packaging, housewares, medical syringes, and food containers | Automotive bumpers, battery housings, appliances, dashboards, and crates |

| Advantages | Cost efficiency and stiffness | Aesthetics and clarity | Durability, impact resistance, and long-life components |

Source: Polaris Market Research Analysis

By Process Outlook

The global PP industry, based on process, is segmented into injection molding, blow molding, extrusion molding, and others. In 2025, the injection molding segment accounted for the largest share, at ~45.8%. Its efficiency and versatility in producing complex and high-precision components across various industries propel dominance. Injection molding is a widely adopted manufacturing process that enables the mass production of polypropylene products with consistent quality, contributing to its dominance. This process is particularly advantageous for applications requiring difficult designs, such as automotive parts, consumer goods, and medical devices, where precision and durability are critical. Additionally, the cost-effectiveness and scalability of injection molding make it a preferred choice for manufacturers seeking to optimize production while meeting the growing demand for polypropylene products. The ability to produce lightweight, durable, and customizable components through injection molding has further strengthened its market share, driving its dominance in the polypropylene market.

By End User Outlook

The global PP market segmentation, based on end user, includes automotive, building & construction, packaging, medical, electrical & electronics, consumer goods/lifestyle, agriculture, and others. The electrical & electronics segment is expected to experience the fastest growth during the forecast period. The increasing use of polypropylene in insulating materials, ultracapacitors, and other electronic components boost the segment growth. Its excellent electrical insulating properties and thermal resistance make it ideal to ensure safety and efficiency in electronic applications. The rising demand for consumer electronics and advancements in renewable energy technologies fuel the PP adoption. The proliferation of electric vehicles is further driving the demand for polypropylene in this segment.

Source: Polaris Market Research Analysis

Regional Analysis

By region, the study provides the polypropylene market growth trends insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2025, Asia Pacific accounted for the largest revenue share of 36.4%. The region's robust manufacturing base; high demand from various key industries such as automotive, packaging, and construction; and significant investments in infrastructure development drove the Asia Pacific polypropylene market growth. According to the International Trade Administration, India is the third-largest automotive market in the world, following China and the U.S.. In the fiscal year 2023, the industry produced around 26 million vehicles across various segments, including passenger and commercial vehicles, as well as two and three-wheelers. The automotive sector contributes 49% to India's manufacturing GDP and 7% to the national GDP. The automotive sector is one of the largest end users of polypropylene. Thus, the growing vehicle production across the country propelled the India polypropylene investments. Further, rising China polypropylene consumption is attributed to the increasing population and urbanization in the country.

The North America polypropylene market is expected to witness the fastest growth during the forecast period due to increasing demand from the automotive and packaging industries, advancements in recycling technologies, and the growing adoption of lightweight and sustainable materials. Government initiatives promoting eco-friendly practices and significant investments in research and development drive market expansion. In November 2024, the Biden-Harris Administration launched a national strategy to tackle plastic pollution. It aims to drive domestic and international efforts to protect communities affected by plastic pollution. The rising use of PP in healthcare and consumer goods applications fuels the regional industry expansion.

Source: Polaris Market Research Analysis

Import and Export Analysis

Top Five Importers and Exporters of Polypropylene (in Primary Forms) in 2024

| Rank | Importers | Exporters | ||||

| Country | Trade Value (1000USD) | Quantity (kg) | Country | Trade Value (1000USD) | Quantity (kg) | |

| 1 | China | 2,428,938.41 | 2,356,110,000 | Saudi Arabia | 4,670,520.52 | 4,257,880,000 |

| 2 | Turkey | 2,259,582.08 | 1,921,690,000 | China | 2,294,742.17 |

|

| 3 | European Union | 1,815,377.44 | Korea, Rep. | 2,119,237.37 | 1,918,050,000 | |

| 4 | Germany | 1,369,869.93 | 903,315,000 | United States | 1,931,114.94 |

|

| 5 | Italy | 1,323,634.11 | 1,036,810,000 | Germany | 1,321,946.20 | 921,781,000 |

Source: Polaris Market Research Analysis

Source: World Integrated Trade Solution (WITS)

China is the major importer of polypropylene in primary forms. It imports PP from countries such as Korea, Rep., the UAE, Other Asia, nes, Singapore, and Japan. However, Saudi Arabia, being a major exporter, exported a significant quantity of PP to Turkey, Egypt, Arab Rep., India, Algeria, and Pakistan.

Key Players and Competitive Analysis

The presence of numerous key players and continuous innovations characterizes the competitive landscape. Leading PP manufacturers focus on strategic initiatives such as mergers and acquisitions, partnerships, and joint ventures. These strategies help them expand their global reach. They are heavily investing in research and development to develop bio-based polypropylene alternatives. Moreover, advancements in new polypropylene production technology and the expansion of production capacities enable companies to meet the increasing PP demand. Key players leverage digitalization and process optimization to reduce costs and improve supply chain efficiency.

Prominent companies such as LyondellBasell Industries, SABIC, ExxonMobil, Borealis AG, and TotalEnergies SE dominate the PP industry, with a strong presence in major regions. These companies are catering to the automotive, packaging, construction, and consumer goods industries. They ensure their products align with evolving customer needs and regulatory requirements. This competitive environment shapes the market outlook.

A few polypropylene market key players are LyondellBasell Industries N.V., ExxonMobil Corporation, INEOS, SABIC, Ducor Petrochemicals, BASF SE, Repsol, Borouge, Borealis AG, MOL Group, Reliance Industries Ltd., Dupont, Braskem, and Formosa Plastic Group.

List of Key Companies

- LyondellBasell Industries N.V.

- ExxonMobil Corporation

- INEOS

- SABIC

- Ducor Petrochemicals

- BASF SE

- Repsol

- Borouge

- Borealis AG

- MOL Group

- Reliance Industries Ltd.

- Dupont

- Braskem

- Formosa Plastic Group

Polypropylene Industry Developments

In May 2025, Borealis announced an investment of over EUR 100 million or USD 117.91 Million in a new production line for High Melt Strength Polypropylene (HMS PP) at Burghausen, Germany site (Source: Borealisgroup.com)

In August 2025, Lummus Technology announced that Vioneo selected it as the polypropylene technology partner for the world’s first industrial-scale facility producing fossil-free plastics from green methanol. Leveraging Lummus’ Novolen polypropylene technology, the project converts green methanol into sustainable polypropylene, representing a breakthrough in decarbonizing the plastics industry. (Source:lummustechnology.com)

In August 2025, ABB partnered with Citroniq to develop the world’s first full commercial-scale facility producing 100% bio-based polypropylene in Nebraska, USA. Using corn-based ethanol feedstock, the plant aims to cut greenhouse gas emissions and strengthen domestic supply chains. ABB will provide advanced automation, electrification, and digitalization technologies to ensure efficient operations, while the project is set to create skilled jobs and support U.S. manufacturing, marking a significant step in sustainable plastics innovation. (Source: New.abb.com )

In March 2025, LyondellBasell announced an investment to expand its polypropylene production. The investment is directed at its Channelview Complex near Houston. The company stated that the production capacity of the unit will be around 400 thousand metric tons. (Source: investors.lyondellbasell.com)

Polypropylene Market Segmentation

By Polymer Type Outlook (Volume, Kilotons; Revenue, USD Billion, 2021–2034)

- Homopolymer

- Copolymer

By Process Outlook (Volume, Kilotons; Revenue, USD Billion, 2021–2034)

- Injection Molding

- Blow Molding

- Extrusion Molding

- Others

By Application Outlook (Volume, Kilotons; Revenue, USD Billion, 2021–2034)

- Fiber

- Film & Sheet

- Raffia

- Others

By End User Outlook (Volume, Kilotons; Revenue, USD Billion, 2021–2034)

- Automotive

- Building & Construction

- Packaging

- Medical

- Electrical & Electronics

- Consumer Goods/Lifestyle

- Agriculture

- Others

By Regional Outlook (Volume, Kilotons; Revenue, USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Polypropylene Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 137.14 Billion |

| Market Size Value in 2026 | USD 143.40 Billion |

| Revenue Forecast by 2034 | USD 246.77 Billion |

| CAGR | 6.22% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, Volume in Kilotons; 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Polypropylene Market FAQ's

The market was valued at USD 137.14 billion in 2025 and is projected to reach USD 246.77 billion by 2034. It is expected to register a CAGR of 6.22% during 2025-2034. Rising PP demand from the automotive and packaging industries will fuel the market growth.

Asia Pacific held the largest share of 36.4% in 2025. The dominance is attributed to robust manufacturing infrastructure and significant production in China and India.

Polypropylene (PP) is primarily used in injection molding, packaging, automotive components, construction materials, and electronics. Its lightweight properties, chemical resistance, durability, and cost-effectiveness propel the PP demand across end-use industries.

LyondellBasell Industries N.V., ExxonMobil Corporation, INEOS, SABIC, Ducor Petrochemicals, BASF SE, Repsol, Borouge, Borealis AG, MOL Group, Reliance Industries Ltd., Dupont, Braskem, and Formosa Plastic Group are major market players.

A few key trends in the market are the rising adoption of bio-based and recyclable polypropylene and the increasing emphasis on sustainable packaging solutions. Also, increasing use in electric vehicles (PP) and lightweight automotive applications for fuel efficiency will drive the PP demand in the coming years.

• The electrical & electronics segment is expected to experience the fastest growth during the forecast period due to the increasing use of polypropylene in insulating materials, capacitors, and other electronic components.

Download Sample Report of Polypropylene Market

Please fill out the form to request a customized copy of the research report.