Global Subscriber Data Management Market Size, Share Analysis Report, 2024-2032

REPORT DETAILS

Subscriber Data Management Market Summery

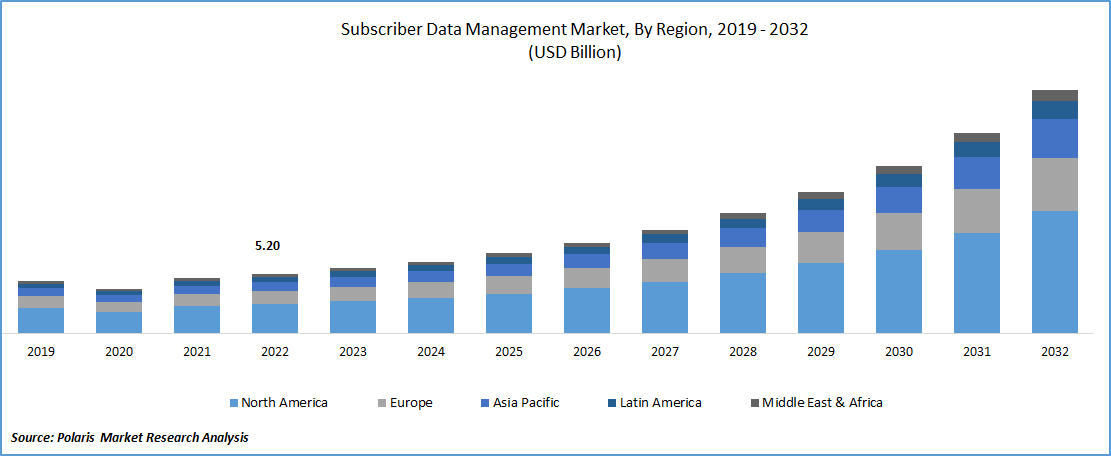

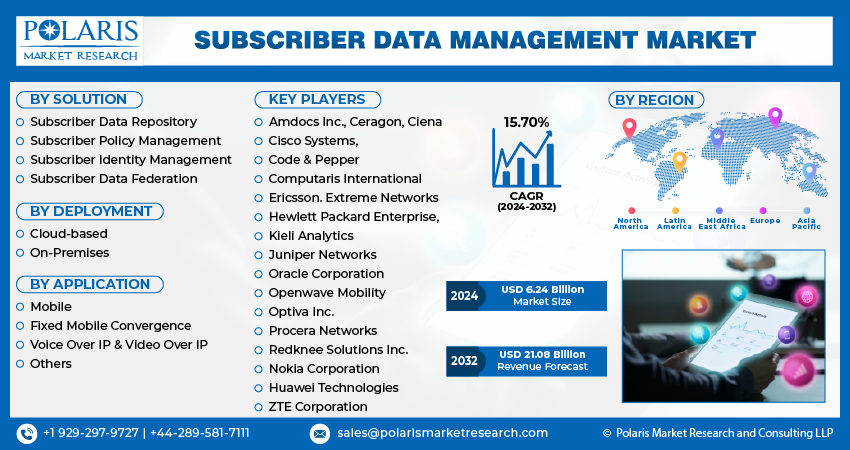

The global subscriber data management market was valued at USD 5.66 billion in 2023 and is expected to grow at a CAGR of 15.70% during the forecast period.

Market Statistics

The significant rise in the usage of mobile devices across the world and surging demand for LTE and VoLTE technologies along with the increasing adoption of these solutions among major telecom companies in order to reduce the network operational expenses and need for consolidating the user’s data, are primary factors propelling the demand and growth of the market. In addition, the growing investments on R&D activities to develop solutions with more enhanced capabilities and features and increasing number of startups entering into the market is likely to create new growth opportunities for the global market.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

For instance, in February 2023, Google Cloud, announced about the launch of its three new telecom products mainly designed to help the communication service providers. The new products include Telecom Network Automation, Telecom Data Fabric, and Telecom Subscriber Insights will provide an unified cloud solution and help CSPs to build, deploy, and operate their networks efficiently.

Moreover, the growing focus on major companies on implementing on customer experience management system to deliver exceptional experiences throughout the customer journey and to provide a holistic view of each subscriber, while enabling operators to offer personalized experiences, targeted promotions, and timely support that can improve customer satisfaction, reduce churn, and increase customer loyalty, is contributing positively towards the market growth.

The outbreak of the COVID-19 pandemic has had both positive and negative impact on the growth of the subscriber data management market. The rapid emergence of deadly coronavirus led to significant increase in data usage, as a greater number of people were relied on digital services for their work, education, communication, and entertainment. However, the pandemic presented challenges in terms of implementing and upgrading these systems due to travel restrictions, lockdown measures, and supply chain disruptions.

Industry Dynamics

Growth Drivers

Increasing demand for consolidating subscriber data is propelling the market growth

Increasing need and demand for consolidating subscriber data which is a core asset for operators nowadays, surging adoption of cloud-based models among large number of major organizations, and rising penetration for improving the productivity and efficiency of organizations through deploying several types of advanced technologies and solutions, are among the major factors fostering the market growth at rapid pace.

Furthermore, the rapid deployment of 5G networks which offers increased bandwidth, lower latency, and higher connection density, leading to a massive influx of data and rising penetration for incorporating advanced technologies like AI and ML, allowing subscriber data management solutions to help service providers to effectively handle the vast amounts of data generated by IoT devices, while ensuring seamless superior customer experiences and uninterrupted connectivity, has been creating lucrative growth opportunities for market.

Source: Polaris Market Research Analysis

Report Segmentation

The market is primarily segmented based on solution, deployment, application, and region.

| By Solution | By Deployment | By Application | By Region |

|

|

|

|

Source: Polaris Market Research Analysis

To Understand the Scope of this Report: Request Customization

By Solution Analysis

Subscriber data repository segment accounted for the largest market share in 2022

The subscriber data repository segment held global share in 2022, on account of growing proliferation of mobile devices and significant adoption of fast internet services across the globe, which results in increased data generated by users. Additionally, the rising customer preference for personalized services specially tailored to their specific needs and requirements and enhancements in data repository solutions allowing service providers to capture and analyze data more efficiently, are also likely to boost the segment market growth.

The subscriber data federation segment is expected to grow at highest growth rate over the next coming years, mainly attributable to its ability to enable the consolidation and centralization of subscriber data from multiple sources such as different network domains or service providers and it also allows for efficient management and utilization of subscriber data. The growing prevalence for the transition towards virtualized network functions and cloud-based architectures creates huge demand for efficient subscriber data federation solutions, as these solutions supports the seamless integration and orchestration of subscriber data across virtualized environments, which in turn, likely to propel the market at rapid pace.

By Deployment Analysis

Cloud-based segment held the significant market share in 2022

The cloud-based segment held the maximum market share in terms of revenue in 2022, which is mainly driven by its numerous advanced and beneficial characteristics including providing advanced security measures to protect subscriber data and real-time data access and analysis. In addition, cloud-based solutions eliminate the need for upfront investments in hardware and infrastructure, reduces capital expenditure, and allow service providers to leverage the pay-as-you-go model, which makes it more cost-effective compared to on-premises solutions, thereby gaining significant popularity across the world.

The growing developments in cloud-based solutions enabling them to easily integrate with other cloud-based services and platforms such as customer relationship management systems, marketing automation tools, and analytics platforms that results in seamless data flow and enhanced overall operational efficiency, is likely to have a positive impact on the market growth.

By Application Analysis

Mobile segment is expected to witness highest growth during forecast period

The mobile segment is projected to witness highest growth rate of over XX% during the anticipated period, mainly due to continuous expansion of mobile subscriber base across the globe because of the surging adoption of smartphones, enhanced network coverage, and declining data tariffs along with the significant increase in data traffic and consumption that led to higher demand for advanced subscriber data management solutions.

The rising evolution of mobile networks particularly the deployment of 5G technology and its future advancements, has been creating a significant demand for subscriber data management solutions, as it helps operators manage the complexity of 5G networks including network slicing, virtualization, and diverse service offerings, are pushing the market growth forward over the years.

For instance, according to a report published in 2023, the number of mobile subscriptions reported across the globe was around 8.6 billion in 2022 with an increase of 0.2 billion from 2021 and the number of mobile subscriptions has now surpassed the global population with 7.9 billion people. Also, the 5G mobile subscriptions is anticipated to exceed 4.3 billion by the end of 2027.

Source: Polaris Market Research Analysis

Regional Insights

North America region dominated the global market in 2022

North America held the largest share, mainly attributable to quick and early adoption of advanced technologies, rising investments of research & development activitie, and robust presence of major market players especially in developed countries like US & Canada. The rising deployment of 5G networks which require dynamic management of subscriber profiles, real-time authentication, and seamless handover between network slices, is propelling the adoption and need for these SDM solutions due to their abilities to address these needs.

The Asia Pacific region is anticipated to be the fastest growing region with a healthy CAGR over the study period, owing to significant expansion and modernization of telecommunication infrastructure, growing internet connectivity, increasing data usage, and proliferation for personalized services. Moreover, the APAC region has been witnessing exponential growth in the adoption of internet of things devices and connected technologies across industries that generate substantial amounts of data that need to be managed efficiently, thereby the need for SDM solutions has emerged significantly.

Source: Polaris Market Research Analysis

Key Market Players & Competitive Insights

The subscriber data management market is competitive and is anticipated to witness competition owing to several players' presence. Major service providers in the market are constantly upgrading their technologies to stay ahead of the competition and to ensure efficiency, integrity, and safety. These players focus on partnership, product upgrades, and collaboration to gain a competitive edge over their peers and capture a significant market share.

Some of the major players operating in the global market include

- Amdocs Inc.

- Ceragon

- Ciena

- Cisco Systems

- Code & Pepper

- Computaris International

- Ericsson

- Extreme Networks

- Hewlett Packard Enterprise,

- Kieli Analytics

- Juniper Networks

- Oracle Corporation

- Openwave Mobility

- Optiva Inc.

- Procera Networks

- Redknee Solutions Inc.

- Nokia Corporation

- Huawei Technologies

- ZTE Corporation

Recent Developments

- In June 2025, Ericsson and Google Cloud launched Ericsson On-Demand, a SaaS-based 5G core designed to deliver elastic scalability and a pay-per-use pricing model for network functions.

- In March 2025, Vodafone Spain chose Ericsson’s standalone 5G core to support its consumer services as part of a multi-year agreement.

- In June 2024, X introduced Advanced Analytics for Premium users, making detailed insights such as impressions, engagement, and profile activity available only through a subscription.

- In February 2024, Alepo and Italtel partnered to deliver end-to-end private 5G solutions by combining SDM, policy control, and cloud-native 4G–5G core technologies.

Subscriber Data Management Market Report Scope

| Report Attributes | Details |

| Market size value in 2024 | USD 6.24 billion |

| Revenue forecast in 2032 | USD 21.08 billion |

| CAGR | 15.70% from 2024 – 2032 |

| Base year | 2023 |

| Historical data | 2019 – 2022 |

| Forecast period | 2024 – 2032 |

| Quantitative units | Revenue in USD billion and CAGR from 2024 to 2032 |

| Segments covered | By Solution, By Deployment, By Application, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

| Key companies | Packard Enterprise, Oracle Corporation, Computaris International, Procera Networks Inc., Openwave Mobility Inc., Redknee Solutions Inc., Extreme Networks, Kieli Analytics, Nokia Corporation, Cisco Systems, Huawei Technologies, Ericsson, ZTE Corporation, Juniper Networks, Code & Pepper, Ceragon, Ciena, Amdocs Inc., and Optiva Inc. |

Source: Polaris Market Research Analysis

subscriber data management market FAQ's

The global subscriber data management market size is expected to reach USD 21.08 billion by 2032.

Key market players in the market Amdocs Inc.,Ceragon,Ciena,Cisco Systems,Code & Pepper,Computaris International,Ericsson.

North America region contribute notably towards the global Subscriber Data Management Market

The global subscriber data management market is expected to grow at a CAGR of 15.7% during the forecast period.

Key segments in the Subscriber Data Management Market solution, deployment, application, and region.

The growth is driven by rising mobile device usage, surging demand for LTE and VoLTE technologies, increasing adoption of SDM solutions among telecom companies, and rapid deployment of 5G networks generating massive volumes of subscriber data.

The subscriber data repository segment held the largest market share, driven by the growing proliferation of mobile devices and rising customer preference for personalized services.

Download Sample Report of subscriber data management market

Please fill out the form to request a customized copy of the research report.