SiC-On-Insulator and Other Substrates Market Size, Report 2026-2034

REPORT DETAILS

What is SiC-On-Insulator and Other Substrates Market Size?

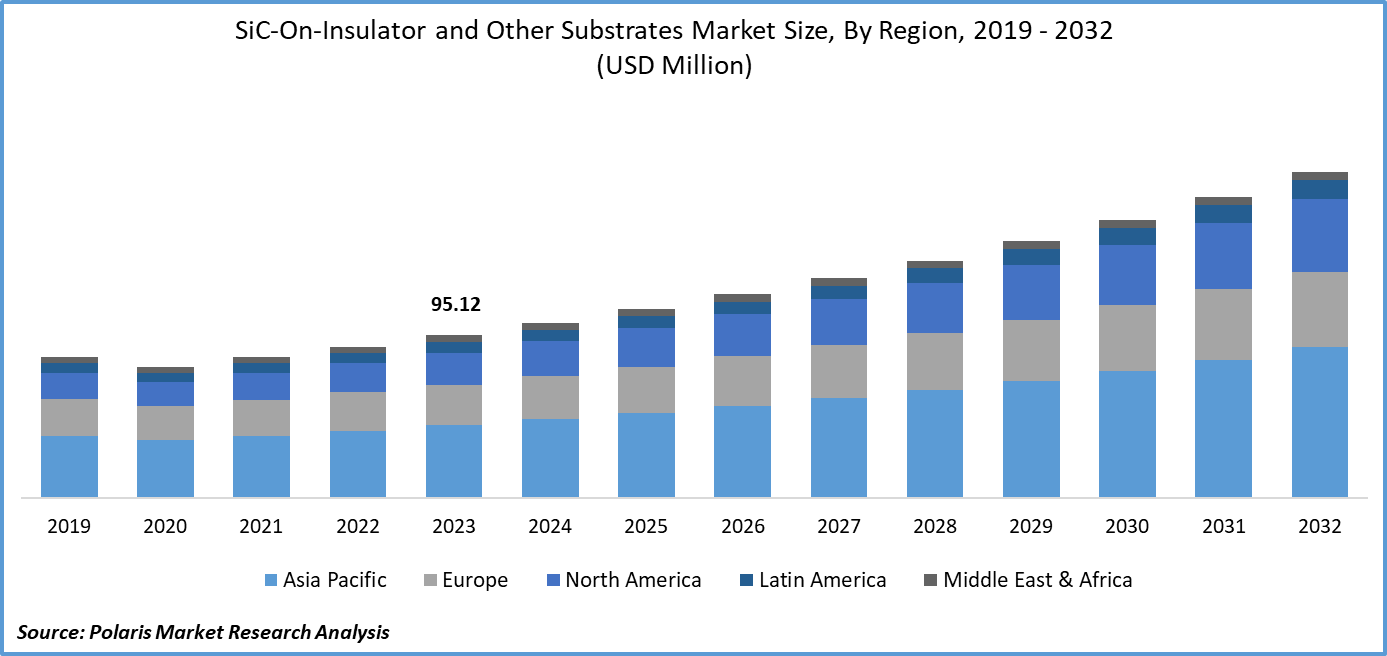

SiC-On-Insulator and Other Substrates Market size was valued at USD 110.41 million in 2025 and is anticipated to exhibit a CAGR of 8.3% during the forecast period. The growth is driven by rising demand for high performance electronics, increase in the new product launch with advance technology, and technological advancement.

Market Statistics

Key Takeaways

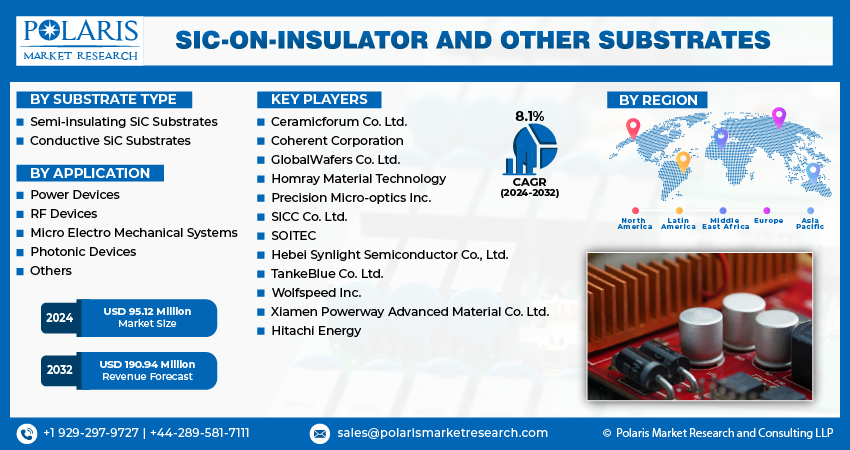

- Asia Pacific dominated the market and contributed over 38% of the SiC-on-insulator and other substrates market share in 2025

- By substrate type category, the conductive SiC substrates segment is expected to grow with a significant CAGR over the SiC-on-insulator and other substrates market forecast to 2034

- By application category, the power devices segment held the dominating SiC-on-insulator and other substrates market share in 2025

Industry Trends

Silicon carbide (SiC) on insulators and other substrates refers to the process of growing or depositing a thin layer of silicon carbide onto an insulating material, such as silicon dioxide sapphire or another suitable substrate material. This technique allows for the creation of high-quality SiC films with excellent electrical and optical properties, which are useful for a wide range of applications.

The global SiC-on-insulator and other substrates market worth are expected to experience significant growth due to the superior properties of silicon carbide, such as high thermal conductivity, chemical inertness, and high-temperature resistance, which make it an ideal material for use in high-power electronic devices, leading to its increased adoption in power electronics and RF power amplifiers. Advancements in CMOS technology have enabled the development of low-cost and efficient SiC-on-insulator materials, further expanding their application scope.

For instance, in May 2022, Leapers Semiconductor, a developer and manufacturer of power semiconductors, introduced compact SiC MOSFET solutions. These solutions are designed to cater to power electronics applications and include SiC and IGBT modules for improved efficiency and performance of power semiconductors.

The growing demand for energy-efficient technologies also drives SiC-on-insulator and other substrates industry worth, as it helps reduce energy consumption by minimizing power losses in electronic devices. However, the high cost of producing SiC-on-insulator and other substrates is a significant challenge for market growth. The expensive nature of raw materials, coupled with complex manufacturing processes, increases the overall cost of these materials, limiting their widespread adoption. Despite these challenges, government support for the development of advanced technologies and increasing investment in research and development activities are anticipated to create opportunities for the SiC-on-insulator and other substrates market key players during the forecast period.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

What are the market drivers driving the demand for SiC-on-insulator and other substrates market?

Technological advancements and new product launches drive the SiC-on-insulator and other substrates market growth

The technological advancements and new product launches drive the global SiC-on-insulator and other substrate markets. The market's growth is attributed to the increasing demand for high-performance power electronics devices that operate efficiently at high temperatures and frequencies. SiC-on-insulator and other substrates offer improved thermal conductivity, reduced thermal dissipation, and higher breakdown voltage, making them ideal for use in high-power electronic devices such as electric vehicles, renewable energy systems, and advanced industrial applications.

Similarly, the development of new products and technologies using SiC-on-insulator and other substrates is propelling the growth of the market. For example, the introduction of gallium nitride (GaN) on SiC substrates has expanded the range of available materials for high-frequency and high-power electronic devices, enabling faster switching speeds and more efficient power transfer. Also, several companies are investing heavily in developing new manufacturing processes and equipment to improve efficiency and lower production costs. This includes the adoption of advanced epitaxial growth techniques, chemical vapor deposition (CVD), and molecular beam epitaxy (MBE). These advancements have enabled the production of high-quality SiC crystals with fewer defects, leading to better device performance and increased yield rates.

Key Trends in SiCOI Substrate

| Trend | Description | Key Drivers | Examples from Practice |

| Smart-Cut layer transfer fabrication | Hydrogen ion implantation into SiC donor wafers followed by bonding to insulator (oxide/Si) and splitting yields thin, single-crystal 4H-SiCOI films on Si substrates. | Cost-effective reuse of bulk SiC donors; enables large-area (100-200mm) substrates vs. epitaxial growth limits. | 4H-SiCOI wafers with 800nm SiC layer, XRD FWHM 75.6 arcsec confirming crystallinity; Q=6.6×10^4 microrings fabricated. |

| Power electronics for EV/rail HV | SiCOI supports MOSFETs/IGBTs with thin drift layers, high doping, low RDS(on) for 750-1200V classes in traction inverters. | 7-10x higher breakdown field vs. Si; enables compact 800V EV systems with 25-30% loss reduction. | Gen4 SiC MOSFETs cut conduction losses, extend EV range; SiC in 1GW/640kV MMC outperforms Si. |

| Quantum photonics platform | 4H-SiCOI waveguides transparent 400-5000nm with <1dB/cm loss; supports SFWM, color centers for entangled photons/single sources. | Both χ²/χ³ nonlinearity + telecom/room-temp qubits; Q>10^6 resonators for QPICs. | CAR>600 photon pairs/s at 0.17mW pump; visibility>99% interference; SHG/SFG potential. |

| Thermal/robustness enhancements | Si-on-SiC hetero-integration dissipates heat better than SOI; high electron mobility for harsh environments. | EV/renewables need >150°C operation, radiation resistance; 2x saturation velocity vs. Si. | SiC handles 350kW+ fast charging, HVDC (1.2MV); low dielectric constant boosts stability. |

| Lateral power devices | SiCOI-based lateral MOSFETs leverage dielectric isolation for high-voltage integration without edge termination. | Simplified fab for power ICs; high field strength enables compact HV designs. | Analytical models predict low on-resistance, fast switching in SiCOI lateral structures. |

| Supply chain/material advances | Poly-SiC and bonded substrates scale production; collaborations boost 200mm wafers for epi. | EV/quantum demand strains bulk SiC; SmartSiC controls power density/reliability. | Soitec/Resonac JDA for 200mm SiC bonded substrates; commercial 6-inch 4H-SiC epi-ready. |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Which factor is restraining the demand for SiC-on-insulator and other substrates?

The high cost and complex manufacturing process limit the market growth.

The high cost of production is a major barrier for many companies, especially small and medium-sized enterprises, which may need more resources to invest in the expensive equipment and processes required to produce high-quality SiC crystals. The manufacturing process for SiC-on-insulator and other substrates is highly complex and requires specialized expertise involving steps such as epitaxial growth, doping, and device fabrication. This complexity leads to higher production costs, making it difficult for companies to achieve economies of scale and reduce prices. Moreover, the need for more standardization in the manufacturing process and the dependence on a limited number of suppliers for high-quality SiC crystals further contribute to the high cost of production.

Report Segmentation

The market is primarily segmented based on substrate type, application, and region.

| By Substrate Type | By Application | By Region |

|

|

|

Source: Polaris Market Research Analysis

To Understand the Scope of this Report: Request Customization

Category Wise Insights

By Substrate Type Insights

Based on substrate type analysis, the market is segmented on the basis of semi-insulating SiC substrates and conductive SiC substrates. The Conductive SiC Substrates segment is expected to grow with a significant CAGR over the forecast period due to the increasing demand for high-power electronic devices, which require high-performance power devices that can handle high currents and voltages. Conductive SiC substrates are well-suited to meet this demand due to their excellent electrical properties. Also, the increasing emphasis on energy efficiency and sustainability has driven the adoption of conductive SiC substrates in renewable energy applications such as solar inverters, wind turbines, and electric vehicles, as they offer lower power losses and higher efficiency compared to traditional silicon devices.

By Application Insights

Based on application analysis, the market has been segmented on the basis of power devices, RF devices, and others. The power devices segment held the dominant market share in 2023 in the market. This dominance is due to the increasing demand for high-power electronic devices, such as electric vehicles, renewable energy systems, and industrial motor drives. This has led to a growing requirement for high-performance power devices that can handle high currents and voltages. SiC power devices are well-suited to meet this demand due to their excellent electrical properties, such as high breakdown voltage and high thermal conductivity. These properties enable SiC power devices to operate efficiently and reliably in high-power applications, making them a popular choice for power electronics designers. Also, the development of advanced manufacturing techniques has improved the quality of SiC crystals, leading to a reduction in production costs to an extent and an increase in the availability of high-quality SiC wafers. This has enabled the production of more affordable SiC power devices, which has helped to drive up demand in the market.

Source: Polaris Market Research Analysis

Regional Insights

Asia Pacific

The Asia Pacific has emerged as the dominant region in terms of market share in the global SiC-on-insulator and other substrates industry. One of the primary reasons for this dominance is the presence of leading semiconductor manufacturers in countries such as Taiwan, South Korea, Japan, and China. These companies have invested heavily in research and development, which has enabled them to develop advanced technologies and production processes that can meet the growing demand for high-performance SiC devices. In parallel, governments in these countries provide various initiatives to encourage the growth of the semiconductor industry, which further supports the expansion of the SiC market. Also, the availability of low-cost labor and raw materials in some Asian countries helps reduce production costs, making it more competitive for companies operating in the region. The increasing adoption of electric vehicles and renewable energy sources in the region creates a significant demand for power electronics devices that use SiC technology, further contributing to the dominance of the market.

North America

The North American region is expected to experience significant growth in the global markets due to the increasing demand for high-power electronics, such as advanced-power electronic devices. These applications require high-performance materials that handle higher temperatures and voltage levels than regular insulators. In addition, the presence of prominent players in the region is also contributing to the growth of the SiC-on-insulator market.

Source: Polaris Market Research Analysis

Competitive Landscape

The market's key players are focused on developing and producing high-quality, reliable, and efficient products that meet the growing demand for power electronics and RF applications. They invest heavily in research and development to improve the properties of SiC materials, such as reducing defects, improving purity, and increasing crystal size, which can enhance device performance and longevity. These key players also work closely with customers to understand their specific requirements and develop customized solutions tailored to their needs.

Some of the major players operating in the global market include:

- Ceramicforum Co. Ltd.

- Coherent Corporation

- GlobalWafers Co. Ltd.

- Homray Material Technology

- Precision Micro-optics Inc.

- SICC Co. Ltd.

- SOITEC

- Hebei Synlight Semiconductor Co., Ltd.

- TankeBlue Co. Ltd.

- Wolfspeed Inc.

- Xiamen Powerway Advanced Material Co. Ltd.

- Hitachi Energy

Recent Developments

- In October 2023, Globalwafers, the manufacturer of silicon wafers, plans to start mass-producing an advanced type of chip substrate by 2025 to address the auto industry's surging demand for power semiconductors.

- In May 2023, Hitachi Energy inaugurated a new SiC e-Mobility production line in Lenzburg, Switzerland. This is an example of smart manufacturing, and the fully automated production line includes fully integrated data systems, as well as a new clean room and server infrastructure.

- In December 2020, Infineon Technologies launched the CIPOS Maxi IPM IM828 series. It is a 1200 V transfer molded silicon carbide (SiC) integrated power module (IPM). The series provides a compact inverter solution with thermal conduction and a wide range of switching speeds for 3-phase AC motors.

SiC-On-Insulator and Other Substrates Market Report Scope

| Report Attributes | Details |

| Market size in 2025 | USD 110.41 million |

| Market size in 2026 | USD 119.10 million |

| Revenue Forecast in 2034 | USD 226.28 million |

| CAGR | 8.3% from 2026 – 2034 |

| Base year | 2025 |

| Historical data | 2021 – 2024 |

| Forecast period | 2026 – 2034 |

| Quantitative units | Revenue in USD million and CAGR from 2026 to 2034 |

| Segments Covered | By Substrate Type, By Application, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

SiC-On-Insulator and Other Substrates Market FAQ's

The global SiC-on-insulator and other substrates market size is expected to reach USD 224.97 Billion by 2034

Key players in the market are Ceramicforum Co. Ltd., Coherent Corporation, GlobalWafers Co. Ltd., Homray Material Technology, Precision Micro-optics Inc., SICC Co. Ltd

North American contribute notably towards the global SiC-On-Insulator and Other Substrates Market

SiC-On-Insulator and Other Substrates Market exhibiting a CAGR of 8.3% during the forecast period

The SiC-On-Insulator and Other Substrates Market report covering key segments are substrate type, application, and region.

Download Sample Report of SiC-On-Insulator and Other Substrates Market

Please fill out the form to request a customized copy of the research report.