Reconciliation Software Market Demand Scenario, Developments, and Growth Prospects, 2025-2034

REPORT DETAILS

REPORT DETAILS

What is the reconciliation software market size?

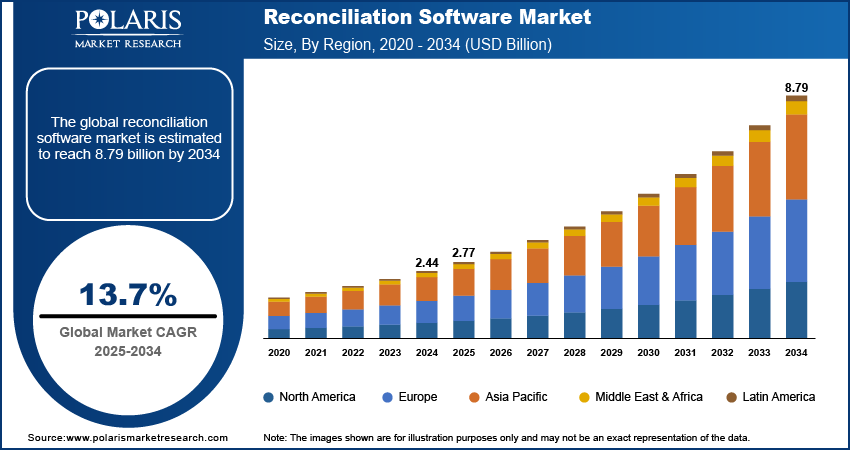

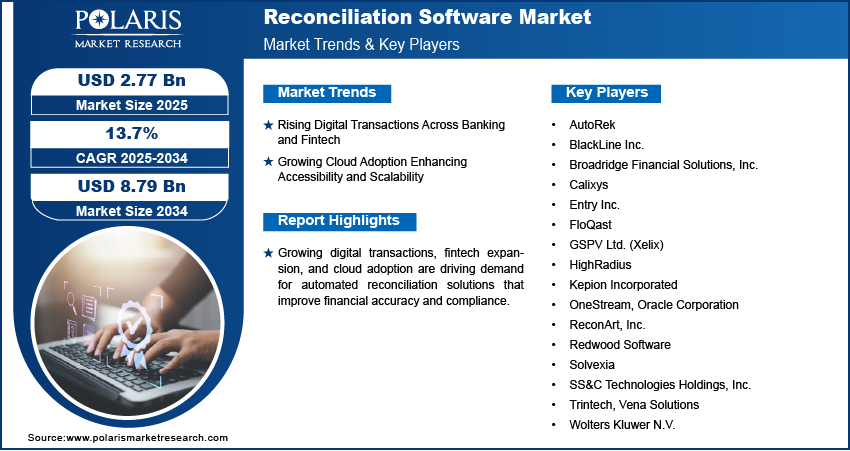

The global reconciliation software market size was valued at USD 2.44 billion in 2024, growing at a CAGR of 13.7% from 2025 to 2034. Growing digital transactions and cloud adoption are driving demand for scalable automated reconciliation systems.

Market Statistics

Key Takeaways

- The cloud segment dominated the reconciliation software market in 2024.

- The retail and e-commerce segment is expected to record the fastest growth driven by increasing online payment volumes and need for automated reconciliation.

- North America accounted for the largest market share in 2024.

- The U.S. market is driven by strong financial institutions and early adoption of AI-driven reconciliation platforms.

- Asia Pacific is projected to grow rapidly from 2025 to 2034 due to expanding digital payment infrastructure and fintech innovation.

- China and India are leading regional growth through rising transaction volumes and accelerated adoption of cloud-based financial systems.

Industry Dynamics

- Rising digital transactions across banking and fintech are boosting demand for automated reconciliation.

- Growing cloud adoption is improving accessibility and scalability of reconciliation systems.

- Increasing use of robotic process automation (RPA) in financial workflows enhancing automation potential while creating opportunity for the industry.

- High setup costs and data security risks are limiting market growth.

What are reconciliation software market consisting of?

The reconciliation software market includes automated platforms designed to match and verify financial transactions across accounts, ledgers, and systems. These solutions are extensively used by banks, fintech companies, e-commerce businesses, and businesses to enhance financial precision and operational efficiency. Vendors concentrate on creating scalable, cloud and AI-enabled systems that increases speed, transparency, and compliance in financial reporting.

Rising digital transaction volumes are boosting demand for automated reconciliation across industries. Growing cloud adoption is improving system accessibility and scalability. Increasing regulatory scrutiny and the need for real-time financial visibility further support market growth. For instance, in October 2025, Omnicell acquired ANiGENT to enhance its reconciliation and drug-diversion detection capabilities in its medication management platform.

However, high deployment expenses, integration issues with legacy systems, and data protection concerns limit adoption by small businesses. Continuous innovation in AI-powered predictive analytics and robot process automation (RPA) is generating new possibilities for smart reconciliation solutions. The market is witnessing increasing adoption across banking, fintech, telecom, and retail industries to maintain accuracy, efficiency, and compliance in financial transactions.

Drivers & Opportunities

Which are the factors driving reconciliation software market growth?

Rising Digital Transactions Across Banking and Fintech: Growth in digital transactions in banking and fintech industries is fueling demand for automated reconciliation as businesses process increasing volumes of transactions and complex data flows. e-CNY transactions in June 2024 totaled USD 986 billion in 17 regions, close to four times the USD 253 billion recorded a year ago, according to the Atlantic Council. Automated reconciliation allows for quicker processing, reduction of errors, and enhanced financial transparency. This trend is growing popular with banks, payment service providers and fintech platforms to obtain precise reporting and effective financial management.

Growing Cloud Adoption Enhancing Accessibility and Scalability: Increasing cloud adoption is enhancing scalability and accessibility of reconciliation systems by making data integration seamless and real-time financial tracking. Cloud-based systems facilitate automation of reconciliation across accounts while lowering infrastructure costs. Scalability and flexibility of such systems are promoting adoption by organizations that seek to maximize operations and improve financial visibility.

Segmental Insights

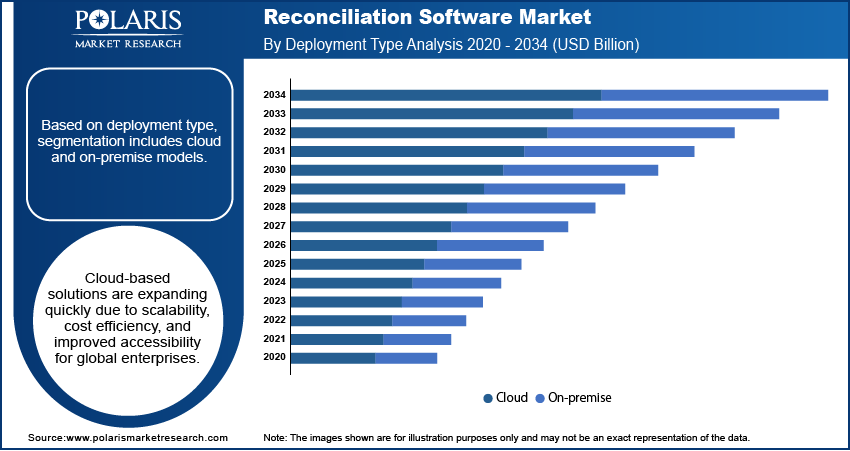

Deployment Type Analysis

By deployment type, the market is divided into cloud and on-premise. The cloud segment led the market in 2024 with growing adoption of SaaS-based financial platforms and digital transformation efforts across enterprises. Also, cloud systems are more scalable and cost-effective.

The on-premise segment is expected to record the highest CAGR through the forecast period with the support of organizations having high data security requirements. Financial institutions prefer on-premise models for higher control over sensitive transaction information.

Enterprise Size Analysis

Based on enterprise size, the market is segmented into large enterprises and small and medium enterprises. Large enterprises led the market in 2024, fueled by significant transaction volumes and higher investment potential for automation. In addition, large companies focus on advanced reconciliation solutions to enhance compliance and financial accuracy throughout worldwide operations.

The small and medium enterprises are expected to develop at the highest CAGR, driven by the presence of affordable, cloud-based offerings. Also, rising digital penetration and financial modernization among SMEs are fueling software installations.

End User Analysis

Based on end user, the market is segmented into BFSI, retail & e-commerce, manufacturing, healthcare, and other end users. The BFSI segment led the market in 2024, fueled by banking, insurance, and payment processing, which have high reconciliation needs. Furthermore, financial institutions place great importance on automation to improve transaction accuracy to meet regulatory audit.

The retail & e-commerce segment is anticipated to grow at the fastest CAGR during the forecast period, supported by expanding online payment volumes. In addition, growing cross-platform transactions are increasing the need for automated reconciliation systems. In October 2025, Adyen and SAP have launched the “Open Payment Framework” for retailers that cuts out manual payment setups and speeds up ecommerce payment integration.

Regional Analysis

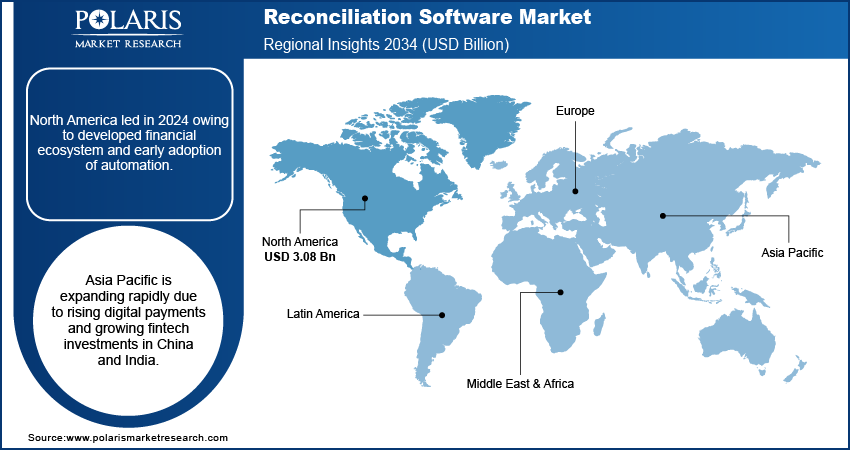

North America dominated the reconciliation software market in 2024, fueled by strong presence of financial institutions and early adoption of advanced automation tools. Moreover, growing regulatory compliance requirements in the U.S. and Canada are driving adoption of reconciliation platforms across banks and fintech companies.

The U.S. Reconciliation Software Market Insights

The U.S. held the highest market share in North America due to high transaction volumes across banking, retail, and fintech sectors are driving the adoption of automated reconciliation systems. According to the Federal Reserve Payments Study (FRPS) report 2024, general-purpose card payments reached 153.3 billion transactions worth USD 9.76 trillion in 2022, growing 6% in volume and 10.5% in value from 2021. Moreover, increasing focus on data transparency and audit compliance is encouraging enterprises to integrate AI-based reconciliation tools in financial workflows.

Europe Reconciliation Software Market Assessments

Europe is expected to hold a significant share owing to strict financial reporting standards and the digital transformation of financial operations across the UK, Germany, and France. In addition, the growing adoption of cloud-based solutions among European banks is strengthening demand for automated reconciliation systems. For instance, in October 2025, Adyen and SAP have introduced a cloud-based “Open Payment Framework” for retailers that reduces manual payment setup and lets merchants integrate payment methods faster.

Asia Pacific Reconciliation Software Market Trends

Asia Pacific is projected to grow at the fastest CAGR during the forecast period, driven by the rapid expansion of digital payment ecosystems in China and India. As per National Payments Corporation of India (NPCI), digital payment transactions rose from USD 23.47 million in FY 2017-18 to USD 2.12 billion in FY 2023-24, growing at a 44% CAGR, while UPI transactions surged from USD 10.43 million to USD 1.48 billion during the same period, registering a 129% CAGR. Additionally, growing fintech investment and government programs advocating for financial digitalization are driving market adoption within the region.

China Reconciliation Software Market Overview

China market is growing at a rapid pace with digital payment platforms like Alipay and WeChat Pay. In addition, government-backed fintech innovation initiatives are fueling software vendors to extend advanced financial management solutions.

Key Players & Competitive Analysis

The market for reconciliation software is competitive, with suppliers trying to create scalable, cloud-enabled, and AI-powered solutions to improve financial precision and automation. Moreover, strategic collaborations between software providers, fintech players, and financial institutions are fueling adoption in core markets around the globe.

Who are the major players in reconciliation software market?

Some of the major firms in the reconciliation software sector are BlackLine Inc., Trintech, GSPV Ltd. (Xelix), Solvexia, OneStream, Redwood Software, FloQast, Oracle Corporation, AutoRek, Broadridge Financial Solutions, Inc., Wolters Kluwer N.V., Entry Inc., Kepion Incorporated, ReconArt, Inc., SS&C Technologies Holdings, Inc., HighRadius, Vena Solutions, and Calixys.

Key Players

- AutoRek

- BlackLine Inc.

- Broadridge Financial Solutions, Inc.

- Calixys

- Entry Inc.

- FloQast

- GSPV Ltd. (Xelix)

- HighRadius

- Kepion Incorporated

- OneStream

- Oracle Corporation

- ReconArt, Inc.

- Redwood Software

- Solvexia

- SS&C Technologies Holdings, Inc.

- Trintech

- Vena Solutions

- Wolters Kluwer N.V.

Reconciliation Software Industry Developments

- September 2025: AutoRek introduced ARIA, an AI-powered reconciliation tool that automates financial data processing and enhances efficiency for financial institutions.

- October 2025: Regions Bank introduced upgraded Treasury Management services for healthcare clients using MediStreams to automate payments, accelerate processing, and simplify reconciliation.

- October 2025: Chargebacks911 introduced the first Disputes-as-a-Service platform designed to unify dispute data across issuers, acquirers, and merchants. The solution aims to streamline chargeback management with centralized, real-time insights.

- June 2025: SmartStream introduced its AI-driven platform for insurers that automates reconciliation of payments, claims and policyholder data in seconds.

- January 2025: Versana launched its new Reconciliation Module, which electronically matches lenders’ positions with agents’ golden-source data in the syndicated loan market to spot and fix discrepancies quickly.

Reconciliation Software Market Segmentation

By Deployment Type Outlook (Revenue, USD Billion, 2020–2034)

- Cloud

- On-premise

By Enterprise Size Outlook (Revenue, USD Billion, 2020–2034)

- Large Enterprises

- Small and Medium Enterprises

By End User Outlook (Revenue, USD Billion, 2020–2034)

- BFSI

- Retail & E-commerce

- Manufacturing

- Healthcare

- Other End Users

By Regional Outlook (Revenue, USD Billion, 2020–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Reconciliation Software Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 2.44 Billion |

| Market Size in 2025 | USD 2.77 Billion |

| Revenue Forecast by 2034 | USD 8.79 Billion |

| CAGR | 13.7% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 2.44 billion in 2024 and is projected to grow to USD 8.79 billion by 2034.

The global market is projected to register a CAGR of 13.7% during the forecast period.

North America led the market in 2024 due to advanced financial infrastructure and strong adoption of automation across banking and fintech.

A few of the key players in the market are BlackLine Inc., Trintech, GSPV Ltd. (Xelix), Solvexia, OneStream, Redwood Software, FloQast, Oracle Corporation, AutoRek, Broadridge Financial Solutions, Inc., Wolters Kluwer N.V., Entry Inc., Kepion Incorporated, ReconArt, Inc., SS&C Technologies Holdings, Inc., HighRadius, Vena Solutions, and Calixys.

The cloud segment dominated in 2024 driven by the rapid shift toward SaaS-based and scalable financial solutions.

The retail and e-commerce is expected to expand rapidly due to increasing online transactions and the need for real-time reconciliation.

Download Sample Report of Reconciliation Software Market

Please fill out the form to request a customized copy of the research report.