Active Pharmaceutical Ingredient (API) Market Size, Share, 2026-2034

REPORT DETAILS

What is the API market size in 2025?

The active pharmaceutical ingredient (API) market size was valued at USD 265.53 billion in 2025 and is expected to register a CAGR of 5.8% from 2026 to 2034. The increasing consumption of over-the-counter (OTC) drugs fuels the market growth. Further, the rising number of local and global generic drug manufacturers boosts the industry expansion.

Market Statistics

Key Takeaways

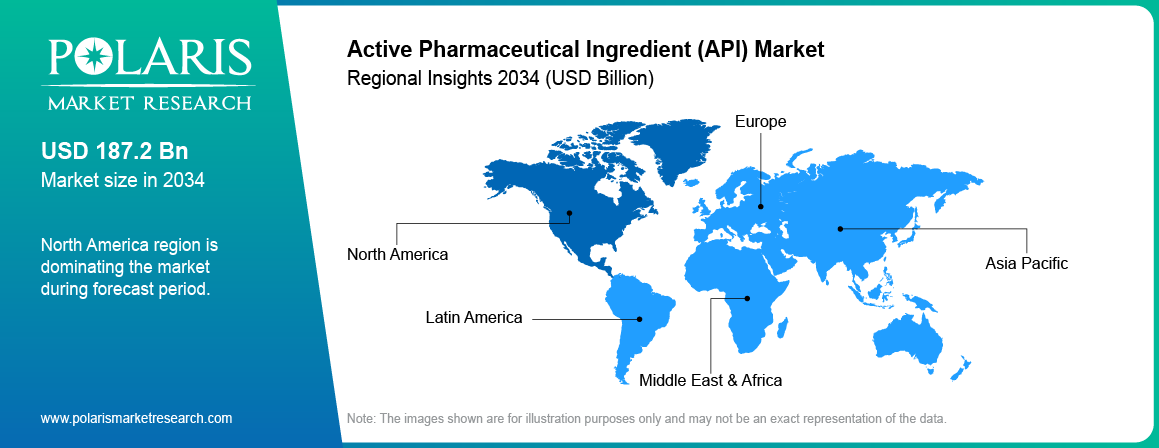

- In 2025, North America accounted for the largest revenue share of 39.79%. The presence of several established pharmaceutical companies and major research and development laboratories in the region contributes to its dominant position.

- The industry in Asia Pacific is projected to register a substantial CAGR of 6.4% over the forecast period. The increasing number of local and global players drives the growth.

- The aqueous segment is anticipated to account for a 6.0% CAGR. It is due to the water solubility of aqueous APIs and their extensive use in oral and injectable drugs.

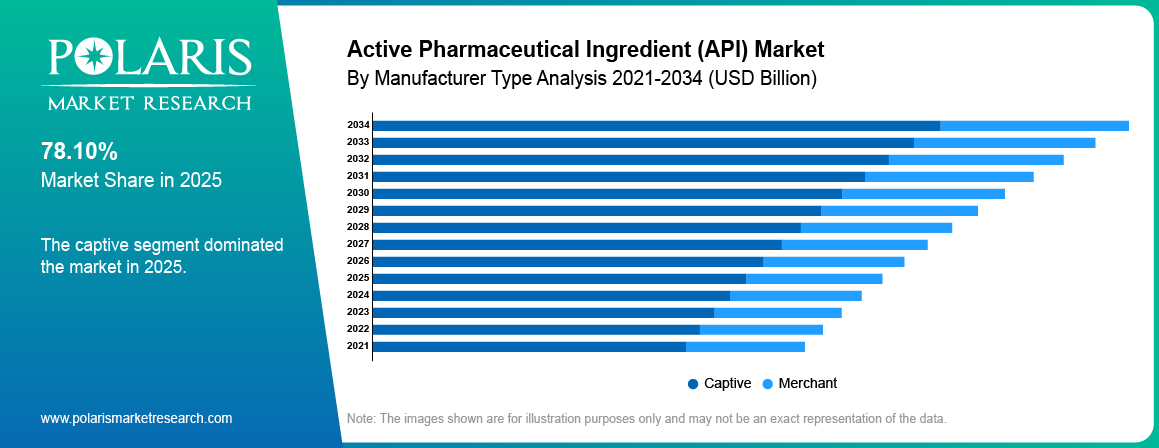

- In 2025, the captive segment held the largest revenue share of 51.2%. The dominance is driven by increasing investments by private investors and various incentives by governments worldwide.

- The cardiology segment accounts for a significant market revenue share of 22.6%. This is due to the rising global incidence of cardiovascular diseases.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Increasing investments in the pharmaceutical sector are driving the API market growth.

- The rising number of pipeline drugs contributes to the expansion of the industry.

- A lack of a skilled workforce hinders the industry's growth.

- Technological advancements in the manufacturing of API are expected to offer lucrative opportunities during the forecast period.

AI Impact on Active Pharmaceutical Ingredient Market

- Artificial intelligence (AI) systems accelerate research and development (R&D) by scanning massive datasets to identify promising compounds. It reduces reliance on time-consuming lab experiments.

- Machine learning platforms are used to analyze protein structures and genetic variations. They help generate novel therapeutic leads.

- AI-integrated systems detect anomalies in production and ensure compliance with regulatory standards.

- AI-based predictive analytics provide predictions on demand fluctuations based on seasonal trends and regional disease patterns. It helps market players in better inventory planning. It reduces waste and improves responsiveness to market needs.

- The technology helps customize APIs for personalized treatment, especially in oncology and neurology areas.

- It is also used to streamline regulatory documentation and safety assessments to reduce time-to-market for new drugs.

-market.webp)

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

What is Driving the API Market?

The active pharmaceutical ingredient (API) is a drug component that effectively produces the desired effect. It is the central ingredient of a generic drug, and the name of the API usually refers to the generic drug.

The market for active pharmaceutical ingredients is primarily driven by an increase in the consumption of over-the-counter (OTC) drugs and the entry of new generic drug manufacturers. For instance, according to the Consumer Healthcare Products Association, the retail sales size of over-the-counter drugs has increased from 1.9 billion USD to 43.4 billion USD between 1964 and 2023. The research was conducted in the USA to observe the first preference of drugs during minor illness; 81% of American youth preferred over-the-counter drugs when dealing with illness. On average, a US citizen makes 25-30 trips a year to purchase OTC drugs, according to the study. Thus, increasing consumption of OTC drugs is expected to fuel the active pharmaceutical ingredients market in the forecast years.

Similarly, the active pharmaceutical ingredient (API) market is driven by an increase in the number of local and global generic drug manufacturers. For instance, according to the Indian Ministry of Health and Family and Welfare, in 2023, the total number of pharmaceutical product manufacturers increased to 3000 drug companies and ~10,500 manufacturing units. Moreover, to support and promote local manufacturing, the Indian government, in coordination with the Health Ministry, plans to develop three bulk drug parks. Consequently, the increasing number of drug manufacturers is expected to increase the demand for active pharmaceutical ingredients and positively impact the market growth from 2026 to 2034.

Market Driver Analysis

Increasing Investment in the Pharmaceutical Sector

The pharmaceutical sector in leading and developing countries is attracting major investment from the public as well as private capital investors. For instance, the pharmaceutical sector in the African region was able to attract 81% of the total investment in 2023. Furthermore, increasing research and development activities have resulted in low-cost drug manufacturing and new drug research, which has led capital seekers to attract private investors and promise better returns on their investments. Additionally, increasing exports of pharmaceutical products have attracted public investors to show their interest in the target sector. For instance, according to Invest India, India is a major exporter of pharmaceutical products to over 200 countries. It supplies over 50% of South Africa’s requirement for generic drugs and 40% of the generic demand in the US. In 2023, India’s total export value of pharmaceutical products was calculated at 27.8 billion. Thus, many investors are attracted to the pharmaceutical manufacturing sector, resulting in the accelerated growth of the active pharmaceutical ingredient market.

Increasing Number of Pipeline Drugs

The API market is experiencing robust growth, largely fueled by the increasing number of pipeline drugs. This surge is attributed to advancements in technology and a reduction in the time required for drug discovery services. In 2023, there were 11,835 drugs in pre-clinical trials, and this number grew to 12,485 by May 2024. Additionally, the total number of applicants seeking approval in 2023 was 21,292, which climbed to 22,884 in 2024 across various stages of development. This increase underscores the accelerated pace of pharmaceutical innovation and the growing demand for APIs to support a rapidly growing pipeline of new drugs. As leading players in the industry continue to push forward with advanced research and development, the need for high-quality APIs becomes more critical. These advancements not only enhance the efficiency of drug discovery but also drive the expansion of the API market by creating new opportunities for suppliers and manufacturers. The heightened activity in drug development phases reflects the industry's commitment to addressing emerging medical needs. Also, it reinforces the pivotal role of APIs in bringing novel therapies to market and simultaneously boosts the growth of active pharmaceutical ingredients.

Source: Polaris Market Research Analysis

Segment Analysis

Market Assessment by Form

The API market segmentation, based on form, includes aqueous, non-aqueous liquid, and dry powder. The aqueous segment is projected to grow with a significant CAGR in the market due to the water solubility of aqueous APIs and their extensive use in oral and injectable drugs. Aqueous APIs are generally preferred for their ease of administration and quick onset of action. Increasing demand and rapid development in formulations of oral and injectable drugs are driving the segment’s growth in the active pharmaceutical ingredients market.

Market Evaluation by Manufacturer Type

The active pharmaceutical ingredient market segmentation, based on manufacturer type, includes captive and merchant. In 2025, the captive segment held the largest revenue share of the market due to increasing investment by private investors and various incentives by governments worldwide. Production incentives in India to promote the manufacturing sector have promoted an increase in the number of local manufacturers. Moreover, various incentives and funds allocated to research and development institutes have resulted in the increasing volume of in-house manufactured pharmaceutical products. For instance, in 2021, 41,500 million Euros were raised by European fundraisers, majorly from the public sector and through government initiatives.

Types of Active Pharmaceutical Ingredients (API)

| Type | Description | Where It Is Commonly Used |

| Innovative (Branded) APIs | These are developed through original research and are usually protected by patents for a certain period. They often involve high investment and long development timelines. | Found in newly developed drugs, especially for complex or critical conditions |

| Generic APIs | They are developed after the expiry of the patents. The generic APIs offer identical medical benefits compared to their branded equivalents. Generic APIs are affordable. | Commonly available in common pharmaceutical products and mass treatment programs |

| Synthetic APIs | The synthetic APIs are synthesized using chemical reactions. The synthetic APIs are produced in larger quantities and are consistent in quality. | Found in different types of pharmaceutical formulations |

| Biotech (Biological) APIs | These are extracted from biological organisms or biological processes. They are highly complex and need special production techniques. | Applications include advanced medications like vaccines and biologics. |

| Highly Potent APIs (HPAPIs) | These exhibit their effects even at very low concentrations. They need to be treated carefully during production because of their strong potency. | Used for oncology and other targeted therapies |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Market Breakdown by Regional Insights

By region, the study provides the API market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2025, North America accounted for the largest revenue share in the active pharmaceutical ingredient (API) market due to the presence of several established pharmaceutical companies and major research and development laboratories in the region. Major multinational corporations and biotechnology firms headquartered in the region, such as Pfizer, Abbott, Sunovion Pharmaceuticals Inc., and Thermo Fisher Scientific, are actively participating in competitive rivalry in the production and development of active pharmaceutical ingredients. These companies and research institutes are backed by large investments and funds for the production and development of new drugs and the manufacturing of generic drugs, which is driving the increased demand for active pharmaceutical ingredients. Additionally, a large pool of local manufacturers of generic drugs is another factor driving the growth of the active pharmaceutical ingredients market in the region.

Source: Polaris Market Research Analysis

Asia Pacific is projected to grow with a substantial CAGR over the forecast period due to the increasing number of local and global players. Also, the growing export of locally manufactured drugs is driving the active pharmaceutical ingredient (API) market in the region. For instance, Vietnam has the highest number of pharmaceutical businesses per capita among all Southeast Asian nations, with 442 as of 2020. The second-highest number of pharmaceutical businesses in the region was situated in Thailand, with 395 companies. The increasing number of pharmaceutical industries and exports of locally manufactured drugs are increasing the demand for active pharmaceutical ingredients and simultaneously driving the market for active pharmaceutical ingredients (API).

The active pharmaceutical ingredient market in China is poised for significant growth due to the country's support for biotech innovations and increased public and private funding. The government of China has implemented various policies and initiatives, such as the 14th Five-Year Plan, which includes substantial investments in research and development (R&D). The plan emphasizes the need to allocate a larger portion of R&D spending to research, as historically, most funding has been directed toward the development of pharmaceutical products. Both public and private financial support play a significant role in developing private equity and venture capital to enhance financing options for innovative companies and future opportunities in the pharmaceutical sector of China. Moreover, the involvement of universities and private foundations in financing R&D is expected to strengthen government efforts in fostering innovation and sustaining growth.

Key Players & Competitive Analysis Report

The API market is constantly changing, with various companies working to innovate and stand out in the market. Big global firms lead the market by utilizing extensive research and development, advanced manufacturing technologies, and wide distribution networks to stay ahead. These companies engage in strategic initiatives like mergers, acquisitions, partnerships, and collaborations to improve their product offerings and reach new markets.

Furthermore, new companies are impacting the market by introducing innovative active pharmaceutical ingredients and meeting the needs of specific market sectors. This competitive environment is amplified by continuous progress in biotechnology, greater emphasis on sustainability, and the rising requirement for tailor-made enzyme products in diverse industries. Major players in the active pharmaceutical ingredient (API) market include Pfizer; Teva Pharmaceuticals Industries Ltd.; GSK PLC; Sanofi; Eli Lilly and Company; Merck KGaA; AbbVie Inc.; F-Hoffman La Roche Ltd; AstraZeneca; Dr. Reddy’s Laboratory Ltd.; BASF Corporation; Sun Pharmaceutical Industries Ltd.; Curia Global Inc.; and Nanjing Jianyou Biochemical Pharmaceutical Co., Ltd.

Pfizer is a pharmaceutical company with significant capital investment and advanced research facilities. The company offers a wide range of products in injectable, oral, and tablet forms. Pfizer operates manufacturing plants in several major countries, including the US, Germany, Spain, the UK, and India, with strategic investments and strong supply chain facilities. Pfizer’s CentreOne is responsible for manufacturing and developing active pharmaceutical ingredients. In 2022, Pfizer Inc. invested $120 million to improve its Kalamazoo, Michigan facility, increasing the production of its COVID-19 oral treatment, PAXLOVID. This expansion led to the creation of over 250 high-skilled jobs and enhanced the site’s capacity to produce 1,200 metric tons of active pharmaceutical ingredients annually. The investment was part of Pfizer’s efforts to strengthen US manufacturing capabilities and meet the global demand for PAXLOVID, which has shown an 88% reduction in COVID-19-related hospitalization or death.

BASF Corporation is an industry expert in the production and development of active pharmaceutical ingredients and chemical raw materials for the production of API. The company offers a wide range of products and services for the pharmaceutical industry, including high-quality synthesis tools such as building blocks, reagents, solvents, iron salts, and catalysts. BASF operates subsidiaries and joint ventures in over 80 countries, with six integrated production sites and 390 other production sites across Europe, Asia, Australia, the Americas, and Africa. In 2023, BASF Pharma Solutions and Merck KGaA, Darmstadt, Germany, launched a new electronic data standard, StaQRD, to improve the transfer of quality and regulatory documentation in the pharma industry. Unlike the previous ASTM-E3077 standard, which focused solely on CoA content, StaQRD includes nine additional compliance document types, such as nitrosamine risk assessments and GMP compliance documents. StaQRD aimed to streamline documentation exchange, enhance data integrity, and reduce errors by using Extensible Markup Language (XML). This initiative addresses the need for accurate, real-time data access and aims to accelerate the time-to-market for new drug therapies.

Top Companies in API Market

- Pfizer

- Teva Pharmaceuticals Industries Ltd.

- GSK PLC

- Sanofi

- Eli Lilly and Company

- Merck KGaA

- AbbVie Inc.

- F-Hoffman La Roche Ltd

- AstraZeneca

- Dr. Reddy’s Laboratory Ltd.

- BASF Corporation

- Sun Pharmaceutical Industries Ltd.

- Curia Global Inc.

- Nanjing Jianyou Biochemical Pharmaceutical Co., Ltd.

Active Pharmaceutical Ingredient (API) Industry Developments

- January 2026: Torrent Pharmaceuticals Ltd announced the completion of acquisition of JB Chemicals & Pharmaceuticals Ltd. According to Torrent Pharmaceuticals, the transaction will strengthen its footprint in chronic therapies and branded generics. (source: www.torrentpharma.com)

- October 2025: Merck announced the completion of the acquisition of Verona Pharma plc. According to Merck, the move strengthens and complements its treatment portfolio for patients with cardio-pulmonary diseases to include Ohtuvayre. (source: www.merck.com)

- May 2025: The two companies merged to form Cohance, creating a stronger and more integrated CDMO/API organization. The merger combines Suven’s commercial manufacturing expertise with Cohance’s specialized platforms, including antibody–drug conjugates and complex chemistry capabilities. (source: www.specchemonline.com)

- May 2024: Eli Lilly and Company announced a $5.3 billion investment at its manufacturing site in Lebanon, Indiana, making it the largest US investment in synthetic medicine API production. This significant increase raises the company’s total investment in the Indiana facility from $3.7 billion to $9 billion. The new investment aims to enhance Eli Lilly's capabilities in producing advanced pharmaceutical ingredients and reflects the company's commitment to advancing synthetic medicine technologies. This expansion not only strengthens the firm's manufacturing infrastructure but also highlights its strategic focus on innovation and growth in the pharmaceutical industry. (source: investor.lilly.com)

Active Pharmaceutical Ingredient Market Segmentation

By Product Type Outlook (Revenue – USD Billion, 2021–2034)

- mAb

- Immunoglobulin

- Cytokines

- Insulin

- Peptide Hormones

- Blood Factors

- Peptide Antibiotics

- Vaccines

- Small Molecule Antibiotics

- Highly Potent Active Pharmaceutical Ingredient (HPAPI)

- Others

By Form Outlook (Revenue – USD Billion, 2021–2034)

- Aqueous

- Non-Aqueous Liquid

- Dry Powder

By Manufacturer Type Outlook (Revenue – USD Billion, 2021–2034)

- Captive

- Merchant

By Application Outlook (Revenue – USD Billion, 2021–2034)

- Cardiology

- Oncology

- CNS & Neurology

- Orthopedic

- Endocrinology

- Pulmonology

- Gastroenterology

- Nephrology

- Ophthalmology

- Others

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

API Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 265.53 billion |

| Market Size Value in 2026 | USD 281.83 billion |

| Revenue Forecast in 2034 | USD 468.0 billion |

| CAGR | 5.8% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Manufacturer Type |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The active pharmaceutical ingredient market size was valued at USD 265.53 billion in 2025 and is projected to grow to USD 468.0 billion by 2034

The market is projected to grow at a CAGR of 5.8% from 2026 to 2034.

North America had the largest share of the market in 2025.

The key players in the market are Pfizer; Teva Pharmaceuticals Industries Ltd.; GSK PLC; Sanofi; Eli Lilly and Company; Merck KGaA; AbbVie Inc.; F-Hoffman La Roche Ltd; AstraZeneca; Dr. Reddy’s Laboratory Ltd.; BASF Corporation; Sun Pharmaceutical Industries Ltd.; Curia Global Inc.; and Nanjing Jianyou Biochemical Pharmaceutical Co., Ltd.

The aqueous segment is anticipated to experience substantial growth with a significant CAGR in the market. This growth is attributed to the indispensable role and adaptability of active pharmaceutical ingredients in various applications.

Download Sample Report of Active Pharmaceutical Ingredient (API) Market

Please fill out the form to request a customized copy of the research report.