Styrene Butadiene Rubber (SBR) Market Research Report, Market share & Forecast, 2026 – 2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Styrene Butadiene Rubber (SBR) Market Summary

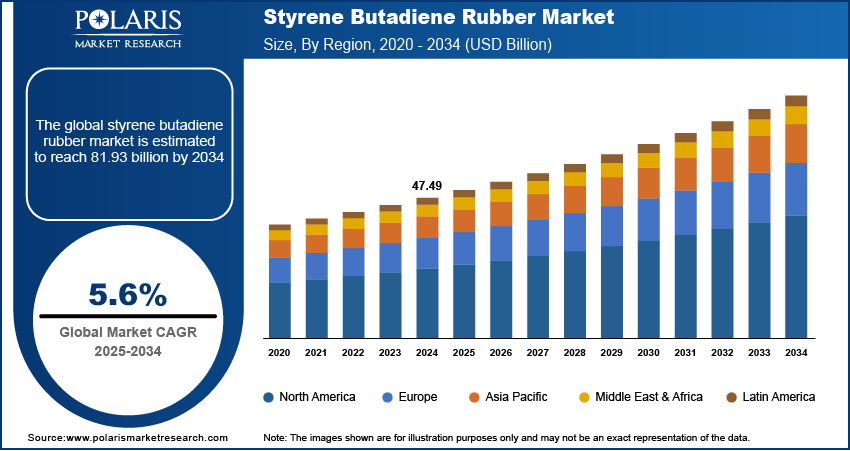

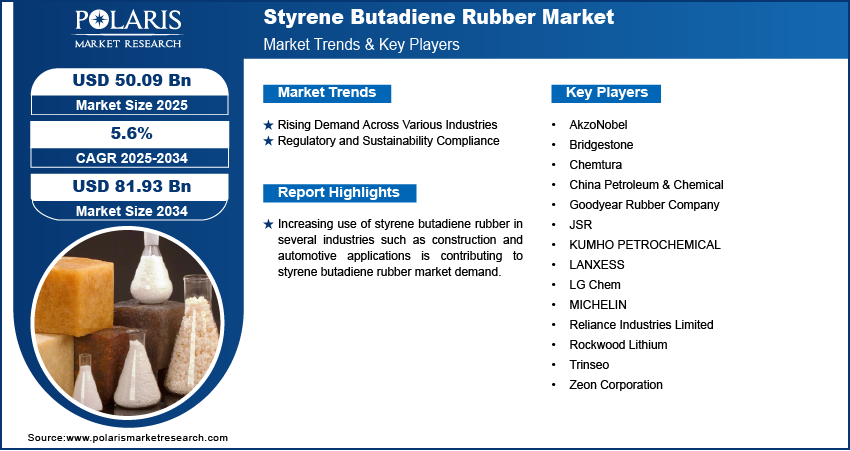

The global styrene butadiene rubber (SBR) market size was valued at USD 50.09 billion in 2025, exhibiting a CAGR of 5.6% from 2026 to 2034. The market is supported by strong automotive demand, growing use in applications such as construction and footwear, sustainability legislation, and the limited supply of natural rubber, which is driving a shift toward synthetic alternatives.

Market Statistics

Key Takeaways

- North America led the global market in 2025, with a 44.3% revenue share, supported by its robust automotive market, infrastructure development, and increasing demand for vehicles and high-performance tires.

- The U.S. held the dominating share of 81.5% in North America. The rising adoption of electric vehicles propels the requirement for high-quality SBR.

- Asia Pacific is projected to expand at the highest CAGR of 6.2%, supported by infrastructure growth, increasing consumer demand, and escalating regional investment in manufacturing.

- In 2025, the E-SBR segment dominated the market, accounting for a 69.6% revenue share, due to its superior properties and lower production costs.

- In 2025, the automotive sector led the market with 58.4% share, fueled by growth in car ownership and automobile production

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The high demand for styrene-butadiene rubber in the automotive sector is a key driver of market growth.

- The shortage of natural rubber supply is increasing demand for affordable synthetic versions, such as SBR, which have similar properties and widen market opportunities.

- Environmental pressures and increased regulations are driving growth in the SBR market as sectors shift towards more environmentally friendly and sustainable materials.

- The market is constrained by volatile raw material costs and environmental issues surrounding production.

To Understand More About this Research: Download Sample Report

What is styrene butadiene rubber (SBR)?

Styrene butadiene rubber (SBR) is made by copolymerizing styrene and butadiene to form long molecules, which are then cross-linked during vulcanization. The styrene-to-butadiene ratio can be adjusted to change the properties of the rubber. SBR is known for its abrasion resistance, aging stability, and durability. It also has good tear, crack, and electrical resistance.

Difference Between Styrene Butadiene Rubber (SBR) and Natural Rubber

SBR and natural rubber are widely used elastomers. However, they differ significantly in performance characteristics and cost structure. SBR offers superior abrasion resistance, aging stability, and lower production cost. These features make it highly suitable for automotive tires, footwear, adhesives, and industrial applications. In contrast, natural rubber provides higher elasticity, tensile strength, and resilience. These characteristics are critical for applications requiring flexibility and dynamic performance. SBR is preferred for cost-effective mass production and durability. However, natural rubber is essential in products demanding superior mechanical properties and shock absorption.

Styrene Butadiene Rubber (SBR) Vs. Natural Rubber

| Parameter | Styrene Butadiene Rubber (SBR) | Natural Rubber |

| Source | Synthetic petroleum-based rubber | Derived from latex of rubber trees |

| Cost | Lower and more cost-effective | Higher due to agricultural dependency |

| Abrasion Resistance | Excellent | Moderate |

| Elasticity & Resilience | Moderate | Very high |

| Weather & Aging Resistance | Better resistance to heat and aging | More prone to degradation |

| Tensile Strength | Good | Excellent |

| Common Applications | Tires, footwear, adhesives, conveyor belts | Gloves, medical products, heavy-duty tires |

| Production Stability | Consistent industrial production | Affected by climate and plantation output |

The high consumption of styrene butadiene rubber in the automotive industry is driving the styrene butadiene rubber market growth. SBR is used in several automotive applications, including tires, belts, automotive hoses, seals, and vibration isolators. In addition, changing consumer lifestyles, along with increased spending on modern commodity products, drive the use of SBR in other applications such as footwear, extruded rubber products, industrial hoses, and other consumer goods. Moreover, regulations and standards promoting safety, performance, and sustainability are further driving the demand for SBR.

The global demand for vehicles, especially in emerging markets, fuels the need for high-performance tires, where SBR is a crucial component. The construction industry, particularly in residential and commercial buildings, utilizes SBR for sealants and waterproofing membranes. The limited supply of natural rubber further drives the demand for synthetic alternatives like SBR. SBR offers a cost-effective alternative to natural rubber while maintaining similar properties, creating several opportunities in the styrene butadiene rubber market.

Styrene Butadiene Rubber Market Dynamics

Rising Demand Across Various Industries

The styrene butadiene rubber market growth is driven by its widespread application across multiple industries. Beyond its primary use in tire manufacturing, SBR is extensively utilized in the production of hoses, footwear, adhesives, and conveyor belts. The rapidly expanding construction industry also relies on SBR for various components, including waterproofing membranes and sealants. In addition, SBR is used in the production of medical supplies such as gloves and tubing, as well as in the modification of asphalt pavers for improved road durability. This broad range of applications underscores the material’s versatility and continues to drive the global demand for SBR.

Regulatory and Sustainability Compliance

Environmental concerns and regulatory restrictions are other major factors driving the styrene butadiene rubber market development. Governments worldwide are implementing stricter emission standards and sustainability initiatives, prompting industries to adopt eco-friendly materials. In the automotive industry, SBR is widely used in low rolling resistance automotive tires, which enhance fuel efficiency and reduce carbon emissions, aligning with global sustainability goals. Additionally, manufacturers are exploring bio-based alternatives and advanced recycling methods to comply with regulatory requirements and reduce reliance on petroleum-based raw materials.

What are the Emerging Trends in the Styrene-Butadiene Rubber (SBR) Market?

The SBR market is witnessing a rapid transition. Advancements in sustainable materials and shifting regional dynamics propel the market expansion. Tire manufacturers focus on lower rolling resistance and fuel-efficient “green tires,” especially for EVs. It drives the demand for high-performance solution-SBR. Market players are emphasizing sustainable practices due to growing interest in bio-based butadiene and rubber recycling technologies. It helps them reduce carbon footprints and meet sustainability goals.

| Trend | Short Description | Business Implications | Key Drivers |

| Shift Toward Solution-SBR (S-SBR) and Premium Grades | The use of S-SBR/functionalized SBR is rising for better wet grip, wear, and fuel efficiency | Higher-margin specialty SBR demand R&D and longer-term supply contracts with tire makers. | Rising adoption of EVs, fuel-efficiency regs, and tire performance specs. |

| Focus on Sustainability and Bio-Based Feedstocks | Development and early commercialization of bio-butadiene and bio-monomers for green SBR. | New supply chains, regulatory advantage for OEMs, and potential pricing premium. | Growing demand for green tires and bio-monomer capacity buildouts. |

| Circularity and Recycling (Rubber Reclaim/Chem Recycling) | Increasing interest in reclaimed rubber and chemical recycling to reduce the use of virgin SBR. | Opportunity for recyclers and blended grades and potential regulatory support and incentives. | Policy pressure and waste-tire circularity programs. |

| Feedstock (Butadiene) Volatility and Supply Tightness | Butadiene price and availability are key cost and supply drivers for SBR. | Requirement for feedstock hedging, flexible sourcing, and backward integration. | Petrochemical disruptions and regional capacity changes. |

| EV Tire Requirements and Lightweighting | EVs push for lower rolling resistance and thermal management propels demand for tailored SBR and SSBR blends. | Co-development with OEMs and premium product roadmaps. | Increasing adoption of EVs and OEM tire specs. |

| Rising Emphasis on Mergers and Acquisitions (M&A) and Capacity Re-allocation | Producers and chemical companies reorganize assets to focus on high-value SBR grades and secure feedstock. | Consolidation risk for smaller companies and strategic capacity investments by majors. | Announced expansions/JV deals; corporate filings. |

What are the Future Trends in the Styrene Butadiene Rubber Market?

Rising global vehicle production would drive the future growth of the SBR market. Also, the increasing demand for high-performance tires with improved durability and fuel efficiency is expected to boost the growth. The rapid electric vehicle (EV) manufacturing will accelerate the need for advanced tire materials. In addition, growing industrial applications in footwear, adhesives, conveyor belts, and construction materials would support broader market adoption. There are increasing advancements in sustainable and bio-based synthetic rubber technologies. Also, there is am increasing focus on recyclable and eco-friendly materials. These factors are expected to strengthen SBR’s position as one of the most important synthetic elastomers in the global automotive and industrial sectors.

Styrene Butadiene Rubber Market Segment Insights

Styrene Butadiene Rubber Market Evaluation by Product Insights

Based on product, the styrene butadiene rubber market is segmented into oil extended, butyl lithium, type 4, non-oil extended, emulsion SBR (E-SBR), solution SBR (S-SBR), phenyl lithium, and others. The emulsion SBR (E-SBR) segment dominated the market with a 69.6% revenue share in 2025 due to its superior properties and lower production costs. E-SBR offers good abrasion resistance and aging stability, making it suitable for various applications, especially in the automotive industry, particularly in tire manufacturing. Large-scale emulsion SBR production benefits from economies of scale, leading to further cost reductions. Additionally, the manufacturing process for E-SBR is simpler and less expensive than that of S-SBR, making it a preferred choice for manufacturers seeking cost-effectiveness.

Styrene Butadiene Rubber Market Assessment by Application Insights

The styrene butadiene rubber market, based on application, is segmented into automotive, polymer modification, catalyst for chemical reactions, footwear, and adhesives. The automotive segment dominated the market with 58.4% share in 2025, driven by rising car ownership and increased automobile production. The demand for high-performance tires has grown as more vehicles are produced and sold. SBR is widely used in tire production due to its durability, abrasion resistance, and ability to enhance grip and fuel efficiency. In addition, the shift towards fuel-efficient and long-lasting tires has made SBR a preferred material among manufacturers. Thus, the ongoing advancements in tire technology and rising demand for vehicles contribute to the segment’s leading market position.

-market-segment.webp)

Styrene Butadiene Rubber Market Regional Analysis

By region, the report provides the styrene butadiene rubber market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America dominated the global market with a 44.3% revenue share in 2025. The region's dominance can be attributed to its well-developed automotive industry, ongoing infrastructure expansion, and rising consumer demand for vehicles and high-performance tires. The growing adoption of electric vehicles, which require specialized tires and components, has further increased the need for high-quality SBR. In addition, large-scale infrastructure projects in the region drive demand for SBR in applications such as waterproofing, adhesives, and sealants. These factors collectively contribute to the region's leading position in the global market.

The Asia Pacific styrene butadiene rubber market is expected to register the highest CAGR of 6.2% during the forecast period. The region is experiencing significant growth in infrastructure projects, particularly in Southeast Asian countries, where SBR is widely used in various construction applications. The presence of a favorable regulatory environment and increased investment in SBR production capacities also drive the regional market growth. Additionally, the growing middle class and rising consumer spending in these countries are fueling demand for consumer goods such as footwear, which frequently uses SBR due to its comfortable and durable properties.

-market-region.webp)

Styrene Butadiene Rubber Market – Key Players and Competitive Insights

The styrene butadiene rubber market includes both global leaders and regional players. Leading market players are pursuing a variety of strategic activities to expand their footprint, including new product launches, acquisitions and mergers, contractual agreements, increased investments, and collaboration with other companies. Market participants are also investing heavily in R&D to broaden their product offerings, which will help the market grow even further.

Manufacturers of styrene butadiene rubber have adopted local manufacturing as a key business strategy to reduce operating costs, benefit customers, and expand the market sector. A few of the key market players are Rockwood Lithium, Chemtura, AkzoNobel, Bridgestone, MICHELIN, LANXESS, JSR, China Petroleum & Chemical, Reliance Industries Limited, LG Chem, Zeon Corporation, Trinseo, Goodyear Rubber Company, and KUMHO PETROCHEMICAL.

List of SBR Market Key Players

- AkzoNobel

- Bridgestone

- Chemtura

- China Petroleum & Chemical

- Goodyear Rubber Company

- JSR

- KUMHO PETROCHEMICAL

- LANXESS

- LG Chem

- MICHELIN

- Reliance Industries Limited

- Rockwood Lithium

- Trinseo

- Zeon Corporation

Styrene Butadiene Rubber Industry Developments

In January 2025, the European automotive industry faced significant challenges, resulting in weakened demand in the European styrene-butadiene rubber (SBR) market.

In December 2024, the automotive sector was experiencing strong growth and emerging opportunities, driven by high demand for styrene-butadiene rubber solutions. This growth indirectly benefited both the automotive and SBR markets, contributing to increased demand for SBR products.

Styrene Butadiene Rubber Market Segmentation

By Product Outlook

- Oil Extended

- Butyl Lithium

- Type 4

- Non-Oil Extended

- Emulsion SBR (E-SBR)

- Solution SBR (S-SBR)

- Phenyl Lithium

- Others

By Application Outlook

- Automotive

- Polymer Modification

- Catalyst for Chemical Reactions

- Footwear

- Adhesives

By Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Styrene Butadiene Rubber Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 50.09 billion |

| Market Size Value in 2026 | USD 53.35 billion |

| Revenue Forecast by 2034 | USD 81.93 billion |

| CAGR | 5.6% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2025 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The market size was valued at USD 50.09 billion in 2025 and is projected to grow to USD 81.93 billion by 2034

The market is projected to register a CAGR of 5.6% from 2026 to 2034.

North America accounted for the largest share of 44.3% in 2025.

Rockwood Lithium, Chemtura, AkzoNobel, Bridgestone, MICHELIN, LANXESS, JSR, China Petroleum & Chemical, Reliance Industries Limited, LG Chem, Zeon Corporation, Trinseo, Goodyear Rubber Company, and KUMHO PETROCHEMICAL are a few of the key market players.

The emulsion SBR (E-SBR) segment dominated the market in 2025 with 69.6% share.

The automotive segment held the largest share of 58.4% in 2025.

Download Sample Report of Styrene Butadiene Rubber (SBR) Market

Please fill out the form to request a customized copy of the research report.