Precision Chemicals Market Demand, Developments & Growth Prospects, 2026-2034

REPORT DETAILS

Market Statistics

Overview

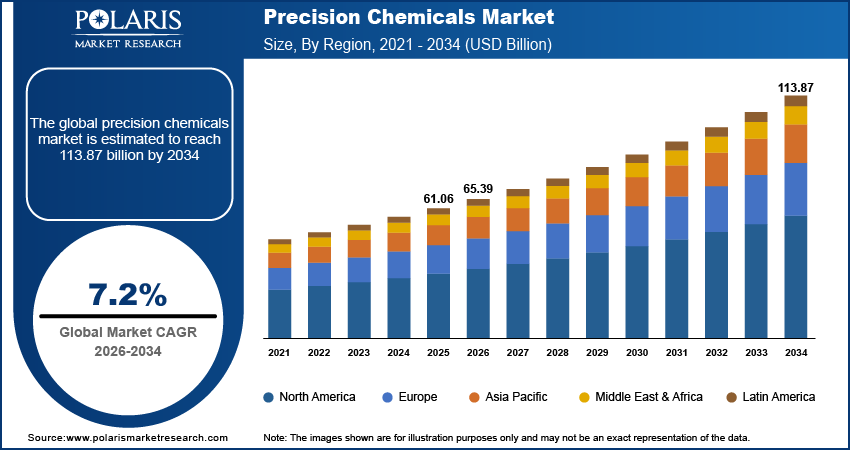

The global precision chemicals market is estimated around USD 61.06 billion in 2025, with consistent growth anticipated during 2026–2034. Driven by the rapid expansion of the semiconductor and microelectronics industry and the acceleration of global chip-production capacity, the precision chemicals market is expected to grow at a steady 7.2% CAGR over the forecast period.

Future Demand Scenarios

- Base scenario: Demand expands in line with stable output across pharmaceuticals, electronics, and specialty manufacturing, supported by consistent consumption of high-purity reagents and intermediates.

- Upside scenario: Stronger penetration of advanced materials, rapid growth in semiconductor fabrication, increased biologics and mRNA production, and wider adoption of high-specification synthesis inputs across emerging industries.

- Conservative scenario: Slower industrial activity, postponed capacity additions in electronics and pharma manufacturing, and reduced purchasing of high-purity reagents due to budget constraints.

Key Insights

- The high-purity chemicals segment held the largest share of the market in 2025 due to their central use in pharma synthesis, analytical QC, and large-volume industrial processes.

- Ultra-pure chemicals are the fastest-growing segment as semiconductor fabs require purity levels that tolerate virtually no ionic contaminants.

- Asia Pacific led the market in 2024, driven by strong semiconductor chemical demand across China, South Korea, Japan, and Taiwan.

- North America is projected to grow rapidly, supported by rising adoption of high-purity and ultra-pure formulations in electronics and advanced manufacturing.

Industry Dynamics

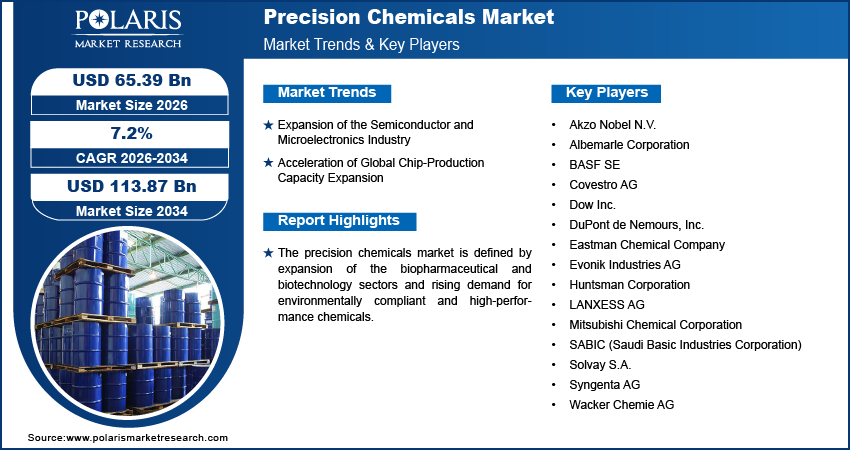

- Expansion of the Semiconductor and Microelectronics Industry

- Acceleration of Global Chip-Production Capacity Expansion

- Rising CAPEX, increasing purity-control costs, and long certification timelines continue to slow scale-up in the market growth.

- Bio-based formulations, PFAS-free alternatives, and cleaner solvent systems are creating opportunities.

Market Statistics

- 2025 Market Size: USD 61.06 billion

- 2034 Projected Market Size: USD 113.87 billion

- CAGR (2026-2034): 7.2%

- Asia Pacific: Largest market in 2025

What is Precision Chemical and Why It Matters

Precision chemicals are high-caliber precision-formulated chemicals manufactured to the most exacting standards of purity for industries that rely on predictable and consistent performance. Differentiated chemical products, controlled manufacturing chemicals, support electronics, pharmaceuticals, and advanced materials where stable reactions and uniform quality are critical. The increasing demand comes from more stringent needs for compliance and inputs that are cleaner and more reliable. With dependable precision chemical supply, product quality, process stability, and a stronger competitive position are ensured in technical markets.

Precision vs Specialty vs Commodity Chemicals

| Category | Definition | Quality & Purity | Application Focus | Pricing | Customer Requirements |

| Precision Chemicals | Chemicals made with high purity and performance standards | Very high; controlled manufacturing and narrow tolerances | Electronics, pharma, advanced materials | Highest | Customized specifications, strict consistency |

| Specialty Chemicals | Performance-oriented chemicals for specific tasks | High; tailored performance attributes | Coatings, adhesives, additives, agrochemicals | Moderate to high | Application-specific behavior, functional performance |

| Commodity Chemicals | High-volume basic chemicals with extended industrial applications | Standardized; lower purity requirements | Plastics, fuels, basic industrial chemicals | Lowest | Cost efficiency, bulk supply, broad applicability |

Source: Polaris Market Research Analysis

Top growth segments center on ultra-low contamination requirements.

- High-purity solvents: Strong demand due to pharmaceutical synthesis, biologics purification, and analytical workflows.

- Ultra-pure reagents: Increasing adoption in genomics, proteomics, and chemical R&D owing to the need for consistent quality.

- Electronic chemicals: Fastest-growing segment led by semiconductor node transitions, AI hardware, and advanced cleanroom standards.

End-use hotspots shape long-term demand.

- Pharmaceuticals: Increased demand for API intermediates, purification solvents, and analytics reagents that supports biologics and mRNA.

- Semiconductor and EV batteries: An expanded use of electronic-grade chemicals in chip fabrication and high-purity materials for cathode and electrolyte production.

- Agrochemicals: growth in the uses of precision catalysts, solvents, and specialty intermediates for higher-efficiency formulations.

- Precision cleaning: Usage in aerospace, medical devices, optics, and defense industries where contamination may be critical in devices or components.

Source: Polaris Market Research Analysis

Drivers & Opportunities

Expansion of the Semiconductor and Microelectronics Industry

Precision chemicals for semiconductors are growing, as fabrication environments have tighter operational tolerances and a demand for high-performance chemical formulations. This is fueled by demand in the regulatory driven sector, where contamination free etch, ultracleaning processes, and deposition chemistries amenable to shrinking nodes have ascended to the highest priority list in fabs. Industry indications also show no letup in this trend. The Semiconductor Industry Association announced worldwide semiconductor industry sales of USD 57.0 billion in April 2025, a sharp increase over USD 55.6 billion in March 2025. This growth is fueling the demand for additional chemicals in each wafer process. Greater system complexities increase demands for precise inputs, thereby fueling demands on ESG chemicals, precision agriculture chemicals, or manufacturers of similar products.

Acceleration of Global Chip-Production Capacity Expansion

The rapid build-out of new fabs strengthens demand for high-purity chemical supply chains. Production line requires repeatable formulations for lithography, CMP, wet cleans, and surface conditioning-each of these pushes suppliers toward advanced high-performance chemical formulations optimized for repeatability. A total of 300mm fab equipment spending from 2026 to 2028 of USD 374 billion is forecast by SEMI, a reflection of the dramatic expansion of the worldwide semiconductor production infrastructure. This spending multiplies chemical intensity per wafer pass and raises the stakes on chemical purity control and compliance with ESG chemical frameworks. Rising fab production volumes are increasingly linked to demand for precise semiconductor chemicals, closely tracking capacity expansion over time. At the same time, sectors such as agricultural chemicals face pressure to improve purity and sustainability as regulatory-driven demand patterns shift.

Restraints & Challenges

CAPEX Requirements

Capital requirements escalate rapidly in precision chemical manufacturing, as producers must invest in specialized reactors, solvent-capture modules, and tightly controlled purification systems built to narrow operational tolerances. As the industries move into pharmaceutical or semiconductor-grade benchmarks, the incremental upgrade in classes brings forth outsized financial commitments, thereby creating an investment environment where minor refinements in processes need disproportionately heavy infrastructure shifts.

Purity-Control Cost

Ultra-high purity maintenance now becomes a layered sequence of analytical checks, reagent conditioning steps, filtration stages, and continuous surveillance, with each adds density to an already expensive operational matrix. As purity thresholds get tighter, QC frequency rises, straining budgets, personnel capacity, and analytical equipment in tandem.

Certification Time

Certification proceeds through long, multi-step testing cycles incorporating impurity profiling, stability testing, and customer feedback loops. These protracted product cycles cause delays in commercialization, leaving product manufacturers in a holding action situation, where their capacity for manufacturing overshadows the approval and licensing of products, particularly in areas of unremitting product reliability, such as biologics, micro-electronics, and advanced coatings.

Buyer Pain Points

- Freezes CAPEX escalation to make vendor growth feel like a transformation instead of a sourcing move.

- Certification sequences add to the length of production times and cause buyer involvement in loop processes of onboarding to interrupt planning horizons.

- Ultra-purity premiums reduce purchasing power, particularly for consumers operating on a high-volume process.

- A limited supplier ecosystem increases vulnerability to allocation constraint, flash price movements, and transport variability.

- ESG-linked documentation trails add administrative drag, requiring buyers to maintain audit-ready transparency at all times.

Emerging Opportunities

A new set of growth pockets is forming in precision chemicals, driven by interest in bio-based formulations, PFAS-free replacements, and cleaner solvent systems. These products demand very tight purity ranges and predictable performance behavior. Requirements shift fast, and specifications become extremely narrow. As industries move toward safer, cleaner, and more engineered chemical inputs, precision chemicals begin sliding into higher-margin territory. These opportunities sit far above traditional commodity lines. The adoption rate is rising in the fields of pharmaceuticals, electronics, specialty coatings, and green technologies. The suppliers able to provide stable and repeatable quality are instant winners with access to high-value customers, with long-term agreements and higher floors.

Business Impact:

- Profit: Bio-based chemicals and PFAS alternatives often generate better margins. The production routes of the latter are more technical, fewer vendors qualify, and returns are pushed higher.

- Supply: These markets create their own supply chains. Traceability, high-purity feedstocks and controlled processing conditions become mandatory. Bulk suppliers cannot meet these expectations, so a separate ecosystem develops.

- Pricing: Pricing is independent of conventional chemical benchmarks. Buyers pay for performance, validated regulatory acceptability, and consistent quality premium pricing is assured for qualified producers.

Source: Polaris Market Research Analysis

Segmental Insights

This report provides granular coverage of the precision chemicals market by grade, product type, application, enabling readers to identify the fastest-growing and most profitable demand pockets.

By Grade

-

High-Purity Chemicals

This grade captured the largest share due to its central role in pharmaceutical synthesis, analytical QC, and high-volume industrial formulations. Grade-wise precision chemicals within this tier provide predictable impurity thresholds to prevent reaction drift. Even a 0.1% impurity rise in an excipient precursor destabilize yields and force batch revalidation. High-purity classifications remain preferred as they balance purity with manageable cost exposure.

-

Ultra-Pure Chemicals

Ultra-high purity chemicals posted the fastest growth. Semiconductor manufacturers demand purity envelopes that tolerate almost no foreign ions, as nanometer-scale circuits fail with part-per-trillion contaminants. A single metal ion spike in an etchant trigger rough pattern edges and wafer losses. These chemicals also support advanced pharmaceutical chemical purity settings, where biologics react sharply to catalytic residues. Momentum stems from this combined pull from electronics and next-generation therapeutics.

-

Reagent-Grade

Reagent-grade chemicals help cost-conscious environments where ultra-purity is not required. They feed routine laboratory reactions, buffers, and non-regulated synthesis tasks. These precision chemical formulations work well in cases where small impurity deviations do not compromise the results. For example, reagent-grade solvents in academic workflows provide flexibility as long as impurity drift does not distort critical endpoints.

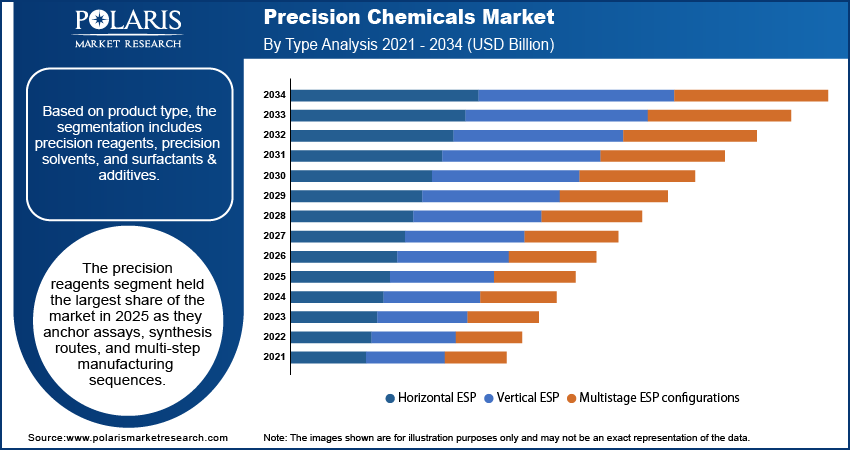

By Product Type

-

Precision Reagents

Precision reagents held the leading share as they anchor assays, synthesis routes, and multi-step manufacturing sequences. Their chemical behaviors solvation, dissociation, thermal patterns must remain consistent across repeated cycles. A slight stereochemical slip in a reagent distort enantiomeric ratios and disrupt dosage uniformity. They remain essential to grade-wise precision chemicals across pharma and specialty chemistry.

-

Precision Solvents

This was the fastest-growing product type. Semiconductor wafer cleaning, pharmaceutical crystallization, and chromatographic workflows require solvents that offer stable evaporation profiles and extremely low trace-metal content. Even microresiduals create ghost peaks or degrade the lithography contrast. As purity deviations impose measurable yield penalties, precision solvents turn out to be of strategic importance.

-

Surfactants & Additives

Interface dynamics, dispersion uniformity, and wetting properties in the case of coatings, cleaners, and agricultural products are influenced by surfactants or additives. As an example, precision additives in crop chemistry, must provide uniformity in the droplet. For this, impurity-driven micelle collapse reduces the adhesion and pest performance of pesticide delivery. Growth remains steady but more application-bound compared to the reagent and solvent categories.

By Application

-

Pharma (API / Excipients)

This segment depends on pharmaceutical chemical purity to safeguard reaction outcomes. API crystallization, impurity rejection, and excipient compatibility hinge on stable chemical inputs. If impurities exceed 0.1%, polymorph shifts may occur, triggering lengthy purification cycles and financial losses. Precision chemical formulations stabilize these risk-sensitive production stages.

-

Electronics (Etchants, Cleaners, Dopants)

The electronics category grew the fastest. Precision semiconductor materials have to have complete control over contamination. Trace ammonia, alkaline ions, or metals create electrical defects and destroy wafer yield. Ultra-high purity chemicals enforce this stability, especially when the shrinkage of logic nodes and the increase in EUV lithography intensify purity thresholds.

-

Agriculture (Crop Chemistry, Smart Formulations)

Agricultural applications are all about efficiency and formulation stability. It is important that smart formulations maintain emulsion integrity through a wide range of temperatures and soil chemistries. Impurities above tolerance levels disrupt droplet behavior and reduce bioavailability. Precision chemicals enhance deliverability and performance for high-value crops.

-

Cleaning Applications

High-spec cleaning systems rely upon solvents and additives possessing predictable behaviour regarding residue, and controlled evaporation. A non-volatile residue as low as 0.05% distort optical surfaces and reduce coating adhesion. Demand is steady across electronics, aerospace tooling, laboratory maintenance, and medical device preparation.

Segmentation Table

| Segment Category | Sub-Segment | Market Share Ranking | Fastest-Growing Indicator | Key Driver |

| By Grade | High-Purity Chemicals | High | No | Broad use in pharma and industrial precision workflows. |

| Ultra-Pure Chemicals | Medium | Yes | Precision semiconductor materials, extreme purity thresholds. | |

| Reagent-Grade | Medium-Low | No | Cost-efficient operational chemistry; acceptable impurity tolerance. | |

| By Product Type | Precision Reagents | High | No | Foundation for controlled reactions, assays, and synthesis. |

| Precision Solvents | Medium | Yes | Wafer cleaning, crystallization purity, chromatographic consistency. | |

| Surfactants & Additives | Medium | No | Stability tuning in coatings, agriculture, and formulations. | |

| By Application | Pharma (API/Excipients) | High | No | Pharmaceutical chemical purity requirements; impurity-sensitive yields. |

| Electronics (Etchants, Dopants, Cleaners) | Medium | Yes | Purity-critical semiconductor workflows; sub-ppm defect sensitivity. | |

| Agriculture (Crop Chemistry) | Medium | No | Smart formulation stability and controlled release performance. | |

| Cleaning Applications | Medium-Low | No | Residue-free solvents and additives fo optics and industrial hygiene. |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Regional Analysis

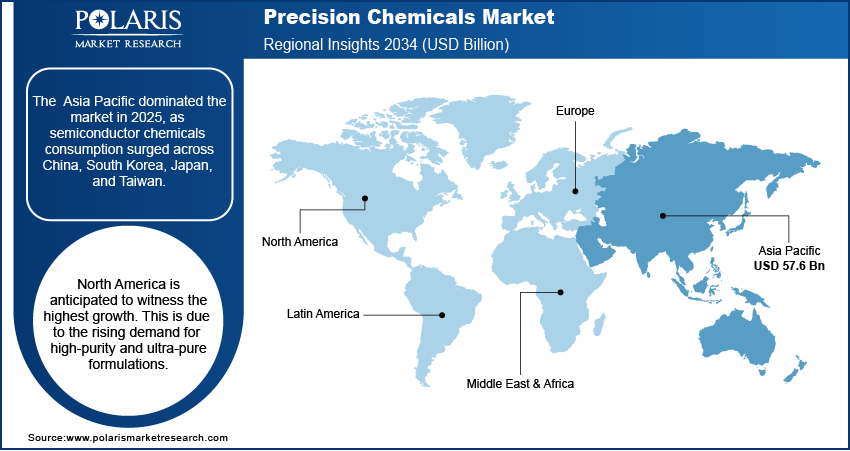

Asia Pacific Market Assessment

The Asia Pacific dominated the market in 2025, as APAC semiconductor chemicals consumption surged across China, South Korea, Japan, and Taiwan. Expanding fabrication capacity considerably raised demand for ultra-pure electronic chemicals, high-purity reagents, and grade-wise precision chemicals consumed in lithography and wafer-level processes. Investments in renewable energy and next-generation storage systems raised demand for precision formulations applied in lithium-ion and advanced battery chemistries. The International Renewable Energy Agency estimates that renewable energy capacity will increase from around 1,300 GW in 2023 to almost 2,500 GW by 2028 in the region. The establishment of chemical R&D hubs and competitive manufacturing ecosystems supported the scaling of high-performance formulations within the region.

North America Precision Chemicals Market Insights

North America is anticipated to witness the highest growth. This growth is supported by rising demand for high-purity and ultra-pure formulations. Expanding semiconductor fabrication in the US and Canada strengthened the need for advanced etchants, cleaners, and deposition chemicals used in cleanroom manufacturing supply chains. TSMC announced that it had increased its planned investment in advanced semiconductor manufacturing in the United States by an additional USD 100 billion. This brought its total planned U.S. investment to roughly USD 165 billion, building on the earlier USD 65 billion committed to its Phoenix, Arizona facilities. Pharmaceutical R&D hotspots in biologics and mRNA technology platforms contributed to the demand for precise-grade reagents and high-purity solvents for their respective regulated manufacturing quantities. The increase in battery production facilities and gigafactory expansions also triggered a demand increase with the emergence of electrolyte chemicals and cathode precursors.

Middle East & Africa (MEA) and Latin America Precision Chemicals Market Overview

The Middle East & Africa (MEA) and Latin America growth in the precision chemicals market driven by expanding healthcare and analytical testing requirements. Diagnostic infrastructure investments across the Gulf countries and South Africa improved the consumption of precision reagents, high-purity solvents, and lab-grade chemicals. Industrial modernization and the production of emerging specialties encouraged greater uptake of controlled specifications. Growth in analytical laboratories, environmental test units, and regulated process industries supported growth in the consumption of precision-grade inputs. Demand clusters expanded gradually, driven by institutional upgrades rather than high-volume industrial shifts.

Source: Polaris Market Research Analysis

Heat Map Analysis

| Region | Demand Intensity | Production Strength | Industrial Consumption | Regulatory Influence | Growth Momentum |

| Asia Pacific | Very High | High | Very High | Medium | Very High |

| North America | High | Medium–High | Very High | High | High |

| Europe | Medium–High | Medium | High | Very High | Medium |

| Middle East & Africa | Low–Medium | Low | Medium | Medium | Medium |

| Latin America | Medium | Low–Medium | Medium | Low–Medium | Medium |

Source: Polaris Market Research Analysis

Value Chain, Competition & Strategic Moves

Value in the precision chemicals market concentrates around three pillars. Purification technology, documentation depth, and controlled logistics. Small shifts in filtration, crystallization, or solvent recovery materially change product grade, creating clear margin hotspots for skilled producers. Documentation remains equally important, as buyers in regulated industries depend on detailed impurity mapping and audit-ready records throughout the supplier qualification cycle. Logistics adds the final layer traceable batches, protective packaging, and climate-controlled transport preserve purity from plant to customer. Manufacturers strong in all three areas convert operational discipline into premium positioning.

Key Strategies

Strategic activity continues to accelerate as precision chemicals manufacturers respond to regulatory and performance pressures. M&A expands capabilities in purification and application-specific chemistry. Backward integration allows producers greater control over quality and impurities. Green chemistry initiatives aim for cleansed solvents, energy-efficient synthesis methods, and waste-reducing synthesis.

Competitive Matrix (3-Tier Placeholder)

| Tier | Supplier Type | Core Strengths | Typical Weaknesses | Ideal Customer Fit |

| Tier 1 | Global Majors | Large-scale production, deep compliance capabilities, multi-site supply continuity, broad product portfolios | Slower customization, higher qualification overhead, premium pricing | Multinational buyers requiring strict documentation, long-term reliability, and global alignment |

| Tier 2 | Niche Specialists | High-purity expertise, rapid customization, shorte supplier qualification cycles, strong technical support | Smaller capacity, narrower portfolios, higher sensitivity to feedstock variability | Buyers with tight specifications, specialty applications, or emerging chemistry needs |

| Tier 3 | Regional Formulators | Cost agility, fast turnaround, localized technical service, flexible MOQs | Limited compliance depth, lighter documentation systems, inconsistent long-term scale | Local buyers needing quick supply, moderate purity ranges, and short-run or pilot-scale formulations |

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The global precision chemicals market is moderately competitive, with the major players concentrating on the formulation of strictly controlled chemicals. Additionally, innovation within the market is driven by the requirement for sustainable methods of synthesis, low-emission production processes, and highly efficient catalysts. Also, the major drivers for innovation in the global precision chemicals market are the increasing demand for semiconductor production processes, crop protection agents, and precision products.

Key companies operating in the global precision chemicals market include Akzo Nobel N.V., Albemarle Corporation, BASF SE, Covestro AG, Dow Inc., DuPont de Nemours, Inc., Eastman Chemical Company, Evonik Industries AG, Huntsman Corporation, LANXESS AG, Mitsubishi Chemical Corporation, SABIC (Saudi Basic Industries Corporation), Solvay S.A., Syngenta AG, and Wacker Chemie AG.

Key Players

- Akzo Nobel N.V.

- Albemarle Corporation

- BASF SE

- Covestro AG

- Dow Inc.

- DuPont de Nemours, Inc.

- Eastman Chemical Company

- Evonik Industries AG

- Huntsman Corporation

- LANXESS AG

- Mitsubishi Chemical Corporation

- SABIC (Saudi Basic Industries Corporation)

- Solvay S.A.

- Syngenta AG

- Wacker Chemie AG

Future Outlook & Scenario Analysis

Future precision chemical demand will concentrate in segments where regulatory intensity overlaps with advanced processing technology. The markets of semiconductor chemicals, bioprocessing reagents, and high-grade solvent systems are already shifting toward emerging purity standards that call for tighter impurity control, automated QC loops, and fully documented batch histories. Suppliers that have high-tech purification platforms, digital documentation pipelines, and low-emission synthesis routes will lead the strongest growth trajectories, as regulators push deeper traceability and cleaner manufacturing footprints.

Macro Risks: Chip Cycles, Pharma Pricing Pressure, Regulatory Bans

Volatility persists despite strength in structural demand. Orders for semiconductor chemicals surge and contract with chip-capex cycles, leading to sharp volume reversals. Pharmaceutical customers are under continuous pricing pressure, which will inevitably dilute the margins of the upstream chemical providers. Simultaneously, regulatory trends-from the restrictions on PFAS to limitations on the use of solvents-make things uncertain and hasten sudden reformulation efforts. These risks demand a blend of scenario planning that combines short-cycle market behavior with long-cycle compliance obligations.

Innovation Opportunities

Closed-loop solvent recovery is emerging as a high-impact innovation arena. It relates to sustainability in chemical production, waste reduction, cost stabilization, and improvement in meeting new requirements of purity and emissions. Suppliers that integrate advanced solvent-recycling modules, on-site purification systems, and energy-efficient recovery technologies will gain an edge in markets where purity drift or waste-handling costs are major bottlenecks.

Tech–Regulation Scenario Matrix for the Precision Chemicals Market:

| Scenario Zone | Regulatory Pressure | Technology Intensity | Market Description |

| Low-Reg × Low-Tech | Low | Low | Slow growth environment; competition centers on cost, volume, and basic formulations. |

| High-Reg × Low-Tech | High | Low | Compliance-heavy setting with margin compression; suppliers struggle to meet rising documentation and purity expectations without advanced tools. |

| Low-Reg × High-Tech | Low | High | Innovation-driven but niche; adoption depends on specialized applications and selective customer segments. |

| High-Reg × High-Tech | High | High | Strongest expansion potential; premium demand, higher price stability, and superior value capture for validated producers. |

Source: Polaris Market Research Analysis

Where Should Companies Invest Now?

Companies should prioritize high-tech purification systems, digital traceability infrastructure, solvent-recovery technologies, and regulatory-aligned product pipelines built around next-generation purity thresholds. These investments anchor long-term competitiveness as both regulation and technology move sharply upward.

Industry Developments

- December 2025: Croda International formed a strategic partnership with Amino GmbH to expand global supply of high-purity amino acids for pharmaceutical and biomanufacturing use. The move supported precision-chemical launches by enabling Croda to introduce its BioXPro high-purity histidine and arginine products.

- December 2025: Enlight Metals launched Enlight TradeHub, a new subsidiary focused on supplying industrial-grade chemicals such as solvents, acids and specialty intermediates across India and Asia, expanding its business beyond metals sourcing.

Precision chemicals Market Segmentation

By Grade Outlook (Revenue, USD Billion, 2021-2034)

- High-purity chemicals

- Ultra-pure chemicals

- Reagent-grade

By Product Type Outlook (Revenue, USD Billion, 2021-2034)

- Precision reagents

- Precision solvents

- Surfactants & additives

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Pharma (API/excipients)

- Electronics (etchants, cleaners, dopants)

- Agriculture (crop chemistry, smart formulations)

- Cleaning applications

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Precision Chemicals Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 61.06 Billion |

| Market Size in 2026 | USD 65.39 Billion |

| Revenue Forecast by 2034 | USD 113.87 Billion |

| CAGR | 7.2% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Precision Chemicals Market FAQ's

The global market size was valued at USD 61.06 billion in 2025 and is projected to grow to USD 113.87 billion by 2034.

The Asia Pacific region holds the largest share in the precision chemicals market, fueled by rising semiconductor chemicals consumption across China, South Korea, Japan, and Taiwan.

Pharma (API / Excipients) is the primary application as this segment depends on pharmaceutical chemical purity to safeguard reaction outcomes.

A few of the key players in the market are Akzo Nobel N.V., Albemarle Corporation, BASF SE, Covestro AG, Dow Inc., DuPont de Nemours, Inc., Eastman Chemical Company, Evonik Industries AG, Huntsman Corporation, LANXESS AG, Mitsubishi Chemical Corporation, SABIC (Saudi Basic Industries Corporation), Solvay S.A., Syngenta AG, and Wacker Chemie AG

Key factors include expansion of the semiconductor and microelectronics industry along with acceleration of global chip-production capacity expansion.

Download Sample Report of Precision Chemicals Market

Please fill out the form to request a customized copy of the research report.